STEM - Stem: Are The Shares A Sell?

2023-08-24 13:38:34 ET

Summary

- Stem's common shares have collapsed and show no signs of recovering in the near term.

- The company's revenue growth rate has moderated with gross profit margins seeing some incremental year-over-year growth.

- Its cash position has deteriorated significantly and external capital might be required within three quarters. This comes as the decarbonization trend ramps up.

The post-pandemic stock market zeitgeist of inflation and an aggressive Fed has posed intense headwinds to the clean energy sector, where wholesale losses across yieldcos to utility-scale battery plays have become the defining feature of the renewable energy transition in 2023. Stem ( STEM ) is now down 39% since the beginning of 2023, with its common shares losing 63% of their value over the last year. The stock is changing hands at a near-record low price-to-sales multiple of 1.9x. This was a ticker that was never meant to end up in this torrid position against triple-digit year-over-year revenue growth for much of 2022 and a roadmap to positive cash flows that came with its higher-margin software businesses. I've always been bullish on Stem. This bullishness was not unfounded and built on the back of the ongoing generational shift to renewable energy, set to be bolstered by the $370 billion 2022 Inflation Reduction Act.

Critically, the deployment of short-duration energy storage systems for the ongoing shift to renewable energy formed an integral but overlooked part of the transition and Stem had carved a fast-growing leadership position within this niche. This formed an integral part of its investment pitch and was set against the winds of change from decarbonization. The renewable energy revolution is real and will forever change the makeup of the global energy system. Further, with the US moving more aggressively to mitigate anthropogenic climate change and contribute to the global effort to restrict the rise in mean global temperature to well below 3.6°F above pre-industrial levels, there will be more growth opportunities for Stem.

The Fiscal 2023 Second Quarter Earnings Highlight Why The Short Interest Sits At 27%

{kind=link}

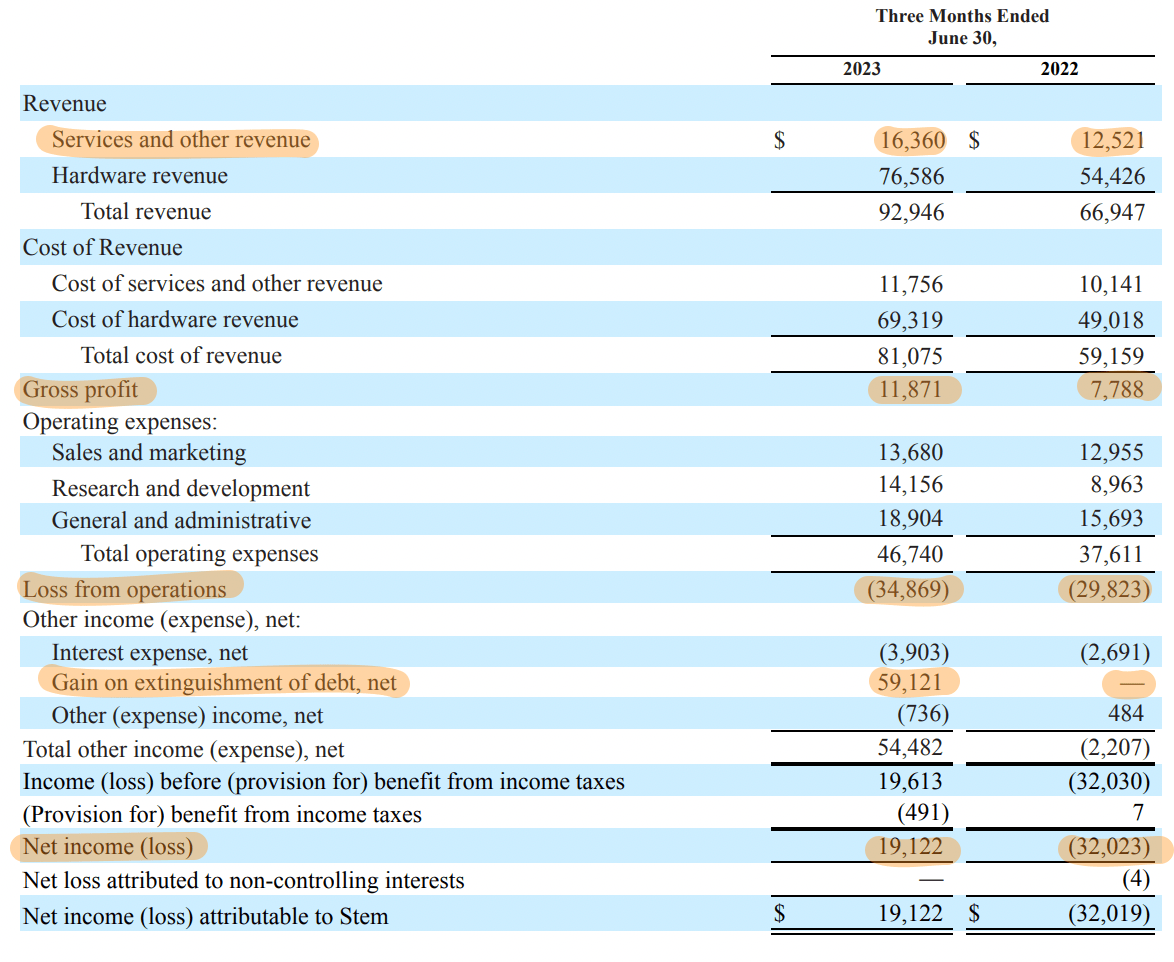

Stem reported fiscal 2023 second-quarter revenue of $92.95 million , 39% growth from its year-ago comp and a beat by $1.29 million on consensus estimates. Bookings grew by 5% year-over-year to $236.4 million with a contracted backlog exiting the quarter at a new record of $1.36 billion, up a huge 88% from $726.6 million in the year-ago comp. Higher margin services and other revenue at $16.36 million comprised 17.6% of total revenue during the second quarter and grew by 30.7% over its year-ago period.

{kind=link}

Bears would flag that this was a slower rate of growth than hardware revenue, with gross profit of 13% for the second quarter coming in around 100 basis points higher than its year-ago comp figure of 12%. The company did report a GAAP net profit of $19.1 million, despite a loss from operations that grew by $5 million over its year-ago period to reach $34.87 million. This came on the back of a one-time $59 million gain from the extinguishment of debt from the repurchase of a portion of the company's 2028 convertible notes. Cash as of the end of the second quarter was $138 million , down sequentially from $206 million in the first quarter.

To Hold Or To Sell?

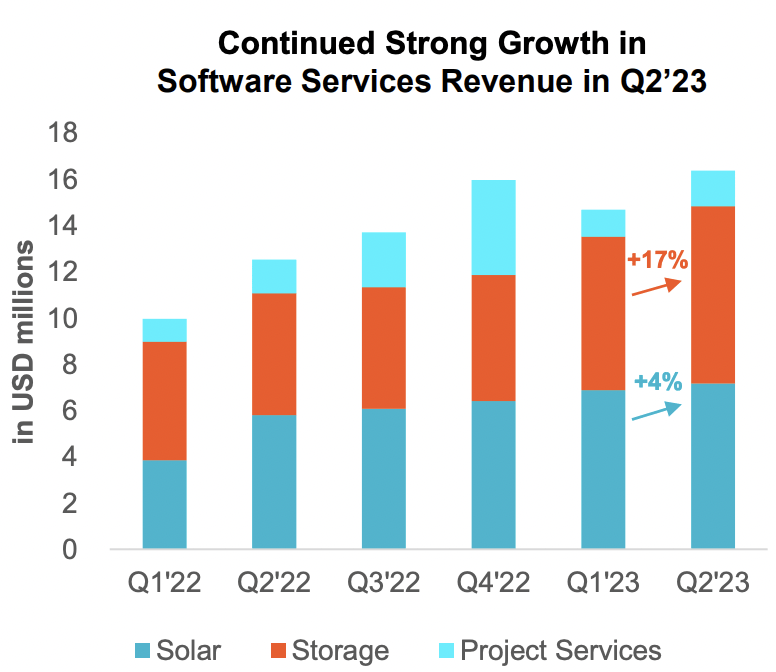

Stem reported software gross profit margins of 28%, more than double the gross margins of aggregate hardware sales, to highlight the promise of the company's software-centric business tilt. Further, the quarter-over-quarter change in cash was driven by a $102 million battery purchase that is set to be converted to sales in the second half of 2023 on the back of what management highlighted during their second-quarter earnings call as a very active delivery cycle.

The company's actual results have lagged behind the initial guidance provided when it was going public via SPAC. This was meant to see blended gross margins of 32%. This underperformance on gross margins versus initial estimates comes as the company's cash position has fallen to a record low. Stem will likely need external capital within the next three quarters based on the historical trajectory of its cash burn, even with management promising positive adjusted EBITDA in the second half of 2023. This line item was negative $9 million for the second quarter, versus an $11 million loss in the same quarter last year. The company is guiding for $550 million to $650 million in revenue for fiscal 2023 with non-GAAP blended gross margins to come in at 15% to 20%.

This would imply a forward price-to-sales multiple of 1.3x against the midpoint of its revenue range. This would be a marked difference from a year ago, when Stem was changing hands at a double-digit multiple. The shares are likely a hold against this record-low multiple, as a potential recovery could come on the back of a Fed pivot improving market appetite for risk assets just as the company reaches positive adjusted EBITDA. However, I will not recommend Stem as a buy before it reaches its profitability guidance and further grows the software component of its revenue.

For further details see:

Stem: Are The Shares A Sell?