STN - Stantec: Good Prospects But Not An Attractive Entry Point

2023-05-24 20:54:07 ET

Summary

- Revenue should benefit from healthy end market demand, government infrastructure investments, strong backlog level, and improved execution.

- Margin should benefit from improving global segment margin, operating leverage, and an increase in productivity.

- Valuation is above historical averages.

Investment Thesis

Stantec, Inc. ( STN ) is expected to benefit from revenue growth driven by a robust demand environment in the infrastructure space. This is attributed to secular trends such as aging infrastructure, energy transition, climate resilience, and the onshoring of manufacturing in the United States. These demand trends are further supported by government investments like the Infrastructure Investment and Job Act (IIJA), CHIPS and Science Act, and Inflation Reduction Act (IRA), which create additional bidding opportunities. Additionally, the company's healthy backlog of C$6.2 billion and improving execution capabilities are expected to contribute to revenue growth.

In terms of margins, Stantec should experience benefits from strengthening global segment margins, improved productivity, and operating leverage. While the company has promising growth prospects and a favorable operating environment, its current valuation already reflects these expectations, trading above its historical averages. Therefore, I would prefer to wait for a better entry point to capitalize on the aforementioned growth prospects. For now, I have a neutral rating on STN stock.

Revenue Analysis and Outlook

In my previous article in February, I discussed how Stantec's revenue growth would benefit from the strong demand in the end market going forward. However, I preferred to remain on the sidelines due to its high valuation, which already factored in the anticipated growth prospects. Since then, the stock price has traded in line with expectations, posting a slight decline.

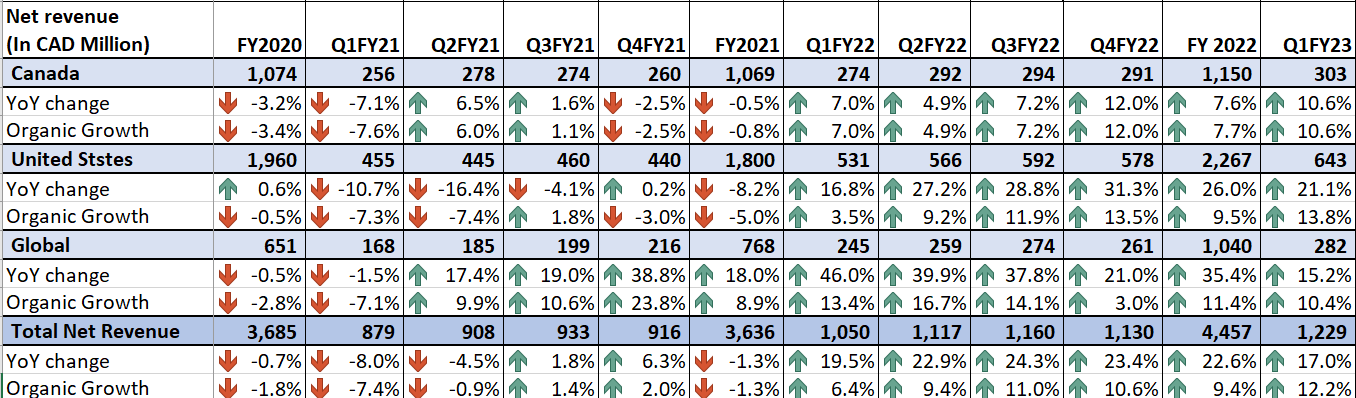

During the first quarter of 2023, the end market demand continued to be robust, supported by various government stimulus funds in the infrastructure sector. Additionally, favorable foreign exchange rates and effective backlog execution contributed to sales growth. As a result, net revenue increased by 17% year-on-year to C$1.2 billion. Excluding the 3.4 percentage point benefit from foreign exchange and the 1.4 percentage point benefit from acquisitions, organic sales grew by 12.2% year-on-year.

STN’s Historical Net Revenue (Company Data, GS Analytics Research)

{kind=link}

Looking ahead, I believe that Stantec should continue to experience revenue growth as it benefits from a healthy backlog, strong end-market demand, and the successful pursuit of large multi-year projects.

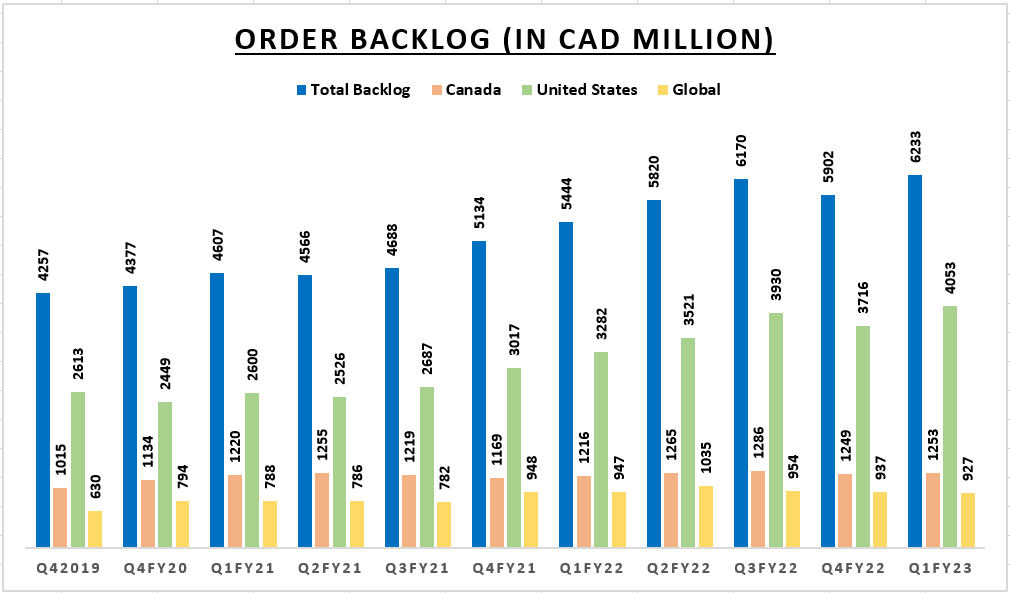

The company's backlog, which serves as an indicator of future revenue growth, is at a healthy level. In the first quarter of 2023, the backlog increased by 14.5% year-on-year, or 5.8% year-on-year on an organic basis, reaching C$6.2 billion. This growth in the backlog was primarily driven by a 23.5% year-on-year increase in the U.S. segment's backlog, supported by rising infrastructure investments. Stantec's backlog represents approximately 13 months of work, providing good visibility for revenue growth in the current year. Additionally, the company is actively increasing its headcount to enhance backlog execution. According to management, the first quarter of 2023 saw the highest number of new hires for the company, indicating a favorable labor market for Stantec. This hiring activity is expected to improve employee retention and contribute to enhanced backlog execution, ultimately supporting revenue growth.

{kind=link}

In addition to improving backlog execution, I am also optimistic about the company’s order outlook given the favorable end market prospects. The demand in the market is supported by several secular trends:

-

Aging and overloaded infrastructure globally, particularly in developed countries like the U.S., which is driving the need for modernization and enhanced safety.

-

Growing focus on energy transition and sustainability, leading to increased demand for renewable sources of power generation and environmentally-friendly solutions.

-

Rising concerns about climate change, leading to projects focused on climate resiliency and mitigation efforts worldwide.

-

Supply chain challenges prompting the reshoring of manufacturing in the U.S. to reduce dependence on other regions.

The federal government is also actively supporting these demand trends through infrastructure investments. Funds from the Infrastructure Investment and Job Act (IIJA) are starting to flow, and Stantec expects a strong order pipeline in the second half of 2023 supported by IIJA. Additionally, the Inflation Reduction Act (IRA) provides expanded credits for clean hydrogen, renewable fuels, and EV charging infrastructure, creating further opportunities for bidding. The CHIPS and Science Act is also fostering the onshoring of manufacturing in the U.S. These secular trends and federal stimulus funds provide a positive multi-year outlook for revenue growth for Stantec.

These demand trends and infrastructure investments have already helped Stantec secure several incremental major project awards in the first quarter of 2023. For example, the company secured contracts for a waterline extension in central Alberta, a wastewater treatment plant and recycled water facility in San Francisco, a new weir in Arkansas, and bridge and roadway design-build services for Kentucky's Licking River Bridge. Furthermore, Stantec was selected for a large-scale pumped storage project in Scotland and appointed to Homes England's development and regeneration technical services framework. These project wins align with the company's expertise and contribute to revenue growth.

Overall, I maintain an optimistic outlook for Stantec's revenue growth prospects in the coming years. Management has reaffirmed its initial guidance of mid to high single-digit organic growth in 2023, a target that appears achievable given the strength of the company's backlog and the positive market conditions.

Margin Analysis and Outlook

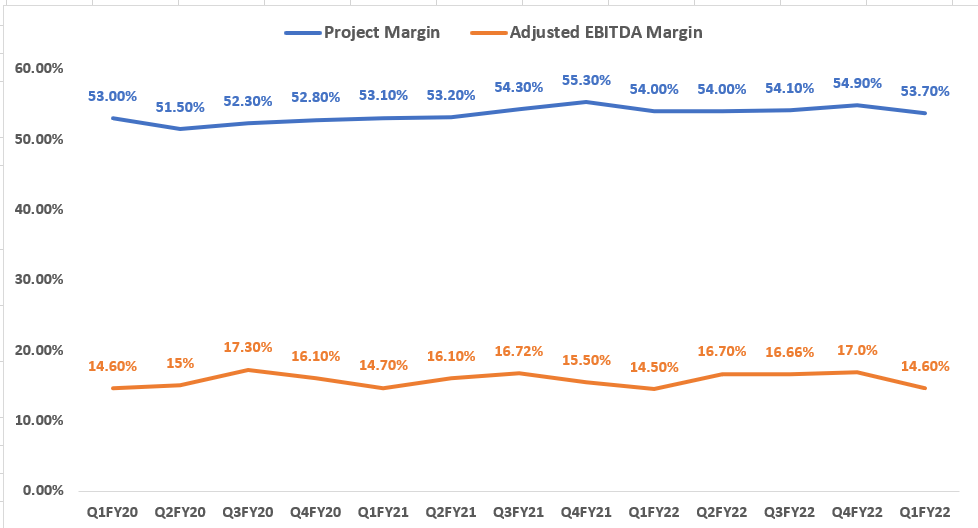

In the first quarter of 2023, the company experienced an adverse impact on its project margin (gross margin) due to shift in project mix in the global region. As a result, the project margin declined by 30 basis points year-on-year to 53.7%. On the other hand, the adjusted EBITDA margin benefited from operating leverage, and increased 10 basis point year-on-year, reaching 14.6%.

STN’s Project Margins and Adjusted EBITDA Margin (Company Data, GS Analytics Research)

{kind=link}

In recent quarters, the company's project margin has been negatively affected by challenges in the Global segment, primarily due to shifts in project mix. However, looking forward, management expects these challenges to diminish, leading to improved margins within the global segment in the upcoming quarters. Furthermore, Stantec is currently seeing less pressure from wage increases now as it recruits new employees. This should also help margins. Additionally, a higher-margin backlog resulting from improved project selection and operating leverage due to revenue growth should further support margin expansion.

Valuation and Conclusion

STN is currently trading at a forward price-to-earnings (P/E) ratio of 22.02x, based on the FY23 Consensus EPS estimate of 2.61. This valuation is above its historical five-year average forward P/E ratio of 20.39x. While I acknowledge the growth prospects of the company in the coming years, the current premium valuation leads me to remain on the sideline. I would prefer a more favorable entry point to take advantage of the company's long-term growth prospects. As a result, I maintain a neutral rating on the stock.

For further details see:

Stantec: Good Prospects But Not An Attractive Entry Point