SCBFY - Standard Chartered: A Rising Tide Lifts All Boats

2023-09-29 22:08:21 ET

Summary

- Standard Chartered has struggled for years to generate meaningful profitability, but the advent of higher interest rates has given it a major boost.

- Near-term earnings and profitability will be more subdued, and 2024 targets of an 11% return on tangible equity will need a bit of cooperation from the macroenvironment.

- My main concern is that this bank looks more exposed than some peers, should a downturn turn out more severe than anticipated.

- Nevertheless, at 0.7x tangible book value these shares still look on the cheap side.

It's said that a rising tide lifts all boats, and nowhere is that expression more apt than at Standard Chartered ( SCBFY ) ( SCBFF ). This London-listed, but mainly Asia-focused bank has had major issues with compliance and risk controls in years past, ultimately resulting in dilutive capital raises, lackluster profitability and poor shareholder returns throughout the latter part of the 2010s.

{kind=link}

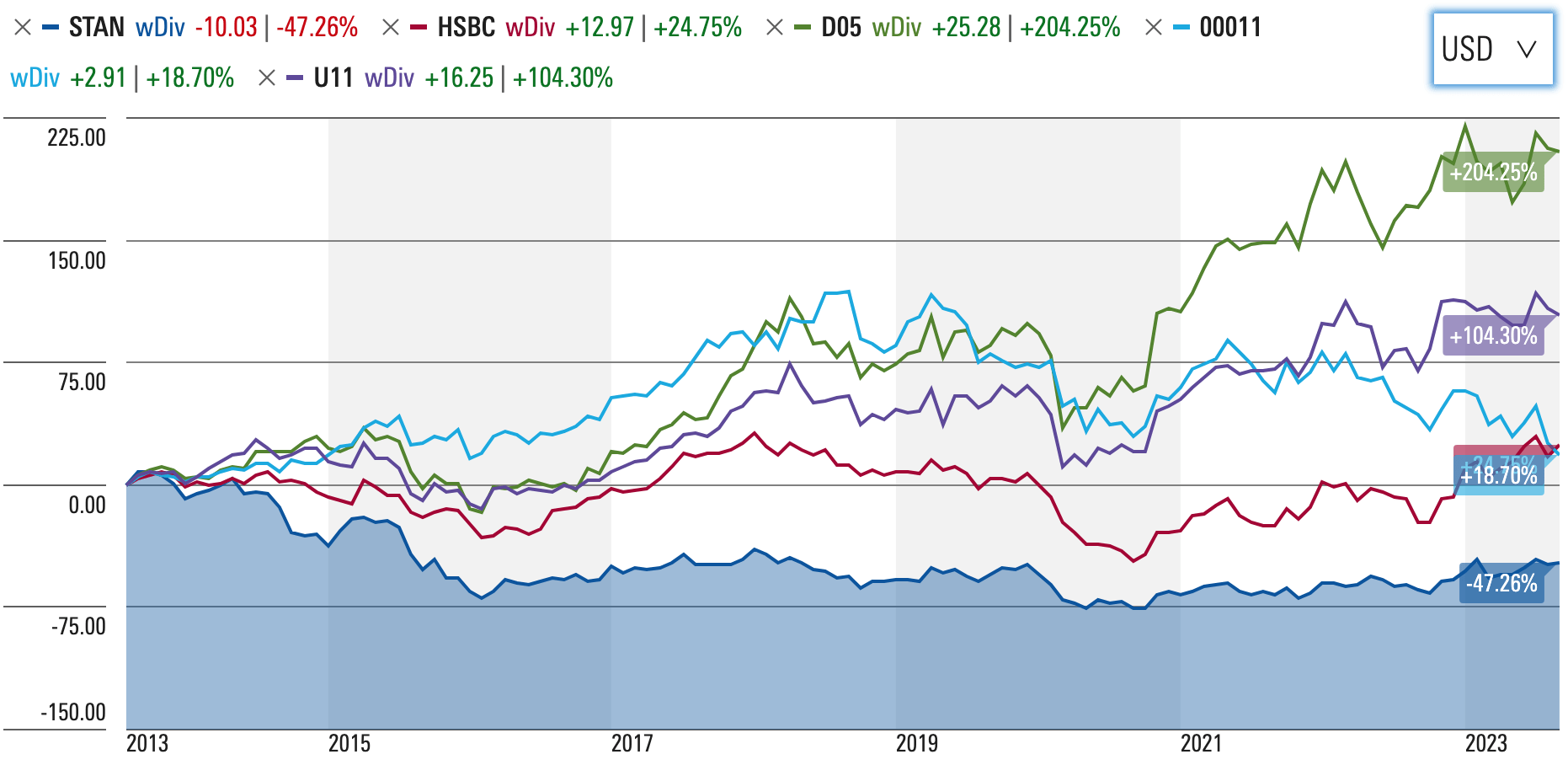

While the above means that these shares have materially underperformed the more obvious names for folks looking for Asian bank exposure, such as HSBC ( HSBC ), Hang Seng ( HSNGY ) and the 'big three' Singapore banks, higher interest rates are indeed a rising tide right now, helping to lift net interest income and profitability to just about an acceptable level.

My main concern is a worse than expected slowdown heading into H2 2023 and 2024, and that could leave the bank more exposed compared to peers like DBS Group ( DBSDY ) ( DBSDF ). Even so, at 0.7x tangible book value I think you could argue for some undervaluation here given management's profitability targets, and while that makes the shares just about a buy in my book, this one is a riskier proposition than some of its regional peers.

A Rising Tide From Higher Interest Rates

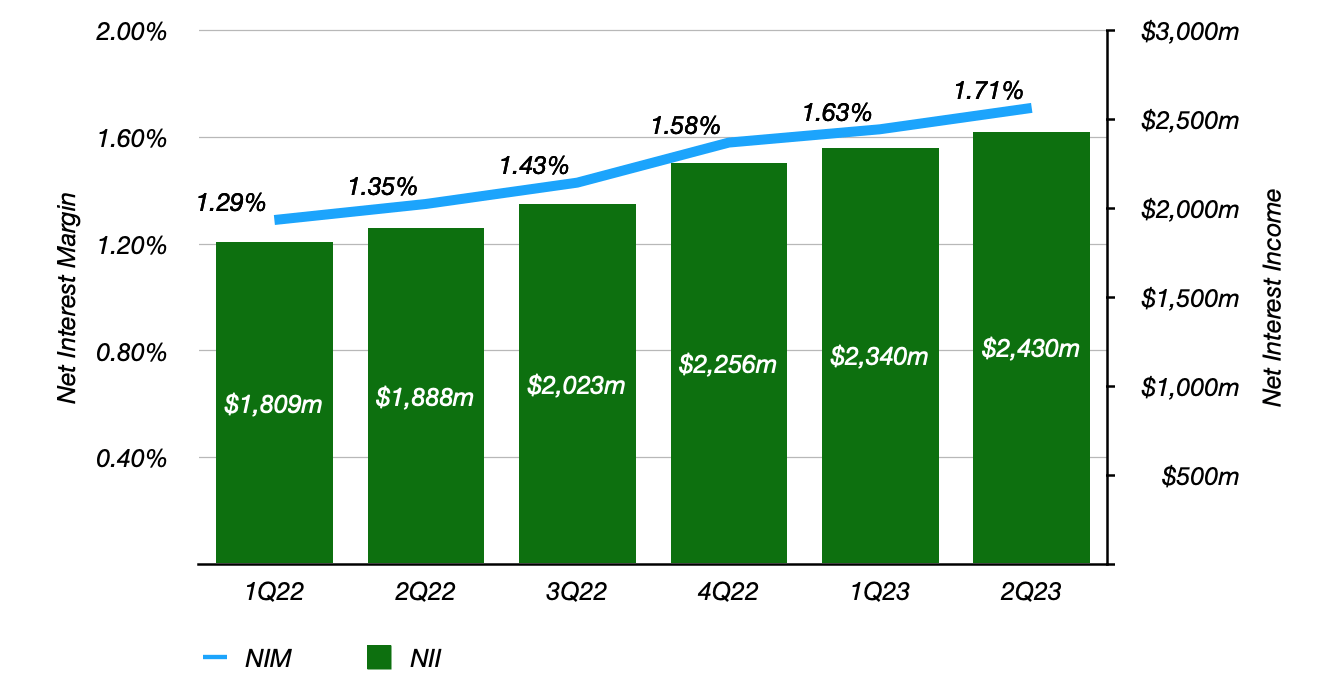

Even with significant non-interest income lines (wealth management, trading income and so on), net interest income ("NII") still accounts for around 53% of Standard Chartered's revenue. With rates having risen at their steepest rate in years, the bank has been on the receiving end of a much needed boost:

Standard Chartered: Quarterly NII and NIM

{kind=link}

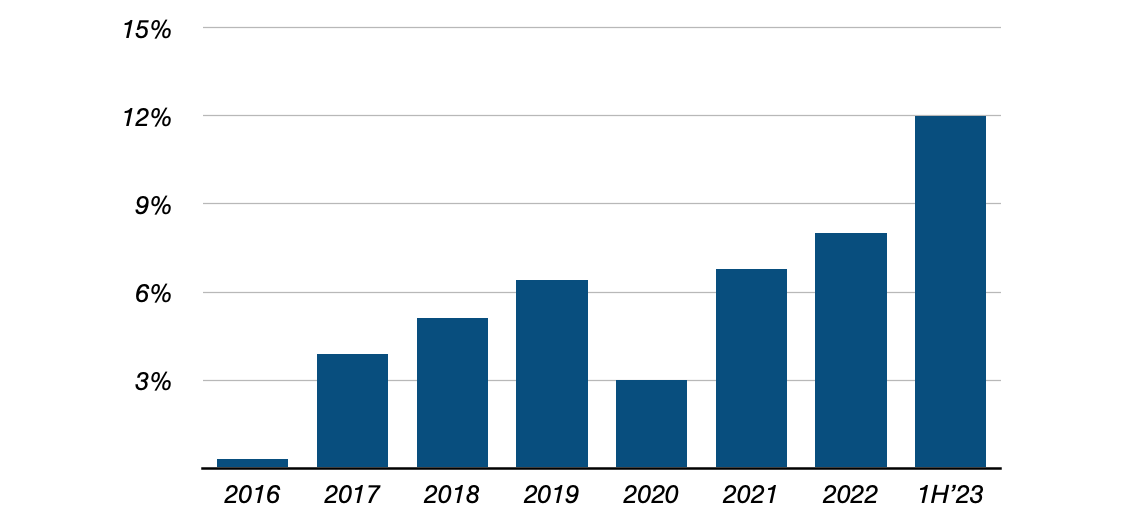

This is also feeding through to the bottom line as provisioning expenses remain low on the back of sound credit quality. As a result, net profit has risen to level whereby the bank's current ROTE is running ahead of management's original FY24 target of 10%. It is also well ahead of the chronically low single-digit numbers it was typically posting in recent years:

Standard Chartered: Annual ROTE

Data Source: Standard Chartered 2Q 2023 Supplemental Data Pack

{kind=link}

To be fair to the bank, some of this improvement is structural. It has made a push these past few years to target higher returning business lines like wealth management, for example, while it has also done good work on strengthening its underwriting standards more generally. The main driver, however, is macro.

Short Term Profits Might Be More Subdued

My main concern with Standard Chartered is what happens if the near-term macro environment gets a bit more bumpy than expected. The bank earned a 12% ROTE in H1 (11.9% in Q1 followed by 12.1% in Q2), but has only guided for a circa 10% ROTE for the full year. That isn't a huge surprise. Most of the benefit from higher interest rates has now been realized for one, and going forward I expect NIM to be broadly stable versus the Q2'23 level (1.71%). Loan growth is also slowing, again due to higher interest rates, and that will put a bit of pressure on the half-on-half comp for NII in H2'23.

Finally, asset quality realistically has only one way to go at this point. Impairment charges in H1'23 landed at around 11bp, which is 20-25bp below management's through-the-cycle target. Normalizing credit losses would obviously be a drag on net income.

Standard Chartered: Annual Loan Loss Rate

Data Source: Standard Chartered 2Q 2023 Results Presentation

{kind=link}

Now, management is guiding for the bank to earn a circa 11% ROTE in 2024, increasing thereafter. To get there it needs to grow NII and non-interest income ahead of operating expenses, plus keep impairment charges within its average through-the-cycle range. It's certainly doable, but I think risks are skewing to the downside.

While Standard Chartered's peers are all pretty much in the same boat, I do worry that there would more downside here should the macroeconomic environment end up worse than expected. I say that because the bank's provisioning is quite a bit lighter than some of its peers, with its allowance for credit losses ("ACL") at around 1.8% of gross loans and Stage 3 provisions covering 78% of non-performing loans (including collateral; 59% without). Just by way of comparison, recently covered DBS Group's ACL covers 1.5% of gross loans but 224% of Stage 3 loans (including collateral; 127% without). At 2.6%, Standard Chartered's Q2'23 NPL ratio was also around 150bps higher than DBS's. Capital looks adequate, with its CET1 (14% as of Q2'23) running a good 360bps above its regulatory requirement, but if the environment turns for the worse then I expect Standard Chartered to underperform.

Valuation Looks Fair, But Good Options Elsewhere

Standard Chartered shares currently change hands for HKD 72.25 in Hong Kong trading and GBX 758 in London. The ADSs ("SCBFY") trade for around $18.55 at time of writing (at a ratio of two ordinary shares to one ADS). Volume is much better in London so I would say US-based investors should look there first if possible.

Those quotes work out to around 0.7x Q2'23 tangible book value per share ("TBVPS"). On paper that looks quite cheap, certainly against 1H'23 ROTE of 12%, but against implied ROTE in 2H'23 it looks less so. Longer term, if your view is that management's targets are doable next year and beyond, then yes, these shares look like good value. You could easily argue for 20%-plus upside to the 0.9x TBVPS area. While that makes Standard Chartered a buy in my book, more risk-averse investors would do better to look at the likes of DBS instead.

For further details see:

Standard Chartered: A Rising Tide Lifts All Boats