RGR - Sturm Ruger: Absence Of Meaningful RoR Does Not Take Away The 'Buy'

2023-07-24 04:12:58 ET

Summary

- My investment in Sturm, Ruger & Company, the largest manufacturer of firearms in the US, has not performed as expected due to the volatile nature of the firearm industry.

- Despite current negative returns, I remain bullish on the company due to its low debt, impressive profit margins, and significant cash flow generation.

- The company's latest results have been better than its valuation suggests, and it continues to adjust its production mix to align with demand, despite a 10% YoY decrease in sales.

Dear readers/followers,

My investment into Sturm, Ruger & Company ( RGR ) has so far not exactly gotten as I've been wanting it to go. Any investment resulting in negative RoR isn't the best investment made, even if my forward expectation, as with this one, includes the company reversing course and seeing better returns.

The firearm/weapon industry is notoriously volatile and correlated to both political and other realities which makes investing in it tricky. That is also the reason why part of my investing strategy, early on, actually included sticking to conservatively priced put options. The risk/reward there was much better.

But now I have native shares in the company, and these are currently in the negative - so let me update on this company and show you why I'm still bullish on the company in the longer term.

Sturm, Ruger - Plenty of upside in firearms - if you have the right expectations

So, first off. You know that this company is in fact the largest manufacturer of firearms in all of the US. Despite this, and despite the popularity of shooting ranges, hunting, and the like in the nation, this company is severely undercovered on SA, likely owing to the trickiness of investing in the business.

However, I want to make one thing clear.

If you're a long-term holder on RGR, if you can handle the ups and downs, and if you haven't sold for over 20 years, you're doing very well for yourself, and your position is significantly in the green.

However, you've done so with the stability of a rollercoaster.

Still, a few things to consider before you leave companies like this behind.

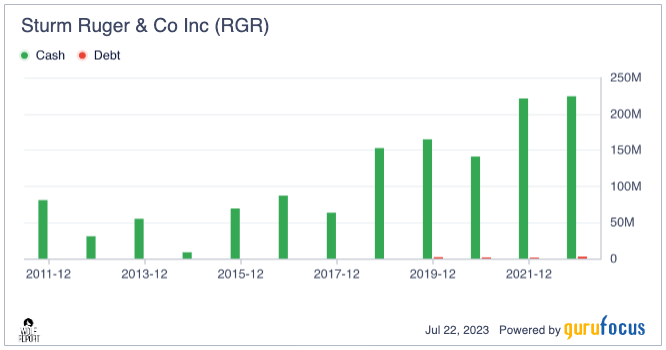

Sturm & Ruger is an extremely cash-heavy, low-debt (a debt/equity of 0.01x, debt to EBITDA of 0.03x, and interest coverage of 430x) , and also comes in with some extremely impressive profit margins. This includes gross margins of almost 30%, operating margins of almost 15%, and net margins of 12.5% and above.

As you might expect, the company is very COGS-heavy, with over 65%, and very OpEx light, with only 12.9%, highlighting a very streamlined SG&A organization, but being a manufacturer of these sorts of weapons. Nonetheless, for 2022, the company managed a net profit margin of almost 15%. Like another company I recently wrote about, Deutsche Börse ( OTCPK:DBOEY ), Sturm, Ruger is very cash-heavy and debt-low in its operations. This lack of debt utilization increases company safety, as It essentially makes the company immune to interest rate risk - at least in terms of financing.

Sturm & Ruger cash/debt (GuruFocus)

{kind=link}

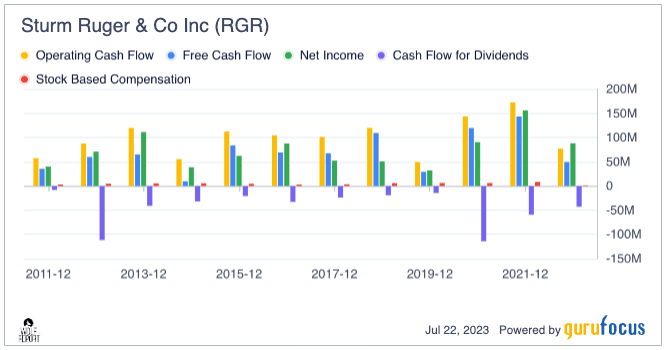

While the company's revenue/net trends do show a significant amount of volatility over time, with lows at 30-60% below highs, the company is an over-time generator of impressive operating, free, and dividend cash flow. It is, however, one of the few US-based companies that entirely scales its dividend payouts for its operating cash flow and income. This makes the dividend difficult to rely on, more than expecting that there will likely be a dividend as long as the company is profitable.

{kind=link}

And this profitability, net of WACC has been easy when the WACC is devoid of almost any cost of debt. The company also hasn't been a heavy issuer of new shares for over 7 years, instead having bought back a significant amount over the past three.

It is, simply put, a company that is doing very well, and where the stockholder equity portion of the total company assets at times has been over 90%, which is one of the best I've ever seen reviewing any company.

The latest results have been better than the company's valuation would suggest.

The company does everything you'd be looking for in firearms. RGR manufactures Rifles, Revolvers, Pistols, Accessories, and other things. The company reported its last quarter about 1.5 months back, and this quarter came in at almost $150M in net revenues, with diluted earnings of 0.81$ on a per-share basis. The company also continued its policy of 40% net income in dividend and sized its dividend at $0.32.

The company can't do much about declining consumer demand - and that's what drove the 10% decrease on a YoY basis in sales - but these comps were on a very high level. As always, RGR adjusted its production mix to align with demand. This, together with continued responsible inventory management is the key to the company's longer-term success, including strong cash flows.

The fact that the company doesn't use debt is actually what sets the business apart from the risk otherwise inherent to this market. I would argue that any market as cyclical and as volatile as this, where the fundamentals aren't really backed up by anything substantial beyond PP&E requires different risk/reward considerations. Sturm, Ruger has done exactly this.

Some news on the political front, which continues to be a major impact on a business like this. Some positives include that several states have moved against state agencies, prohibiting them from engaging with banks that discriminate against firearms and munition businesses. The FIND Act is another piece of legislation to keep an eye on, as it may become relevant going forward.

Sturm & Ruger is especially exposed here. It can confirm that Bank of America ( BAC ) and Wells Fargo ( WFC ) within the past five years have confirmed that they will not provide credit because of the products they sell. This is objectively hypocritical, given that these banks provide credit to companies that within the scope of their international operations have been known to use child labor, to flout environmental laws and other local, national, and international laws.

I've always personally been surprised by the hypocrisy that some investors employ, arguing against defense and military companies while gleefully investing in companies that for several decades have employed predatory marketing strategies which are objectively as controversial, but perhaps with a different target audience.

I personally will invest in most companies - and considerations like the ones made above will not prevent me, or dictate my investments. But as an investor, I'm always against that law-abiding companies being discriminated against on the basis of them selling products that a certain category of investors, citizens, or legislators disagree with - so I welcome legislation that prohibits this.

Aside from such considerations, what I would be looking for when it comes to this company is inventory and demand as well as production trends. The company is, based on experience, apt at managing this. At most, you'd see an imbalance in demand and inventory that might take 8-16 months to normalize, as we saw during some periods of COVID-19.

Specific highlights for the quarter include sales of new products, including the new MAX-9 pistol, the LCP MX, the new 1895 Marlin lever-action rifle, and other products. The company's margins did drop, and this was due to fixed costs, decreased production and sales, as well as inflation from production costs, inflation in transport, energy, and fuel.

The industry seems to have gone into a "rebate" mode, which the company confirms, with plenty of promotional activity at the stores- The company also expects a bit of seasonal slowdown, but with the company's lineup, the demand picture is a bit more nuanced. For instance, demand for the new Marlin rifle remains solid, to the degree that the company has to increase production.

With this mixed picture, we look at valuation and future potential upside.

Sturm, Ruger - The valuation remains compelling in case of an upside

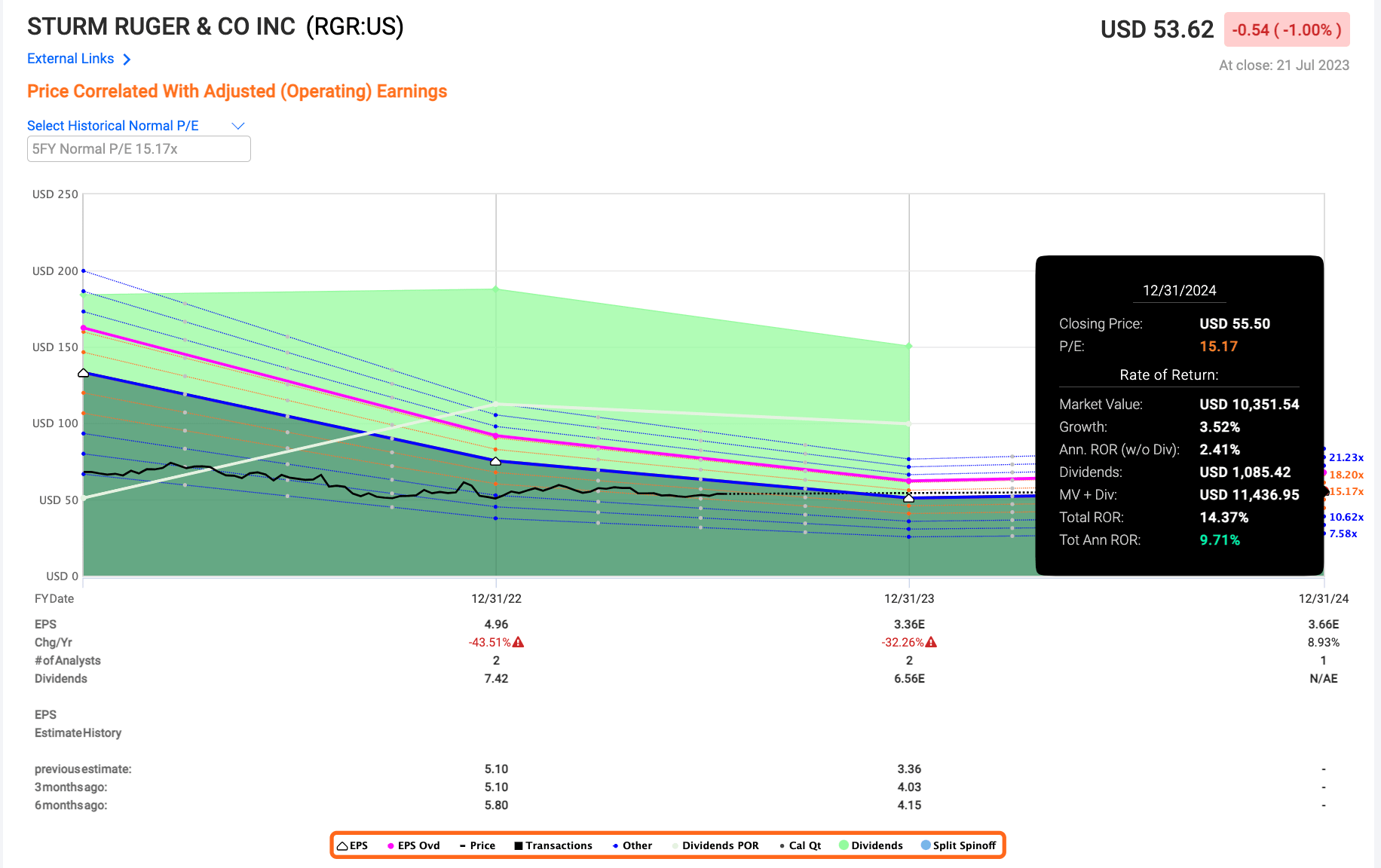

There will be one change for my thesis for Ruger as of this article. I no longer consider the company to be "cheap" here on the basis of forward valuation. The current expectation is for a bottoming of the share price and demand in 2023E, with an upside beyond this.

At a forward 15-16x P/E, this is an upside close to the double digits.

{kind=link}

I would also like to point out at this time, that I expect RGR to do significantly better than this. I base this on historical data, with the company beating analyst expectations more than 65% of the time (Source: FactSet).

Beyond this, consider for a moment that other analyst targets have this company at least 25% higher than the current share price. This is based on analyst targets from S&P Global, starting at a low of $64, and going up to $70/share, well above the current share price levels.

In the end, this company has the sort of long-term upside I'm looking for. It's no longer cheap. I'd also argue that the company is a solid target for selling cash-secured puts, or maybe some write-buy strategies with covered calls above buying the common share here. But for me, owning common shares in the company, I would not sell my shares here, and I can't fault anyone that's interested in adding shares of RGR at this valuation.

Be aware of the volatility, and be aware of the political realities of this stock - but I would also say, don't be afraid of investing in a stock because it's volatile or subject to political volatility. Not if the underlying company is solid.

And despite what you may read in other articles, or see in terms of share price, this is a solid company with excellent fundamentals.

Because of that, here is my current thesis for the company.

Thesis

- This is an absolutely solid business despite the lack of a credit rating and the choppy, volatile earnings and dividend history as well as political instability.

- If bought at the right price, RGR is a proven candidate to deliver solid Alpha over both short and long periods of time. You're investing in a timeless segment - don't necessarily listen to what moral-oriented investors tell you here. As long as humans have been around, we have fashioned weapons to defend ourselves and our loved ones with, as well as for sport. This is a modern iteration of this.

- RGR is a "BUY" with a PT of $72. I'm impairing heavier for inflation, input, and the fact that I expected demand to stay somewhat higher than we're seeing here.

- I still view Options as an attractive play here, as well as the potential of using some buy-write strategies.

Remember, I'm all about:

- Buying undervalued - even if that undervaluation is slight and not mind-numbingly massive - companies at a discount, allowing them to normalize over time and harvesting capital gains and dividends in the meantime.

- If the company goes well beyond normalization and goes into overvaluation, I harvest gains and rotate my position into other undervalued stocks, repeating #1.

- If the company doesn't go into overvaluation but hovers within a fair value, or goes back down to undervaluation, I buy more as time allows.

- I reinvest proceeds from dividends, savings from work, or other cash inflows as specified in #1.

Here are my criteria and how the company fulfills them ( italicized ).

- This company is overall qualitative.

- This company is fundamentally safe/conservative & well-run.

- This company pays a well-covered dividend.

- This company is currently cheap.

- This company has a realistic upside based on earnings growth or multiple expansion/reversion.

This means that the company fulfills every single one of my criteria except it being cheap, making it relatively clear why I view it as a "BUY" here.

For further details see:

Sturm, Ruger: Absence Of Meaningful RoR Does Not Take Away The 'Buy'