RGR - Sturm Ruger & Company: Valuation Is Key But I'm Still At A Buy

Summary

- I own shares in Sturm, Ruger & Co., and have done so for about half a year at this point, with three instances where I bought small portions.

- Part of the buys are in the green - but I'm mostly flat/red on this position if we take away FX. Sturm, Ruger has somewhat underperformed.

- I'll revisit the company for 2023 - I like firearms companies, but investing cheap is really key here to see good RoR.

- I believe there is upside to be had in RGR, though that requires a decent amount of risk tolerance.

Dear readers/followers,

I've been following up on the more prominent firearms companies on the market for about a year at this point. One of my first forays into the sector was the company Sturm, Ruger ( RGR ), and my coverage hasn't exactly, this far, returned the most positive of results. Thankfully, my position in the company remains a small one for the time being.

I do want to invest and have exposure to this sector - because I believe in the necessity for the product, and I believe these companies and their peers have a hard-to-assail position on the market - a bit of a moat if you will.

We already saw a large drop, and somewhat of a recovery in the company.

Let's see what we can see for 2023.

Looking at Sturm, Ruger for 2023

Investing in the largest firearms manufacturer in the US shouldn't be a hard sell, but the company is relatively under-covered - and its somewhat meager longer-term RoR goes some way to explain this.

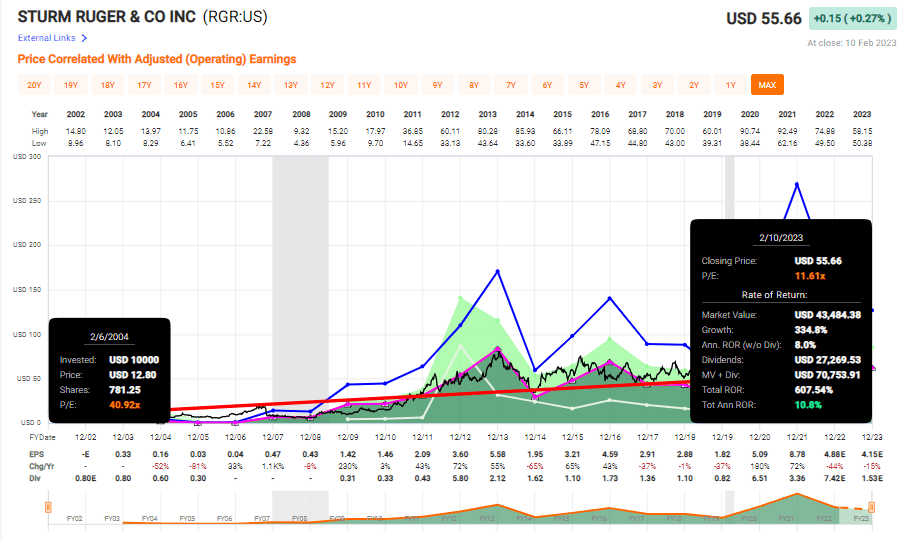

Oh, long-term investors in RGR have beaten the market quite handily - but they've done so with significant volatility, ups, and downs in valuation that should have dictated trim and entry points even at the time, and a pattern that calls into question how we should go about investing in the business here.

F.A.S.T graphs RGR RoR (F.A.S.T graphs)

{kind=link}

I doubt there's anyone reading this article that's held the stock for 20+ years - but if so, please let me know because I'd be interested!

Anyway, the latest trends out of Sturm, Ruger are not uninteresting - especially in the light of the relatively recent dividend bump we saw in 2022 of almost double digits, reflecting good company performance. However, as with any company in this field, RGR is a play as much on inventories as on sales. The company had sold out of most of its inventory in 2021, and part of why I liked investing in RGR is that unlike certain companies I could name (adidas ( ADDYY ), V.F. Corp ( VFC ), I'm looking at both of you), RGR has exemplary inventory management and cycling.

This can be exemplified through recent management increases in production of 30%, while manpower only increased by 10% - extremely efficient manufacturing. The fact that most/all the manufacturing for the company, with the exception of input/feedstock, is done domestically, insulates this business from the typical uncertainties and patterns we see in other manufacturing. It's a positive, as I see it.

The ordinary dividend isn't the only positive, of course. In fact, in November, the company declared a truly massive extraordinary dividend, more than twice the annual level, reflecting the company's extraordinary results. This dividend was paid out in January. I would have highlighted this further, but given the RoR in my positions at the time, and that it really, at this point, isn't a massive position for me, argued against over-emphasizing this investment as such.

However, recent results deserve a bit more - because they actually went in a different direction than I would have expected. 3Q22 came out in November, and the company reported a significant diluted EPS decline, as well as a net sales decline.

The problem wasn't consumer demand, even if inflation played a role. The issue, or the trend, was an overall lower 2022 demand flow compared to the 2021 level, which due to COVID-19 was really something of a record/non-recurring year.

This also saw significant margin impacts - not only due to lower sales, but due to inflation. GM went from 36% to 28% - and this came from unfavorable fixed costs due to lower production and sales, as well as costs in inputs/commodities used by the company to manufacture. Energy and fuel were obviously more expensive as well.

RGR was one of the companies here that did not manage to offset these increases with price increases. The company's net results were positively impacted by a significantly lower tax rate - less than half of 2021 - due to R&D tax credits - but that's about as positive as it gets here. The company's extremely low/zero debt ambition makes looking at shareholder equity more interesting here. The fact is that as of the latest quarterly results, the BV/share was just north of $22.5/share here, which based on today's share price implies a relatively low overall multiple for buying the company here.

RGR continues to invest in manufacturing and modernization - $25M in the last quarter alone, and they bought a new facility in NC used for both manufacturing and warehousing - that's 225,000 new square footage. This isn't a new asset for the company - if you look through the latest financials, you'll see that the company has been leasing the area for over a year, but it's new insofar that the company owns it as opposed to leasing it.

When we look at the granularity with regard to demand, we can see that 2022 volumes of NICS background checks, which are typically a pretty good indicator of future demand trends, are down 14% YoY. The inflation-related pressures impacting consumer spending especially were noticeable in modern sporting rifles and polymer centerfire pistols, products which had seen significant popularity in recent years.

The company's new innovations and products tend to do better - and RGR released the LC Carbine, a command – a companion carbine to the successful router 5.7 pistols. RGR also brought a new SFAR chambered in 308 Winchester, and the marlin Model 1895, which reintroduces the Marlin Guide Gun family of lever-action rifles to the market.

Sales of the company's new products were better than expected, and the company is ramping up production here, while also maintaining a strong production of legacy products.

If you recall my first article on Ruger, I actually went "into" the company using an attractive options play. That was my first contact with the business, prior to establishing a small position in my portfolio - that currently, and on the whole of it, is in the negative. Transparency is key here - view the option play as a success, the investment, because investing is a binary activity and I compare it to index development, was a failure because it's been underperforming, not outperforming.

Can we expect better going forward?

Sturm, Ruger Valuation - there's an upside, but it's tricky

Most of my play with Ruger has been through options - and that remains the main avenue of investing that I take in the company. While I do own a small stake in common shares, the forward potential for these has some limitations, as I see it.

There is an upside to investing in the common, first of all. Not just in Book value/share, in NAV, or in other relatively simple sales or revenue multiples. I always look at multiple perspectives when establishing that a company has an undervaluation, and RGR at 11.6x P/E normalized, is undervalued - and I'd happily defend that assertion if you don't share or see it.

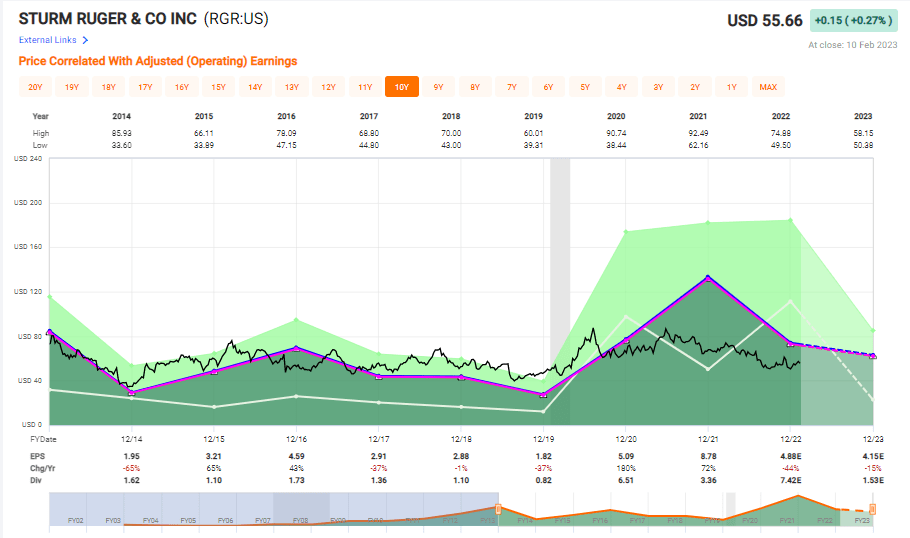

However, the forecast accuracy for companies like these is extremely poor. I'm uncomfortable going further than 2-3 years in the future due to the volatility of how these businesses earn. In 2022, we saw a massive EPS decline due to the 2021 record period. EPS on an adjusted basis declined by over 44%, and it's forecasted to decline even further in the 2023E fiscal. Now, this may sound like an absolute horror show, but it's crucial to understand where this comes from in the longer term. Take a look at the 10-year EPS trend.

F.A.S.T graphs RGR (F.A.S.T graphs)

{kind=link}

So, you can see that even normalizing down below $4/share, this company would essentially still earn more than it did most of the past 10 years. Seeing what sort of impact this has on valuation is interesting - because as you can see the company really moves up and down in response to these earnings and trends. The dividend is also unstable as such, impacted by a significant amount of extraordinary dividends in great times. Over the past 10 years, it can generally be said that "BUY"ing the company at below $45/share, you would have beaten the market. That's an extremely low share price, but that's where I see basically a "guarantee". My previous PTs ranged from $70-$80/share for the company.

The latest S&P Global trends are impacted by how expectations are looking for this next fiscal. The average is down to around $68/share based on a total of 2 analysts - not many following that company, and changes in their PTs are relatively rare. 1 analyst is at a "BUY", and 1 at a "HOLD". Very little in terms of trends can be gleaned from that.

Forecasting here is hard. While I do see a double-digit sort of upside for a 15x normalized P/E on a 2023E basis, and I can say that compared to most of the relevant peers in sports outside the firearms sector, the company is undervalued, that is not true when we consider that RGR is heading into this with negative estimated earnings, and at a valuation that comes in above that of say, Smith & Wesson ( SWBI ) in not only revenues but in EBITDA, P/E and in a pure DCF upside perspective as well.

This sector is small, dear readers. It's small if we look at the firearm leisure category - there are only RGR and SWBI. In DCF, I use a double-digit discount rate with a growth rate of 4-5% per year on the terminal side, which calls for an average range starting at $62 and going up to $75/per share. Add my own calculations in terms of the multiples and forecasts here, and I would impair that somewhat, lowering my PT for RGR to around $72/share.

That still makes this company a "BUY" - but I would still take a look at favorable options plays above common share investments - especially if you can write some CSPs during a down day when premiums are statistically more likely to be higher.

If possible, I would then target strikes of at, or below $45/share at a 30-90 day expiration. I believe that's a decent way to go about investing in RGR.

Other than that, you can still buy the common - but I view this as the less attractive possibility here.

This is my 2023 thesis on Ruger, updated for the estimated EPS for the coming year.

Thesis

- This is an absolutely solid business despite the lack of a credit rating and the choppy, volatile earnings and dividend history.

- If bought at the right price, RGR is a proven candidate to deliver solid Alpha over both short and long periods of time. You're investing in a timeless segment - don't necessarily listen to what moral-oriented investors tell you here. As long as humans have been around, we have fashioned weapons to defend ourselves and our loved ones with, as well as for sport. This is a modern iteration of this.

- RGR is a "BUY" with a PT of $72. I'm impairing heavier for inflation, input, and the fact that I expected demand to stay somewhat higher than we're seeing here.

- I view Options as the more attractive play here, however.

Remember, I'm all about:

- Buying undervalued - even if that undervaluation is slight and not mind-numbingly massive - companies at a discount, allowing them to normalize over time and harvesting capital gains and dividends in the meantime.

- If the company goes well beyond normalization and goes into overvaluation, I harvest gains and rotate my position into other undervalued stocks, repeating #1.

- If the company doesn't go into overvaluation but hovers within a fair value, or goes back down to undervaluation, I buy more as time allows.

- I reinvest proceeds from dividends, savings from work, or other cash inflows as specified in #1.

RGR is a "BUY" with a PT of $80/share.

Here are my criteria and how the company fulfills them ( italicized ).

- This company is overall qualitative.

- This company is fundamentally safe/conservative & well-run.

- This company pays a well-covered dividend.

- This company is currently cheap.

- This company has a realistic upside based on earnings growth or multiple expansion/reversion.

This means that the company fulfills every single one of my criteria, making it relatively clear why I view it as a "BUY" here. It should be noted though that some of these are somewhat individualized - there is no credit rating, the dividend is choppy, and the company is in a downward trend. Consider this prior to buying/writing.

Thank you for reading.

For further details see:

Sturm, Ruger & Company: Valuation Is Key, But I'm Still At A Buy