SPXSY - Spirax-Sarco: High Quality Industrial With Secular And Recurring Opportunity

2023-06-28 23:35:29 ET

Summary

- Spirax-Sarco is an LSE-listed industrial conglomerate that holds leadership positions over their niche markets.

- Although financials are of safe quality, the more nimble size of the company also suits long-minded investors.

- I expect returns to rival companies who are more often the first choice for investors.

- Whether replacing those rivals with a more aggressive allocation or merely diversifying into Spirax-Sarco, the outlook is positive.

Introduction

Spirax-Sarco ( OTCPK:SPXSY ) is a leading producer of steam and fluid management systems worldwide thanks to a history dating back over 100 years. The company is now split into three revenue bases: Steam Specialties, Watson Marlow, and a new Electric Thermal Solutions segment. Current and historical financial performance is strong due to factors such as providing essential technologies and services to defensive industries such as healthcare and food & drink, a high proportion of recurring and service oriented revenues, and a collaborative spirit driving value-creation alongside clients. As such, the company has matured into a quality, rather than speculative investment, and deserves consideration by a wide range of investors.

Quality company in a small package

As summarized in the image below, despite only having ~$1.5 billion in annual revenues, Spirax-Sarco generates significant profits, provides a rising and sustainable dividend, and still grows at a rapid clip. I expect this pattern to continue thanks to the strength of their client industries. As I will point out later in this article, the company offers both quality and opportunity for growth as compared to peers. While I personally do not worry about the short-term share price implications of an impending recession, or lack thereof, I will point out that Spirax-Sarco’s biggest risk is their slightly high valuation when compared to peers. But I do also believe in the opportunity available and that recurring investments will continue to outperform trading this name.

Spirax-Sarco Website

Firstly, the strong subsidiary Watson Marlow is one of the premier providers of peristaltic pumps, devices that require significant amounts of customized engineering and quality assurance, along with generally providing essential operations for clients. Examples include pumps for bioprocessing- the sterile and impurity-free manufacturing of extremely sensitive and complex therapeutics-and one of their key customers is the leading provider Thermo Fisher ( TMO ). Listed below are summaries of the TMO technology integration , along with summaries of all the major industry services that Watson Marlow provides .

Watson-Marlow Presentation

Thermo Fisher

Considering opportunities in the rapidly growing biopharma, mining, chemical, and environmental services industries, Watson Marlow also benefits from diverse secular growth opportunities, and provides the most revenue growth for Spirax-Sarco. However, a new TargetZero initiative is attempting to rediscover growth opportunities in the slower moving Steam Specialties group. The basis of growth is through the provision of heat capture and energy generation services alongside and integrated with the company’s normal steam systems.

As we all know, industry is a major contributor towards carbon emissions, and the new solutions are merely ways to increase current energy consumption efficiency, generate renewable electricity, and be economically sensitive at the same time. Over the next few years, I expect Spirax-Sarco to maintain their above market revenue growth, ~7-10%, thanks to these opportunities. But, as I will highlight later, profitability may become an issue with these new services.

Spirax-Sarco Investor Presentation 2023

Future proofing with both secular and consistent growth opportunities

As I am an investor who prefers gradually accumulating only the best long-term investments, I have searched the market for companies that offer innovation and essentiality. Often referred to as a high barrier to entry, or moat, the industrial industry has many hidden assets that offer these qualities. However, not all moats reflect positively financially, and innovation or risk-taking are also factors I look for as momentum drivers. As discussed, Spirax-Sarco has numerous leadership positions thanks to both the Steam Solutions and Watson Marlow, but also identifies new secular opportunities to maintain momentum. One way to see this process working sustainably is by looking at the breakdown of sales by type.

The presentation slide below does a great job indicating the positive feedback loop that is in place. First, approximately 15% of annual sales are from large scale customer Capex spending in which the two groups work together to develop and deploy new systems. Then, after these major systems are operational, 45% of all revenues are related to maintenance and repair of existing systems. Essentially, recurring revenues that grow with the Capex-generated installations. Then, another 40% of revenues are based on less volatile Opex spending, typically for upgrades or bolt-on improvements to existing systems. This helps to increase recurring maintenance revenues and offset any economic weakness that may reduce Capex spending on large projects.

Spirax-Sarco’s business model has allowed for a resilient growth profile, with long-term growth averaging over 8% annually. Cyclicality has also not been a significant issue, although the Steam Solutions segment’s growth is slower overall. This is now offset in 2023 with Watson Marlow now approaching a majority share of revenues due to higher growth, and will likely carry Spirax-Sarco for the years to come. We also see the effects of the bolt-on acquisition strategy underpinning organic growth opportunities with the new Electric Thermal Solutions segment’s rapid growth. However, analysts are only expecting growth to be in the mid-% range, with 2024 revenues only reaching $2.38 billion on average. This suggests weakness in the industrial market, but I believe this is only a short-term issue.

Spirax-Sarco Investor Presentation 2023

Spirax-Sarco Investor Presentation 2023

Organic earnings growth facing slight headwinds

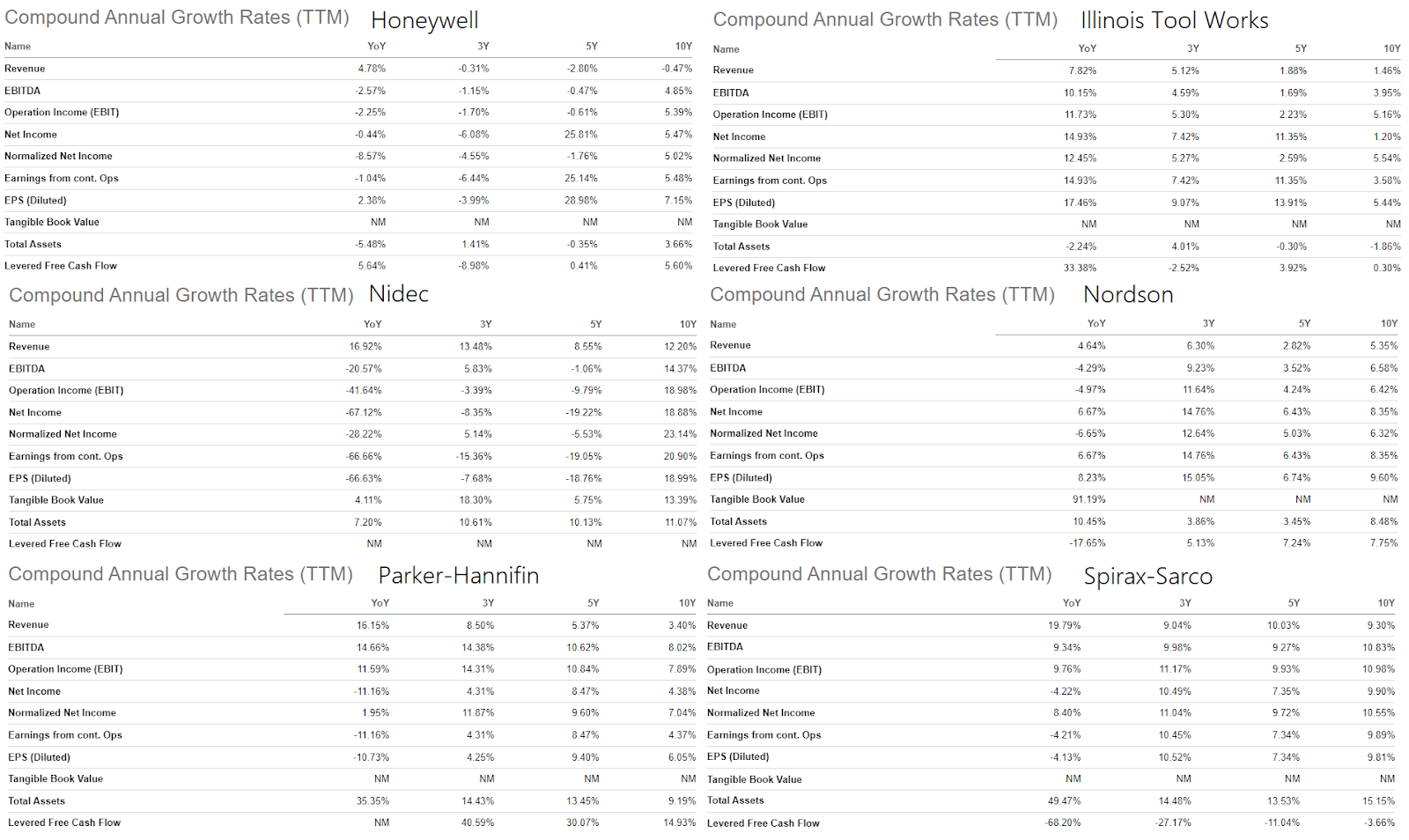

With growth risk ahead, it is also important to assess profit generation and the financial foundation of Spirax-Sarco. As shown in the table below, over the past 10 years, the company has generally raised earnings at a faster rate than revenues. However, the past few quarters have seen a decline in profitability, ending a nearly two decade long streak of margin improvement. We have heard frequent discussion of supply chain and raw material pricing issues, but there may be some issues relating to the profitability of the new ETS segment (either through increased investment or lower margin sales). Therefore, to be truly comfortable with the holding, I will be watching for maintained or rising profit margins moving forward. This will be reflected as a staircase pattern of rising CAGR growth rates from revenue all the way to EPS.

The CAGR data for Spirax-Sarco. (Seeking Alpha)

The historical quarterly EBITDA and Net Income of Spirax-Sarco, with margins. (Koyfin)

{kind=link}

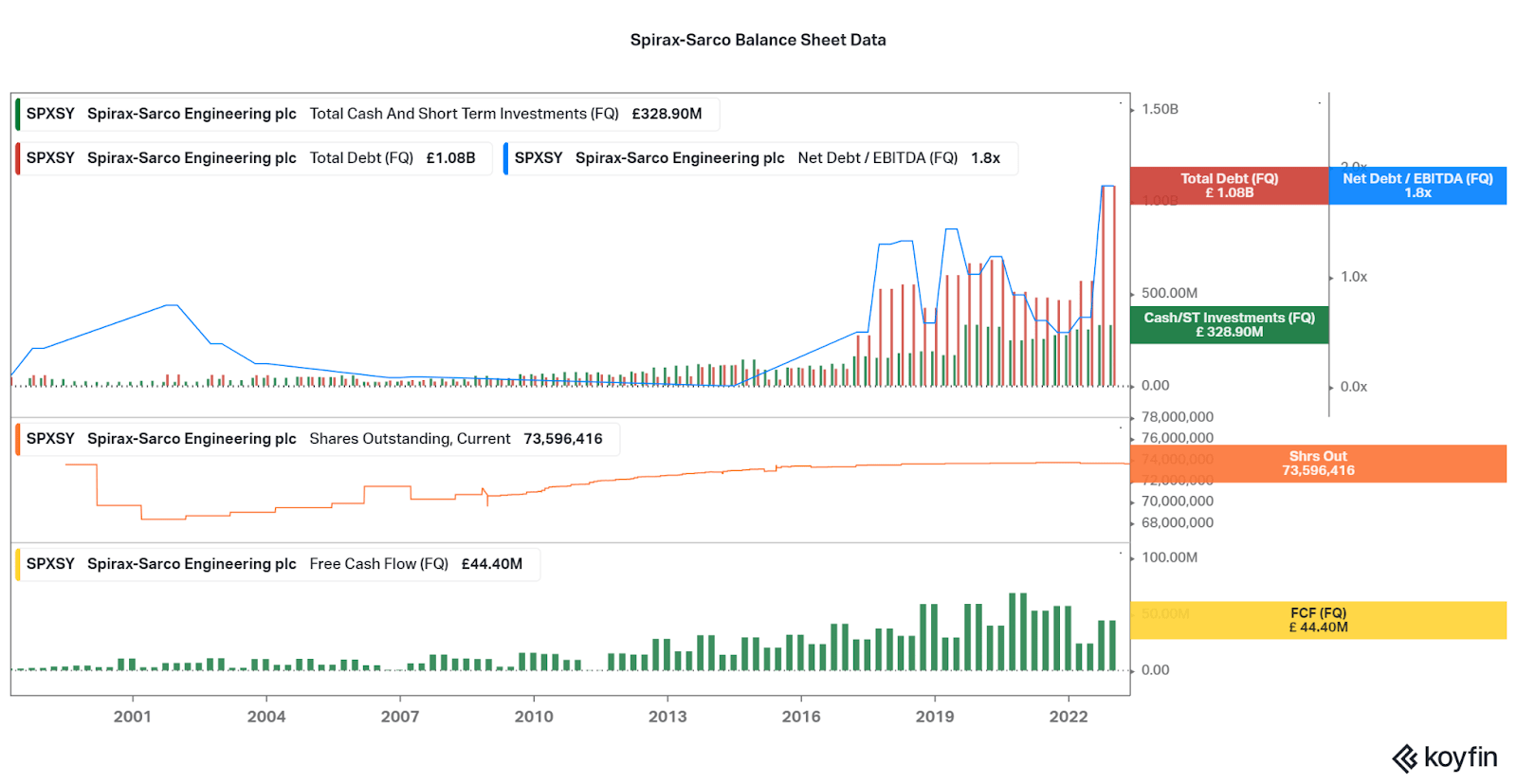

Maturing balance sheet, still conservative

Spirax-Sarco has traditionally been very conservative with issuing debt, but dilution was the replacement source of funding. Now, dilution has ceased but leverage is rising. The current £1.1 billion in debt has caused leverage to rise close to 2.0x EBITDA, but remains at a manageable level when compared to peers (all relevant peers discussed below normally range from 1.0x-2.0x). Any increased EBITDA generation or payback of debt will reduce significant risk from this level, so I am not worried at the moment. Spirax-Sarco has also been very careful in generating continually rising cash flows, and so there is plenty of spare cash around each quarter to continue supporting shareholders and operations.

The balance sheet data of Spirax-Sarco (Debt, Cash, Leverage, Dilution, and FCF). (Koyfin)

{kind=link}

Despite recent profit weakness, SPSXY outperforms

So while Spirax-Sarco may be a strong company, there are many other choices within the industry. Does Spirax-Sarco stand up to top peers, especially considering it is an OTC equity for US investors. The easiest way to easily highlight the way SPSXY stands out is with CAGR data. When compared to top industrial equipment and solutions equities such as Honeywell ( HON ), Illinois Tool Works ( ITW ), Nidec ( OTCPK:NJDCY ), Nordson ( NDSN ), and Parker-Hannifin ( PH ), it is clear that Spirax-Sarco is superior in growth.

Combined with the fact that profitability remains strong as well, the data suggests that Spirax-Sarco will continue to rise into the size and quality of these peers in time. However, when incorporating factors like earnings volatility and safety levels, the growth outperformance will be hindered and this may allow Spirax-Sarco to perform in-line with these peers. I expect nimble investors to gain trading advantages playing volatility, but for hands-off investors, you will need to think about your personal risk tolerance. Since all of these companies are worthwhile in my eyes, there are no right or wrong choices.

The long-term CAGR data for Honeywell, Illinois Tool Works, Nidec, Nordson, Parker-Hannifin, and Spirax-Sarco. (Seeking Alpha. Compiled by Author)

{kind=link}

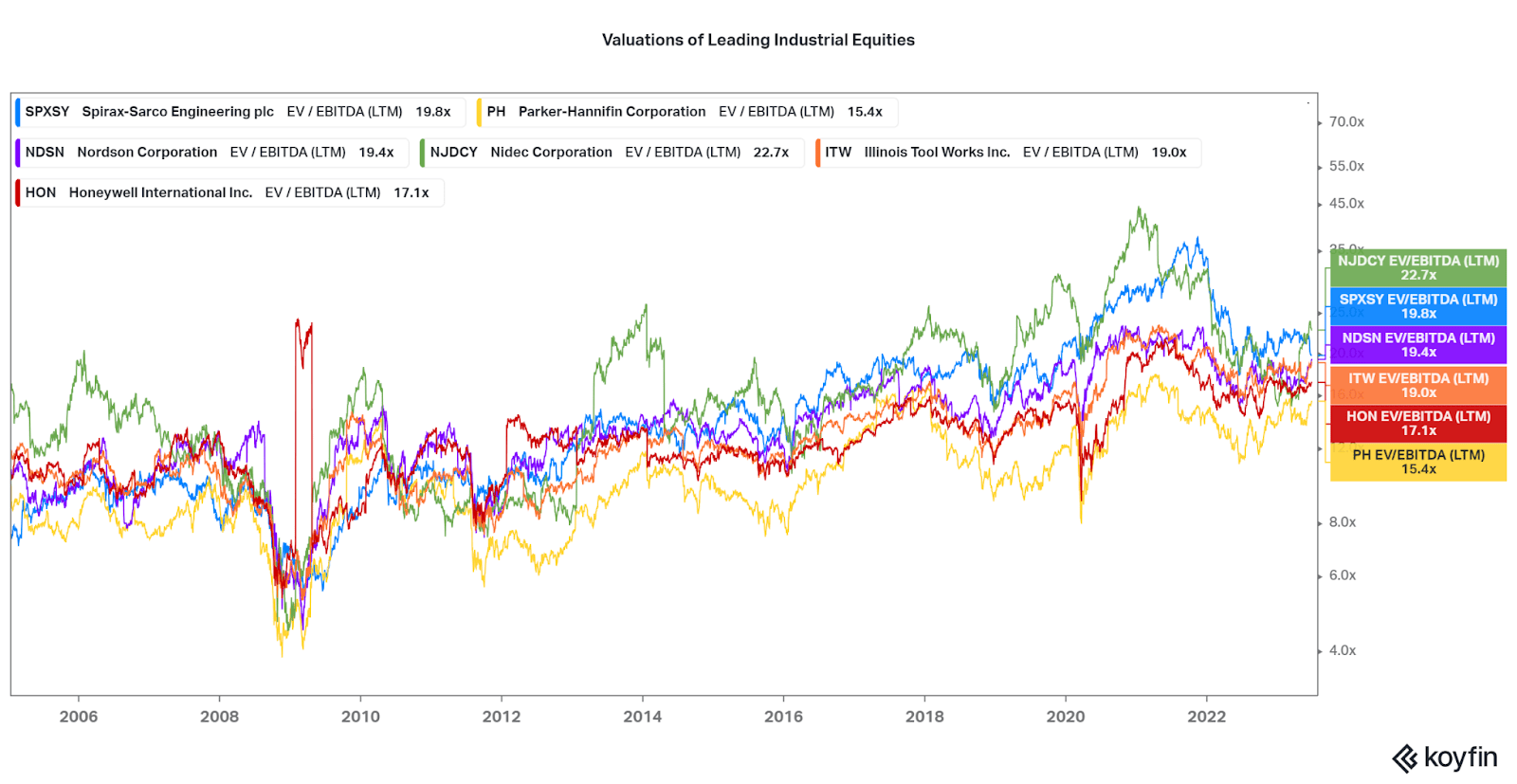

Valuation is favorable

But as always, the single factor of valuation will weigh heavily in investors’ minds. Reflecting growth rates almost perfectly, Spirax-Sarco is the second most expensive holding of the group. However, this has almost always been the case due to superior growth opportunities. With those remaining, and earnings current facing headwinds, I expect that the current valuation is actually favorable for investors. When a.) earnings increase over the next few quarters, and b.) top-line growth remains, the share price will have nowhere to move but up. Therefore, I would keep the current valuation in mind and if Spirax-Sarco continues to perform well financially, but the valuation falls below peers, then it is an opportune time to take advantage and load up on shares.

The EV/EBITDA (LTM) data of industrial company peers. (Koyfin)

{kind=link}

Conclusion

Advantageous investments often occur when a company is a small size, and investors are able to compound over many years. However, selecting quality early on is difficult so it is important to diversify. For those with interest in industrials, particularly those with unique exposure to secular growth trends, this is especially true as many of these equities come with significant risk. Spirax-Sarco is one of a few assets that are on the cusp of rising from a more aggressive nature to a more quality and secure nature. There is still plenty of opportunity for growth oriented investors, but quality also limits the downside. And, when compared to peers, Spirax-Sarco stands out. I believe they are worth consideration, and I would recommend those interested to steadily accumulate shares over the years to come.

Thanks for reading. Feel free to share your thoughts below.

For further details see:

Spirax-Sarco: High Quality Industrial With Secular And Recurring Opportunity