SHOO - Steven Madden: Better Performance Expected (Rating Upgrade)

2024-01-10 16:00:17 ET

Summary

- Steven Madden's stock price rebounded in November after hitting its lowest point in September 2023 on account of improved performance in Q3 2023 and more robust growth expectations.

- Even though forecasts for 2024 look good, there are risks ahead as the US economy can slow down and there's limited likelihood for further margin expansion.

- In the meantime, its market multiples have risen higher than the consumer discretionary sector median, indicating that the price upside has been exhausted for now.

When I last wrote about the shoe company Steven Madden ( SHOO ) last April, there was good reason to expect a decline in share price. Its performance was on the decline and the gloomy outlook (fair as it was, in hindsight) made matters worse. There might still have been a Buy case on the stock were it undervalued. It wasn't. It was actually fairly priced compared with the consumer discretionary sector, prompting a Sell rating.

{kind=link}

The prediction came to pass as the stock touched its lowest in September 2023, with a decline of 15% from the time I wrote about it. However, much has changed since. Come November, it saw an uptrend again, and even with a price correction toward the end of the year, it has now erased these losses entirely.

Here I take a look at why the price started rising in November and whether these gains can be sustained in 2024.

Why did the price rise?

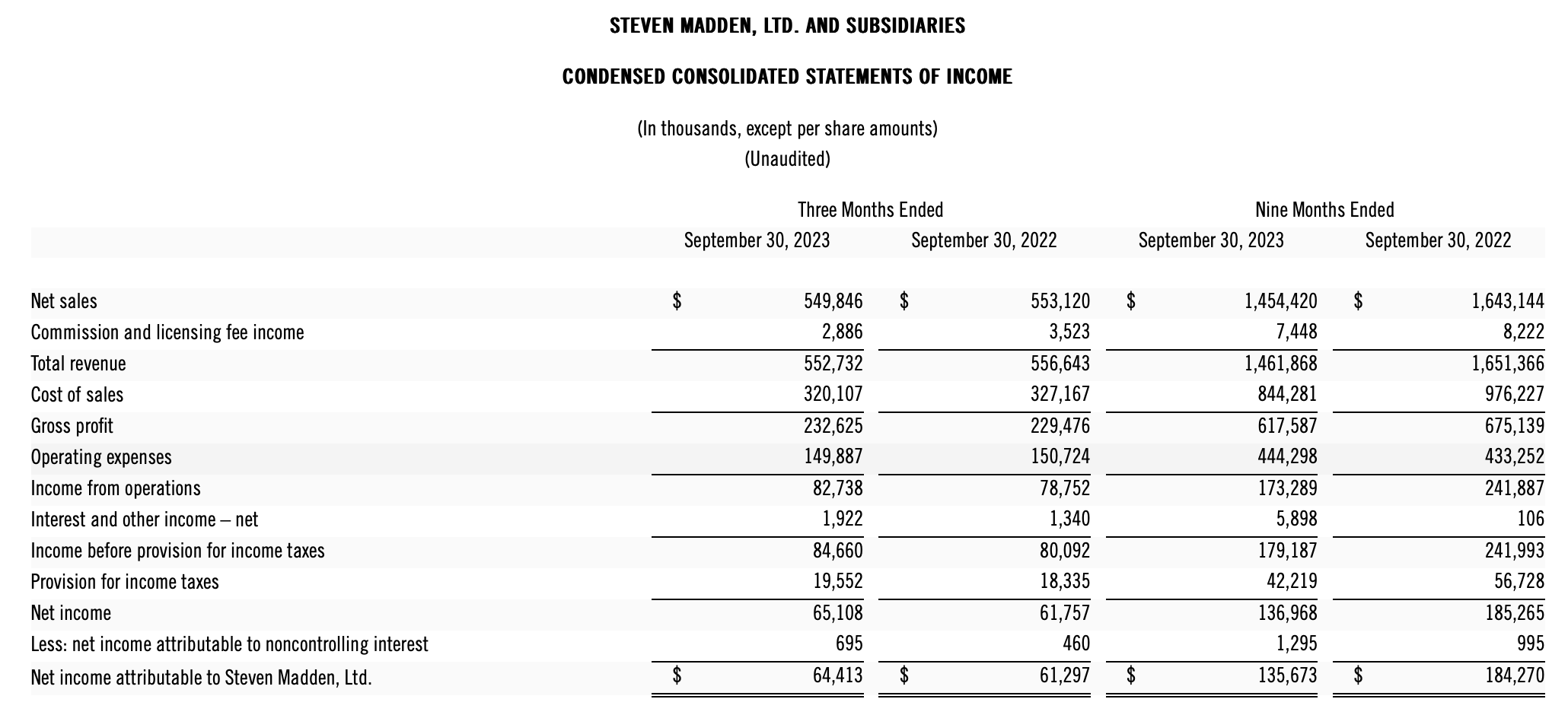

At first glance, a look at its results for the first nine months of 2023 (9m 2023) makes the price rise puzzling. Its revenues declined by 11.5%, which is far more than the company's expectation of a 6.5-8% decline in 2023. It performed better on the earnings per share ((EPS)) front, which came in at USD1.81 for the period. At this rate, it would make it to the full-year guidance range of about USD2.40-2.50. My calculation indicates that it would end up with a USD2.41 figure.

However, a closer look at the standalone figures for the third quarter (Q3 2023) reveals the reason for the optimism. First, revenue declined during the quarter, but it amounted to a small 0.7% decline, and second, all profit categories improved, aided by actual declines in both cost of sales and operating expenses.

{kind=link}

While gross profit grew by 1.4% year-on-year (YoY), operating and net profit grew by 5.1% each. Notably, the operating margin in Q3 2023 rose to 15%, appreciably higher than the 11.9% for 9m 2023. The net margin (for income attributable to the company) also crossed the 10% mark. It came in at 11.7%, up from 9.3% for 9m 2023.

This was a clear reflection of improving performance after a challenging first half of the year for Steven Madden. Further, by the time the earnings release came in, in November, the stock was still trading close to its September lows. The stock would have looked particularly attractive at a time when the S&P 500 Consumer Discretionary index was up by more than 20% YoY.

Improved performance and dividends ahead

There's even better news for Steven Madden as it readies for its full-year earnings update due in February. Even considering that it expects a 7% revenue decline for 2023, in Q4 2023, it will still see a 10% rise in the number. Further, with the diluted income per share expected to come in at USD2.35, the figure for the final quarter will grow by 28.6%.

Further, analysts expect the numbers for 2024 to be positive as well , with revenues seen rising by 8.6% and EPS expected to rise by 13.3%.

This also bodes well for Steven Madden's dividends. Its forward dividend yield is at 2%, which is a shade lower than the 2.2% for the consumer discretionary sector. However, considering that its TTM dividend payout ratio is 38% there is definitely room for an increase here especially as its earnings are expected to grow. While the stock's five-year returns are underwhelming, the addition of dividends has improved them (see chart below), making it a point to consider.

{kind=link}

The downside

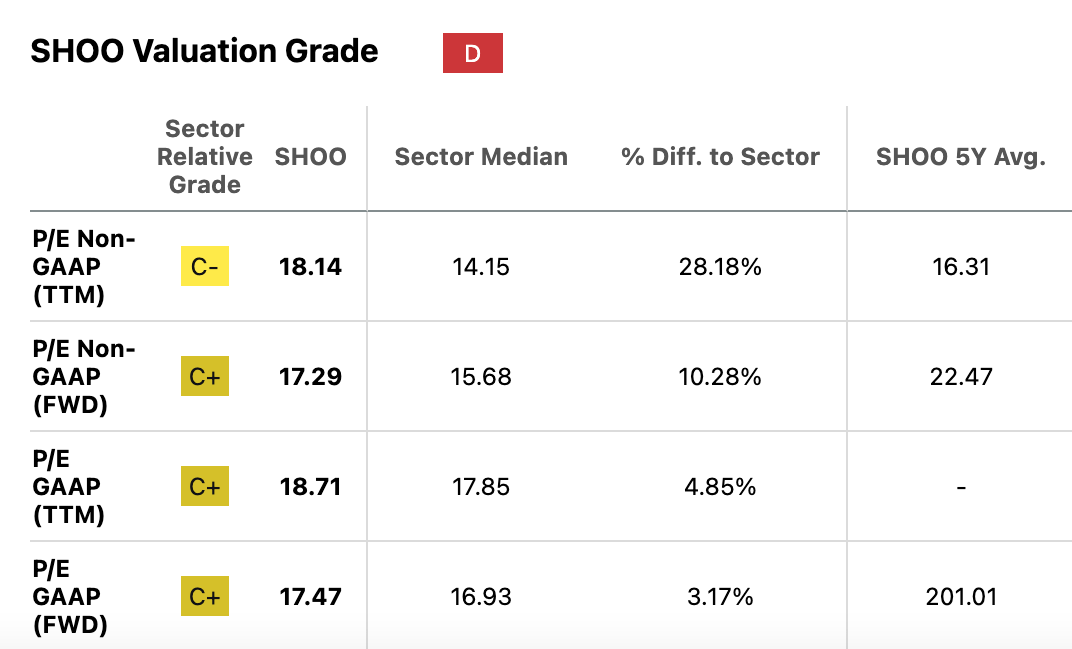

It's not like there won't be challenges ahead for the stock though. As a result of its price rise in the past few months, its market multiples are ahead of sector averages (see table below), indicating limited upside to the stock, if not a correction.

{kind=link}

The only exception is the soon-to-be TTM GAAP price-to-earnings (P/E) ratio for 2023, which is at 17.6x. This is slightly lower than the average for the consumer discretionary sector at 17.85x. However, even this doesn't imply any significant upside.

Further, the macroeconomic conditions might not be favourable either. The US economy is expected to see a slowdown this year. And while the rapid easing in inflation rates over the past year has been positive for the company's margins, there are likely to be limited margin gains in the next year.

To my mind, this can put the 2024 forecast at risk. In its Q3 2023 earnings release, company CEO Edward Rosenfeld did point this out saying, "softer trends across the industry since September have left us incrementally more cautious on the near-term outlook." He doesn't specify what near-term means, but it likely means at least the early part of 2024 since its outlook indicates positive expectations for Q4 2023.

What next?

All said, though, Steven Madden does look much better placed now than it did last April. The company seems to have come out of the worst of the slowdown it saw earlier last year. From the final quarter of 2023, it will likely see good growth and earnings expansion as well. The forecasts for 2024 are encouraging too.

It's little wonder that the share price has risen in tow, especially considering that it was a laggard as consumer discretionary stocks rose over the year. However, the stock's market multiples now suggest that there's little upside. And the company's caution about the near term coupled with the expected slowdown in the US and limited room for margin expansion does indicate that it might not be entirely out of the woods.

I believe the prudent action right now is nothing. It's best to wait for its full-year 2023 results due next month to see how Steven Madden expects to perform this year and make an investing decision based on that. What's clear for now is that it's no longer a Sell. I'm upgrading SHOO to Hold.

For further details see:

Steven Madden: Better Performance Expected (Rating Upgrade)