STC - Stewart Information Services: Waiting For Better Times

2023-08-14 02:29:15 ET

Summary

- Stewart Information Services Corporation is in the property and casualty insurance industry.

- STC holds a 10% market share in the title market and operates in multiple countries.

- The company is facing challenges in the current market environment but has the potential for growth in the future.

Introduction

Stewart Information Services Corporation ( STC ) is in the property and casualty insurance industry. As many are aware, there was a lot of uncertainty in the last few months for the financial sector as the turmoil of some regional banks seems to have dragged the whole sector down with it. When looking at the chart for STC it seems clear the share price is recovering. What has me very worried however is the fact that the valuation is incredibly high for an insurance company, with a p/e of 24.

I think that investors that want a potentially undervalued should be looking elsewhere right now. STC offers far too much downside risk right now to be suitable as a buy case. They may hold a strong position in the title market where it makes a lot of its revenues, but that doesn't constitute that the valuation should be where it is right now in my opinion.

Company Structure

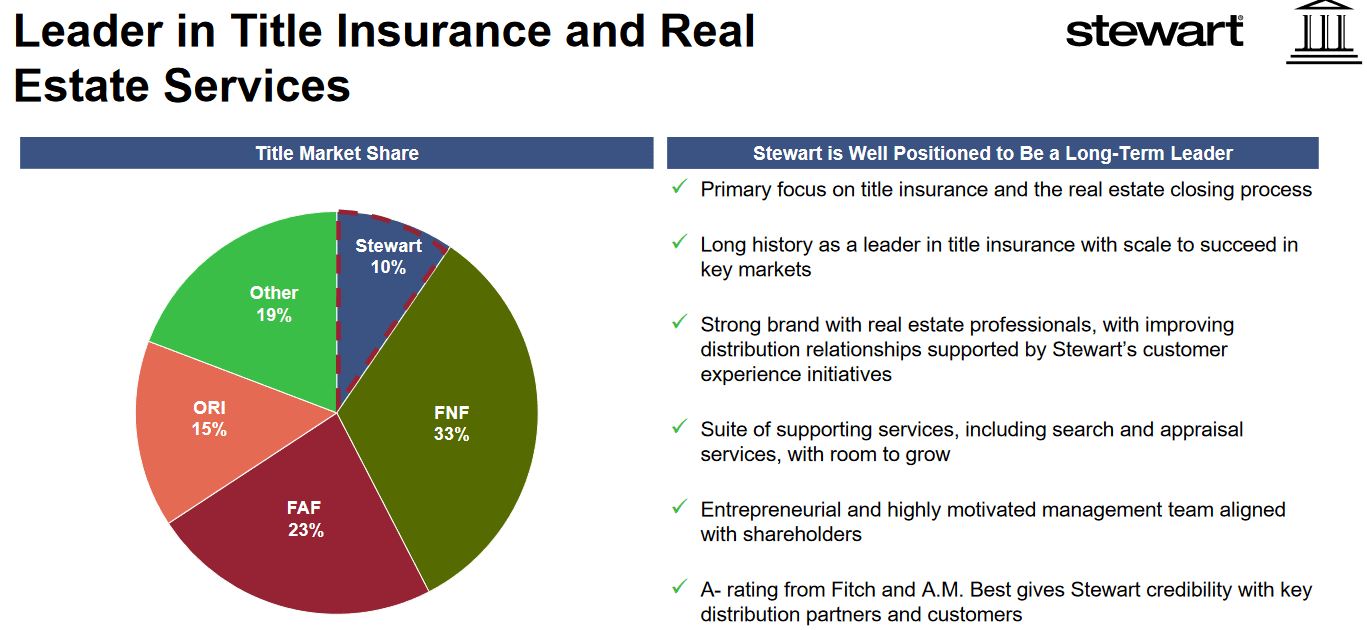

In the title market STC has made a name for itself and according to their last investor presentation they hold a 10% market share here. The history of the company is rich and dates back to 1893 and today it focuses on providing title insurance and real estate transactions related services.

Within STC two segments make up the company structure. These are the Title segment and the Real Estate Solutions segment. With the first one, the operations circulate searching, examining, and ensuring the condition of the title to real property. Besides these services, they also offer home and personal insurance services. The second segment provides appraisal management and credit and real estate information for both home buyers and sellers in the market.

{kind=link}

Within the title insurance market, STC has gained a remarkable share of it at around 10%. This doesn't necessarily make them the largest compared to the other 4 major companies STC makes up the lowest portion of it. But what I find positive about this is that STC might have an easier time gaining more market share from competitors. They are operating more from an attacking position than from a defense competition. For STC the capital expenditures do make up a decent portion of the earnings. In 2022 they landed at $47 million compared to $162 million in net income. That doesn't seem to have constituted a solid growth in terms of revenues. Instead, the revenues have decline significant which also comes from deteriorating market conditions. Going forward, noting the capital expenditures compared to net income will be important.

{kind=link}

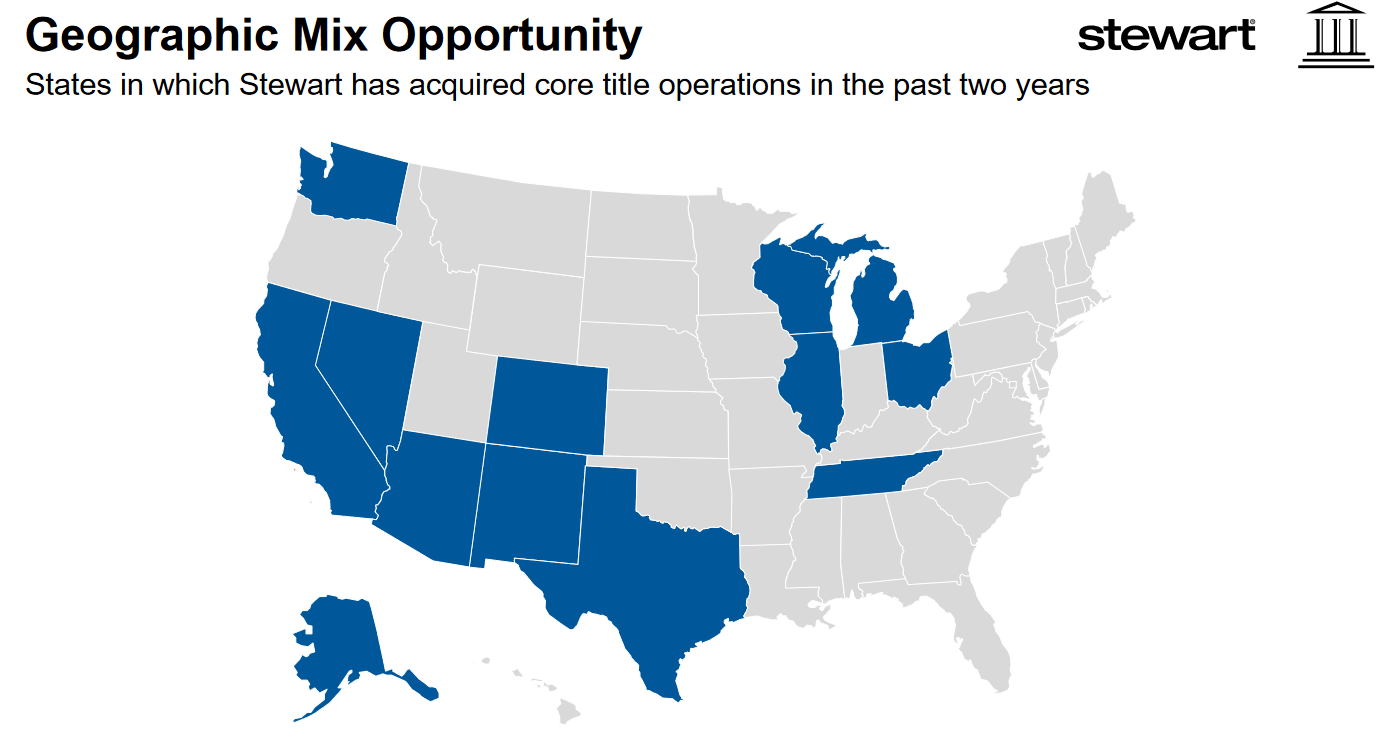

Looking at where STC has established itself it consists of some of the largest markets in the US, those being Texas and California. But what is worth noting is that STC also operates in Canada, the United Kingdom, and Australia. What has been positive from the rise of the interest rates is that STC now generates stronger investment incomes than ever. In Q2 2023 the investment income came in at $12.1 million, a rise of 80% YoY.

Earnings Transcript

On July 27 we got the earnings call from STC and the CEO of the company Frederick Eppinger had the following to say.

-

"In difficult markets such as the current, it is often indeed a focus on achieving these long-term goals. However, I'm very pleased with our progress on these enterprise initiatives during the second order, and are not serviced with improving our long-term performance".

The current market is admittedly difficult to work in and STC has made this quite apparent. The focus now should be on solid margin retention rather than significant top and bottom-line growth.

-

"So, the active new homes is strong although listings for existing homes remains very low. We expect the challenges of this environment to continue throughout 2023. We advantage cost carefully throughout this market, while on our long-term strategy, which requires a careful balance between investing in initiatives and managing expenses".

Looking at where we are heading it seems that some struggles are going to continue and we aren't completely out of the woods yet. With a slowing market of new homes, there is less availability for STC to generate revenues from. It seems that the priority for the company is to just get through this slump in the market and hopefully sentiment will recover in 2024. From there on out I think the future looks bright, which is why I still have a hold rating for the company.

Valuation & Comparison

GGM Model (Author)

Looking at the model above here we see that STC might be able to generate a decent return to investors. The company has a very high payout ratio that is nearing 75%. Going forward I am anticipation a 5% annual dividend increase. This seems quite in line with what is possible as the historical growth is over 7%. The share price however necessary to secure these returns is below where STC trades today and that does negate a buy case right now. However, if we raise the dividend increase to 7% instead, then the target price lands at $60. That is above where STC is today. For me, this comes down to whether or not you think STC can keep up the historical growth or not. I tend to lean towards being more conservative and that results in the target being below where it's trading today.

Risk Associated

This observation underscores a higher vulnerability to risks specific to the company, distinct from broader market fluctuations. While market risks cannot be disregarded, the focus here is on the unique challenges that the company itself might encounter within its operational landscape.

It's important to acknowledge that in the current economic landscape, the Federal Reserve's hawkish stance has been a defining factor. Coupled with a collection of indicators pointing towards the persistence of inflationary pressures, the scenario becomes more intricate. The company's stock price might experience a heightened level of strain, particularly as the calendar turns to the second and third quarters of 2023.

Growth Opportunity (Investor Presentation)

The Federal Reserve's monetary policy decisions have a direct impact on the interest rate environment, which subsequently influences borrowing costs and investment decisions. The prevailing hawkish stance suggests that the trajectory of interest rates might continue on an upward path, potentially affecting various sectors and industries. In this context, the company's specific operations and business model must be closely scrutinized for their capacity to absorb and adapt to these changes.

Investor Takeaway

For investors that want to get a growth opportunity in the title insurance market then STC could be one, but the market environment seems quite volatile and uncertain now to make any concrete assumptions. I lean towards a more conservative valuation in most cases and this has unfortunately showcased STC as a slightly overvalued play right now. However, the quality of the business leads me to rate it a hold at least.

For further details see:

Stewart Information Services: Waiting For Better Times