PAXS - Strategies For Growing Income In The New Year

Summary

- Gradually growing income levels of income portfolios is a goal of many income investors.

- In this article, we discuss some of the typical but unsustainable ways some investors pursue this goal which often results in disappointment.

- And highlight a few more sustainable alternatives which we have used this year.

This article was first released to Systematic Income subscribers and free trials on Dec. 16 .

Growing income remains one of the hallmarks of successful income investing. In this article, we discuss different strategies that can allow investors to achieve this in a sustainable way while avoiding some of the pitfalls.

There are any number of obvious ways investors can increase the income level of their portfolios. However, it's important to highlight that many of these strategies are not sustainable and can actually lead to a drop in income as well as underperformance and disappointment. In this article, we review both unsustainable ways many investors try to grow their investment income and their more sustainable, and ultimately, more successful versions.

Unsustainable Strategies To Grow Income

There are a number of ways income investors often try to boost their investment income. One such strategy is to simply buy securities that have higher distribution rates than their peers. The trouble with this strategy is that these high distribution rates are often either artificial or a result of a higher level of risk-taking whether through a higher level of leverage or through allocation to riskier assets.

Let's go through these in turn.

When considering an allocation to a particular sector such as high-yield bonds it's very tempting to just go for the fund with the highest yield . The intuition is perfectly understandable. A fund with a relatively high yield seems to have some "secret sauce" which allows it to generate a higher level of income than the rest of the space.

A good example here is the PIMCO Corporate & Income Opportunity Fund ( PTY ) which has had one of the highest NAV distribution rates across the CEF space. For years, we saw any number of articles pitching PTY as having some magic which allowed it to keep its distributions unchanged for over a decade and how investors were well-advised to buy the fund at its 30+% premium.

What happened next was the fund cut its distribution by around 9% which also drove its premium from a 50% peak in 2021 to its still-expensive 19% level. Since 2020, the fund has delivered a total price return of -7.6%, considerably underperforming the average CEF. Chasing distribution stability and high yield has delivered neither distribution stability nor high yields but only underperformance.

Our refrain here is that CEFs operate within a competitive environment of publicly tradable assets run by managers who pretty much see the same things on their screens and who have access to similar tools. Yes, performance does vary across funds and managers, but maintaining a consistent advantage is nearly impossible.

Another common but unsustainable strategy to boost income is to go for funds with the highest level of leverage . This strategy is related to the previous one as higher leverage often allows funds to deliver higher yields. The trouble with this strategy is two-fold. First, a high level of leverage obviously multiplies downside during drawdowns, making it more difficult for investors to remain invested. And secondly, a high level of leverage increases the likelihood of a forced deleveraging.

Here, we can turn to another PIMCO set of CEFs - their Municipal tax-exempt suite. PIMCO tends to run their tax-exempt funds at very high leverage levels - around 10-15% above the average fund in the sector. This leaves little margin of safety before the funds are forced to deleverage.

As we highlighted a couple of times, this suite deleveraged twice this year, locking in economic losses.

Systematic Income

One would think that running at an elevated level of leverage should deliver higher total returns, however, that's not the case if we compare a fund like the PIMCO Municipal Income Fund II ( PML ) to a fairly generic tax-exempt CEF like the Nuveen Quality Municipal Income Fund ( NAD ). The repeated forced deleveragings of PML means the fund has significantly underperformed a lower-beta fund like NAD. PML tends to gain on NAD during risk-on periods but then tends to give it all back and more during drawdowns.

Systematic Income

The third common strategy investors use to boost income is to allocate to riskier assets . Many investors are lulled into a false sense of security using this strategy when markets are particularly calm and when even lower-quality securities seem "money-good".

Many investors also feel compelled to move along the risk spectrum because in calm market environments the yields on higher-quality assets are puny. However, this situation tends not to last for very long as security prices and yields tend to revert and investors are often punished for moving out the risk curve during calm periods.

The following chart shows that investors who felt they were forced to buy CCC-rated assets to generate high single-digit yields in 2021 could have achieved the same yield in investment-grade securities by waiting for a bit over a year. And we are not even adjusting these yields by the expected default rates of CCC and BBB-rated assets - after which BBB-rated assets would clearly stand head and shoulders above their CCC-rated counterparts.

Systematic Income

Clearly, there is no formula for this kind of mean reversion but time and again market history shows that the temptation to increase risk in a calm market environment in order to keep yields high typically results in investor disappointment.

The key takeaway from this section is that the more "obvious" ways to grow income are often illusory and unsustainable.

Sustainable Strategies To Grow Income

In this section we review some of the strategies for increasing income that we consider to be more sustainable.

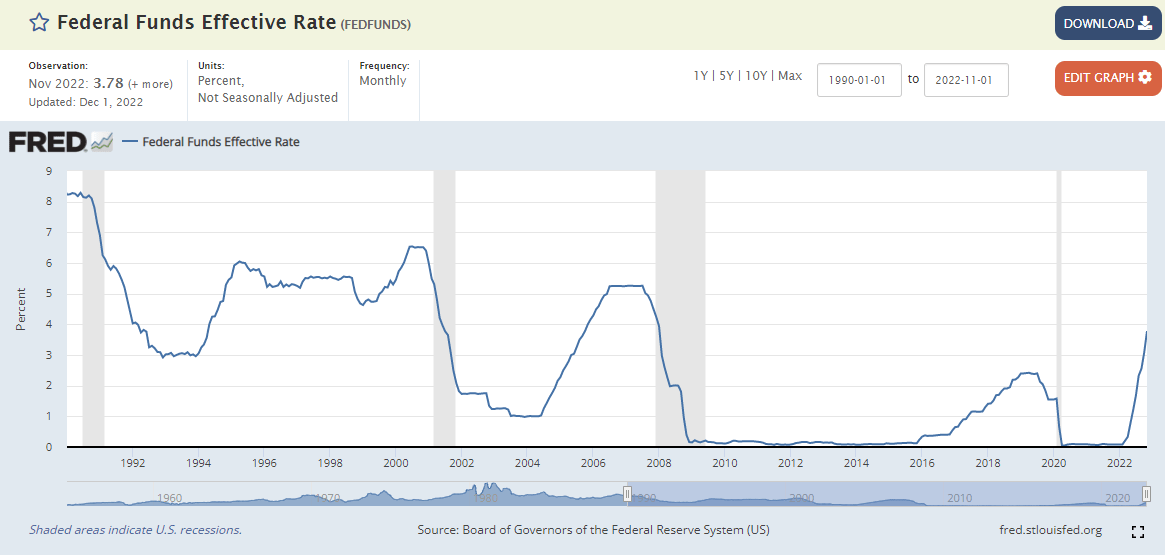

The first strategy is simply aligning portfolio allocation in the direction of short-term rates . As the following chart shows, unlike nearly all other assets, short-term rates tend to trend over time. This is clearly linked to the fact that Fed policy tends to trend over time. The Fed manages their cutting and hiking cycle gradually given the old adage of monetary policy working with "long and variable lags". The current interest rate hiking cycle has been unusually sharp, however, even this cycle will likely take at least a year.

{kind=link}

This is not a totally out-of-the-box strategy and many investors allocate to floating-rate assets in response to shifting short-term rates. However, it's important to add a key nuance which is that while for many investors this strategy is akin to upping exposure to loan CEFs during periods of rising short-term rates, we would put a number of other vehicles ahead of loan CEFs. Specifically, we would focus more on floating-rate preferreds, higher-quality BDCs and floating-rate crossover-rated bonds (i.e. those with decent-quality BB/BBB ratings).

The reason we wouldn't primarily focus on loan CEFs in a rising rate environment is three-fold. First, loan CEFs are not optimized for rising short-term rates since their leverage facilities are typically floating rate as well. Second, loan CEF are liable to a deleveraging during periods of market volatility - something we have seen this year across many leveraged CEFs. And three, rising short-term rates put pressure on loan borrowers many of whom are already relatively low quality (most loan CEFs sweet spot allocation is to B-rated borrowers).

The other three types of vehicles mentioned above don't have as many downsides. Floating-rate preferreds can be chosen across the quality-spectrum from investment-grade securities to lower-quality ones. Preferreds have another advantage of having specified coupons where it's easier to understand the income that investors receive - what you see is what you get - whereas loan CEFs may not bother to increase their distributions for some time, particularly if they were already overdistributing. Floating-rate preferreds have been a fixture of our Income Portfolios this year and have held up very well.

BDCs are much less liable to a deleveraging than loan CEFs as their NAVs are much more stable during periods of drawdowns. They also have a higher income beta to rising short-term rates due to their somewhat higher leverage and due to, in part, fixed-rate liabilities (the average BDC has about half of its liabilities in fixed-rate format).

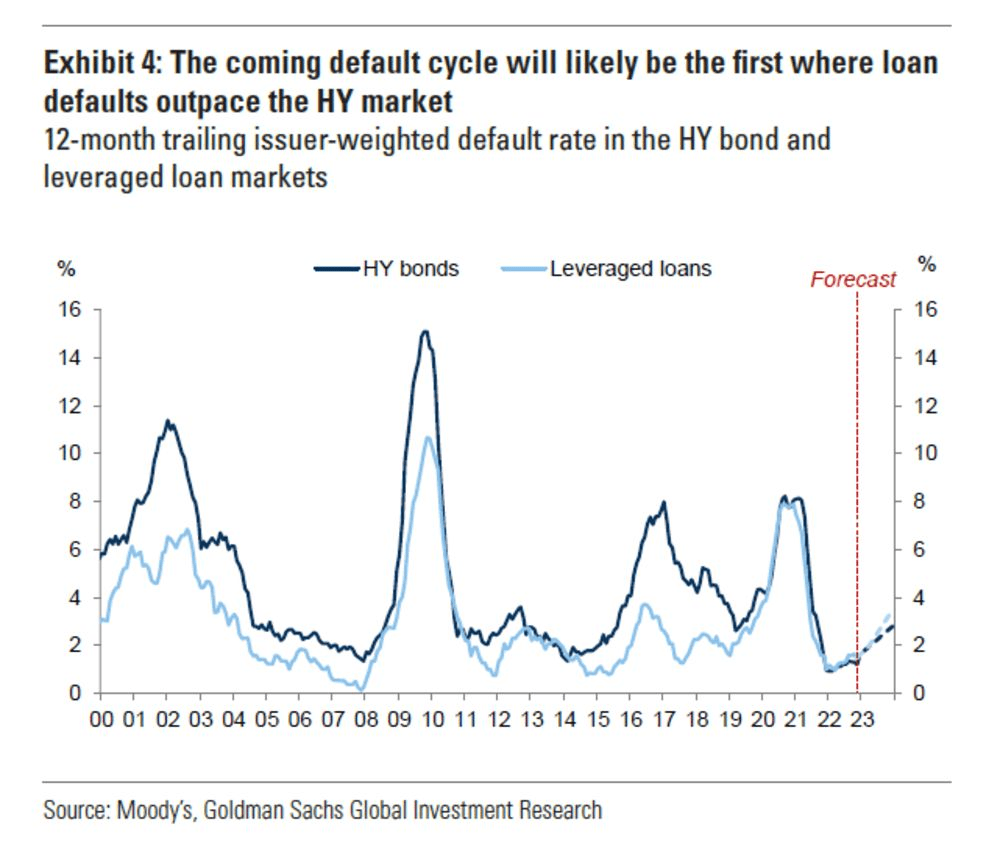

Finally, crossover-rated floating-rate bonds can be appealing as well due to their higher quality relative to bank loans. In short, defaults are less likely to eat away at investor income levels in these securities than for loans. As the chart below shows the loan default rate is expected by some analysts to exceed that of high-yield corporate bonds. Crossover rated bond default rates are significantly lower than for their high-yield counterparts.

{kind=link}

A second strategy of sustainably increasing income levels is what we call risk rotation . This strategy involves rotating between lower-beta assets such as open-end funds and higher-beta assets such as CEFs in response to overall valuations. The key intuition here is that income assets mean revert so taking some chips off the table when valuations are rich (e.g. in 2021) will allow investor portfolios to remain more resilient, with more capital remaining to be put to work in higher-yielding assets when valuations are very attractive (for most of 2022).

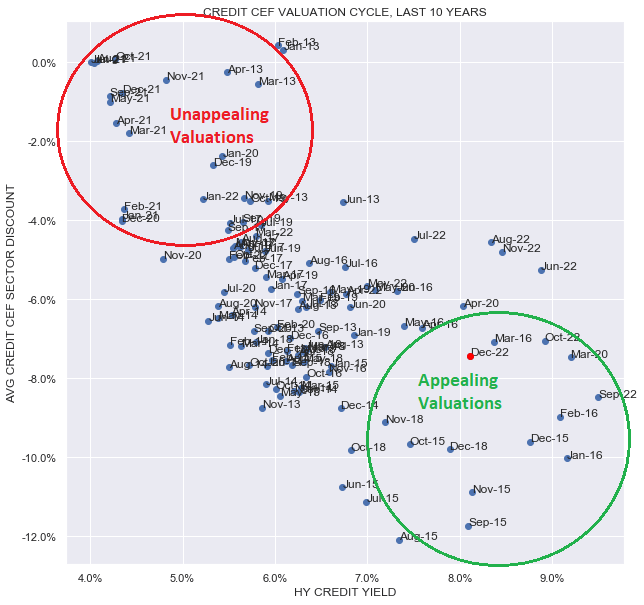

One way how we gauge overall valuations in the income market is by using a two-dimensional matrix of high-yield corporate bond yields (x-axis) and CEF discounts (y-axis). What this matrix shows us is that 2021 was almost uniformly unappealing featuring low asset yields and tight discounts. This year, on the other hand, looks much more attractive with high yields and wide discounts.

{kind=link}

In 2021, we significantly reduced our allocation to CEFs, precisely because underlying yields were low and discounts were tight. In the environment of 2021, CEFs did not generate much additional yield for investors over and above unleveraged open-end funds but only expose investors to greater losses if markets correct. That's pretty much what happened in 2022 with high-yield corporate bond CEFs, for example, registering losses double that of open-end funds as the extract from our Funds Tool shows below.

Systematic Income Funds Tool

However, now that both asset yields are high and discounts are wide we have been adding back to our CEF exposure.

A third strategy is relative-value switches where investors can switch between very similar assets based on relative valuation. This strategy is particularly effective during drawdown periods or in taxable accounts where capital gain tax implications are lower.

This year we have taken advantage of a number of these switches in the following pairs:

- Credit Suisse high-yield corporate bond CEFs ( CIK ) and ( DHY )

- Cohen & Steers preferreds CEFs ( LDP ) and ( PTA )

- PIMCO credit CEFs ( PDO ) and ( PAXS )

- Annaly preferreds ( NLY.PF ) and ( NLY.PG )

- Two Harbors preferreds ( TWO.PA ) and ( TWO.PB )

The chart below shows a normalized total return of two NLY preferreds: NLY.PF and NLY.PG . As the chart shows we held NLY.PF through November at which point we switched to NLY.PG when F became very expensive on a forward yield basis. Then, once G caught the eye of investors and rallied sharply relative to F, outperforming it by around 7%, we switched back to F which we continue to find more attractive.

Systematic Income

We did something similar with two PIMCO sister CEFs: PAXS and PDO which have flipped around in relative value terms quite a bit this year.

Systematic Income

This strategy of rotating across very similar securities is attractive as it not only locks in higher yields for nearly identical exposure but also provides an additional margin of safety in the process.

Takeaways

Gradually increasing income in investor portfolios is one of the goals that many investors have. However, the more obvious strategies to make this happen can also be unsustainable and ultimately self-defeating. Chasing the highest yields on offer, allocating to highly leveraged CEFs and moving out the risk spectrum when yields fall are strategies that are unlikely to deliver on investors goals.

More sustainable strategies in growing income are to allocate in response to shifting short-term rates via appropriate investment vehicles, allocating between lower and higher-beta income assets in response to valuation in a countercyclical fashion and taking advantage of relative value switches. These strategies are more likely to allow investors to organically grow the income levels of their portfolios over time and meet their investment goals.

For further details see:

Strategies For Growing Income In The New Year