STEM - Stem: Awaiting Software Inflection

2023-12-21 04:56:03 ET

Summary

- Stem's Q3 results were mixed, with adjustments to historic hardware sales and a decrease in revenue guidance for 2023.

- We like the sector but were expecting a higher growth rate in H2, supported by software sales.

- Looking ahead, we lower sales and margin estimates, and as a consequence, we reduce our target price.

Here at the Lab, since our publication on Superchargers And Electric Vehicles called Chickens And Eggs released in 2020, we have had a positive view of the Battery Energy Storage System companies. In our last analysis, we recently reported how Stem (STEM) was On Track For A Positive 2023 H2 ; however, looking back to our study and incorporating Stem's Q3 results, we are now more cautious. Today, we briefly comment on the results from the past quarter and then apply our changes for the next visible period. Our buy rating was supported by an asset-light business model and long-term growth thanks to a favorable environment. Our team is disappointed with the company's stock price evolution, and Stem now trades at $3.7 per share. Indeed, Wall Street no longer justifies the company's valuation, and we partially agreed.

Q3 results with negative & positive take

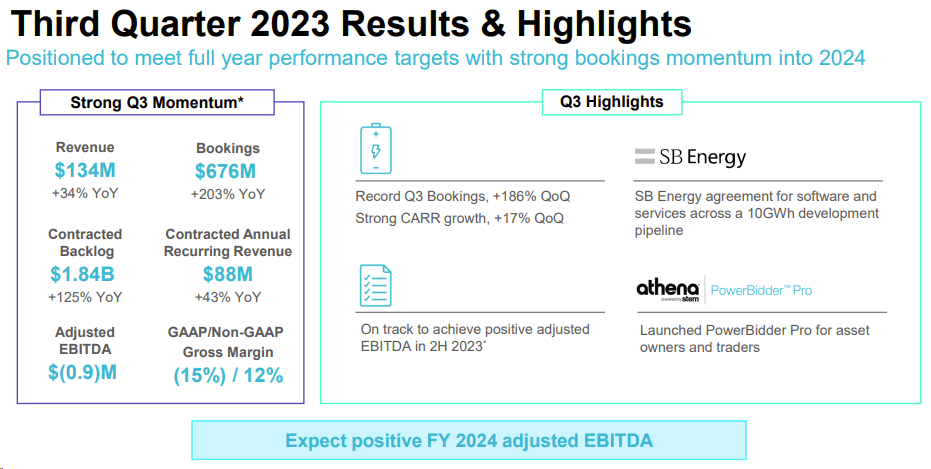

In Q3, the company delivered a mixed performance, which included top-line sales adjustments to historic hardware turnover. Stem confirmed its outlook to be adjusted EBITDA positive in Q4 2024; however, in our last assessment, we reported how 75% of the total company's sales were due in H2 with Q3 turnover guidance between $165 million and $195 million and booking between $350 million and $425 million. Looking ahead and considering Stem's target 2024 growth, we expected a positive EBITDA in 2024. Going into the details, Stem reported a negative $37 million one-off from hardware sold last year. Q3 sales reached $134 million with a growth of 34% and were significantly below our expectations, while non-GAAP gross margin was 12.5%. Q3 bookings reached $676 million with a 203% growth year on year and were far above our optimistic guidance. Despite that, the company previously offered some guarantees that hardware value would not reduce; however, this adjustment proved a different story and implicated another risk to consider. In addition, the company decreased its Fiscal Year 2023 top-line sales guidance between a range of $513 million and $613 million and narrowed the adj. EBITDA outlook from a loss of $ -5/-35 million to a loss of $-15/25 million. This new outlook implied a Q4 adjusted EBITDA between -$1 million and +$9 million. On a positive note, bookings were maintained at $1.4-1.6 billion at the aggregate level. Our team is now more cautious about the cash and cash equivalents. In H1, Stem ended the quarter with $140 million and was guided to increase its cash level position by $10 million at year's end. Post Q3 results, we now forecast a lower number.

{kind=link}

Changes in estimates

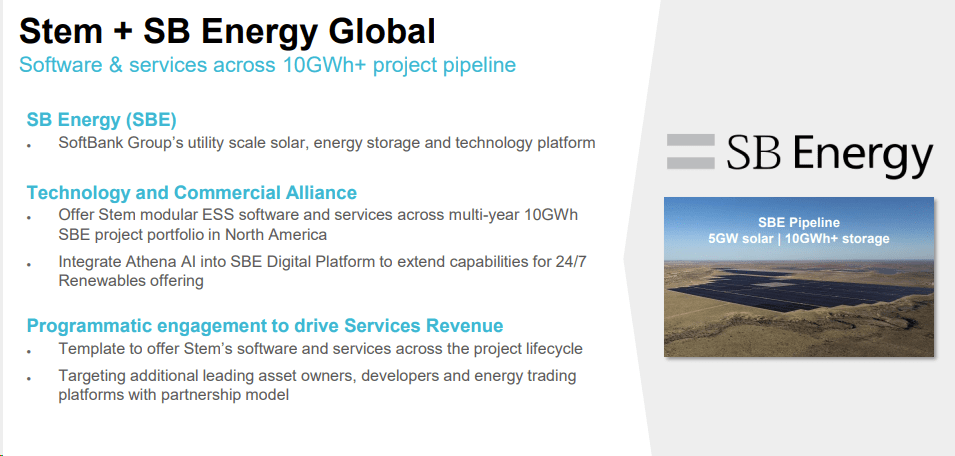

Following the results, we revised our 2023-25 adjusted EBITDA forecast from $(21)/75/150 million to $(20)/20/85 million. The above numbers are based on $565, $865, and $1.2 billion in sales in 2023, 2024, and 2025. Heading into the Fiscal Year 2024, the company closed Q3 2023 with cash and cash equivalents of $125 million, and top management guided at a cash balance at year-end of $150 million. Our team sees this as achievable, but we know the shift to modular solutions is crucial to the company's future cash flow. Stem anticipates working capital improvements; however, we are now more prudent, following the elevated cash conversion cycle recorded in 2023. As already happened in another growth story, we are now more cautious about long-term growth aspirations. Looking back, in 2023, Stem's sales are +31% year-over-year. On a positive note, we believe Stem is a clear beneficiary of the IRA-driven storage demand. The company announced an alliance with SB Energy to support our buy to provide software for a 10GWh North America project portfolio. On a positive note, we still see Athena as a critical differentiator, and PowerBidder Pro will likely help the company achieve higher software sales. In addition, we see a cross-selling opportunity, even if it is still modest. Despite that, we should note that EV demand has been lower than anticipated.

{kind=link}

Conclusion and valuation

Our internal team has always seen Stem as a growing energy storage market leader. The company, coupled with the Athena platform, has an advantage in incorporating EV charging applications and solar monitoring. Stem's key milestone is its progress toward profitable growth, and we should also focus on the company's software sales growth. Here at the Lab, we should emphasize how STEM is a high-risk/reward investment, and the company has yet to report a quarterly profit. Therefore, we decided to decrease our buy rating target price from $9 to $4.2 per share. This is based on an EV/EBITDA multiple of 6.5x. Peer multiple suggests this target valuation. Still, the Stem backlog now stands at $1.84 billion and should support solid revenue visibility into 2024 and beyond. We are waiting for the software inflection (less capital-intensive with a higher margin). This lower target price is due to a reduced profit estimate over the visible period and a lower margin expansion ramp-up. In addition, there is uncertainty about the acceleration in storage capital investment, and this risk cannot go unnoticed.

For further details see:

Stem: Awaiting Software Inflection