KBWY - Storage REITs: Victims Of Own Success

2024-01-17 11:00:00 ET

Summary

- Self-Storage REITs delivered incredible growth early in the pandemic driven by surging housing market activity, but have been victims to their own success of late amid a supply-driven cooldown.

- Robust double-digit rent growth and relatively low operational barriers to entry prompted a wave of new development, with a roughly 12% expansion in total supply expected between 2022 and 2024.

- This supply boom - twice the magnitude of the multifamily sector - has reignited fierce "storage wars" between competing facilities, which has led to double-digit dips in new lease rates since mid-2022.

- Storage demand is driven largely by housing activity – specifically, home sales and rental market turnover - and the recent moderation in mortgage rates has eased some concerns and sparked a rebound for self-storage REITs following a period of weak performance from mid-2022 through late 2023.

- Softer fundamentals combined with the surge in financing costs have hit the smaller, more highly-levered owners in these markets particularly hard. We expect storage REITs to leverage their stellar balance sheets to scoop-up highly-levered upstarts seeking an exit, providing some accretive external growth at a time of flat-to-negative organic growth.

REIT Rankings: Self-Storage

{kind=link}

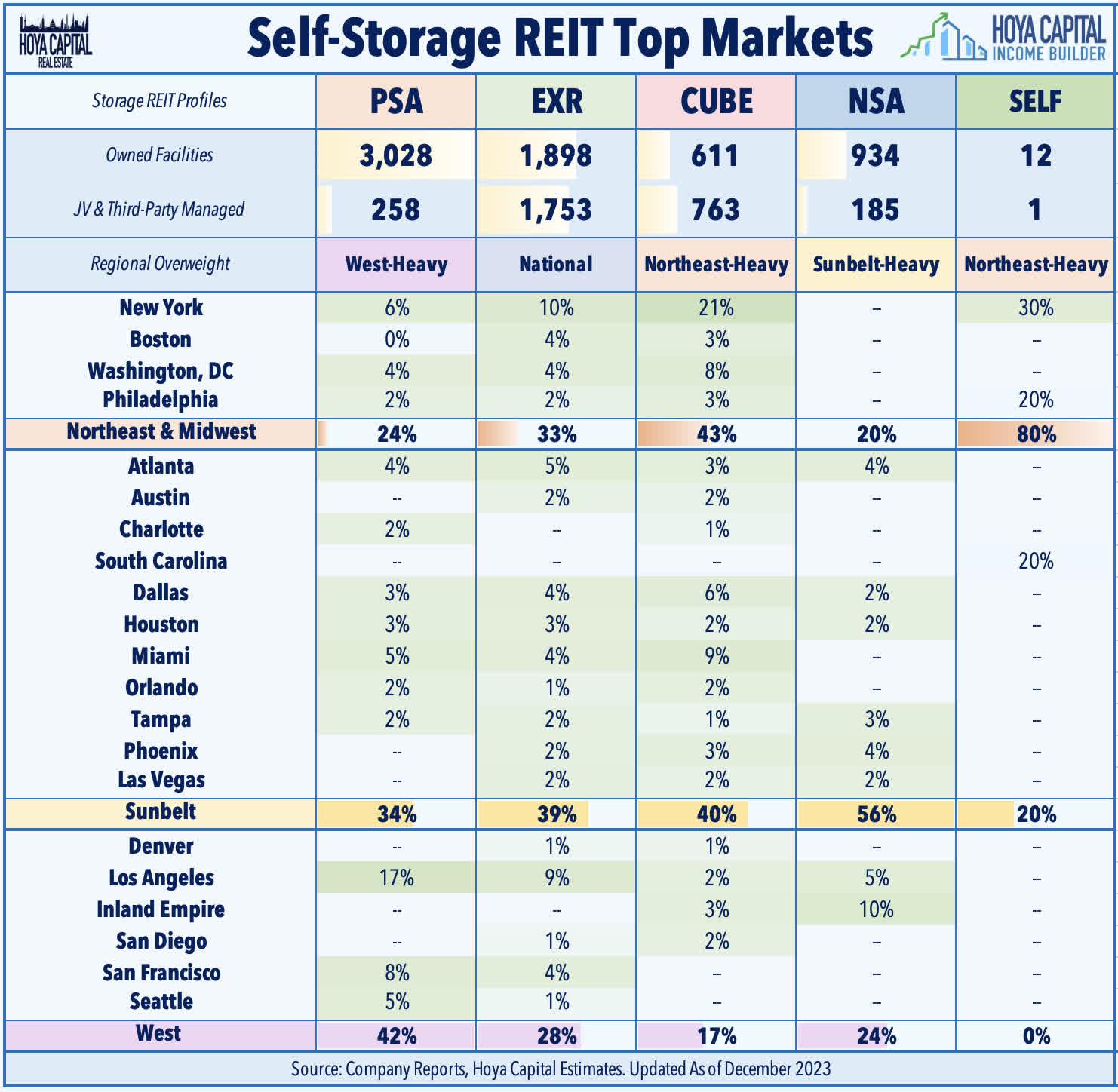

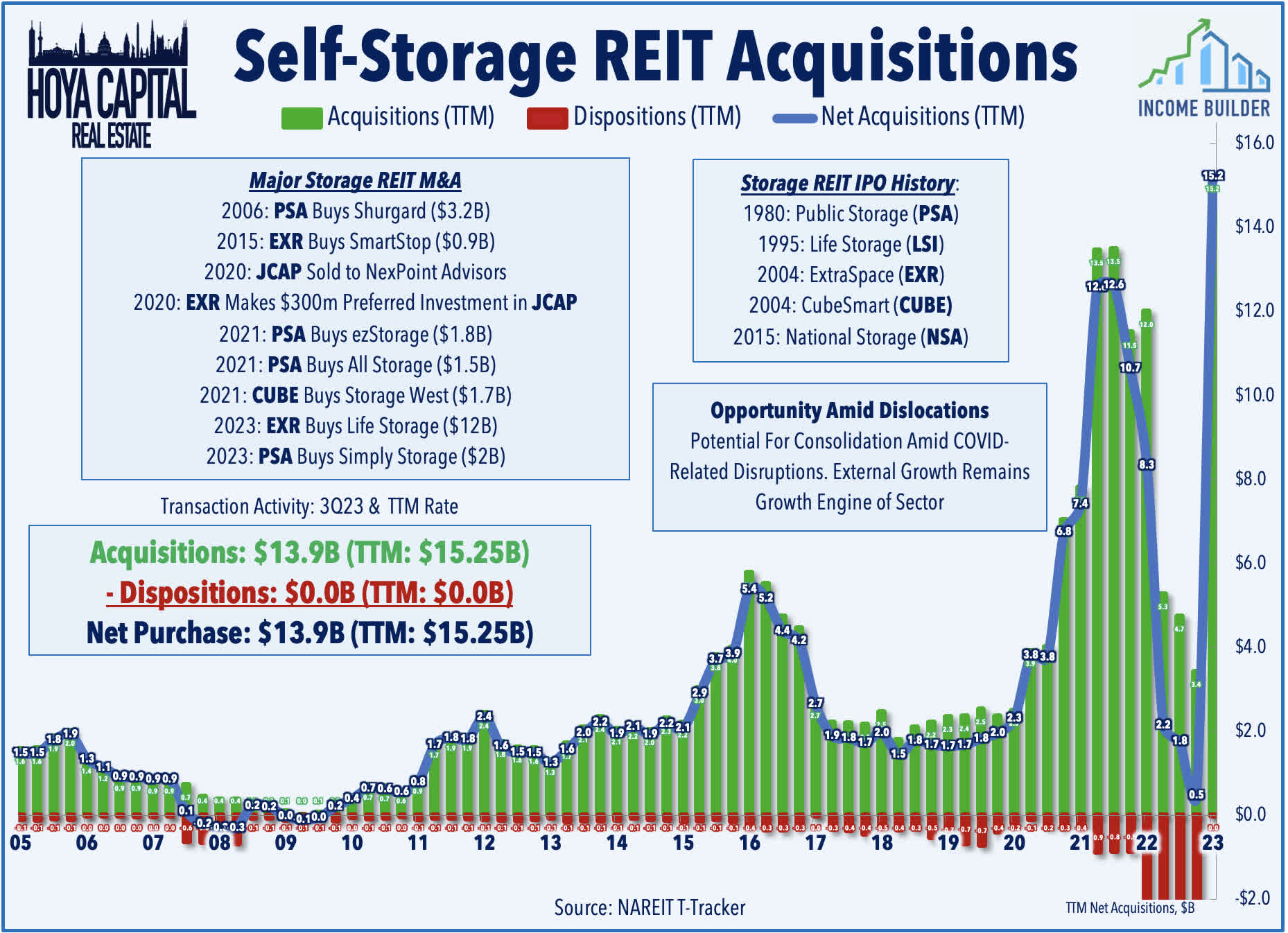

Self-Storage REITs delivered incredible growth early in the pandemic driven by surging housing market activity, but have been victims to their own success of late amid a supply-driven cooldown. In the Hoya Capital Self-Storage REIT Index , we track all five publicly-traded self-storage REITs, which account for roughly $100 billion in market value and comprise about 8% of the Equity REIT Index: Public Storage ( PSA ), Extra Space Storage ( EXR ), CubeSmart ( CUBE ), Life Storage ( LSI ), National Storage ( NSA ), along with micro-cap Global Self Storage ( SELF ). We've seen some notable consolidation activity over the past several quarters, as EXR closed on its acquisition of Life Storage in July - a $12.4B deal that was reached just weeks after the latter rejected a takeover offer from PSA . The deal between the second-and third-largest operators created the largest self-storage REIT by the quantity of assets operated.

{kind=link}

The United States has approximately 51,000 self-storage facilities comprising about 14 million units and 2.04 billion total square feet, per SpareFoot . Approximately 11% of households in the United States (14.6 million households) utilize a storage unit, and pay an average monthly rent of $110 per unit ($16 per square foot per year). Roughly 70% of self-storage customers are residential while 30% are businesses. The four largest public REITs and non-REIT U-Haul Holding ( UHAL ) are the five largest self-storage owners in the country. U-Haul (previously known as Amerco) had explored a REIT conversion back in 2015, but shareholders ultimately voted to remain a C-corporation. The three largest REITs - PSA , CUBE , and EXR - operate relatively higher-rent portfolios (average rents of $175-200) in more primary markets, while NSA and SELF operate facilities with lower rents (average rents of $100-125) in secondary and tertiary markets.

{kind=link}

These five REITs control a relatively dominant share of the self-storage market, owning or operating close to half of the nation's self-storage facilities. Revenue and expense management technology, brand value, and cost of capital have historically given these REITs a competitive advantage over private market competitors and smaller brands. Beginning in the mid-2010s, these self-storage REITs have monetized this scale and operating platform by offering third-party management services to smaller asset managers, which has provided a higher margin "asset lite" business line that compliments their core business of asset ownership. There are eight other "institutional-size" portfolios of at least 50k units, including StorageMart, Merit Hill Capital, Prime Storage, SORA Capital, SmartShop, City Line Capital, StorQuest, and Andover Properties, along with several dozen "family-office" portfolios of 25-50k units.

{kind=link}

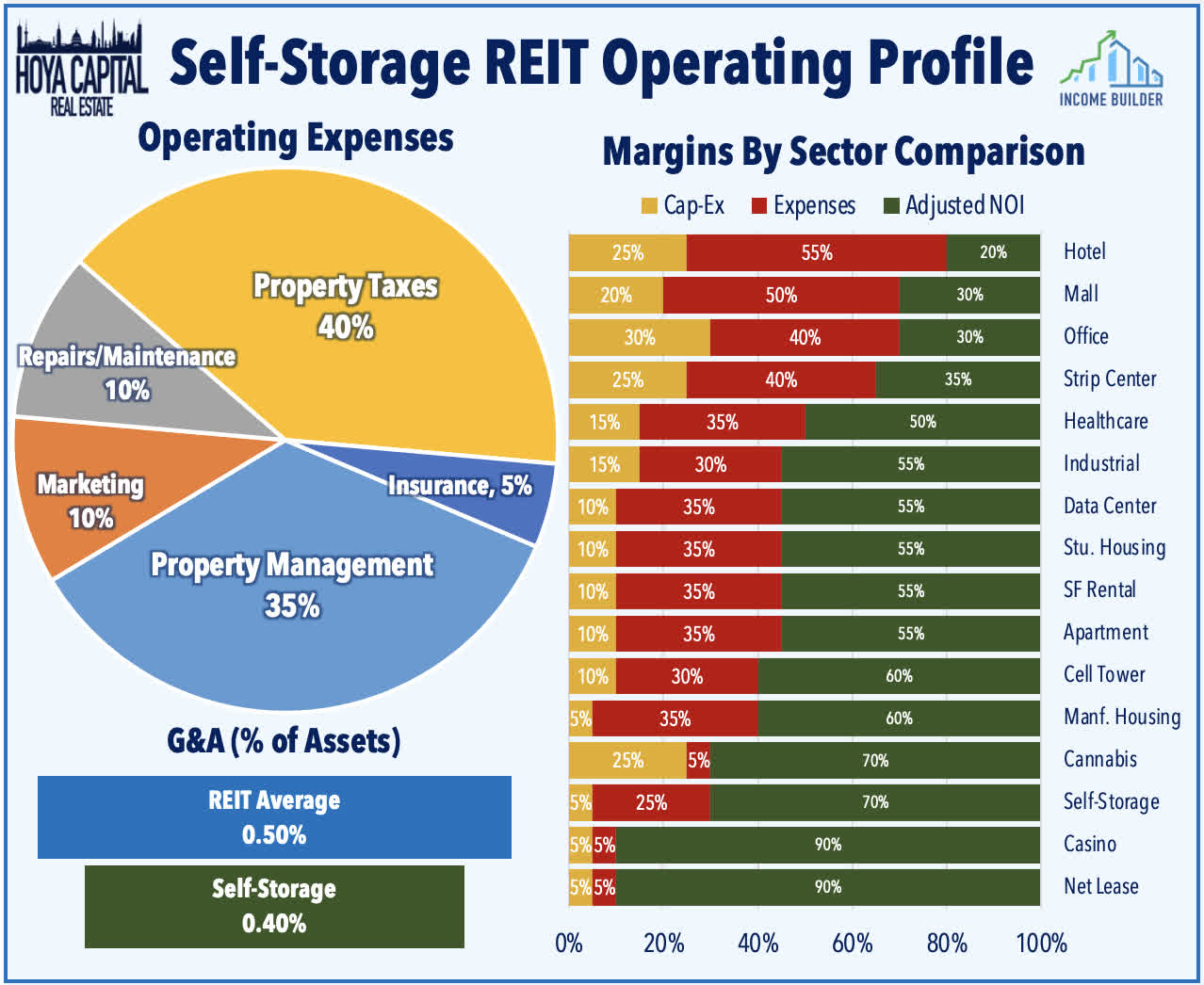

Much like the multifamily and single-family rental sectors, there also exist thousands of "mom-and-pop" self-storage operators that own one or a handful of self-storage facilities, a function of the relatively modest "entry cost" and low operational barriers to entry - made even lower by the availability of third-party portfolio management. Typically constructed for around $10-15k per unit and valued upon stabilization (2-4 years to reach stable occupancy) at around $15-25k per unit, smaller self-storage facilities can be built or acquired for $5M or less. The operating efficiency of the self-storage business is second to none in the real estate sector, commanding some of the highest NOI margins at over 70% while requiring minimal ongoing capital expenditures to maintain the facilities. Operating expenses are typically fixed and steady, with the exception of marketing spending, which increases as competition intensifies.

{kind=link}

Historically one of the most active consolidators across the REIT sector, we expect self-storage REITs to kick into a higher gear over the next 24 months and foresee these REITs using their stellar balance sheets to scoop up smaller, over-levered players that are seeking an exit. Consistent with that theme, several months after "whiffing" on Life Storage, Public Storage scooped up Simply Self Storage - the tenth-largest self-storage platform in the nation - from Blackstone's ( BX ) non-traded real estate platform - one of several major asset sales from BREIT that have become necessary to meet investor redemption requests. As with the apartment REIT sector, the pockets of rate-driven distress have remained isolated to the most highly-indebted corners of the private markets, and this distress should present further opportunities for well-capitalized REITs. While organic growth will be flat-to-negative in 2024, conditions are favorable for these storage REITs to lean heavily into external growth via acquisitions during this period of softer fundamentals.

{kind=link}

Self-Storage Fundamentals

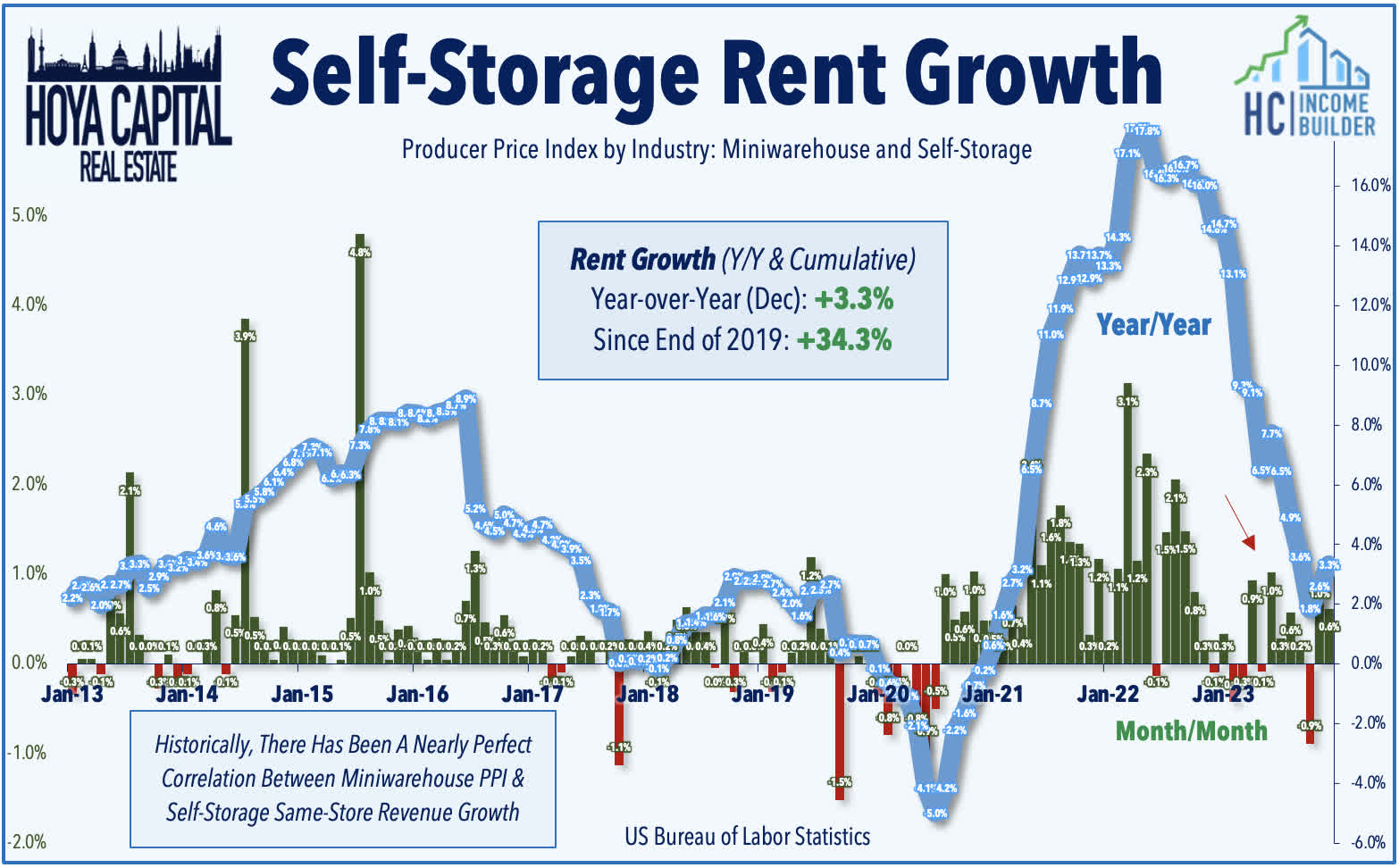

The best of times, and the worst of times. Self-storage REITs stumbled into the coronavirus pandemic era with challenged fundamentals and an outlook for near-zero growth amid oversupply challenges - not unlike the current environment - but demand came roaring back to life beginning in late 2020 as booming housing market activity amplified pre-existing demographic tailwinds to drive record occupancy levels and double-digit rent hikes. The Producer Price Index for self-storage facilities - which has historically exhibited a near-perfect correlation with blended rent growth (combined average of new and renewed leases) - illustrates this incredible turnaround - along with the recent sharp moderation. Peaking last April with a record-high annual increase of 17.9%, the most recent PPI report for December showed a continued cool down in the annual rate of growth to 3.4% in December - but still at levels that remain nearly 30% above the pre-pandemic baseline.

{kind=link}

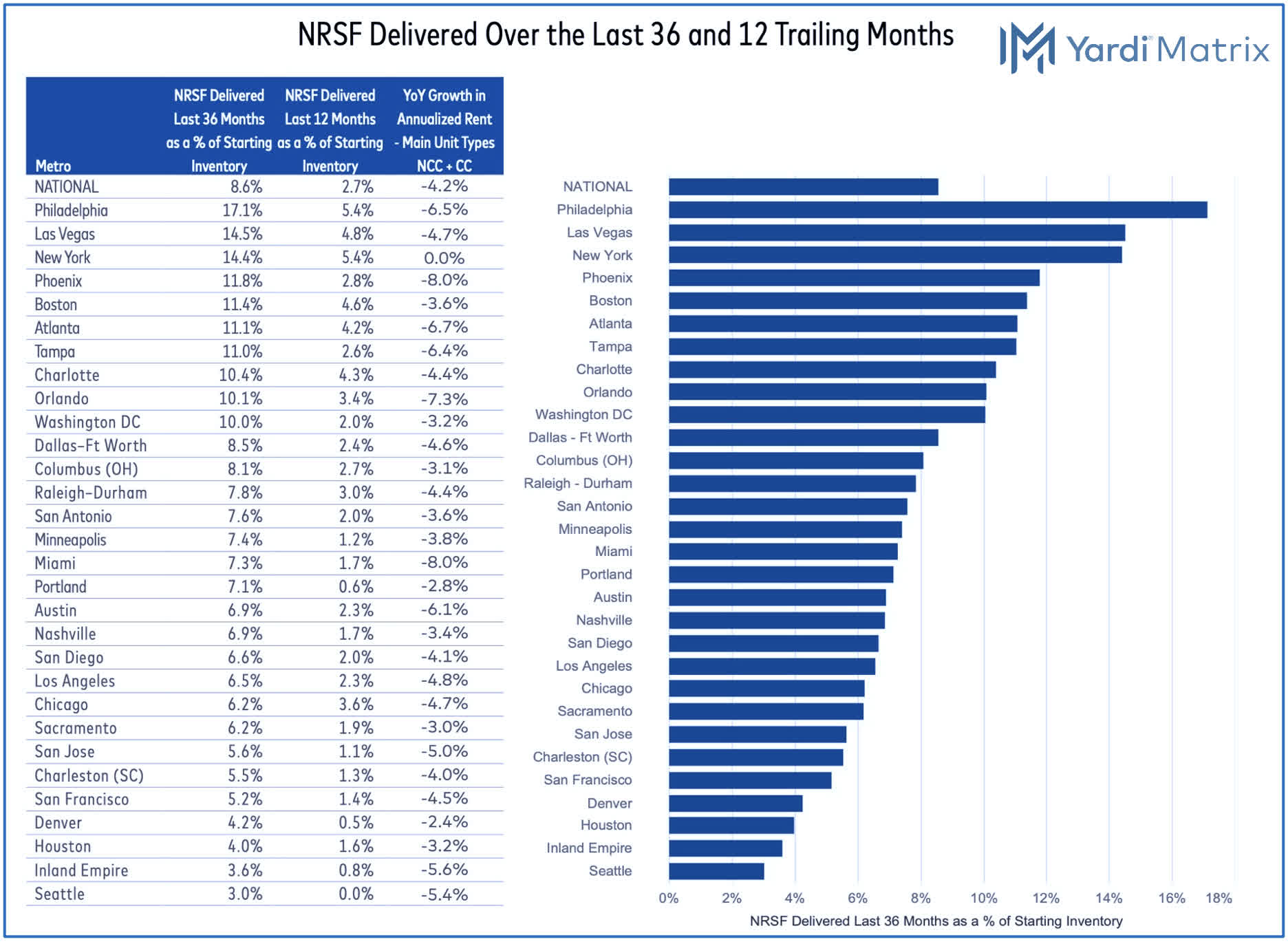

A central theme of this report, this operating efficiency can be a "double edge sword" for these self-storage REITs. Robust rent growth over the past decade - especially during the pandemic-era housing boom - prompted a wave of new development. Per leading self-storage industry data provider Yardi Matrix, the amount of new supply delivered over the past three years equals roughly 8% of inventory at the start of the period, with another 4% of inventory currently in the pipeline. This level of inventory expansion is more than twice the magnitude of the multifamily sector - a segment with known supply headwinds - and more than three times the magnitude of the single-family space. As with the multifamily space, the fastest-growing markets - most of which in the Sunbelt region - have seen the highest-levels of new supply growth in recent years, while "primary" markets on the Coasts have also seen elevated supply.

{kind=link}

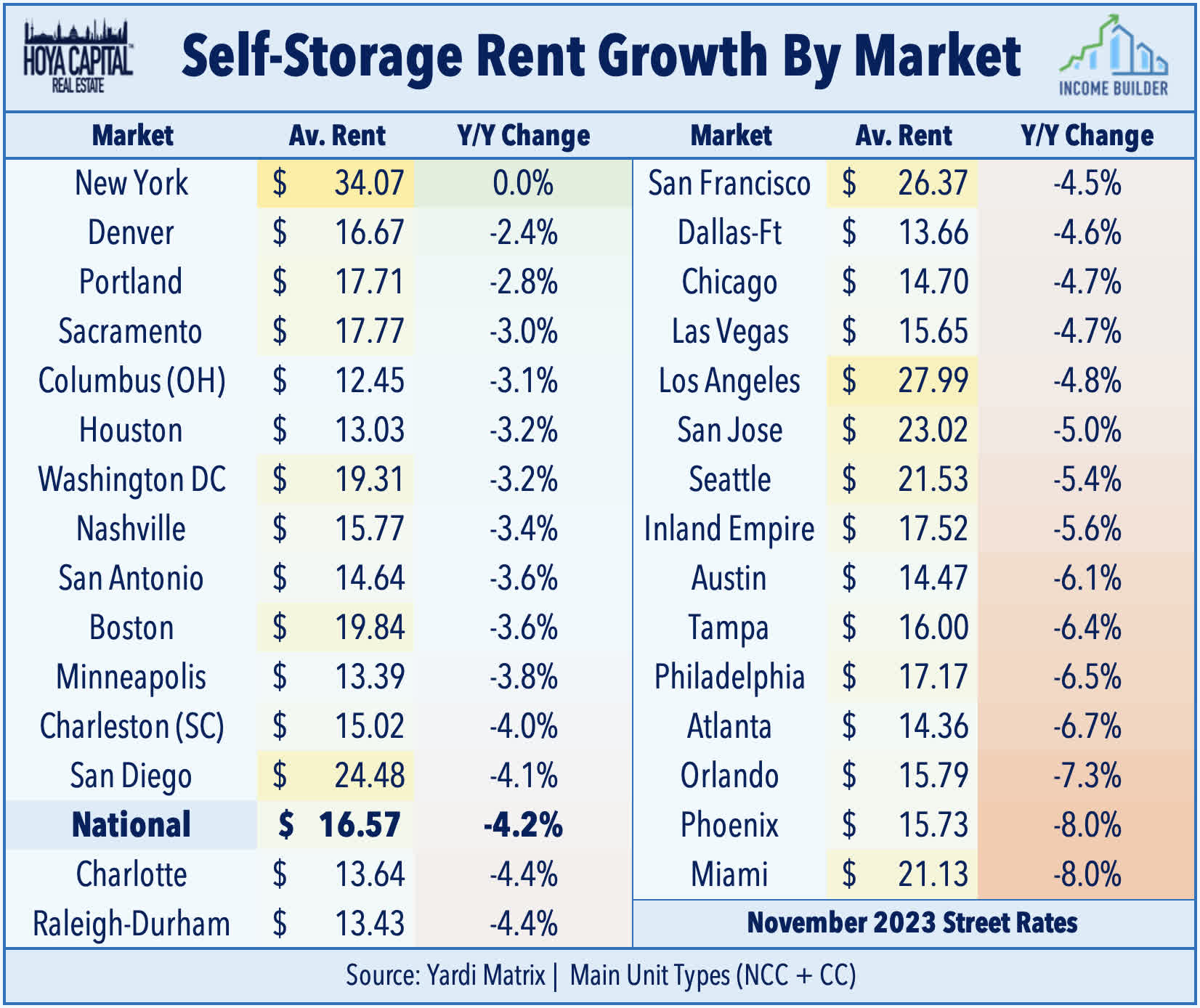

While demand has remained relatively firm, this surge in new supply has prompted "storage wars" between competing operators, driving down rents on new leases by double-digit percentages and pressuring occupancy rates to their lowest levels since before the pandemic. Yardi reports that new lease rates - which are referred to in the industry as "street rates" - were lower year-over-year by an average of 4.2% nationally, which was roughly 10-15% below the peak in street rates in mid-2022. Many of the Sunbelt markets seeing ample supply growth have been among the weakest-performing, with Miami, Phoenix, and Orlando seeing rent declines nearing 10% from last year and approaching 20-25% declines from the peak in mid-2022. Softer fundamentals combined with the surge in financing costs have hit the smaller, more highly-levered owners in these markets particularly hard, prompting a rise in default rates with likely more to come in the quarters ahead.

{kind=link}

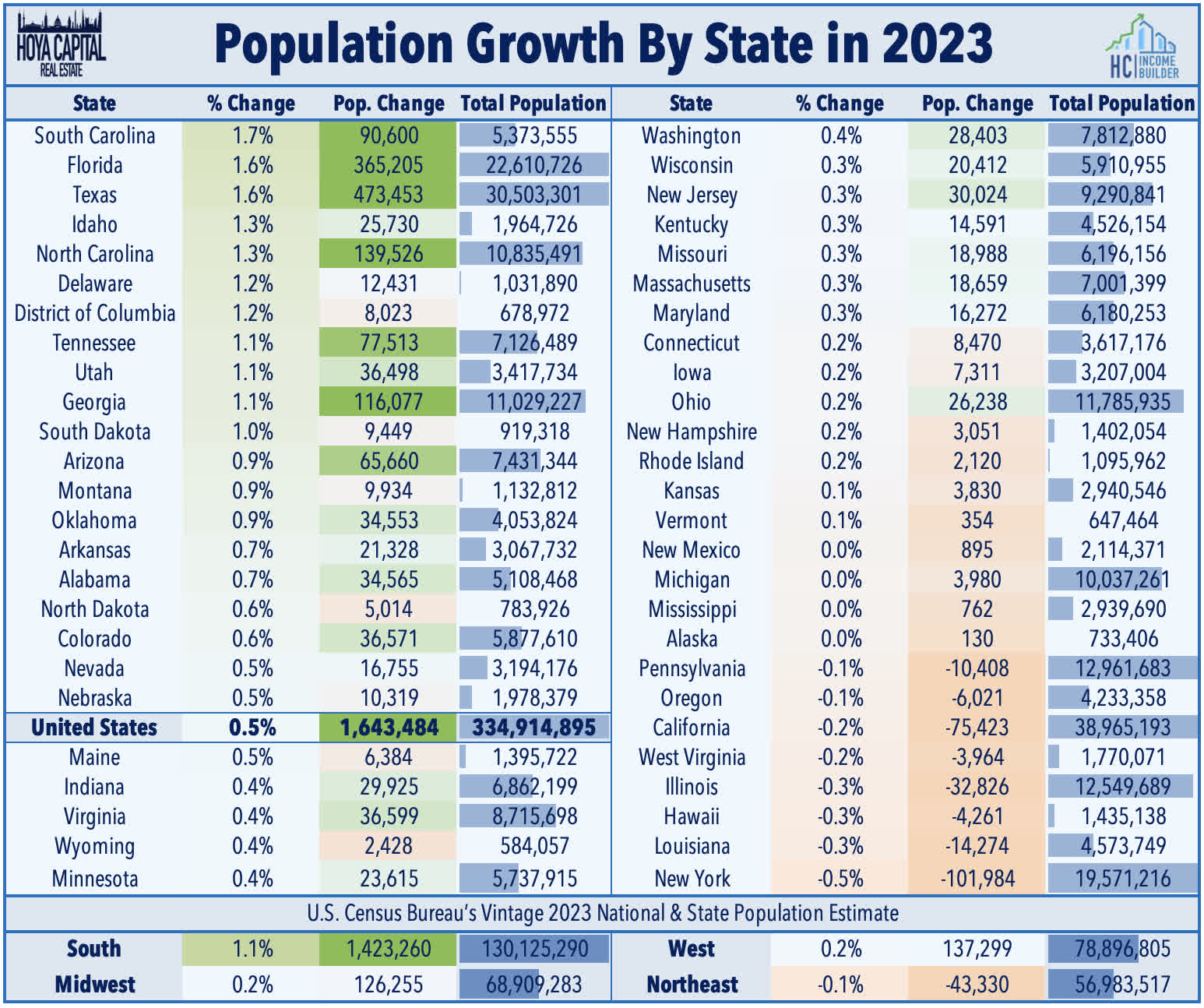

While Sunbelt markets are seeing elevated supply growth, these markets are also benefiting from significantly higher levels of overall population growth. Per the annual Moving Report from U-Haul and newly-released Census data, Florida was again among the fastest-growing state in 2023 on a percentage basis with an annual population increase of 1.6%, while Texas earned the top spot on an absolute basis with the addition of nearly a half-million new residents. These two states were also the top one-way U-Haul truck customers during 2023, ranking as the top growth states on the annual U-Haul Growth Index. On the flipside, California and Illinois recorded six-figure decreases in resident population and were again at the bottom of U-Haul’s list for states that gained population, following similar net-migration trends revealed in 2022. At the regional level, the South was the fastest-growing region last year, increasing by 1.1% while the Midwest and West region grew 0.2%. The Northeast region, however, recorded a population decline of -0.1%.

{kind=link}

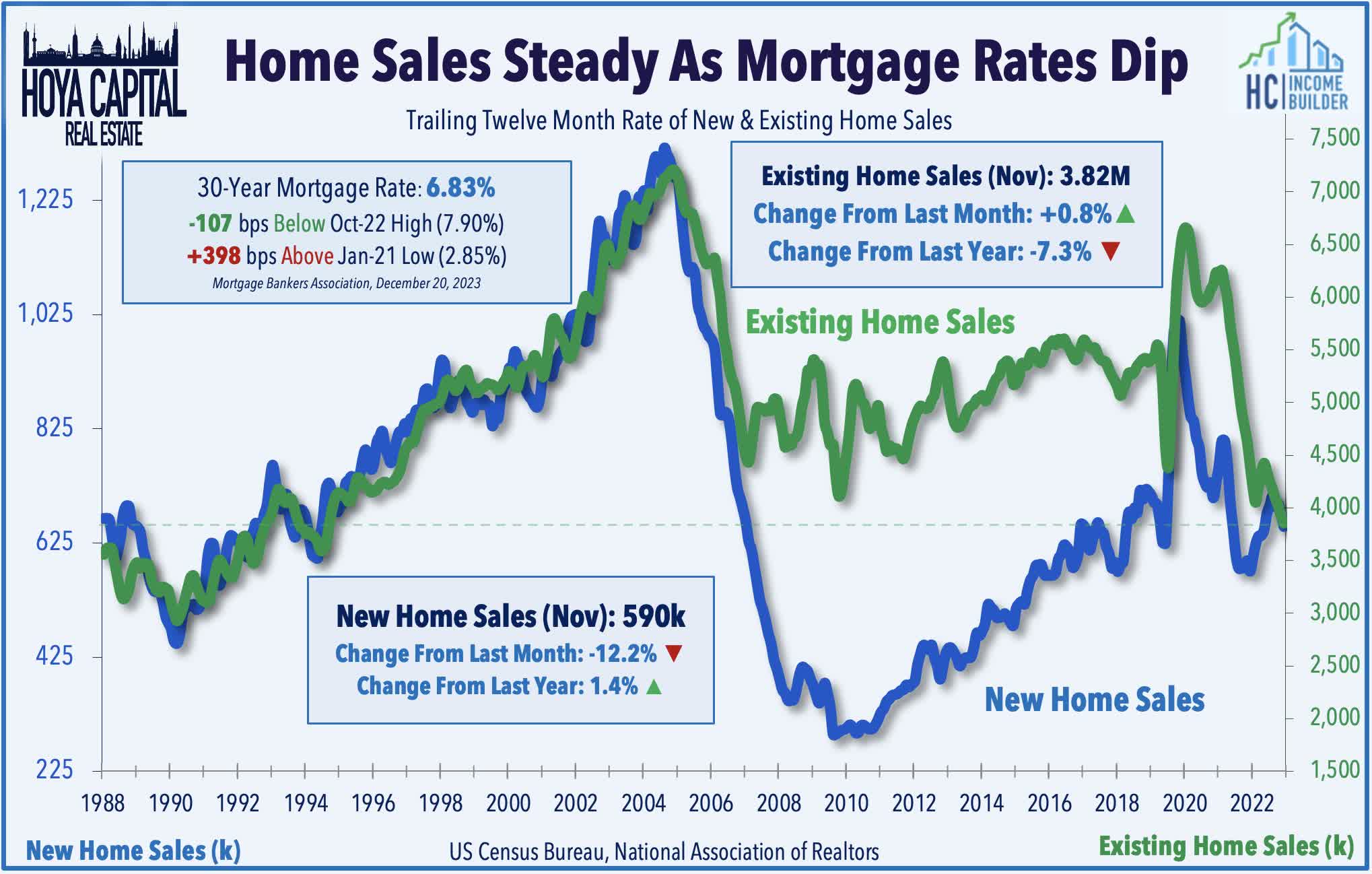

Self-storage demand is more closely-correlated with household moving rates than many presume - specifically home sales and rental turnover - a previously-underappreciated correlation that was on full display early in the pandemic as robust housing market activity from mid-2020 through mid-2022 fueled a corresponding boom in self-storage demand. This trend worked in reverse amid the rate-driven housing cooldown that sent the pace of both New and Existing Home Sales to their lowest levels since 2011. Rental market turnover was similarly sluggish - dipping to the second-lowest rate ever recorded by RealPage in 2022 and remained historically low in 2023. The recent moderation in mortgage rates has breathed some new life into the sluggish housing market, however, as mortgage-purchase applications have rebounded from their three-decade lows seen last November, while other forward-looking indicators - including Redfin’s Homebuyer Demand Index and new listings data - have inflected higher in recent weeks.

{kind=link}

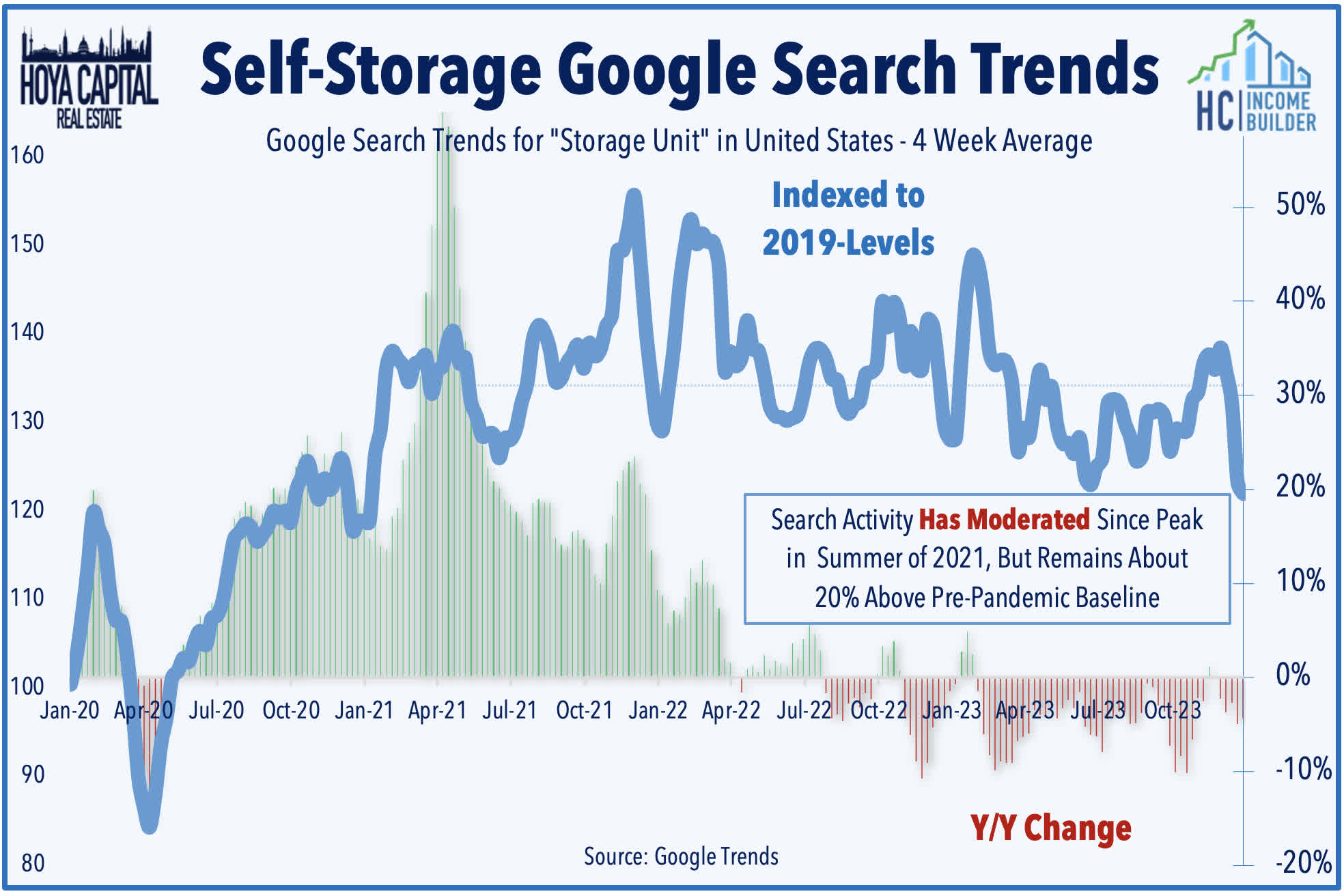

Don't underestimate the potential demand impact from a recovering housing market. Storage REITs hit 'rock bottom' of a multi-year downtrend early in the pandemic and were left for dead by many analysts and investors. Green shoots began to emerge by late 2020, and after these signs of strength were initially dismissed as a short-term blip, these REITs built on the rebound in each of the subsequent quarters. Searches on Google for "self-storage unit" - which has historically exhibited a strong correlation with occupancy rates - climbed to as high as 60% above 2019-levels in early 2022, but began to moderate alongside the housing cooldown by mid-2022 and currently stand at levels that are about 20% above the pre-pandemic baseline.

{kind=link}

Self-Storage REIT Earnings Analysis

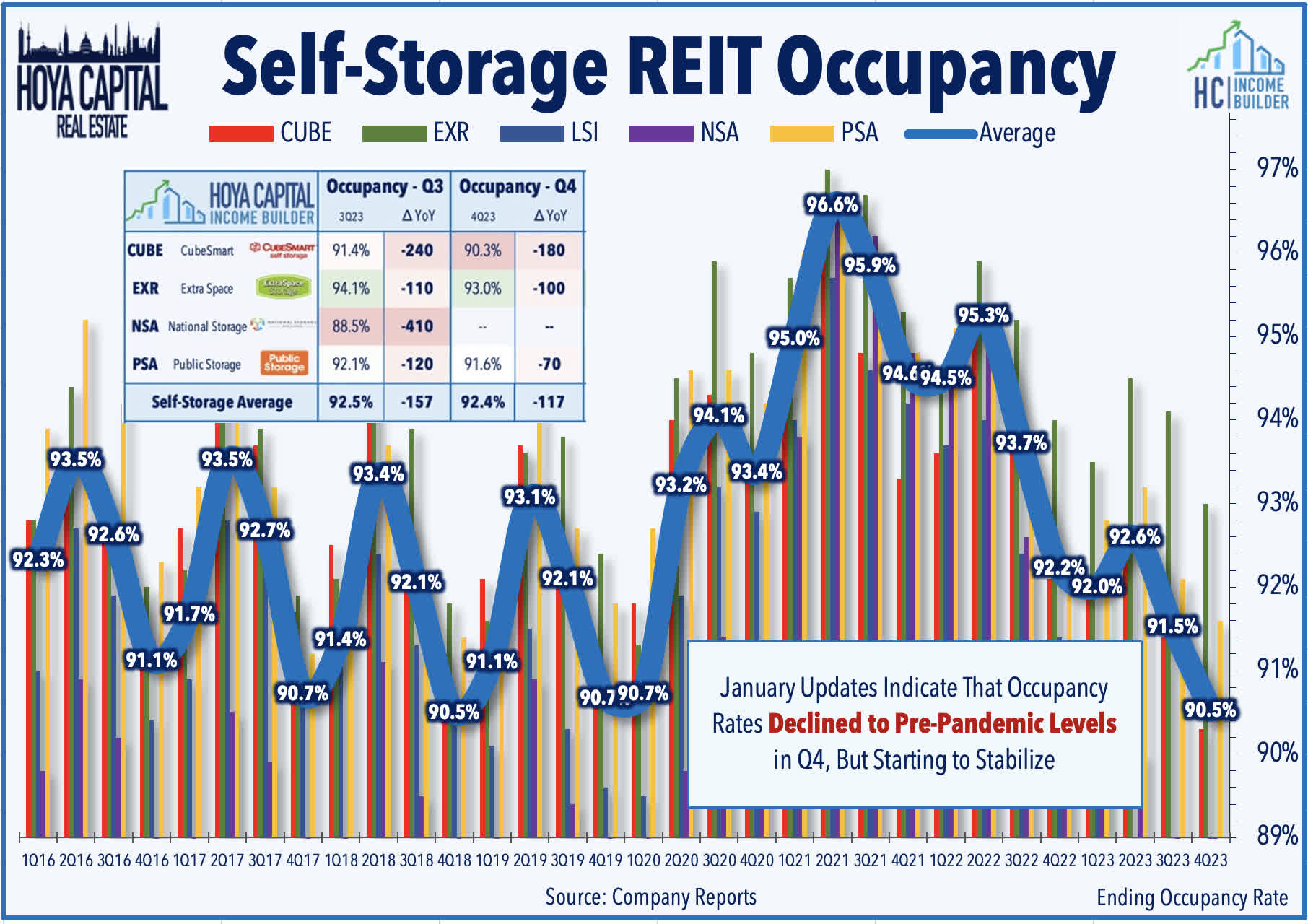

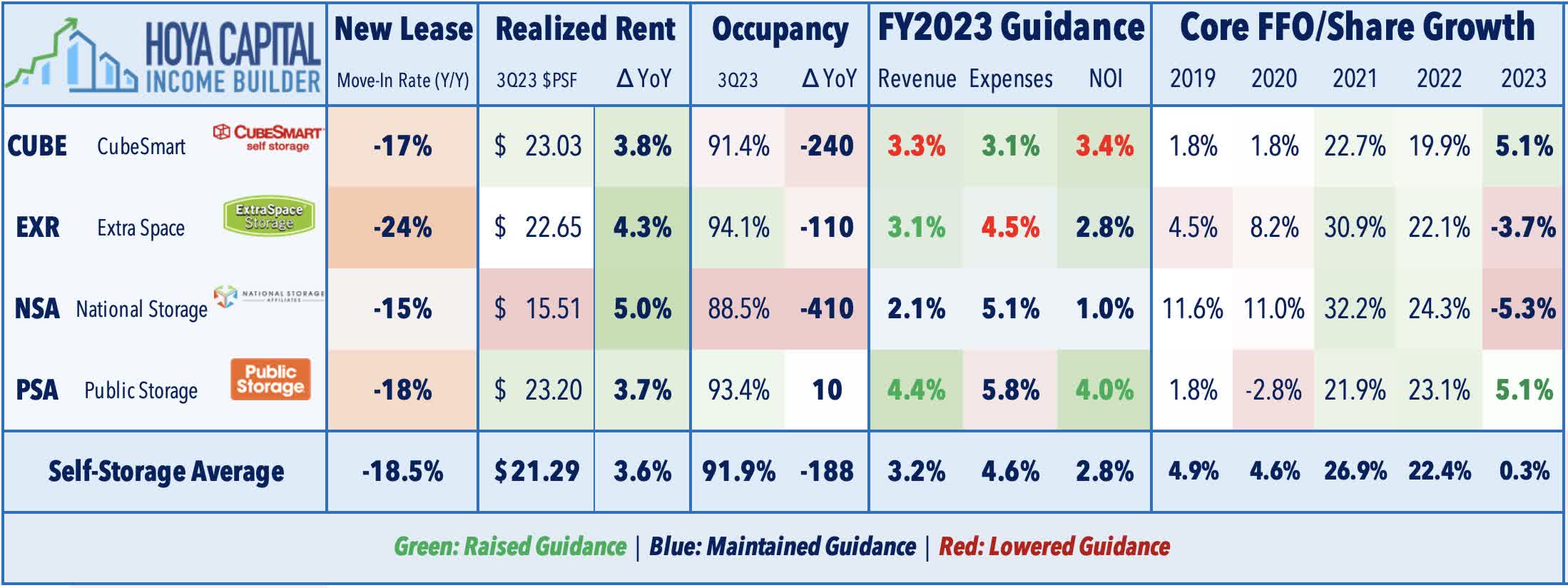

As discussed in our Real Estate Earnings Recap, third-quarter results and recent interim updates show that headwinds on the supply front persist heading into 2024, but there were some early indications that an upward inflection in housing market activity is starting to revive some demand. Public Storage reported last week that same-store occupancy rates declined to 91.6% at the end of the year, which was the lowest since Q4 of 2018. However, PSA noted "improving trends throughout the quarter" and noted that its average rent per square foot was still higher by 1% year-over-year as steady mid-single-digit rent growth on renewals has offset a sharp 15-20% decline on new leases. Reports from CubeSmart and Extra Space Storage showed similar trends, with both REITs reporting their lowest occupancy levels since at least 2019, but also showed solid demand trends, particularly later in the quarter.

{kind=link}

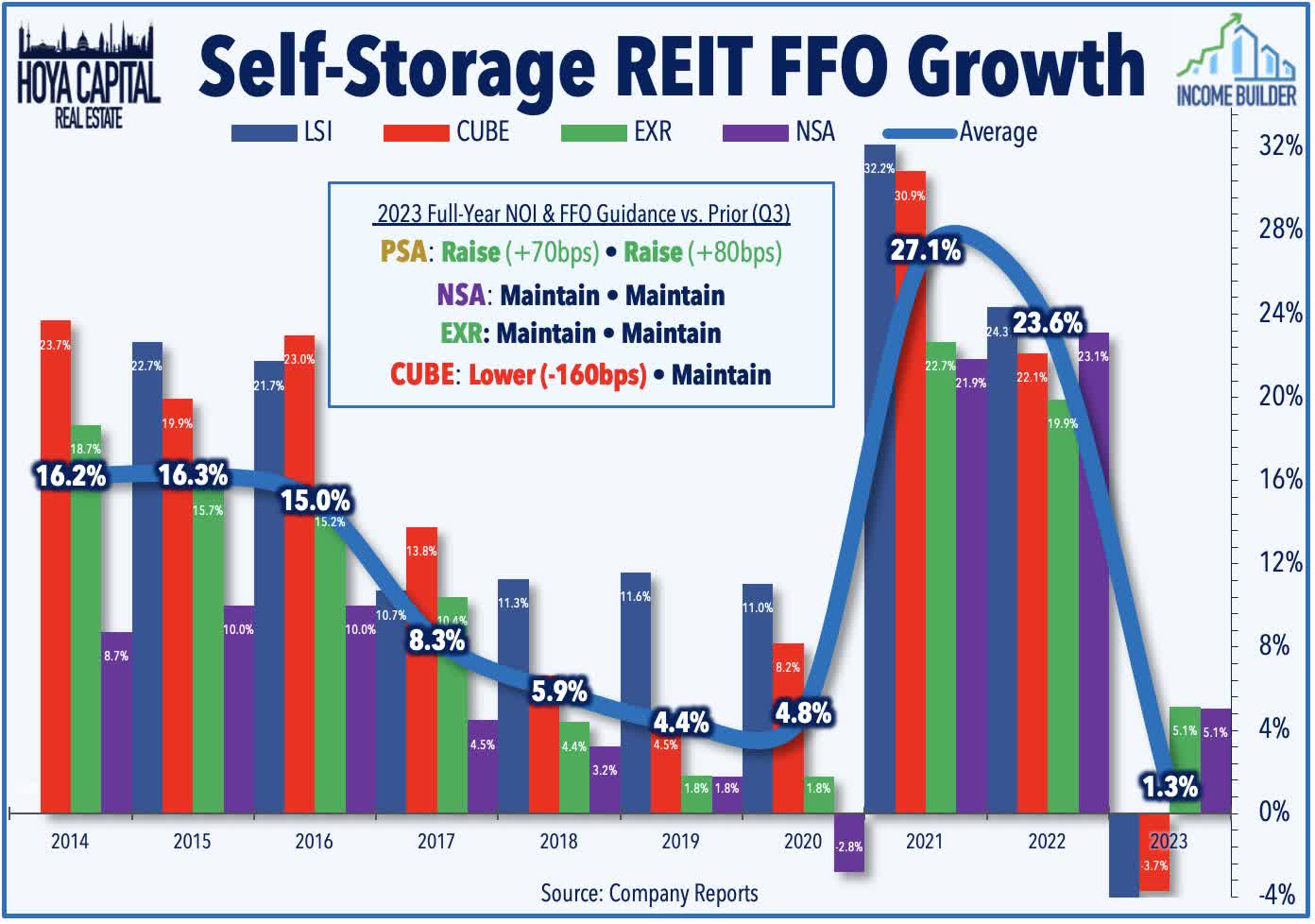

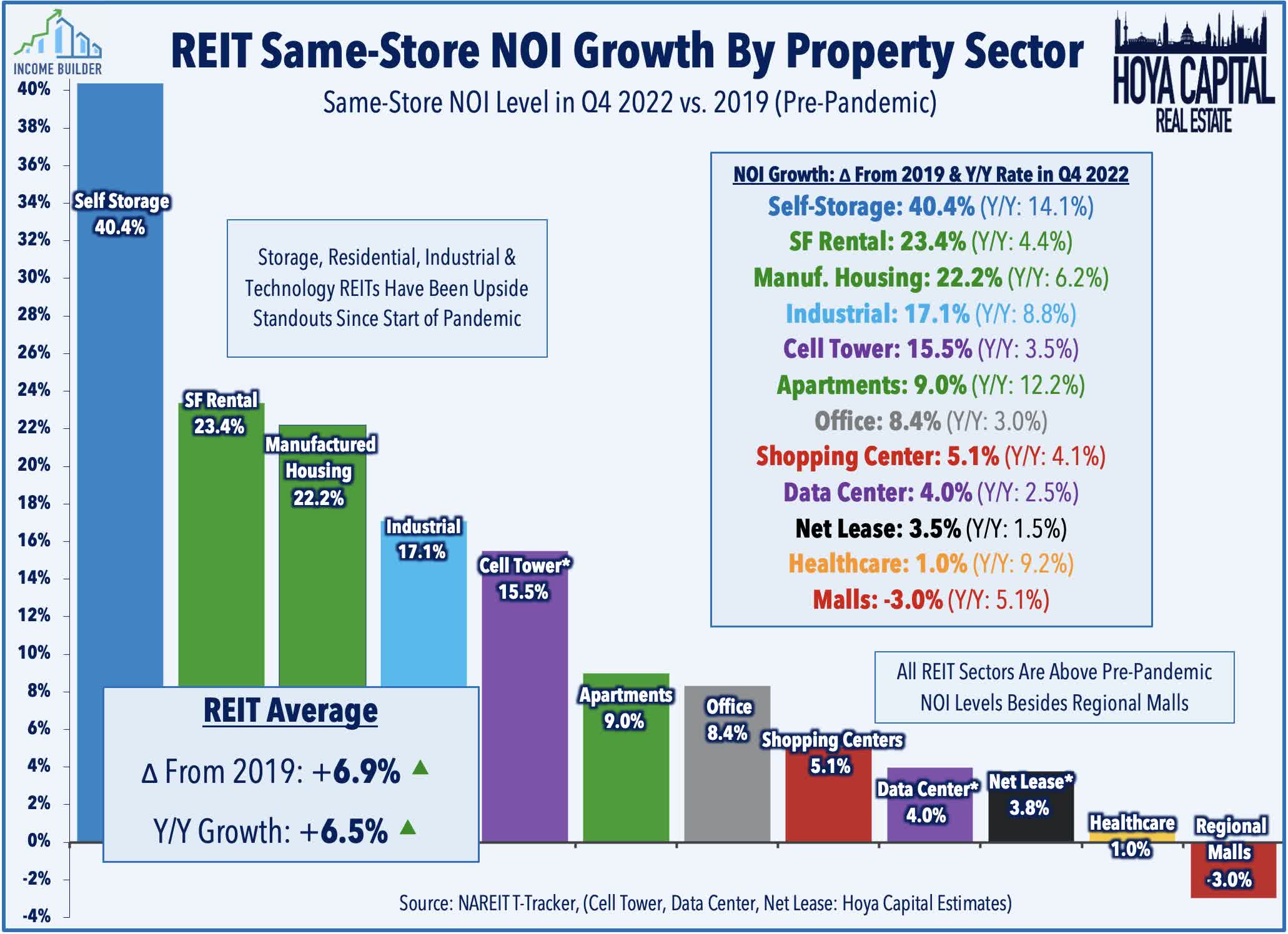

As with the prior quarter, all four self-storage REITs reported double-digit declines in "street rates" on new customers in Q3 and into Q4, but this pricing weakness has been more-than-offset by mid-single-digit rent growth on renewal leases, resulting in a total rent PSF increase of about 4% in Q4 compared with last year. While 'sticky' demand and steady rent growth on existing tenants is a feature of the sector, the pricing gap can only extend so far before tenants pack up and move to another nearby facility, offering ample concessions and lower rent. Following incredible FFO growth of over 20% in 2021 and 2022, self-storage REITs are expected to report full-year growth of around 1% for 2023, which would be the softest growth rate since 2010. That said, Storage REITs have delivered cumulative FFO growth of over 60% and cumulative NOI growth of over 40% since the start of 2019 - the best in the REIT sector.

{kind=link}

The strongest report of third-quarter earnings season came via Public Storage , which raised its full-year NOI and FFO outlook, citing continued strength in its California markets - one of the lone exceptions to the West Coast underperformance theme, as restrictive zoning has limited new self-storage development in recent years. Extra Space also performed well after reporting Q3 results, reporting rapid progress on its integration with Life Storage - which it acquired in July - and noted that it has reached its anticipated G&A expense savings run rate, and is on pace to reach its total synergies by next quarter. National Storage has also seen a solid rebound since its Q3 earnings report in which it maintaining its full-year outlook and commenting that its "toughest comps are behind us as far for street rate and year-over-year occupancy." CubeSmart meanwhile, reported strength in its suburban NYC markets but noted that the overall pricing environment on new customers has been "weaker than we previously thought."

{kind=link}

Storage REITs indicated that supply growth is expected to be a headwind over the next several quarters, but generally expect new deliveries to moderate later in 2024 as the effects of higher interest rates and macroeconomic uncertainty temper the development appetite. Construction spending data from the Census Bureau has indicated that the peak in development appears to have occurred in 2017 and declined by more than 10% in 2021, but soaring rents and record-high occupancy rates spurred a rebound in starts in 2022 and into early 2023. Data from Yardi shows that Sunbelt markets are among the most active builders with Dallas, Phoenix, and Orlando among the top 5 markets for units under construction alongside New York and Los Angeles.

{kind=link}

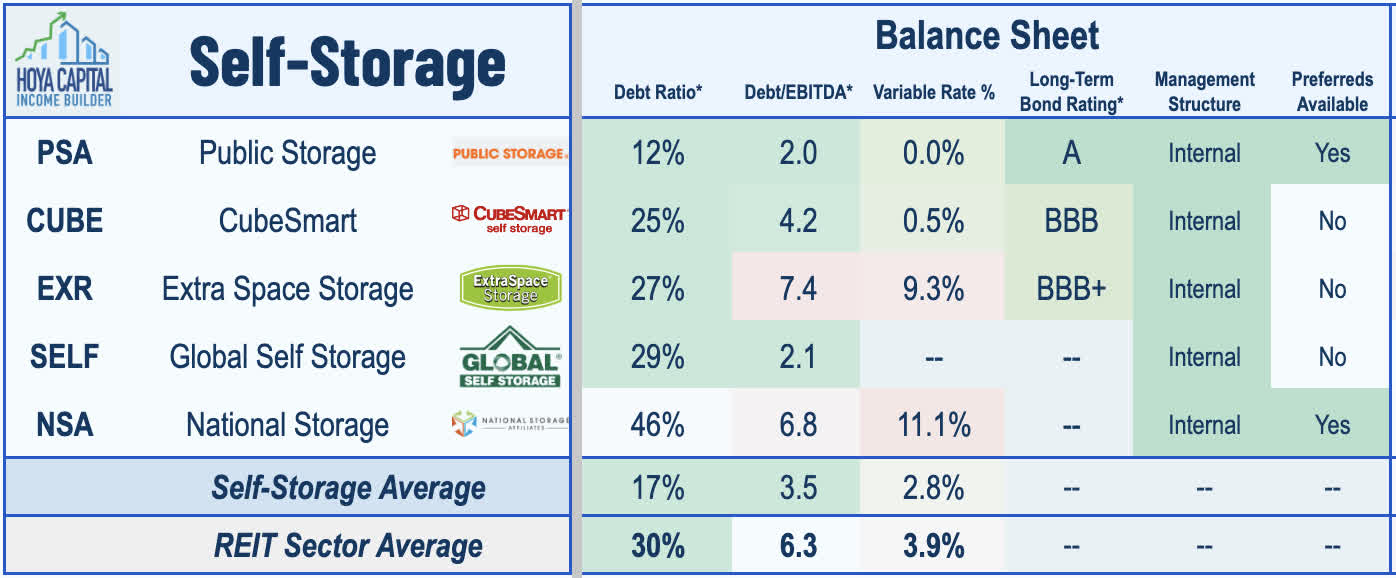

Importantly for their external growth prospects, self-storage REITs operate with some of the most well-capitalized balance sheets across the real estate sector. On average, self-storage REITs operate with debt ratios that are well below the REIT sector average of 20%, led by Public Storage , which operates with perhaps the most conservative balance sheet within the REIT sector with one of the few, coveted "A-rated" long-term bonds. CubeSmart , Life Storage , and Extra Space all hold investment-grade long-term bond ratings as well. Five of the six self-storage REITs operate with debt ratios below 30%. National Storage employs a more aggressive leverage profile, but the company was proactive in late 2022 in addressing its variable rate exposure.

{kind=link}

Self-Storage REIT Performance

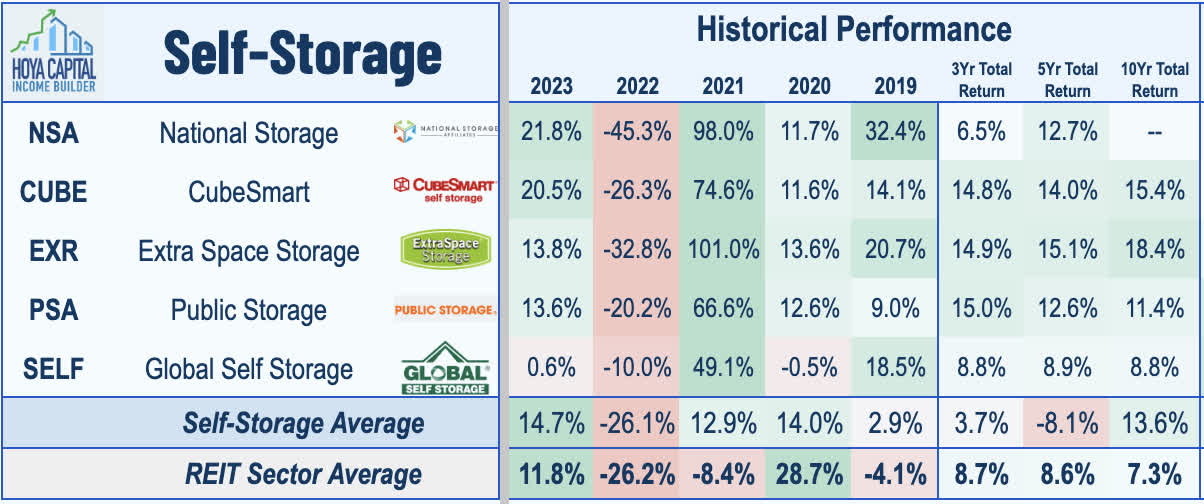

Following two years of sector-leading performance early in the pandemic, self-storage REITs have performed roughly in-line with the broader REIT sector average over the past two years. The Hoya Capital Self-Storage REIT Index - a market-cap weighted benchmark - delivered total returns of 14.7% in 2023, slightly outpacing the 11.8% total returns of the broad-based Vanguard Real Estate ETF ( VNQ ) and the 26.2% returns from the S&P 500 ( SPY ). The relatively strong year in 2023 followed a sharp 27% dip in 2022, which was slightly worse than the 25% dip on the broader REIT average. Through two weeks of 2024, self-storage REITs are lower by about 4% - slightly underperforming the 2% decline on the broader REIT average.

{kind=link}

Diving deeper into the company-level performance, Life Storage posted the strongest returns in 2023 following its takeover by Extra Space . Among the REITs still ticking, National Storage was the top-performing storage REIT in 2023 after getting pummeled in 2022 amid pressure on its relatively higher-levered balance sheet compared to its larger peers. Elsewhere, CubeSmart also posted very strong returns in 2023 as it closed the once-wide valuation gap with its larger peers, driven by several catalysts, including its addition to the S&P 400 and by outperformance in its critical NYC market. Public Storage and Extra Space each delivered total returns of around 14% last year, while micro-cap Global Self Storage traded roughly flat.

{kind=link}

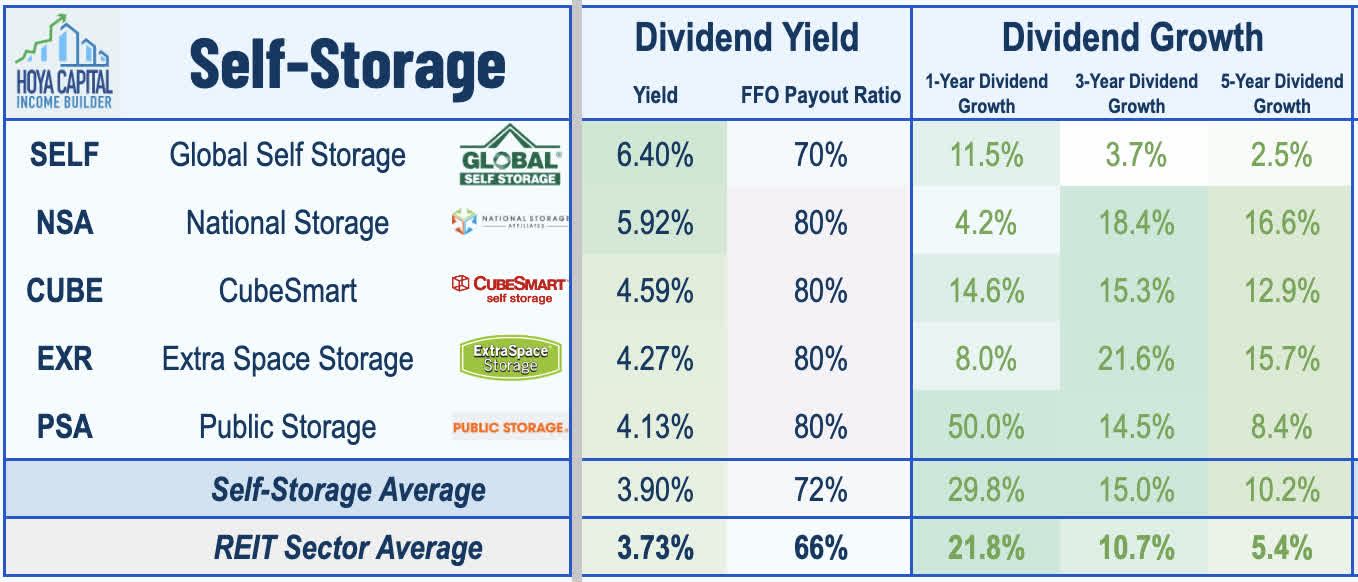

Self-Storage REIT Dividend Yield

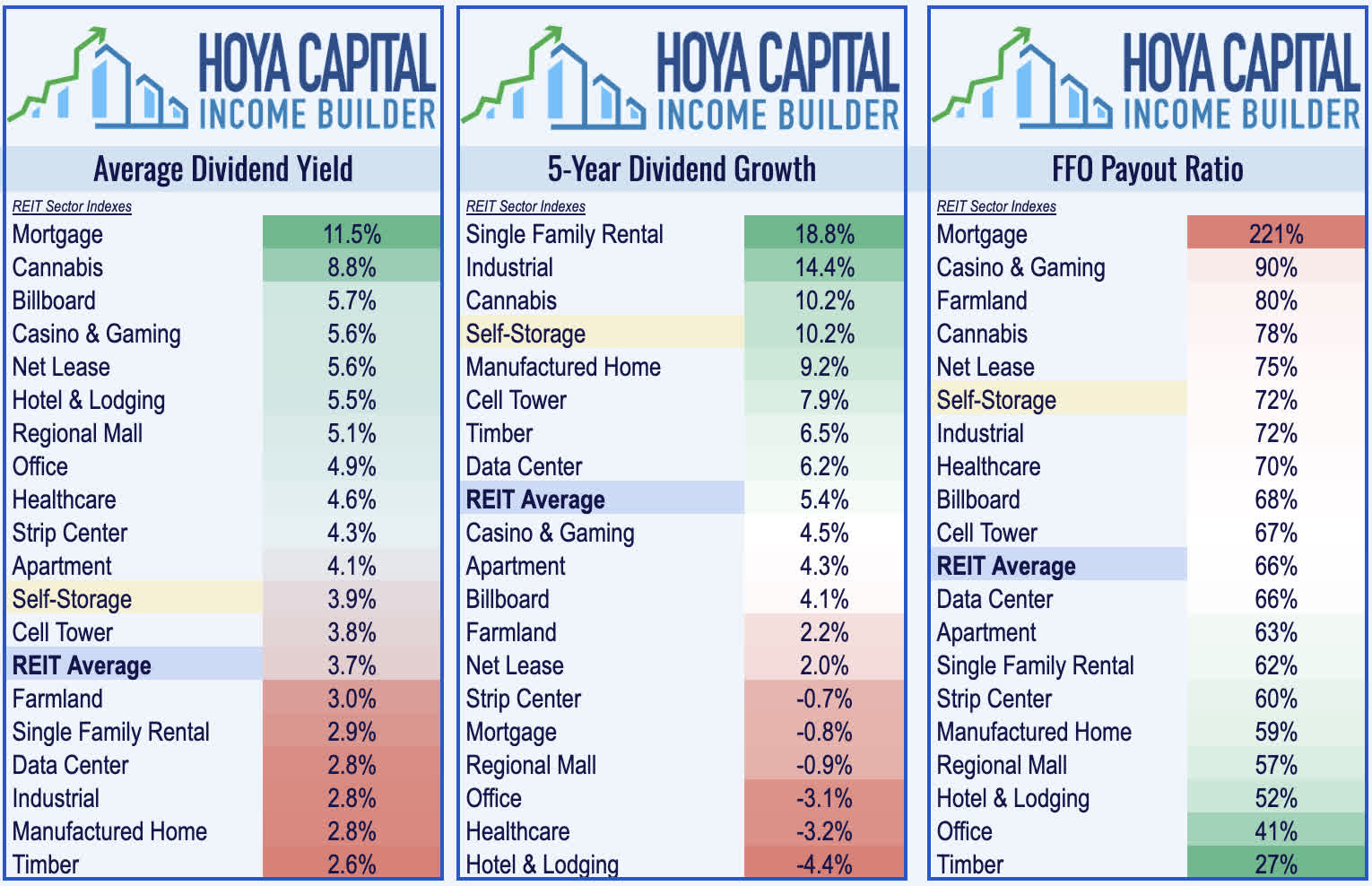

Storage REITs were one of the only property sectors that went completely unscathed by the wave of coronavirus-related dividend cuts that swept across the REIT universe in 2020 and were among the leaders in dividend growth in 2021 and 2022 as well. Storage REITs pay an average dividend yield of 3.9% which is slightly above the market-cap-weighted REIT sector average of 3.7%. Self-storage REITs pay roughly 80% of their available cash flow.

{kind=link}

Diving deeper into the sector, we note that the dividend yield ranges from a high of 6.40% from micro-cap Global Self-Storage and 5.92% from National Storage to a low of 4.13% from Public Storage . Notably, CubeSmart , National Storage , and Extra Space have been among the leaders in dividend growth across the REIT sector over the past five years with double-digit average annual dividend growth rates. All six REITs have hiked their dividends over the past year, led by a 50% dividend boost from Public Storage, which had previously held its dividend steady since 2016.

{kind=link}

Takeaway: Victims of Their Own Success

Self-Storage REITs delivered two years of incredible growth early in the pandemic driven by the surge in housing market activity, but have been victims to their own success of late amid a sharp supply-driven cooldown. This supply boom - twice the magnitude of the multifamily sector - has reignited the fierce "storage wars" between competing facilities, which has led to double-digit dips in new lease rates since the peak in mid-2022. Softer fundamentals combined with the surge in financing costs have hit the smaller, more highly-levered owners in these markets particularly hard, but this distress should present further opportunities for well-capitalized REITs. We expect storage REITs to leverage their stellar balance sheets to scoop-up highly-levered upstarts seeking an exit, providing some accretive external growth at a time of flat-to-negative organic growth.

{kind=link}

For an in-depth analysis of all real estate sectors, check out all of our quarterly reports: Apartments , Homebuilders , Manufactured Housing , Student Housing , Single-Family Rentals , Cell Towers , Casinos , Industrial , Data Center , Malls, Healthcare , Net Lease , Shopping Centers , Hotels , Billboards , Office , Farmland , Storage , Timber , Mortgage , and Cannabis.

Disclosure : Hoya Capital Real Estate advises two Exchange-Traded Funds listed on the NYSE. In addition to any long positions listed below, Hoya Capital is long all components in the Hoya Capital Housing 100 Index and in the Hoya Capital High Dividend Yield Index . Index definitions and a complete list of holdings are available on our website.

{kind=link}

For further details see:

Storage REITs: Victims Of Own Success