RCA - Stop Chasing 'Sucker Yield' Syndrome

2023-03-22 07:00:00 ET

Summary

- This desire to own the newest and supposedly greatest is often irrespective of the practical need for it.

- Many investors suffer from this constant need to chase yield, only to be disappointed later.

- I know some of you may not like what I have to say, but if I can steer one investor away from dangerous sucker-yielding stocks, I’m satisfied.

The shiny toy syndrome is characterized by wanting to own the latest glittery new toy and getting an intense but temporary sensation of happiness from the ownership, before it fades.

I remember when I was a kid I always wanted a train set, and when Santa delivered one, I would spend hours entertaining myself. However, months later the excitement was over, and I would move on to the next big thing.

This desire to own the newest and supposedly greatest is often irrespective of the practical need for it. The shiny toy syndrome doesn't only apply to physical things: many investors suffer from this constant need to chase yield, only to be disappointed later. A 1920's Wall Street writer, Frank J. Williams, summed it up as follows:

"People of the dupe type are hypnotized by the glare of gold. They stare so long at glistening fortune that their minds are brought under subjection to one of nature's strongest passions-greed. They will listen to any tip, however wild and ridiculous, and impulsively act on any suggestion."

In this bear market, there's no room for error and I have purposely decided to write more content on Seeking Alpha focused on risk avoidance.

It's natural to be attracted to shiny new high-yielding toys; research has shown that being exposed to novel experiences activates the release of dopamine in the central nervous system.

But when it becomes a consistent habit in the way you invest, it can be extremely damaging. Luckily, there are a few things you can do to develop self-awareness and combat the shiny toy syndrome, which of course is the purpose for this article…

Ready Capital Corporation ( RC ): 16.9% Sucker Yield

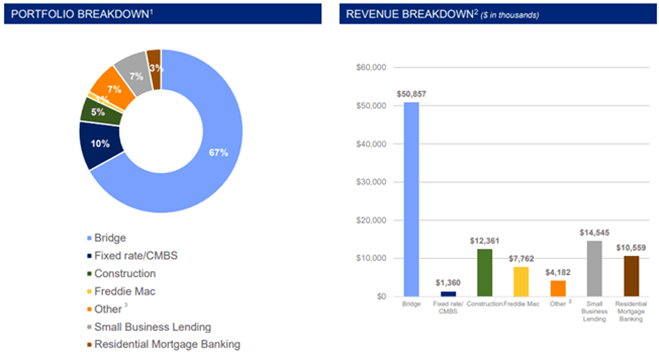

Ready Capital is an externally managed commercial mortgage REIT ("mREIT") that originates, acquires, and services commercial real estate loans and securities related to real estate. They have a $10.1 billion portfolio with 99% of loans having a senior lien. In total, they have more than 5,300 loans diversified across all 50 states & Europe.

Ready Capital has several lending products including small balance commercial loans ("SBC"), agency loans, residential mortgage loans, bridge loans, construction loans, mortgage-backed securities, and small business loans backed by the U.S. Small Business Administration ("SBA").

The largest loan product by both percentage of their portfolio and by revenue is bridge loans. A portion of the loans originated are held for investment (to receive interest income), and a portion is securitized and sold. Generally, they issue loans that are used by businesses or investors to acquire real estate including office, multifamily, retail, warehouse, or mixed-use real estate.

{kind=link}

Their largest business segment is their SBC lending business with $565.1 million in interest income as of December 31, 2022. Their second largest category is their Small Business lending segment that makes up $98.1 million in interest income, their smallest segment is residential mortgage banking with interest income of $7.9 million.

{kind=link}

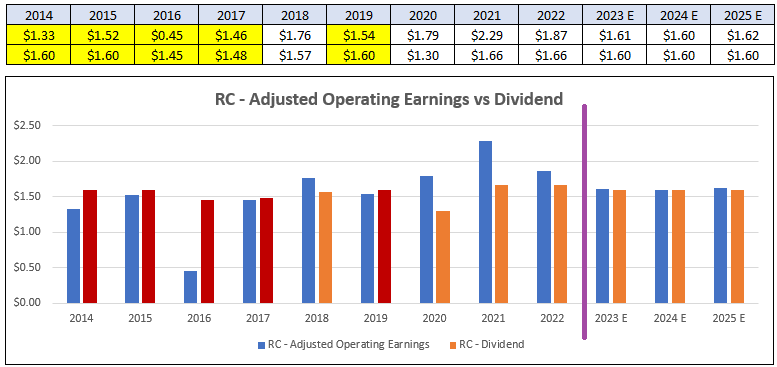

Ready Capital's adjusted operating earnings have had an overall growth rate of 2.82% since 2014. Earnings have been sporadic, with earnings increasing in 2014-2015, but then falling from $1.52 in 2015 to $0.45 in 2016 for a decline of 70%.

Earnings resumed growth from 2016-2018 but then fell again in 2019 by 12%. Finally, earnings fell from $2.29 per share in 2021 to $1.87 per share in 2022 for an 18% decline. Analysts expect further declines in earnings with projections for earnings to come in at 1.61 in 2023, 1.60 in 2024, and 1.62 in 2025.

In several years since 2014, Ready Capital's adjusted operating earnings have not covered their dividend. I marked each year in which the dividend exceeded earnings with a red bar. Between 2014 and 2019, earnings only covered the dividend in one year.

The dividend has been cut multiple times in this same period with cuts in 2017, 2020, and an expected cut in 2023. What's worse is that their dividend has just recovered in terms of the rate paid with its current dividend slightly exceeding the amount paid in 2014.

By 2025, analysts expect the dividend to be cut back down to $1.60 per share , which would equal the rate paid in 2014. Since 2014, Ready Capital has had a negative dividend growth rate. Over the last 9 years, their compounded growth rate comes in at negative -2.68%.

{kind=link}

{kind=link}

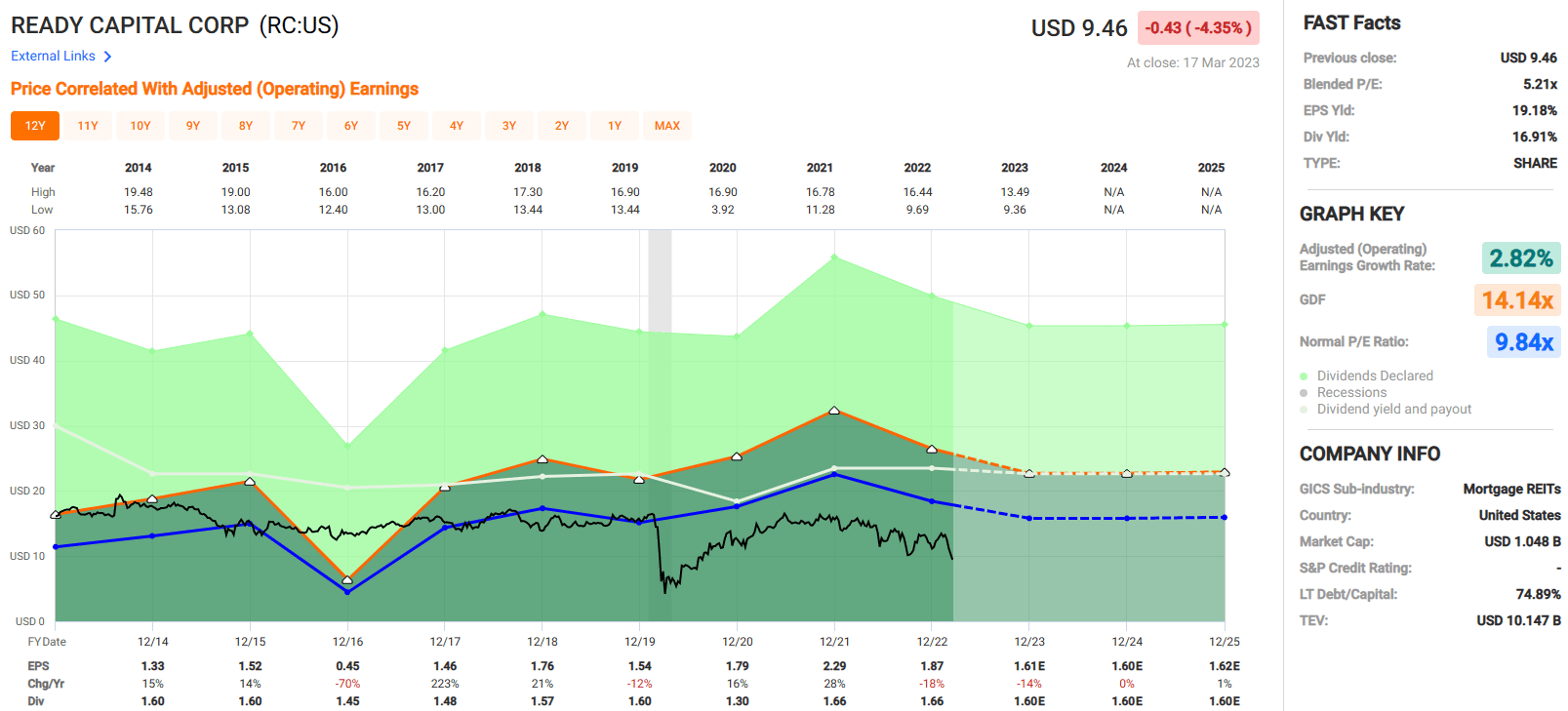

Another concern is the heavy share dilution over the last several years, but especially in 2022. Weighted average diluted shares outstanding numbered 68,660,906 in 2021 vs 117,193,958 in 2022 for a 70.68% increase in shares.

{kind=link}

In my opinion, Ready Capital is a REIT to avoid.

They pay a tempting 16.91% dividend yield, but this looks like a "suckers yield" to me. Their earnings are sporadic and only show a modest growth rate since 2014. In many years their earnings don't cover the dividend and analysts expect earnings to decline significantly in 2023.

If analysts' projections hold up, RC's earnings next year will barely cover its dividend, which could lead to further cuts. Ready Capital has shown a history of cutting their dividend which leads me to believe the company is at a risk of another cut given analysts' expectations of declining earnings.

{kind=link}

Annaly Capital Management, Inc. ( NLY ): 14.1% Sucker Yield

Another REIT I would avoid is Annaly Capital Management. NLY is an internally managed mREIT that invests in debt instruments collateralized by residential real estate. Annaly does business through three investment groups.

Their agency group is their largest segment and invests in residential agency mortgage-backed securities ("MBS") that are backed by agencies including Fannie Mae, Ginnie Mae, and Freddie Mac. NLY's second investment segment is its residential credit group which invests in non-agency loans consisting of both whole and securitized residential loans.

The last segment is their Mortgage Servicing Rights ("MSR") Group that allows them to service residential mortgages in exchange for a percentage of the interest payments made.

{kind=link}

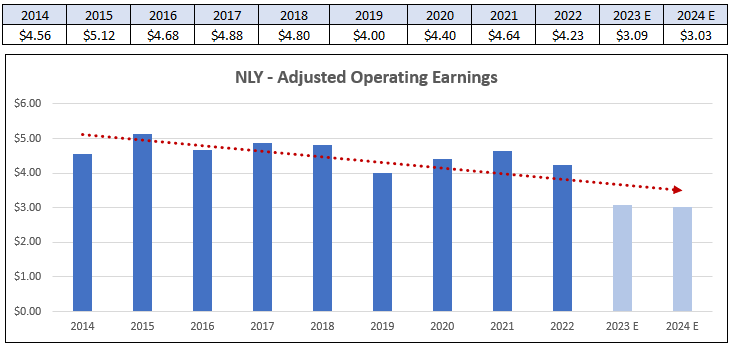

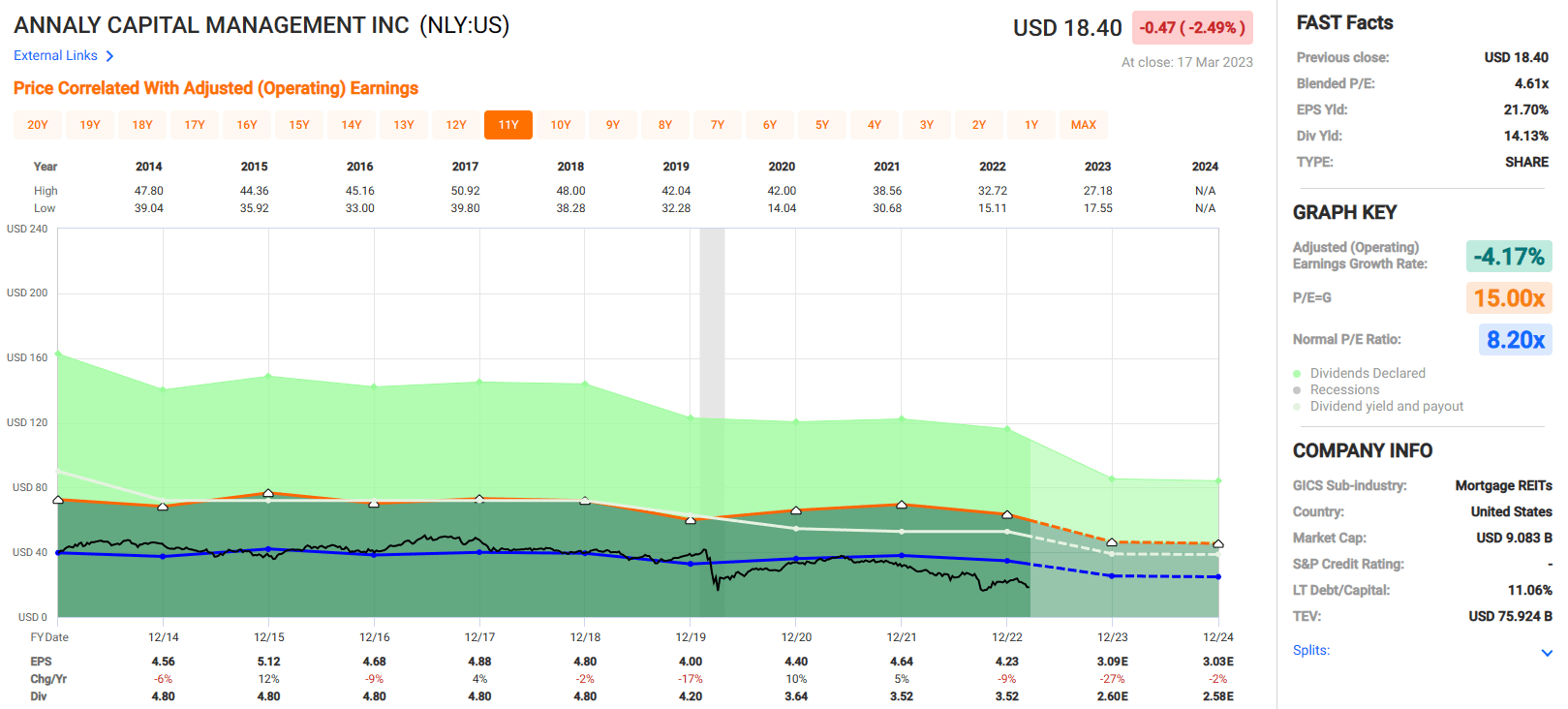

Annaly's adjusted operating earnings have been declining since 2014 with an overall growth rate of negative -4.17%. Earnings fell -6% in 2014, -9% in 2016, -2% in 2018, -17% in 2019, and -9% in 2022. A significant decline in earnings is expected by analysts in 2023, with earnings projected to fall by -27%.

{kind=link}

NLY has been able to cover the dividend with adjusted operating earnings over the past 3 years with payout ratios of 82.73%, 75.86%, and 83.22% in the years 2020, 2021, and 2022 respectively. Unfortunately, they have reasonable payout ratios based on operating earnings due in part to the serial dividend cuts they have made over the last several years.

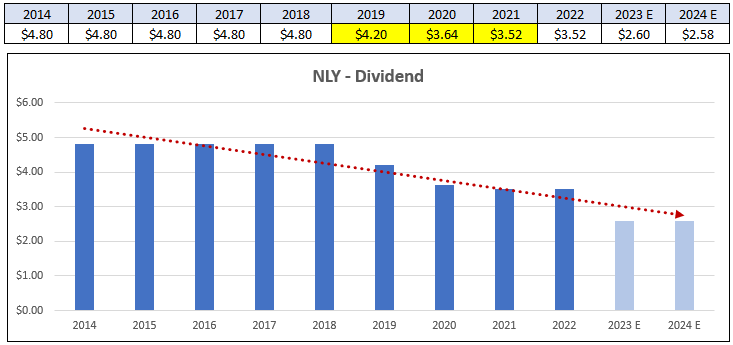

From 2014 to 2018 they maintained their dividend at $4.80 with no increases. Then they cut the dividend in 2019 from $4.80 to $4.20, then cut it again to 3.64 in 2020, then cut it again to $3.52 in 2021.

It was not raised in 2022, and in 2023 analysts expect a significant dividend cut of 26.14%. In total, the dividend average "growth rate" has been negative -5.46% since 2014.

{kind=link}

{kind=link}

While NLY pays a juicy dividend yield of 14.13% and is trading at almost half its normal multiple, this is another REIT that looks like a "suckers yield" and one I would avoid.

They have a negative rate of growth for both earnings and their dividend with significant declines in both expected in 2023 by analysts. If analysts' projects hold up, Annaly's dividend will be $2.58 in 2024, approximately half of the $4.80 they paid in 2014. While the yield and price discount can be tempting, this is another REIT I would avoid.

{kind=link}

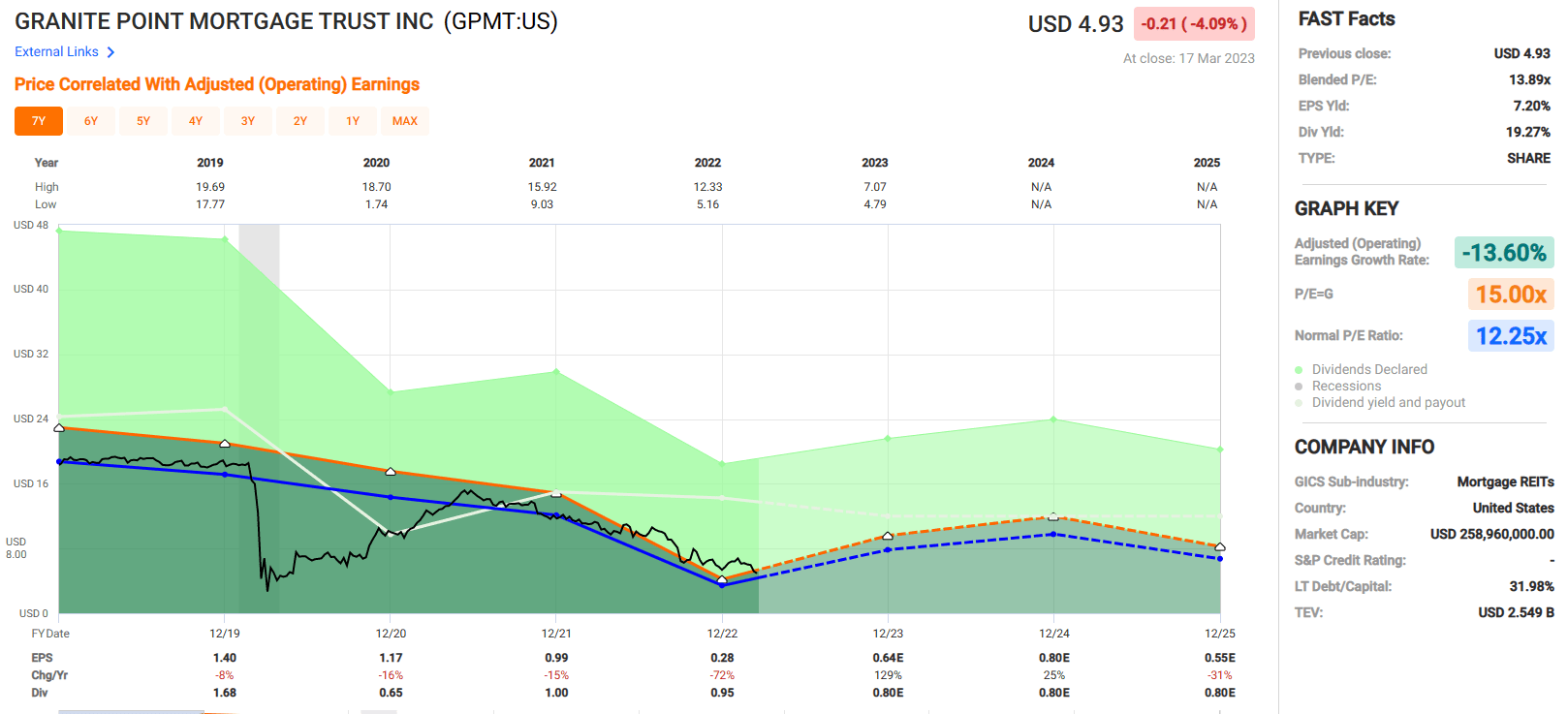

Granite Point Mortgage Trust Inc. ( GPMT ): 19.3% Sucker Yield

Granite Point Mortgage Trust is an internally managed mREIT that originates, invests in, and manages senior floating-rate commercial loans and other types of commercial real estate debt. Their debt investments are primarily senior loans with senior loans making up 99% of their investments.

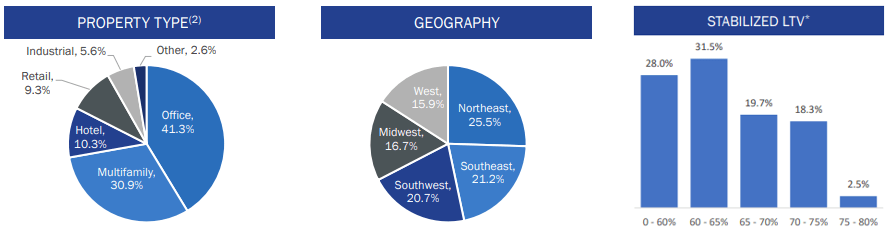

Their loans are conservatively underwritten with a weighted average stabilized loan-to-value ("LTV") of 62.9% at origination. 28% of GPMT's portfolio has an LTV under 60% while 31.5% of their portfolio has an LTV between 60-65%. Only 2.5% of their portfolio has a loan-to-value between 75-80%.

GPMT's collateral is well spread out across different areas of the country and consists of multiple property types including office, multifamily, hotels, retail, and industrial. Their largest two categories are office at 41.3% and multifamily at 30.9%.

{kind=link}

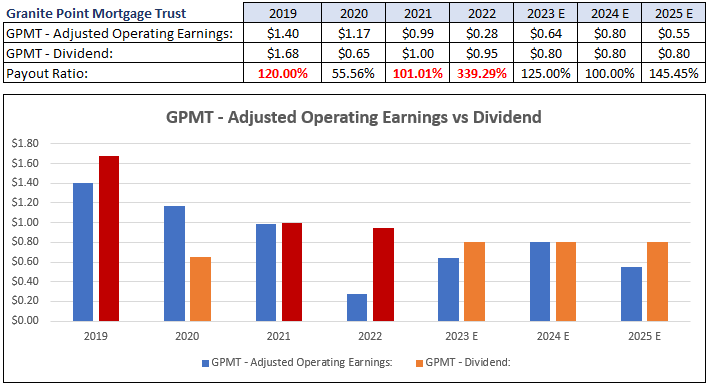

Since 2019, Granite Point Mortgage Trust's adjusted operating earnings have had a blended average "growth rate" of negative -13.60%. Earnings dropped -8% in 2019, -16% in 2020, -15% in 2021, and a whopping -72% in 2022.

Analysts expect a large rebound in earnings in 2023 for an increase of 129%, another increase of 25% in 2024, but then expect earnings to fall -31% in 2025.

FAST Graphs (Compiled by iREIT)

GPMT hasn't done any better with their dividend. The dividend was cut by -61.31% in 2020, it was raised in 2021 but then cut another 5.00% in 2022. Overall, since 2019 their average dividend growth rate is a negative -2.19% and their compound growth rate is -12.49%.

Analysts expect another cut in 2023 to $0.80 and for the dividend to remain at that level until 2025. If estimates pan out, the dividend in 2025 will be less than half of what it was in 2019.

FAST Graphs (Compiled by iREIT)

{kind=link}

GPMT's payout ratio when based on adjusted operating earnings is even more concerning than their "growth" rates. Over the last 4 years, GPMT has paid out more in dividends than their operating earnings.

Only in 2020 did their earnings exceed the dividend paid. In 2019, they had a payout ratio of 120.00%, in 2021 their payout ratio was 101.01% and in 2022 their payout ratio came in at 139.29%.

Analysts don't expect the payout ratio to improve with it projected to be 125% in 2023, in 2024 the payout is expected to be 100%, and in 2025 analysts expect the payout ratio to jump to 145.45%. I've highlighted the years between 2019 to 2022 with red bars to indicate when the dividend exceeded earnings.

{kind=link}

This is another REIT I would avoid. Their earnings and dividends have been declining over the past several years and analysts expect this trend to continue. What's more, the dividend does not appear safe with payout ratios of 100% or more in each year since 2019 and an expected payout ratio of 125% in 2023.

GPMT pays a very high dividend yield of 19.27%, but this looks like a suckers yield if I've ever seen one. Another dividend cut looks very likely given the high payout ratios and earnings that have been in decline.

To top it all off, this stock is actually trading at a premium to its normal multiple. Currently, GPMT trades at a P/E of 13.89x compared to its normal P/E of 12.25x. I would definitely avoid this one.

{kind=link}

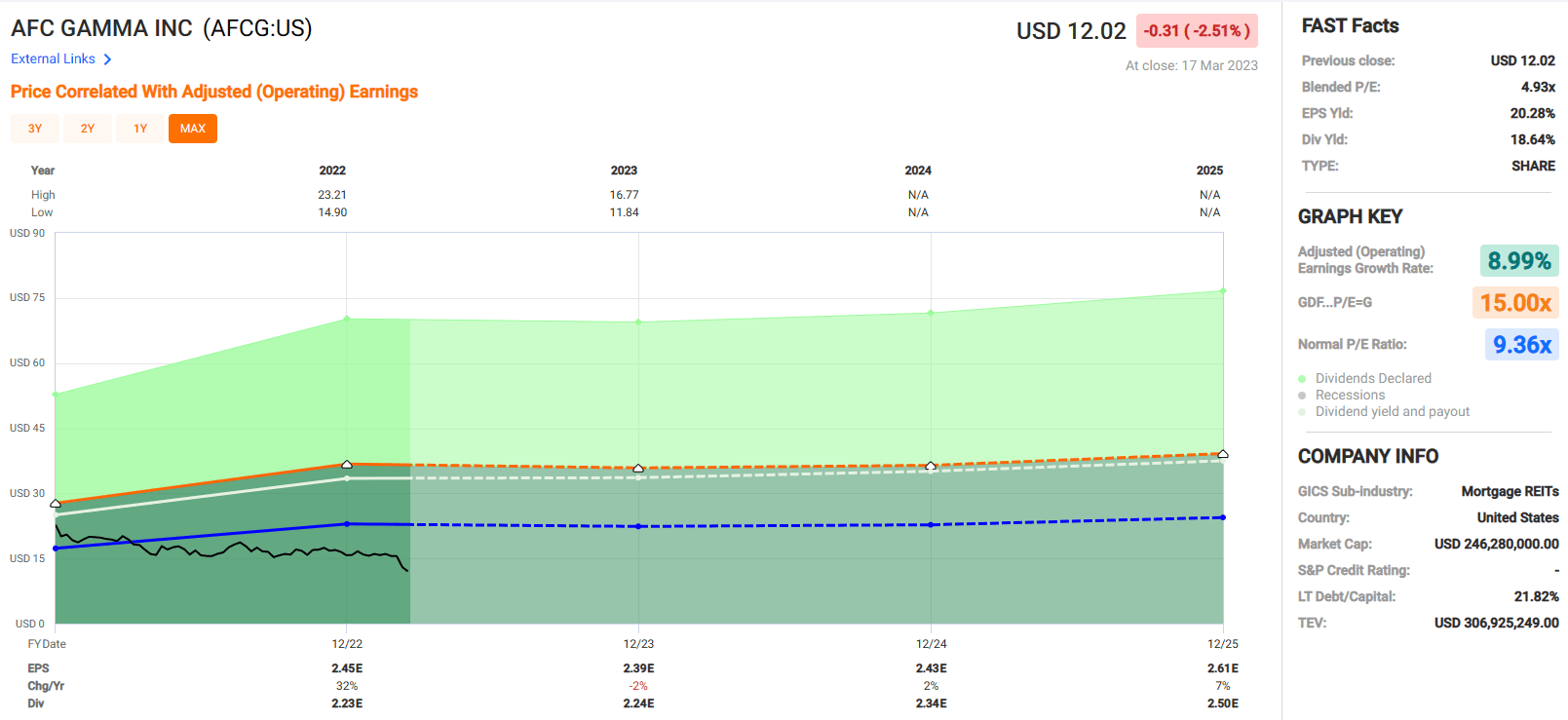

AFC Gamma, Inc. ( AFCG ): 18.6% Sucker Yield

The last REIT that we will cover today is another one I'd stay away from. AFC Gamma is an externally managed mREIT that originates and invests in secured loans that are collateralized by commercial real estate.

AFCG was primarily a lender to operators in the cannabis industry but has recently overhauled its investment strategy to invest in debt instruments backed by commercial properties across multiple real estate sectors.

They now invest in first and second-lien mortgage loans, bridge loans, direct loans, and mortgage-backed securities. AFCG just went public in early 2021, but approximately two years later they felt it necessary to make a strategic shift to include other property sectors and offer additional debt instruments.

What's most alarming is that AFCG recently disclosed it had not invested in any new cannabis debt instruments in the last 9 months. For a company that started as a lender to the cannabis industry, it is concerning that they have all but retreated from this strategy given that they have not made an investment in this space over the last 3 quarters.

{kind=link}

Recently I wrote on AFCG and went into more detail on their strategic shift. Suffice it to say that I see a lot of red flags with this change in strategy and downgraded AFCG to a sell. You can read the full article at the link below:

Cannabis REITs: Separating The Weed From The Chaff | Seeking Alpha

As previously mentioned, AFCG just went public 2 years ago (March 2021), so we really don't have much to work with regarding earnings and dividend history.

Between 2021 and 2022 AFCG increased its adjusted operating earnings by 32%, but this will normalize and should not be used to reflect future growth rates. Analysts expect earnings to decline by -2% in 2023, but then to increase by 2% in 2024 and then increase by 7% in 2025. If analysts' estimates are correct, AFCG won't surpass its 2022 earnings level until 2025.

FAST Graphs (Compiled by iREIT)

Similar to AFCG's earnings, we don't have a lot of dividend history to review. Analysts expect the dividend to increase each year until 2025, but at their current dividend rate, AFCG has a payout ratio of 91.02% when based on adjusted operating earnings.

This does not leave much room for error. AFCG's earnings will need to come in as analysts expect in order to support the dividend, but for the year we have, the dividend is covered, but with an uncomfortably high payout ratio.

FAST Graphs (Compiled by iREIT)

AFCG is currently trading at a significant discount to its normal multiple. Its current P/E is 4.93x compared to its normal P/E of 9.36x. Additionally, AFCG has a very high dividend yield of 18.64%. In this case, I think the discounted price is warranted and the high dividend is a suckers yield.

We really can't get a good fix on earnings and dividend growth rates, but what we do know is they already have a high dividend payout ratio at 91.02% of their operating earnings and analysts expect earnings to decline in 2023 and not exceed their current levels until 2025. At the same time, analysts expect the dividend to increase consecutively over the next 3 years.

If projections for both earnings and the dividend are accurate, this will only put additional pressure on their payout ratio. Above all else is my concern with the change in investment strategy.

The company appears to be in disarray, and at this point, there doesn't seem to be any "real" strategy which makes me question management's planning and execution. At iREIT, we rate AFCG a sell and this is certainly a REIT I would avoid.

{kind=link}

In Closing

When I reflect on my experience as a developer (for over 30 years) and REIT analyst (for 13 years), I can assure you that I have plenty of battle scars. Hopefully, you know by now that I'm all about protecting the principal at all costs.

I've seen multiple recessions, and in the last "great one" I transformed myself into a battle-tested investor who understands the concept of principal preservation. One of the worst things that any investor should be today is to chase yield and I insist that you understand how to play the game.

"People suffered the agony of financial loss and many had to start life over again because they would not take the trouble to learn the rules of the game they were playing (in 1929)." Frank J. Williams.

I know some of you may not like what I have to say, but if I can steer one investor away from dangerous sucker-yielding stocks, I'm satisfied.

"This is a matter of cold, hard common sense and safety. It is absolutely unsafe to gamble in stocks unless the trader can protect himself at all times. It is wiser to build up a substantial reserve before invading the stock-market than to fritter away money in hopeless attempts to beat it." Frank J. Williams.

For further details see:

Stop Chasing 'Sucker Yield' Syndrome