RGR - Sturm Ruger & Company: Holding Not Buying

2023-05-11 18:01:31 ET

Summary

- I think the most recent financial results reveal that the company is obviously on a downswing. In spite of this, I'm hanging on to my shares.

- The balance sheet is rock solid, putting this company head and shoulders above the vast majority of public companies. The prudent dividend policy is also compelling.

- The problem is the valuation. A great company like this one can be a terrible investment at the wrong price. I think the price is currently wrong.

It's been a little over five months since I wrote my latest bullish piece on Sturm, Ruger & Company (RGR), and in that time the shares have returned a loss of about 4.7% against a gain of 3.5% for the S&P 500. I thought I'd review the name again to see if it makes sense to finally take my lumps here, and move on, or to buy more at a cheaper price. The company reported earnings since then, so I thought I'd review those. Additionally, shares trading at $53.65 are, by definition, a less risky investment than shares trading at $56.75, so I thought I'd review the name again.

It's a very busy world in which we find ourselves, and for that reason I offer a "thesis statement" near the beginning of each of my articles. I do this so you'll be able to get into the article, get the "gist" of it, and then get out before being exposed to too much Doyle mojo. You're welcome. While I'm a fan of this business, I think we all have to acknowledge that the firm has taken a downturn recently. I'm comfortable hanging on, given the solidity of the balance sheet among many other positives, I'm not comfortable adding at the moment. The reason for this is that the shares are no longer as cheap as they were when I last reviewed the name. Add to that the fact that an investor can earn about 100 basis points more than the much vaunted dividend in a risk-free investment, and I see nothing compelling here at the moment. I'm comfortable holding my shares, but I'm of the view that it would not be prudent adding at current levels. When the business picks back up and/or when the risk-free rate falls from current levels, I'll review again. For now, though, I'm holding, not adding.

Financial Snapshot

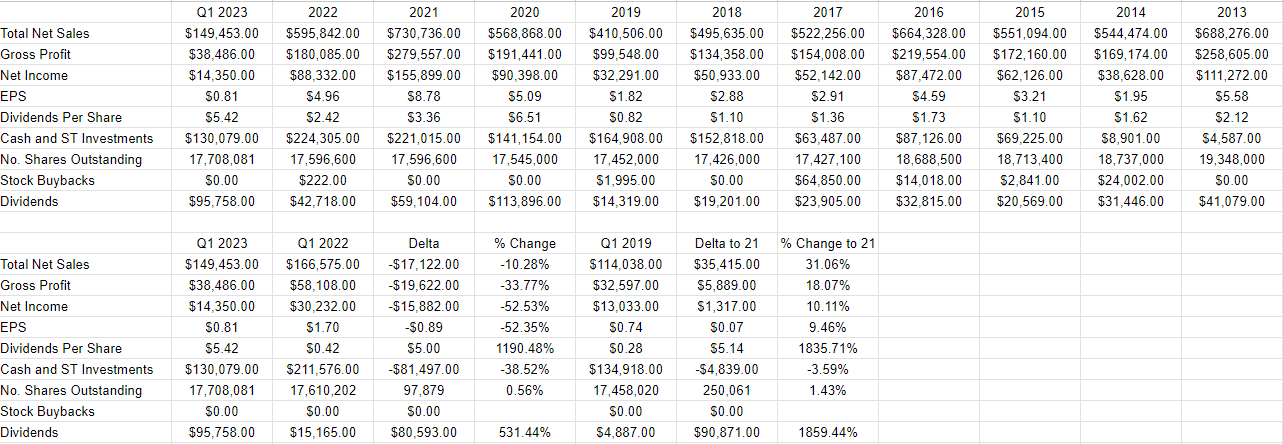

The latest financial results have been predictably lackluster. As I suggested in my prior post on this name, the business cycle exists, and if you're going to invest in this, or any other business, you should be aware of that fact. So, the latest quarter was much weaker than the same period a year ago. Specifically, revenue and net income were lower by 10.3%, and 52% (!), respectively. The net income dropped so precipitously more as a result of a thousand financial cuts than a single issue. For instance, COGs were up only 2.3%, selling expenses increased by 9.4%, and G&A expenses increased by 11.8%, none of which stand out as being egregious given what was going on in 2022. So, costs are relatively fixed, and may move higher in the teeth of falling revenue. The fixed nature of such things is a risk here, and we shareholders should be aware of it.

I should also point out that the capital structure remains quite robust, which strongly implies that the dividend is very well covered. Specifically, as of the most recent filings, the company had cash and short term investments in the amount of $130 million, and total liabilities amounting to only about $67 million. At a time when many investors are worried about the capital structure of many small businesses, this is no small thing in my view.

So, I think an investor in this stock should gird themselves for some volatility. The company is certainly subject to the vagaries of the ups and downs of demand for firearms. In the background, though, is the fact that management throws its pennies around like manhole covers, as evidenced by the dividend policy, and the very clean capital structure. Additionally, management has a demonstrated history of treating shareholders very well with the odd special dividend. For my part, I like this approach to capital very much, because often times, I'd rather see it in my hands than at management's discretion.

Given the above, I'm comfortable continuing to add to my position here, assuming the valuation is reasonable.

Sturm Ruger Financials (Sturm Ruger investor relations)

{kind=link}

The Stock

If you're one of my regulars, I can understand that you might be thinking the phrase 'assuming the valuation is reasonable" has caused me to talk myself out of great buys in the past, and you'd be right. Sometimes I eschew a stock because it's not cheap enough, and it goes on to perform well. In response, I'd remind my readers, yet again that I'm of the view that it's better to miss out on some gains than lose capital. So my fastidiousness not only causes me to miss out on some gains, but also some losses.

Additionally, if you read my stuff regularly, you know that I consider the "business" and the "stock" to be quite different things. Every business buys a number of inputs and turns them into a final product or service. The stock, on the other hand, is an ownership stake in the business that gets traded around in a market that aggregates the crowd's rapidly changing views about the future health of the business, future demand for investment intelligence services, future margins, and so on. The stock also moves around because it gets taken along for the ride when the crowd changes its views about "the market" in general. A reasonable sounding, if counterfactual, argument can be made to suggest that shares of Sturm Ruger would be even more attractively priced if the S&P 500 itself wasn't up by ~3.5% since. If the demand for "stocks" as an asset class hadn't held up well, my shares may well have fallen further in price. Of course, it's impossible to prove this point definitively, but it's worth considering. In any case, the stock is affected by a host of variables that may be only peripherally related to the health of the business, and that can be frustrating.

This stock price volatility driven by all these factors is troublesome, but it's a potential source of profit because these price movements have the potential to create a disconnect between market expectations and subsequent reality. In my experience, this is the only way to generate profits trading stocks: By determining the crowd's expectations about a given company's performance, spotting discrepancies between those assumptions and stock price, and placing a trade accordingly. I've also found it's the case that investors do better/less badly when they buy shares that are relatively cheap, because cheap shares correlate with low expectations. Cheap shares are insulated from the buffeting that more expensive shares are hit by.

As my regulars know, I measure the relative cheapness of a stock in a few ways, ranging from the simple to the more complex. For example, I like to look at the ratio of price to some measure of economic value, like earnings, sales, free cash, and the like. I like to see a company trading at a discount to both the overall market, and to its own history. When I last reviewed Sturm Ruger, I liked the fact that the shares were trading at a price to free cash of about 14.65, a PE ratio of about 10.25 times, and the dividend yield was sitting at about 3.9%. Fast forward to the present, and here's the lay of the land.

So, at the moment, the shares are between 27% and 43% more expensive, and the dividend yield is about 150 basis points lower than it was when I last reviewed this name. Additionally, I think it necessary to place this investment in the context of a world where an investor can receive about 100 basis points more on a risk- free investment than they can on these shares.

In addition to looking at ratios, I want to try to understand what the crowd is currently "assuming" about the future of a given company, and in order to do this, I rely on the work of Professor Stephen Penman and his book "Accounting for Value." In this book, Penman walks investors through how they can apply the magic of high school algebra to a standard finance formula in order to work out what the market is "thinking" about a given company's future growth. This involves isolating the "g" (growth) variable in this formula. In case you find Penman's writing a bit dense, you might want to try "Expectations Investing" by Mauboussin and Rappaport. These two have also introduced the idea of using the stock price itself as a source of information, and then infer what the market is currently "expecting" about the future.

Anyway, applying this approach to Sturm Ruger at the moment suggests the market is assuming that this company will grow profits at a rate of about 5.5% from here. In my view, that is a pretty optimistic forecast.

I'm of the view that in the domain of investing, everything's relative, and we're always hunting for the most attractive alternative. Given that these shares are no longer objectively cheap, and given that it's possible to earn 4.7% risk-free at the moment, I'll not be adding to my stake here. I'm not going to sell my shares, but I won't add until such time as the price takes another tumble.

For further details see:

Sturm, Ruger & Company: Holding, Not Buying