SEOJF - Stora Enso: Turning Bullish Thanks To Strong Growth Prospects

2023-04-19 10:30:00 ET

Summary

- Stora Enso is a Finnish company strengthening its focus on cardboard packaging rather than paper.

- 2022 was great, 2023 will be more challenging but the operating cash flow should remain very robust.

- The company kicked off a 1B EUR conversion project with an anticipated return on operating capital of 20%.

- I'm not expecting much from Stora in 2023, but the longer-term future looks good.

Introduction

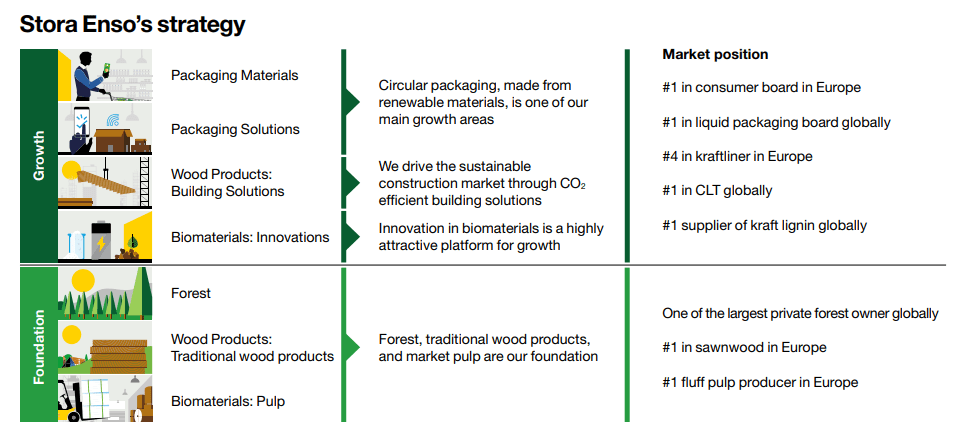

Stora Enso ( OTCPK:SEOAY ) ( OTCPK:SEOJF ) has reinvented itself in the past 15 years. Whereas the company was best known as an almost pure paper-focused player, the company has recently sold its final paper-related assets and is investing heavily in cardboard and pulp based packaging solutions . Stora Enso rapidly gained market share in Europe and is currently one of the largest packaging-focused companies in Europe.

{kind=link}

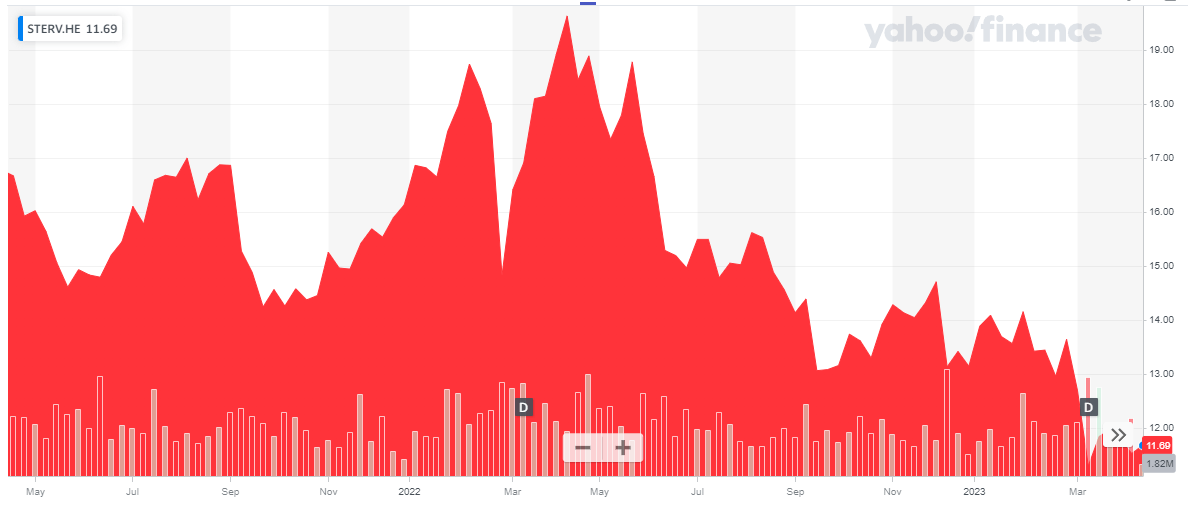

As explained in a previous article, Stora Enso has two types of shares, but in this article I will focus on the R-shares trading with STERV as the ticker symbol on the Helsinki Stock Exchange . Not only is this the most liquid listing with an average daily volume of approximately 1.8M shares per day versus just a few thousand for the A-shares , the Helsinki listing is in EUR which makes it easier to discuss the per-share results as Stora reports its financial results in the same currency. There are a total of 789M shares outstanding resulting in a market cap of just over 9.2B EUR using the share price of the R-Shares at the closing bell on Monday, April 17. The only difference between the shares are the voting rights: an R-share has 1/10th of a vote while the owner of an A-share is entitled to a full vote. As I'm interested in making a profit on the shares and have no intention to be an activist investor, the focus of this article will be on the R-shares which are trading at a 10% lower share price but offer the same economic benefits.

{kind=link}

2022 was great

2022 was a great year for the company and although we shouldn't expect Stora to be able to repeat the excellent performance in 2023. The exceptional results last year paved the way to rapidly improve the balance sheet and generate enough cash flow to start a heavy investment cycle this year.

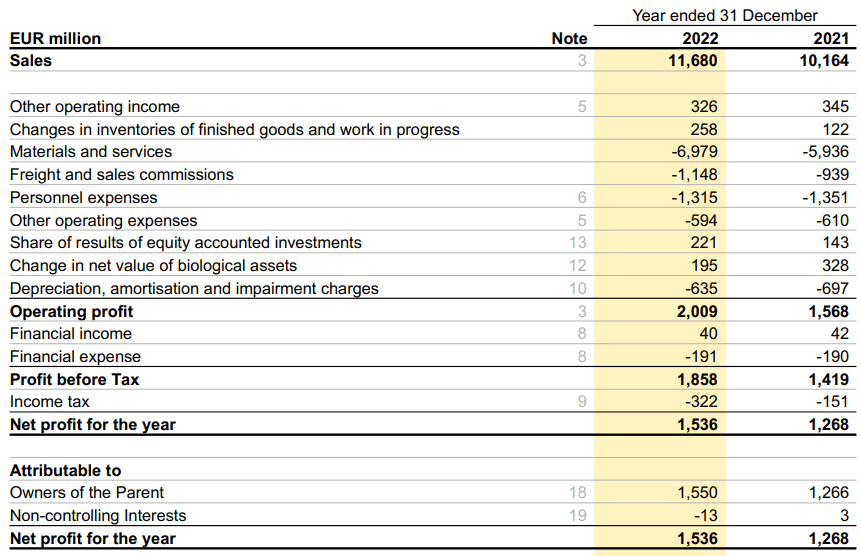

The total revenue in 2022 was 11.7 BEUR , an increase of approximately 15% compared to the revenue in 2021, and this resulted in a 300% increase in the operating profit. And as you can see below, even despite a higher average tax rate, the net income of 1.54B EUR was a clear improvement compared to the 1.27B EUR in FY 2021.

{kind=link}

Including in the reported net income is a 13M EUR loss attributable to non-controlling interests which means the net income attributable to the shareholders of Stora Enso came in at 1.55B EUR for an EPS of 1.97 EUR. That's about 20% higher than the 1.61 EUR per share in 2021.

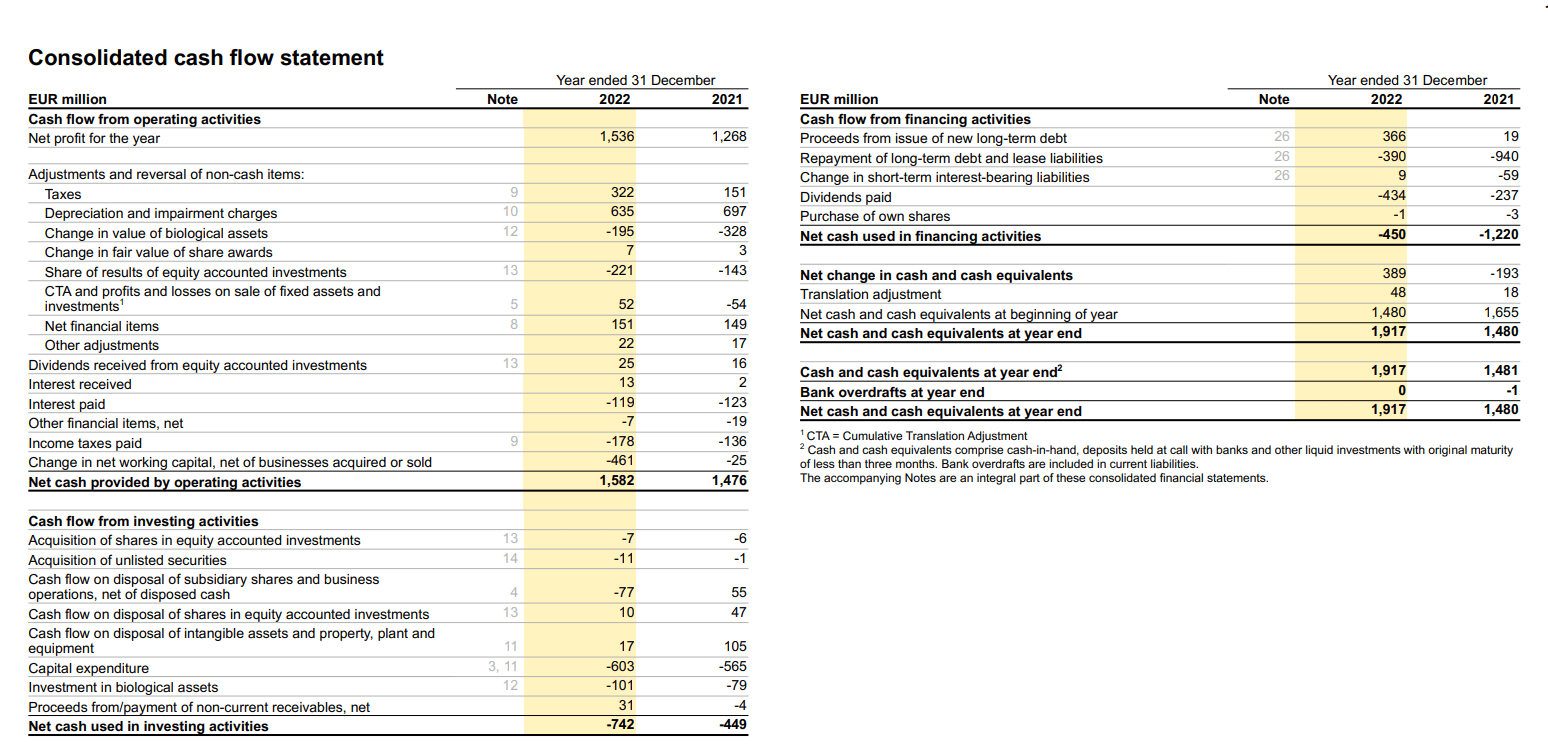

The company's free cash flow result was a bit weaker as the income statement contained an attributable income of 221M EUR from equity accounted investments but those investments paid a dividend of just 25M EUR. And as you can see below, this means the 221M EUR in income was deducted from the operating cash flow calculation. The total operating cash flow was approximately 1.58B EUR but this includes just 178M EUR in taxes (while 322M EUR in taxes were due) and it includes a 461M EUR working capital investment. This means the adjusted operating cash flow was approximately 1.9B EUR (with one caveat: I couldn't find the exact amount of lease payments made by Stora during 2022).

{kind=link}

The total capex was 704M EUR (I'm using the 603M EUR capex and the 101M EUR purchase of biological assets) resulting in a free cash flow result of approximately 1.2B EUR. That's 1.52 EUR per share. This difference with the EPS could easily be explained by Stora spending more on capex than the depreciation expenses were and the obvious delta between the attributable income from equity investments versus the total amount of dividends received from those investees.

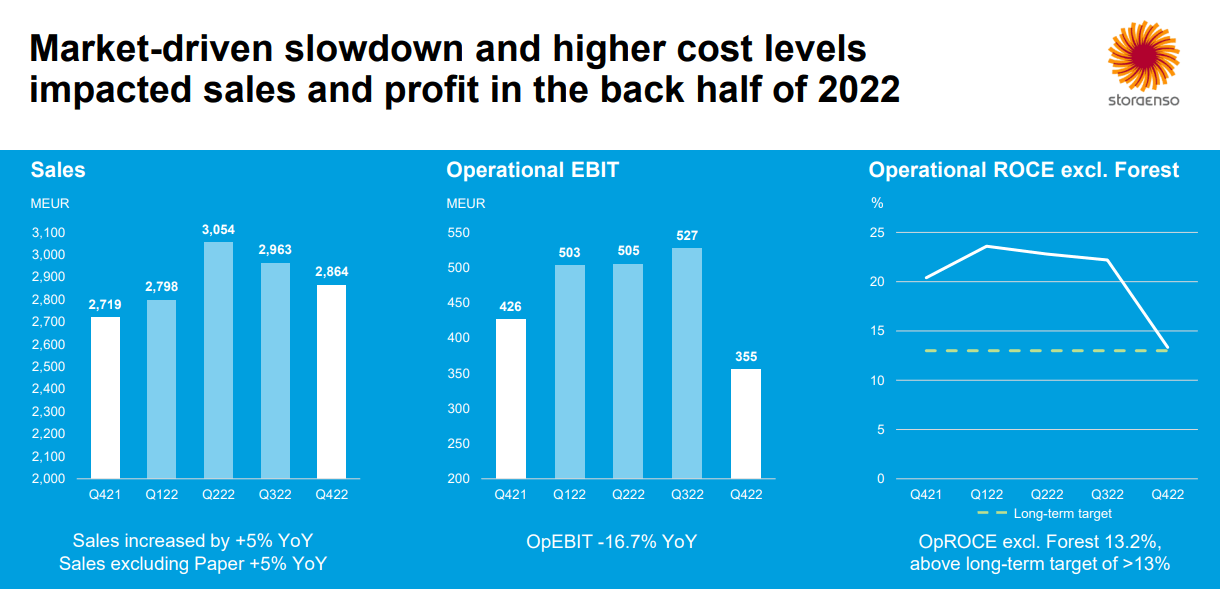

2023 will be more challenging: expect a lower EBIT and a much higher capex

Despite recording in excess of 3.5 EUR per share in net income in the past two years, Stora's share price has been sliding throughout the year as the financial performance weakened as the year progressed.

{kind=link}

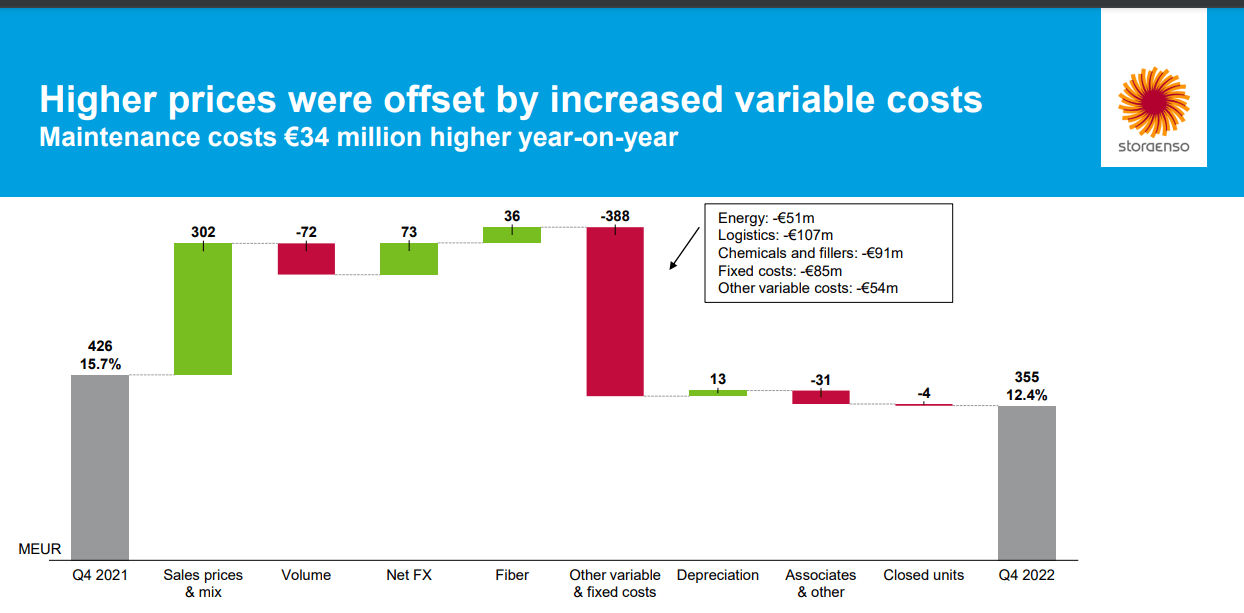

Q4 2022 wasn't great either but although I do think and expect the temporary tailwinds to be over, there still is plenty of value at Stora Enso.

{kind=link}

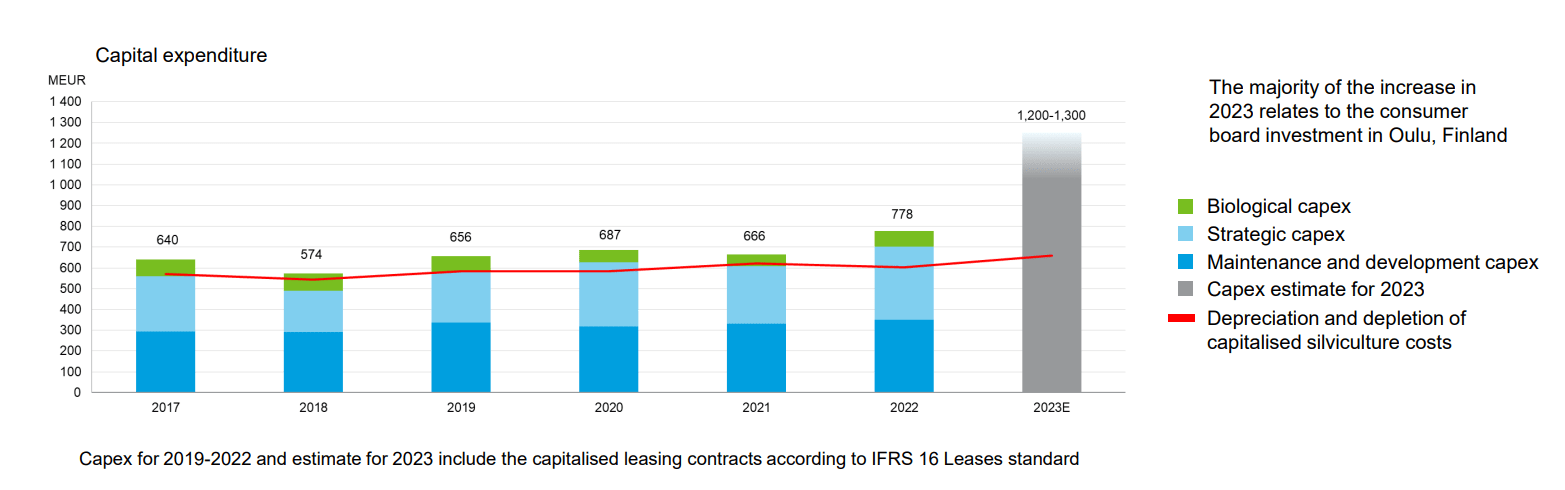

First of all, it's important to understand what the total level of capital expenditures is about. The image below shows the underlying sustaining capex and biological capex was just 450M EUR in 2022. This means the underlying free cash flow result in 2022 was approximately 30 cents per share higher than the 1.52 EUR indicated by the cash flow statement.

{kind=link}

We also see Stora will aggressively ramp up its capex plans as the company will convert its Oulu paper mill into a plant producing additional packaging offerings. Stora will invest approximately 1B EUR and expects to generate a Return On Operating Capital of 20% on this investment when the new plant will be completed in 2025.

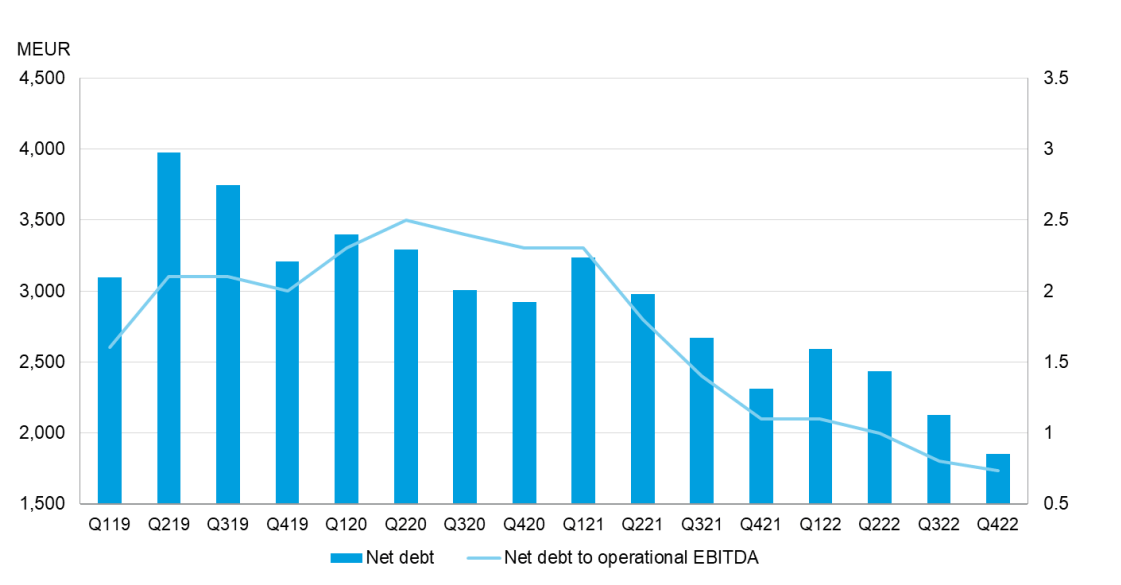

Fortunately the total incoming operating cash flow should be sufficient to cover the 2023 capex program. And I expect the net debt level to remain pretty stable while the debt ratio should have remained below 1 excluding acquisitions. But the recent completion of the acquisition of the Dutch De Jong Packaging Group will temporarily push the debt ratio to approximately 1.4-1.5 .

{kind=link}

Investment thesis

It is very unlikely Stora Enso will be able to repeat the excellent performance of 2021 and 2022 in 2023. But I do think this creates opportunities: Stora's share price is currently already trading 40% below the level it was trading at a year ago so the weakening performance likely is already included in the market perception. And as long as Stora is able to autonomously fund its expansion plans (and potential smaller M&A deals like the acquisition of De Jong ), I am for sure willing to cut the company some slack.

Stora's share price is currently approximately 30% lower than where it was trading at the last time I discussed the company , and patience is a virtue. I am getting increasingly interested in picking up Stora Enso, but investors will have to focus on the mid-term and longer term future of the company rather than hoping for a quick gain.

For further details see:

Stora Enso: Turning Bullish Thanks To Strong Growth Prospects