STEM - Stem: The Slow Collapse Of Cash Is Worrying

2023-12-07 17:24:40 ET

Summary

- Stem has experienced significant sales growth due to the demand for solar energy ramping up. Bookings were up 203% for its fiscal 2023 third quarter.

- Cash and equivalents continue to decline to place the company's solvency at risk without a material reduction in free cash burn.

- The ramp in bookings and guidance for positive adjusted EBITDA for 2024 offer hope for bulls against the backdrop of a possible dovish Fed pivot.

Stem's ( STEM ) sales growth has been remarkable, with the company recording an 83% two-year compound annual growth rate from its fiscal 2023 third quarter on the back of ramping demand for renewables. Solar and wind energy are now on track to account for 16% of total US electricity generation in 2023, growing to 18% in 2024 with dual production tax and investment tax credits provided by the 2022 Inflation Reduction Act set to bolster the growth of US solar by an additional 160 gigawatts over the next decade. Stem provides a pick-and-shovel play on the decarbonization macrotrend with demand for utility-scale energy storage for renewables set to grow materially over the next decade. The common shares are down 63% year-to-date, with topline growth being followed by deep unprofitability and free cash burn that has materially impeded Stem's cash runway.

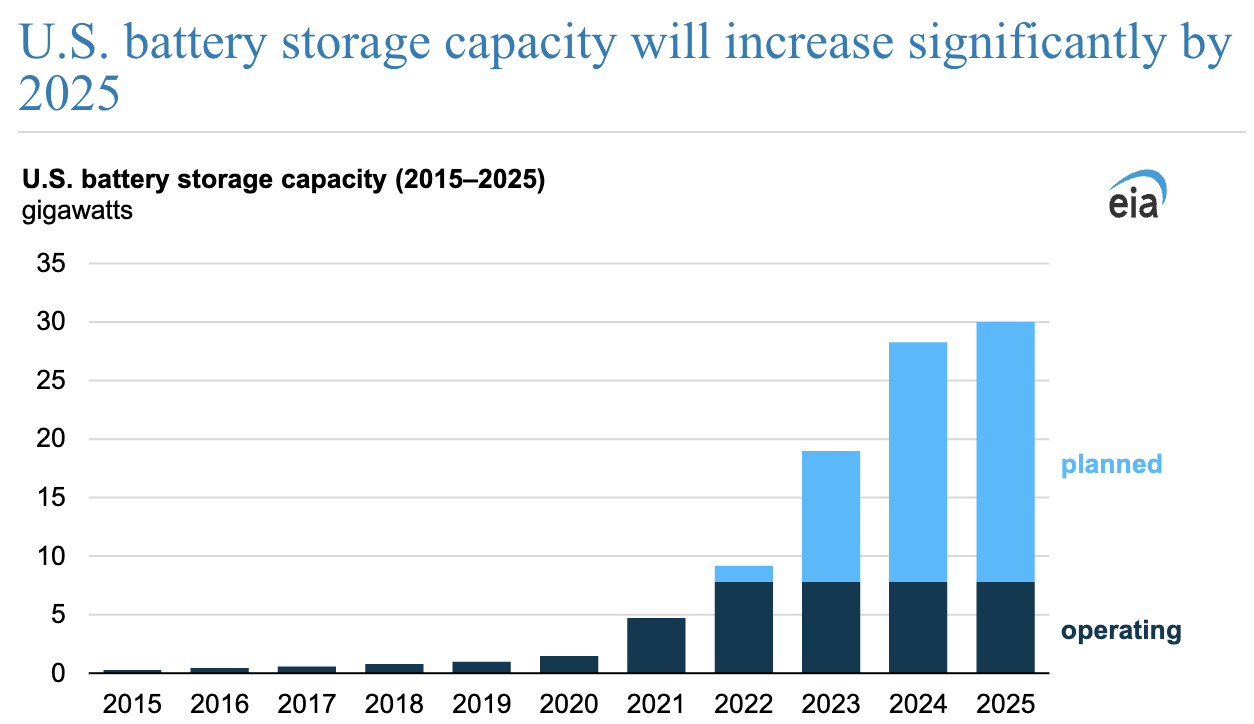

US Energy Information Administration

At risk here is the company's solvency against cash and equivalents at $125.4 million at the end of the recent third quarter. This was down $12.8 million sequentially and down around $168 million versus a year ago. Not great. Stem's flexibility to layer on debt to extend this runway is also somewhat impeded, with total debt at $606 million at the end of the third quarter.

{kind=link}

US Energy Information Administration

However, the bulk of this debt is near-zero interest rate convertible debt including 2028 unsecured convertible notes that bears interest at a rate of 0.5% per year. Hence, Stem only faced a $4.4 million third-quarter interest expense. It's hard to overstate just how material the opportunity is ahead for Stem. The US Energy Information Administration expects at least 20.8 GW of battery storage capacity to be added from 2023 to 2025. This will increase capacity to 30 gigawatts, a more than six-fold increase from 2021.

Net Losses And Bookings Surge

{kind=link}

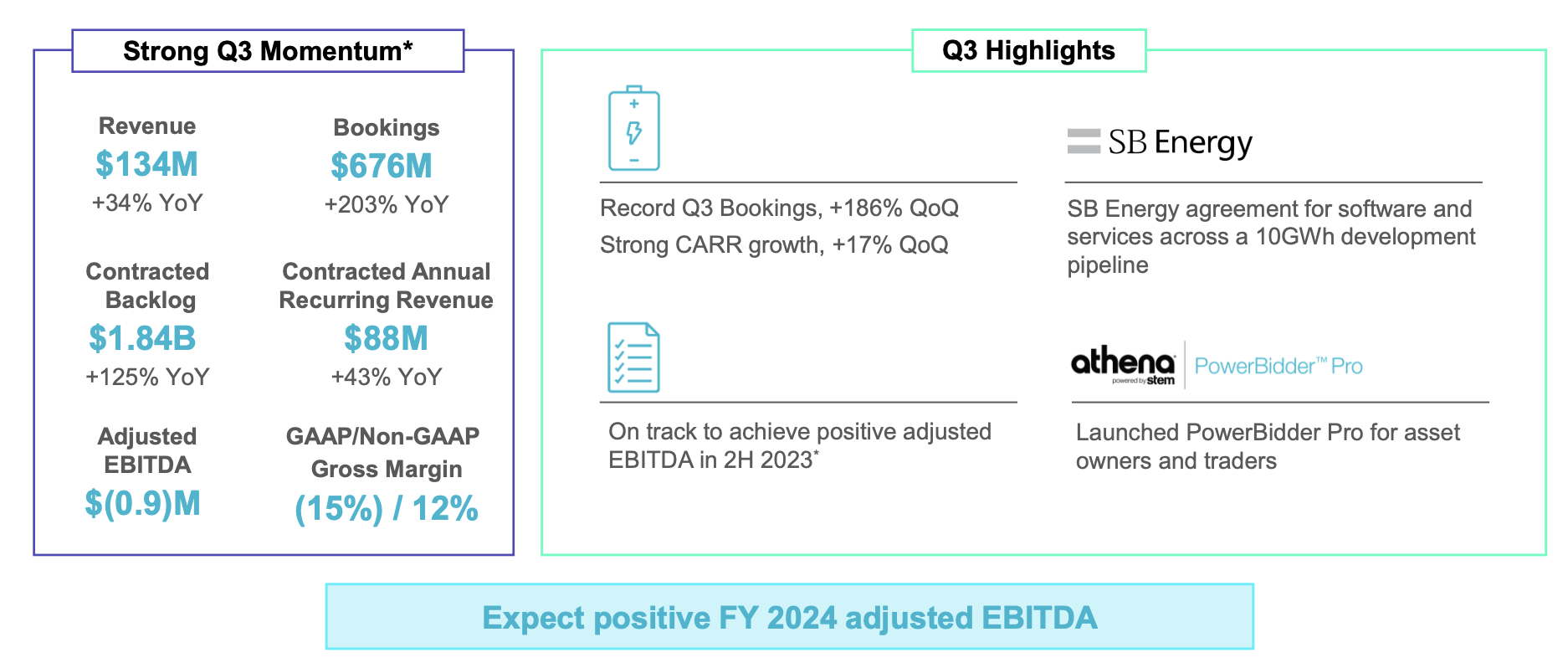

Stem Fiscal 2023 Third Quarter Presentation

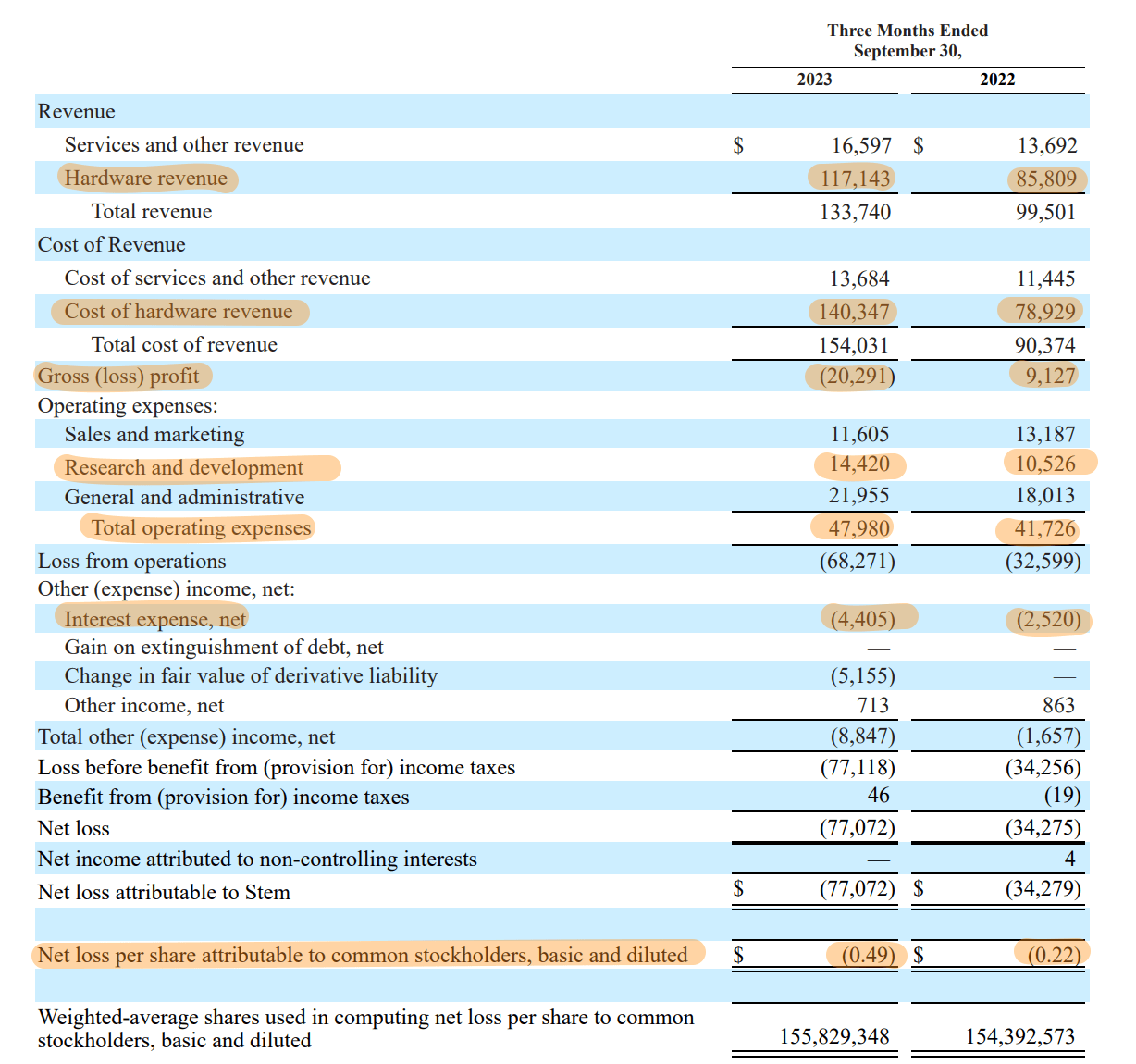

Stem recorded third-quarter revenue of $133.7 million , up 34.4% over its year-ago comp but a huge miss by $46.46 million on consensus estimates. Bookings grew a material 203% over the year-ago comp to $676 million , a new record, to underscore just how significant the demand for battery energy storage systems is. Guidance for full-year 2023 will see revenue come in at $513 million to $613 million, representing year-over-year growth of 25% at the midpoint. This is forecasted to then grow by at least 40% annually for the next two years. However, the bulk of this is made up of extremely low-margin hardware revenue.

{kind=link}

Stem Fiscal 2023 Third Quarter Form 10-Q

Hardware revenue of $117.14 million came with costs of $140.34 million with Stem recording a gross loss of $20.29 million during the third quarter, a negative GAAP gross margin of 15%. This dipped from a positive margin of 9% in the year-ago period. The decline in gross margin drove a significant expansion of net loss, which came in at $0.49 per share, up 27 cents from the year-ago period.

The Danger Ahead As Bearish Narrative Deepens

Free cash burn for the quarter came in at $4.4 million, an improvement from a burn of $38.3 million in the prior year-ago period. This comes on the back of the company's guidance for positive adjusted EBITDA for the full year 2024, an improvement from a full-year 2023 adjusted EBITDA loss of $15 million to $25 million. Stem's free cash burn is running at $245 million for the last 12 months, assuming a 50% reduction of this figure for the next four quarters would see a total cash burn of $122.5 million. I've admittedly been bullish on the ticker in prior coverage , but the lack of its higher-margin software division ramping as per the initial SPAC guidance has meant the market sharply revaluing the company lower, with its price-to-sales ratio dropping to 1.07x.

{kind=link}

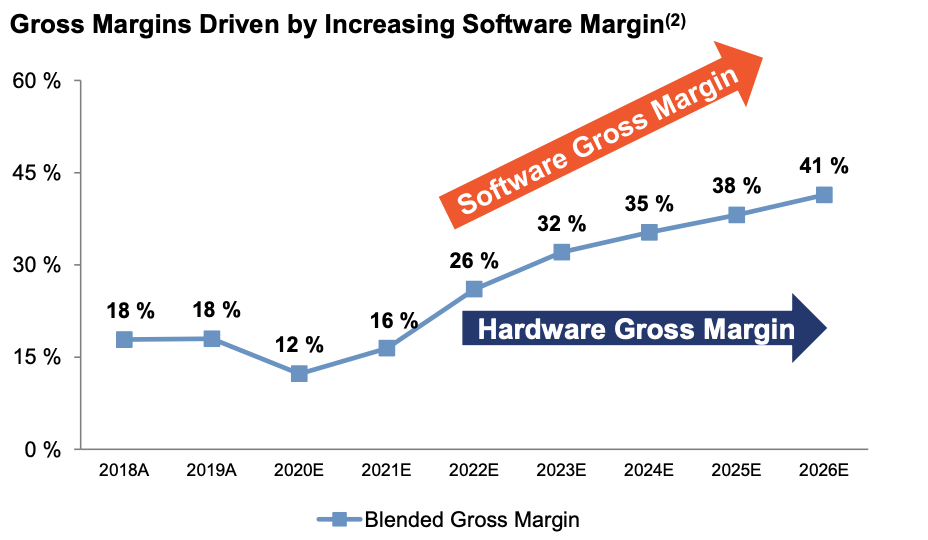

Stem 2020 SPAC Investor Presentation

Critically, the company was guiding for blended gross margins to be at 32% for fiscal 2023. That figure is currently 1.86% on a GAAP basis for the last 12 months. The bearish narrative on Stem has focused on the company's flagging software sales and low gross margins against steep losses, high cash burn, and a declining liquidity position. These negative trends have come amidst a generational surge in demand for renewables, driving ever higher energy storage volume. There is more competition in the market too, with Fluence Energy ( FLNC ) reporting 52% year-over-year growth for its most recent quarter. Hence, the 27% short interest in Stem does not look misplaced, the company has less than four quarters of cash left against its current cash burn trajectory without a material reduction in outlays. However, rating this as a sell is difficult against a possible dovish Fed pivot, the strong growth in bookings, and guidance for positive adjusted EBITDA in 2024. Stem is a hold for now, but could see more near-term downside if its cash burn profile fails to recover.

For further details see:

Stem: The Slow Collapse Of Cash Is Worrying