SCBFY - Standard Chartered: High-Quality Global Bank Priced At A Deep Discount

2023-07-01 21:40:47 ET

Summary

- Standard Chartered has sold off in recent months on US/EU banking and China real estate contagion fears.

- The fundamentals paint a different picture, however, with credit risk well-managed and the capital position robust.

- At the current ~50% discount to book, Standard Chartered equity may have been penalized too harshly.

London-headquartered banking group, Standard Chartered’s ( SCBFF ) underwhelming track record of shareholder value creation, has long been an overhang on its valuation. Along with most major European banks post-2008 financial crisis, returns on equity have lingered in the low-single-digits %. Yet, management’s commitment to a double-digit ROE target has reignited interest in the shares, driving a solid run last year. Since then, the market's skepticism of the ROE improvement narrative has returned, with the discount to book value rising to an eye-opening ~50%. In contrast, credit risks have been well-contained thus far, while the strong capital position has continued to enable $1.25bn of buybacks/year (mid-single-digits % of the current market cap) on top of an attractive 5-6% dividend yield. In sum, investors don’t need much to go right fundamentally for the stock to work. Keep an eye on the ongoing aviation finance sale talks as an incremental buyback catalyst, along with renewed takeout interest following the First Abu Dhabi sale talks earlier this year.

Tracking the Momentum in Hong Kong

With the China reopening fizzling out following a promising start to the year, bearish sentiment on anything China has only worsened in recent weeks. Given its credit exposure to the region, Standard Chartered hasn’t been spared; alongside heightened concerns following the US/EU banking failures, the stock suffered a steep sell-off in March, erasing most YTD gains. While it is true that the bank plays a key role in cross-border financing across its footprint, particularly for Chinese customers, the distinction is that its primary P&L driver isn’t the onshore market but the offshore one (i.e., Hong Kong). As management highlighted at its Asia seminar last month, Hong Kong not only contributes the largest deposit base and segmental profits to the group but also higher ROTEs at three to four times that of the onshore business.

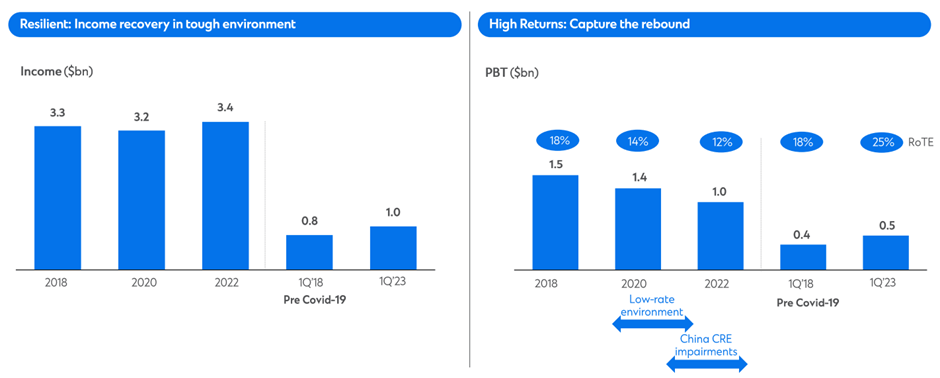

{kind=link}

To be clear, Hong Kong isn’t spared from credit headwinds, given its ties to global trade. But a more resilient consumer (note the rebound in Q1 retail sales) and modest growth in the key mortgage segment (up low-single-digits % currently) has helped to offset weakness in areas like trade finance. Meanwhile, the HK/China border reopening has continued to gain momentum, with visitor numbers now up to 2.3m in May 2023. While still well below pre-COVID levels, the encouraging consumer-led rebound bodes well for Hong Kong’s economic dependence on consumer finance. Having already seen a wealth management-led income recovery (now above pre-COVID levels) and significantly improved returns (25% ROTE) in Q1 2023, the bank remains poised to ride the recovery. Beyond wealth, tailwinds from Hong Kong’s retail sales growth (which translates to higher credit card spending) and bancassurance (tied to the physical return of mainland Chinese) should lead the next leg higher.

The Rate Tailwind Isn’t Over Just Yet

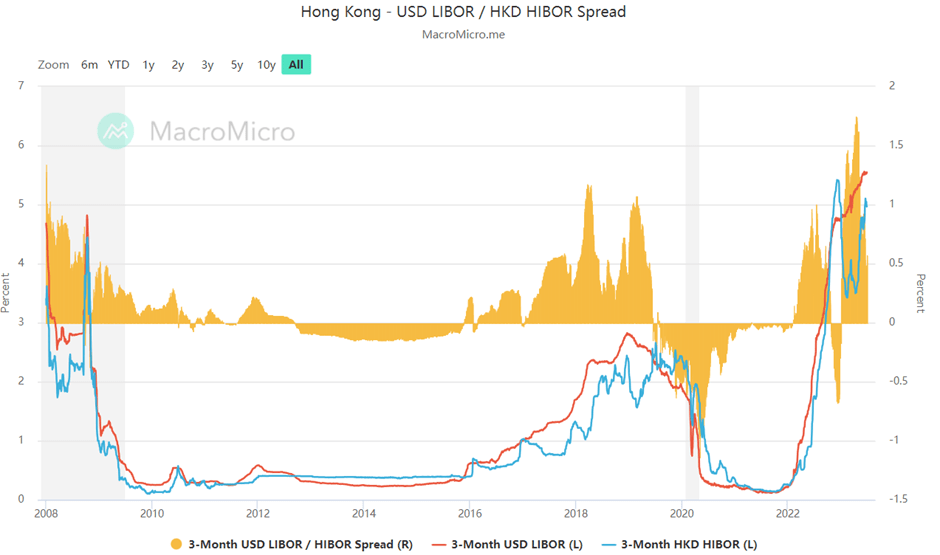

While rates have accelerated higher in the US/EU, Hong Kong interbank rates have lagged, and thus, the key question remains when (and if) domestic rates will converge with its developed market peers. For context, the Hong Kong Monetary Authority (‘HKMA’) runs an exchange rate-targeted monetary policy, so the base rate on its overnight discount window moves in lock step with the Fed. But the Hong Kong dollar interbank offer rates (‘HIBOR’) continue to lag comparable benchmarks at ~4.95% for the one and three-month tenor (vs. the USD Libor at 5% and 5.5%, respectively). This gap should eventually converge, though, helped by the HKMA mopping up HKD liquidity, presenting upside to the HIBOR through Q2 2023.

{kind=link}

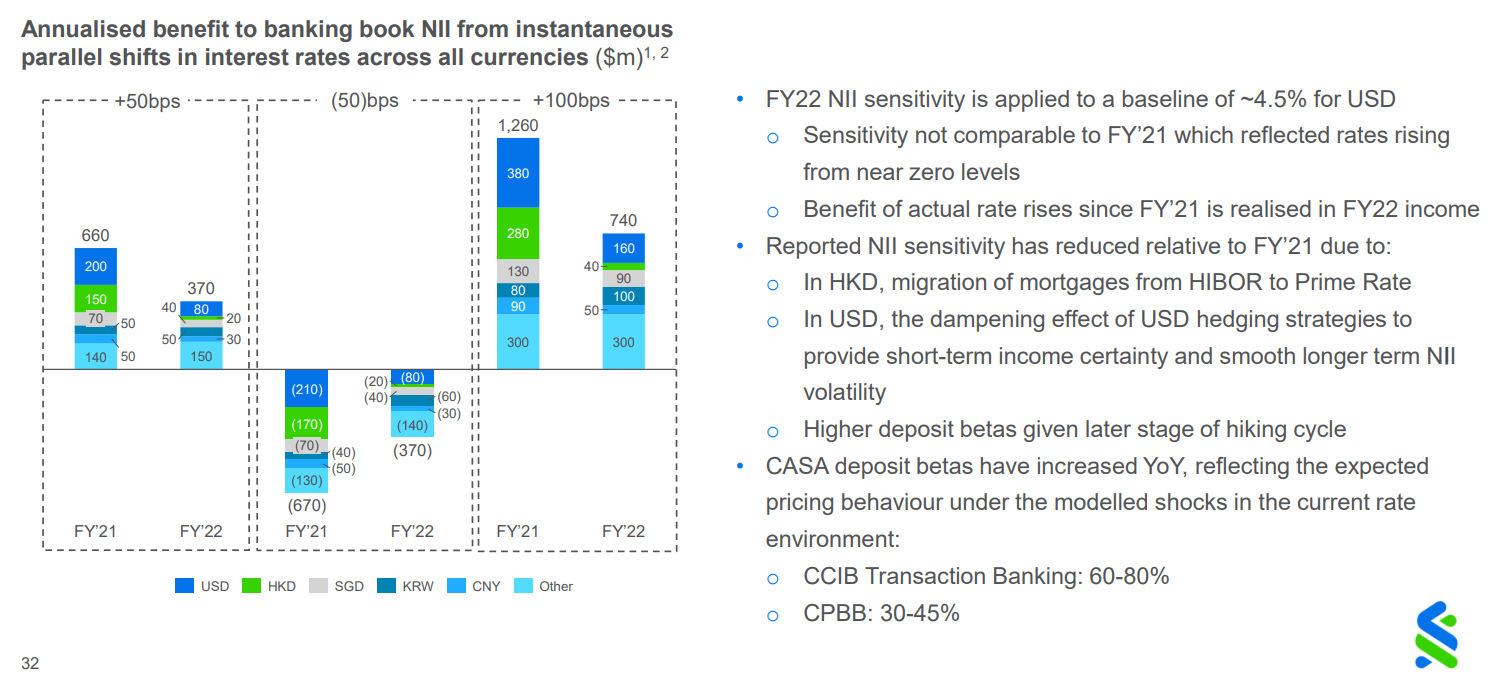

While Hong Kong rates offer less upside to Standard Chartered net interest margins, it should benefit from higher rates, nonetheless. Recall that as of Q4 2022, management had sized the impact of a 100bp rise in Hong Kong rates at +$40m (vs. +$160m for the US). Extrapolating this sensitivity assumption would suggest a 50bps normalization of the HIBOR could add an incremental ~$20m/year to net interest income. In the likely scenario we get another 50bps of Fed hikes (based on recent Fed commentary ), an incremental ~$40m/year (~$80m on the USD side) could well be on the cards for the banking book.

{kind=link}

Robust Capital Position Intact; More Capital Return on the Horizon

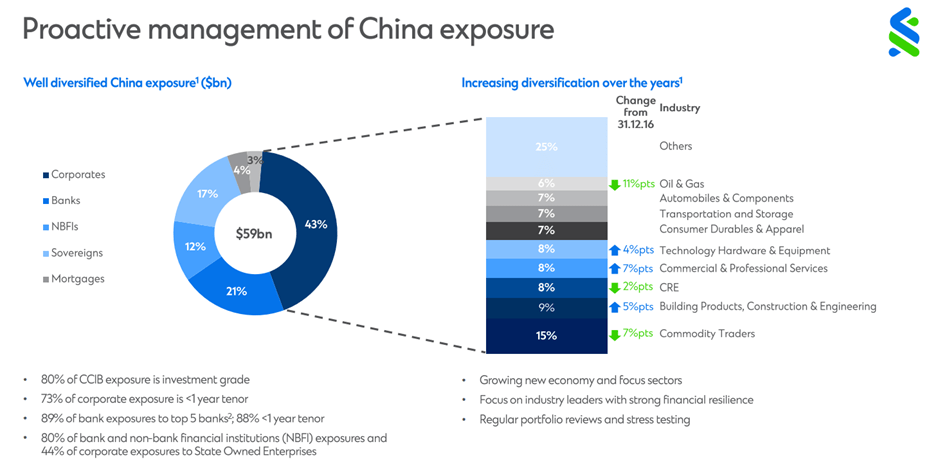

In the face of heightened China credit concerns , the bank is well-capitalized - even in a worst-case scenario. Recall that in Q1, the CET1 ratio came in at a solid 13.7% on the back of +50bps profit accretion, offsetting a 40bps headwind from buybacks and another ~10bps from AT1 payouts and dividends. For now, my base case is for no deterioration in underlying credit quality given the benign Q1 result (non-performing loans down to 1.7%) and the prospect of further economic recovery and falling unemployment in Hong Kong. While I do acknowledge the risk that comes with Standard Chartered’s China exposure, a major source of impairments in recent years, context is important. Post-diversification efforts, Chinese commercial real estate is now down to ~8% of the country-specific loan book. Against the bank’s massive $800bn asset base and ~$50bn of equity as well, its exposure looks manageable.

{kind=link}

With risk-weighted assets still on track for low-single digits % growth and the bank already midway through its $1bn buyback program (post-FY22 results announcement), another buyback announcement seems likely this year. With the stock also languishing at a ~50% discount to book, any buyback here should prove accretive over the long run. Hence, an upsized buyback should take precedence over enhancements to the dividend payout. Expect incremental capital return upside if the bank completes the disposal of its aviation finance operation to AviLease at the reported $3.7bn price tag (implying a book value premium), particularly with the bank already nearing the upper limit of its 13-14% target range.

High-Quality Global Bank Priced at a Deep Discount

After years of post-GFC underperformance, Standard Chartered doesn’t have the best record when it comes to shareholder value creation. But I wonder if shares are priced too cheaply here. At a wide ~50% discount to book, despite running a massive shareholder return yield comprising $1.25bn of share buybacks last year (likely more this year) and a well-covered mid-single-digit % dividend, the stock seems far too cheap. Execution toward management’s double-digit ROE target should help with investor perception, as will higher rates in the US/Hong Kong and credit risk management. Elsewhere, an upsized buyback post-sale of its aviation finance business or renewed M&A interest adds compelling optionality.

For further details see:

Standard Chartered: High-Quality Global Bank Priced At A Deep Discount