AVNS - STAAR Surgical Company: The Stock Is Still An Eyesore

2023-08-11 06:22:38 ET

Summary

- STAAR Surgical Company's revenue continues to grow, but its bottom line financial performance has been disappointing.

- The stock is trading at a very high price, making it overpriced compared to similar firms.

- More likely than not, the stock should fall further, even after tumbling for the past year and a half.

One of the biggest mistakes that investors can make is buying a company that continues to grow, but that is trading at a very high price. A great example of this that I could point to is STAAR Surgical Company ( STAA ), an enterprise that produces implantable lenses for the eye, as well as delivery systems that are used to deliver those lenses to the eye. It also produces other products as well, such as intraocular lenses and silicone lens-based preloaded injectors. Management continues to grow revenue for the company nicely, and that trend does not seem to be stopping today. Having said that, bottom line financial performance as of late has been disappointing. Add on top of this the fact that shares look very pricey, especially on a forward basis, and I would argue that the stock likely deserves further downside from what it has already experienced over the past several months.

Taking a good look

Back in the middle of February 2022, I ended up writing an article about STAAR Surgical that painted the company in a rather bearish light. At the time, revenue growth for the business was looking positive. In the long run, I felt as though further growth was almost guaranteed. But I could not get past just how expensive the stock was. In fact, I even went so far as to describe the company as being 'drastically overpriced'. That led me to rate the company a 'sell' to reflect my view at the time that shares should significantly underperform the broader market for the foreseeable future. Since then, nine other articles have been written by other analysts about the business, none of them taking as negative a stance as I have. But so far, my call has been on the nose. Since the publication of the article, the stock is down 37.7%. That compares to the 1.4% increase that the S&P 500 saw.

{kind=link}

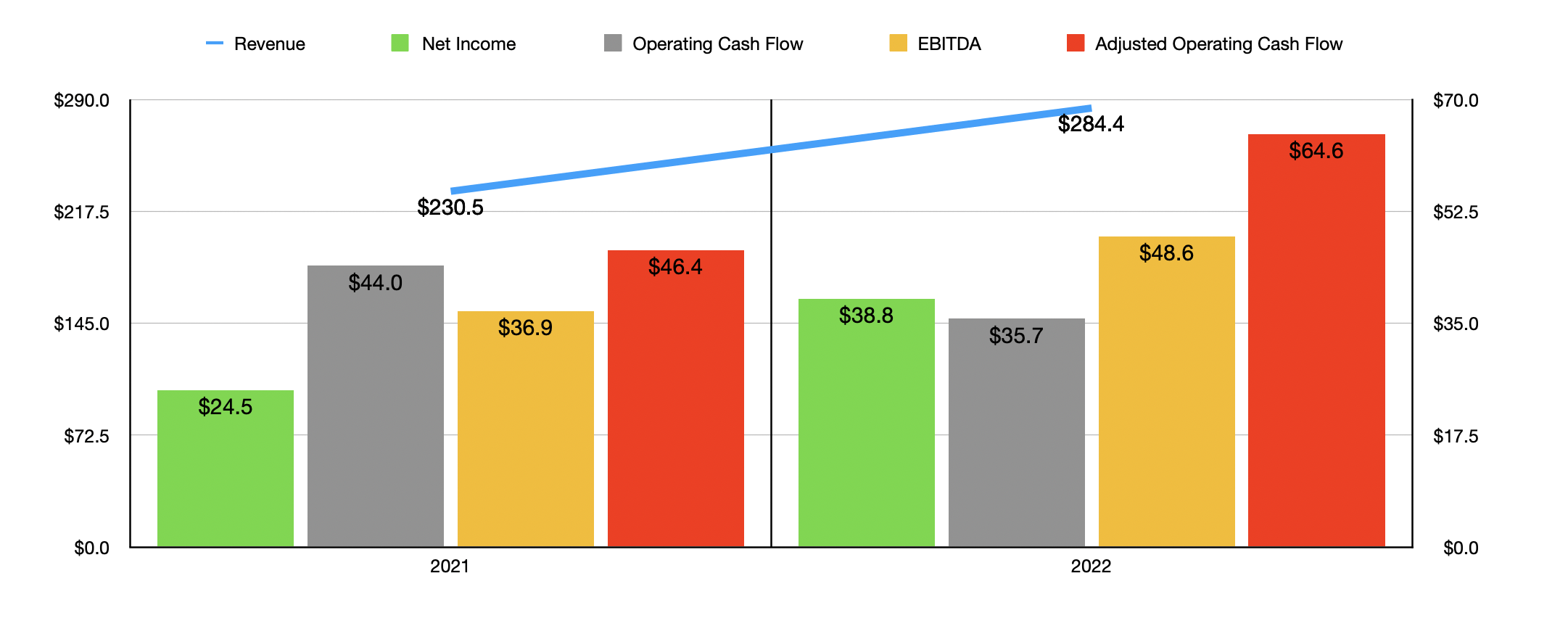

If we look only at the annual data provided by management, you might be perplexed as to why shares took such a tumble. Consider 2022 compared to 2021 . As you can see in the chart above, revenue last year totaled $284.4 million. That's 23.4% higher than the $230.5 million the company reported one year earlier. Most of the company's product lines actually experienced downside during that time. But its primary product, the Implantable Collamer lens, or ICL, saw revenue spike $56.8 million year over year. That's more than the $53.9 million in sales that the company saw in the form of growth in 2022 compared to 2021. This increase, amounting to roughly 27%, was driven by a 33% rise in unit count. Most of that growth, management said, came from the Asia Pacific region, with distributors there demanding 43% more of the company's products. In China, growth was 38%, while in India it was 37%. Interestingly, growth would have been higher had it not been for foreign currency fluctuations. They impacted sales negatively by $12.9 million.

On the bottom line, the picture also improved. Net income jumped 58.4% from $24.5 million to $38.8 million. It is true that operating cash flow fell from $44 million to $35.7 million. But if we adjust for changes in working capital, we would actually see that number grow from $46.4 million to $64.6 million. And finally, EBITDA for the company jumped from $36.9 million to $48.6 million.

{kind=link}

Where the picture for the company starts to look worse is when it comes to the 2023 fiscal year. As you can see in the chart above, revenue for the company continued to increase year over year for the first two quarters , climbing 14.9% from $144.3 million to $165.8 million. Again, ICL sales led the way, with sales growth of 19% there, led by a 26% increase in the Asia Pacific region. But what the chart also shows is that profits and cash flows decreased significantly for the company year over year. Part of this problem was a drop in the company's gross profit margin from 78.4% of sales to 77.4%. That was largely the result of reserves that the company had to put into place for cataract IOLs.

Even more problematic was a jump in general and administrative costs from 18% of sales to 21.8%. That alone resulted in an additional $10.3 million in expense for the company on a pre-tax basis. Management attributed this to hire bonuses, stock-based compensation expenses, and other related payroll items. There were other painful items as well. The one that had the largest negative impact was the selling and marketing expense category. This shot up from 28.8% of revenue to 35.4% because of the same payroll related items, as well as because of higher sales commission costs, trade show and sales meeting expenses, and increased advertising and promotional activities. Even though this is an investment by the company in its growth, it is disconcerting that they had to increase these costs so much in order to keep revenue climbing. Finally, R&D costs also rose, growing from 11.4% of sales to 13.3%. Just like the other items, this was largely the result of higher payroll related expenses. But clinical trials also played a role in this.

{kind=link}

What we have here is a company that is continuing to grow its revenue. However, it is having to spend far more money on payroll costs, marketing, and other activities, in order to achieve it. If we were to annualize the financial results reported for the first half of the year, we would get net income of $15.1 million, adjusted operating cash flow of $49.4 million, and EBITDA of $21.9 million. Using these figures, you can see how expensive the stock is on a forward basis in the chart above. But even if we use the more attractive 2022 results, the stock still looks expensive. In the table below, I also compared STAAR Surgical to five similar firms. Even using the 2022 figures, four of the five firms ended up being cheaper than our prospect when it comes to the price to earnings approach and the EV to EBITDA approach. Shares only become reasonably priced when looking through the lens of the price to operating cash flow multiple. In this case, two of the five companies were cheaper than it.

| Company |

| Price / Earnings |

| Price / Operating Cash Flow |

| EV / EBITDA |

| STAAR Surgical Company |

| 58.2 |

| 35.0 |

| 42.6 |

| UFP Technologies ( UFPT ) |

| 29.6 |

| 61.1 |

| 19.6 |

| Embecta Corp ( EMBC ) |

| 13.2 |

| 8.9 |

| 9.9 |

| Avanos Medical ( AVNS ) |

| 26.6 |

| 14.0 |

| 10.7 |

| Neogen Corporation ( NEOG ) |

| 442.2 |

| 54.5 |

| 51.5 |

| Merit Medical Systems ( MMSI ) |

| 46.0 |

| 43.7 |

| 21.8 |

Takeaway

Based on the results so far, I must say that I am still rather bearish regarding STAAR Surgical. Yes, I know that shares have fallen significantly at a time when the broader market has inched up. But trading multiples, even under a very generous hypothetical scenario where we assume financial performance reverts back to what it was last year, still looks high. This is true both on an absolute basis and relative to similar firms. Given these factors, I've decided to keep the company rated a 'sell' for now, though if it drops another 10% or 20%, I could upgrade it slightly.

For further details see:

STAAR Surgical Company: The Stock Is Still An Eyesore