RGR - Sturm Ruger: Delivered Increase In Sales Price And Headcount Growth Could Enhance Stock Price

2023-07-31 05:59:20 ET

Summary

- Sturm, Ruger & Co. has a product catalog that includes rifles, pistols, and revolvers, with a focus on the domestic market.

- The company has a clean balance sheet with no debt and a healthy asset/liability ratio.

- The company's financial model suggests that headcount growth, R&D investments, and increases in the average sales price could lead to a valuation of $89 per share.

Sturm, Ruger & Company ( RGR ) delivered an increase in the average sales price, which may have a beneficial effect if the demand trends back after the decline in recent quarters. I would also expect further headcount growth and innovations considering the investments in R&D and the know-how accumulated in 70 years in the industry. Additionally, with a clean balance sheet, I think that new opportunistic acquisitions like that of Marlin Firearms would enhance future FCF margins. Yes, inflation, lack of raw materials, or changing regulatory framework in the United States are major risks, however I think that the stock could trade at much more than its current market price.

Sturm, Ruger & Company

With a product catalog that includes rifles, pistols, and revolvers, Sturm, Ruger & Co is a company dedicated to the design, manufacture, and marketing of firearms for domestic users in the United States.

{kind=link}

Source: Corporate Website

{kind=link}

Source: Corporate Website

Due to global legislation on the use of firearms, the products of this company are mostly consumed locally. During 2022, only 6% of production was assigned for export. Sales are made through independent distributors and wholesale as well as to final consumers, mainly in markets related to the sports field.

Sturm, Ruger & Co has two business segments: firearms and ammunition. The firearms segment includes the sale of rifles, revolvers, and pistols. In 2022, it represented almost all of the company's revenue. The second of these segments manufactures elements from metal casting, ammunition, and accessories, and represents a minimum production in the company's operations.

Regarding its clients, we can highlight the great concentration of sales that exists. Its 3 main buyers, namely Lipsey’s, Davidson’s, and Sports South, represent more than 60% of the company's annual sales. If we read the domestic firearms market, the lack of diversification becomes understandable as there are few dealers with official federal licenses for sales nationwide.

As shown in the quarter ended April 1, 2023, most revenue came from the sale of firearms. With a fat gross profit, the company also reported positive operating income, which represented close to 11%. The figures for the quarter were a bit worse than that reported in 2022, however management did report positive quarterly net income.

Source: 10-Q

Like other financial advisors, I expect a slight decline in net sales, Q2 2023 EBITDA margin, and operating margin growth. Quarterly sales close to $135-$140 million, and an operating margin of around 13% appears reasonable. If the numbers are better than expected, the stock price may increase. However, given the decreased consumer demand for firearms delivered in Q1 2023, I do not expect significant changes in Q2.

Source: Market Screener

The Recent Decrease In Assets Was Not Alarming, And The Balance Sheet Appears Quite Clean

In the last quarterly report, Sturm, Ruger & Co noted a decrease in assets driven by lower short-term investments, lower inventories, and lower property and equipment. I am not concerned about the decrease in assets because the company does not really report liabilities, and the recent net sales decline does not seem alarming. With that, investors may want to have a look at the most recent quarterly report. They also want to check the new 10-Q to assess whether the decrease in assets would continue.

As of April 1, 2023, the company reported cash worth $8 million, short-term investments worth $122 million, trade receivables of about $65 million, prepaid expenses and other current assets close to $6 million, and total current assets of about $263 million. Total current assets are significantly larger than the total amount of liabilities, so I believe that the company does not suffer from a problem of liquidity.

Long term assets include net property, plant, and equipment of about $72 million and deferred income taxes of about $6 million. Total assets stand at about $389 million, and the asset/liability ratio looks quite healthy. In sum, I believe that the balance sheet appears quite clean with no debt and little accounts payable.

Source: 10-Q

The list of trade accounts payable and accrued expenses stands at close to $33 million, with contract liabilities with customers of about $1 million, employee compensation and benefits close to $17 million, and total current liabilities of close to $61 million.

Source: 10-Q

Financial Model: Headcount Growth, R&D, And Increases In The Average Price Of Ending Backlog Could Lead To A Valuation Of $89 Per Share

Under my assumptions, I included continued headcount growth, which I believe is one of the secrets of Sturm, Ruger & Co. After more than 70 years in the same industry, the company appears to offer beneficial packages to employees, who stay a long time with the company. In my view, the following text from the annual report and the headcount growth chart are valuable.

The Company is an equal opportunity employer dedicated to the attraction, development, and retention of our employees by providing a preferred work environment that promotes and celebrates our core values of Integrity, Respect, Innovation and Teamwork. Our goal is to develop, motivate, retain and reward passionate and dedicated employees. As of February 1, 2023, the Company employed approximately 1,890 full-time employees, approximately 28% of whom had at least ten years of service with the Company. Source: 10-k

Source: Ycharts

Sturm, Ruger & Co reported a decrease in the number of firearm orders received in 2022 as compared to 2021 and 2020. Management explained the decrease with the following words.

The estimated sell-through of the Company’s products from the independent distributors to retailers in 2022 decreased 25% from 2021. These decreases are attributable to decreased consumer demand for firearms from the unprecedented levels of the surge that began in 2020 and remained for most of 2021. Source: 10-k

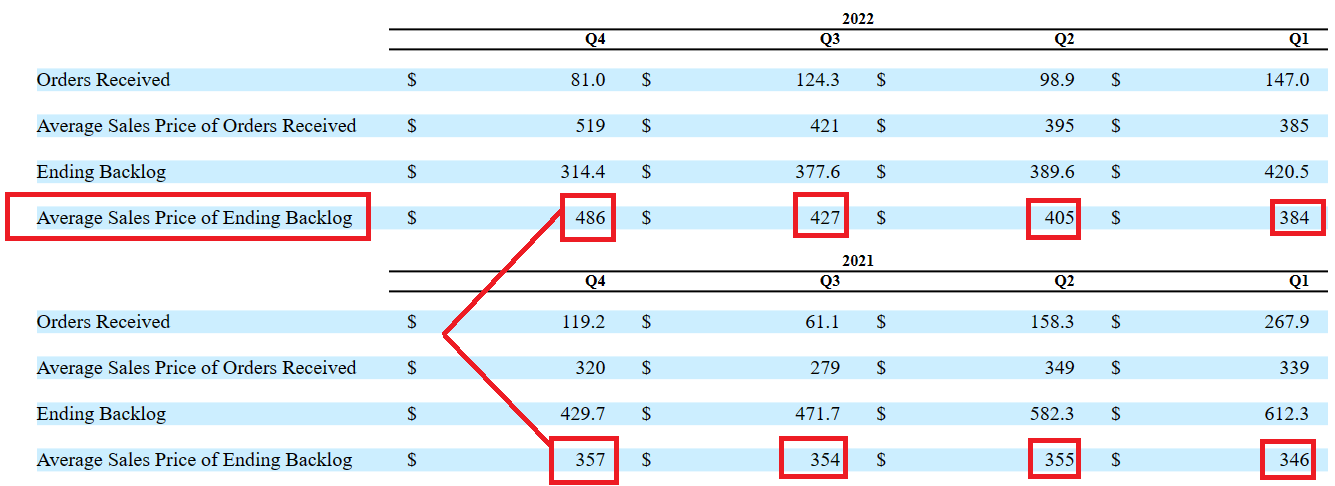

With that, the average sales price of the ending backlog increased, which I believe is quite appealing. Under my discounted cash flow model, I assumed that considering the know-how accumulated by Sturm, Ruger & Co and the consolidated brand, future orders will most likely trend higher as marketing efforts increase too. If the average sales price continues to trend higher, net sales growth will most likely remain elevated.

{kind=link}

Source: 10-k

It is also worth noting that we can expect innovation coming from the expenditures in research and development, which stood at close to $9.6 million, $8 million and $11.7 million in 2022, 2021, and 2020 respectively. With around 57 employees only dedicated to R&D and many years in the industry, we can expect new successful models in the coming years. As a result, I believe that we can forecast net sales growth and FCF margin expansion.

In 2022, 2021, and 2020, the Company spent approximately $9.6 million, $11.7 million, and $8.0 million, respectively, on research and development activities relating to new products and the improvement of existing products. Research and development expenses are included in costs of products sold. As of February 1, 2023, the Company had approximately 57 employees whose primary responsibilities were research and development activities.

Sturm, Ruger & Co maintained an active acquisition strategy in recent years that allowed it to complete the purchase of assets from Marlin Firearms, the brand through which it currently markets its line of lever action rifle products.

Source: 10-k

The company paid close to $28 million for the assets of Marlin Firearms. The target was private, but I could find that Marlin Firearms reported around $150 million in revenue in the past. Considering the price paid for the assets, I believe that the market would most likely celebrate new acquisitions like that of Marlin Firearms.

Source: zippia.com

I also assumed that the company will successfully work a bit more with other independent dealers and distributors, which market participants would most likely appreciate. The company mentioned that it is mainly working with some of them, but the company appears to have connections with many other distributors.

The Company has 15 independent distributors that service the domestic commercial market. Additionally, the Company has 45 and 25 distributors servicing the export and law enforcement markets, respectively. Source: 10-Q

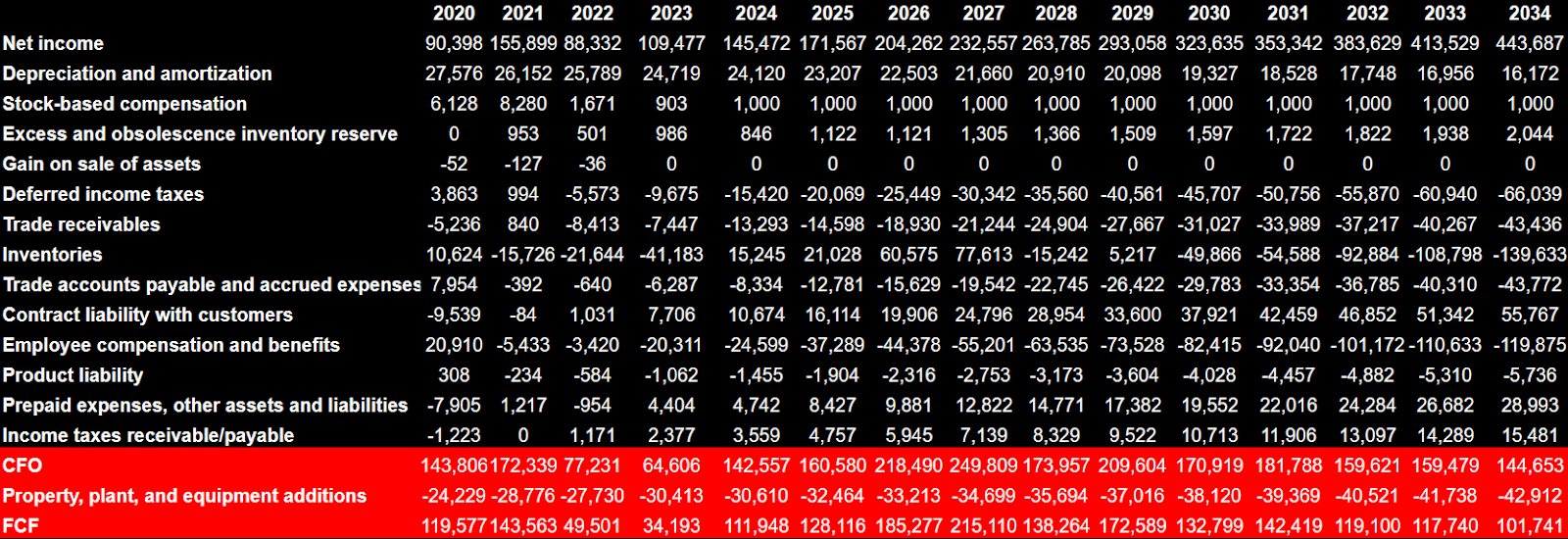

My discounted cash flow model resulted in a 2034 net income close to $443 million, D&A of $16 million, excess and obsolescence inventory reserve worth $2 million, and deferred income taxes close to -$67 million.

I also included changes in trade receivables worth -$44 million, changes in inventories of -$140 million, and changes in trade accounts payable and accrued expenses worth -$44 million.

Besides, I assumed future changes in contract liability with customers close to $55 million and changes in employee compensation and benefits of -$120 million, which implied 2034 cash flow from operations of $144 million. If we also subtract 2034 property, plant, and equipment close to $43 million, the implied 2034 FCF would be $101 million.

{kind=link}

Source: Financial Model

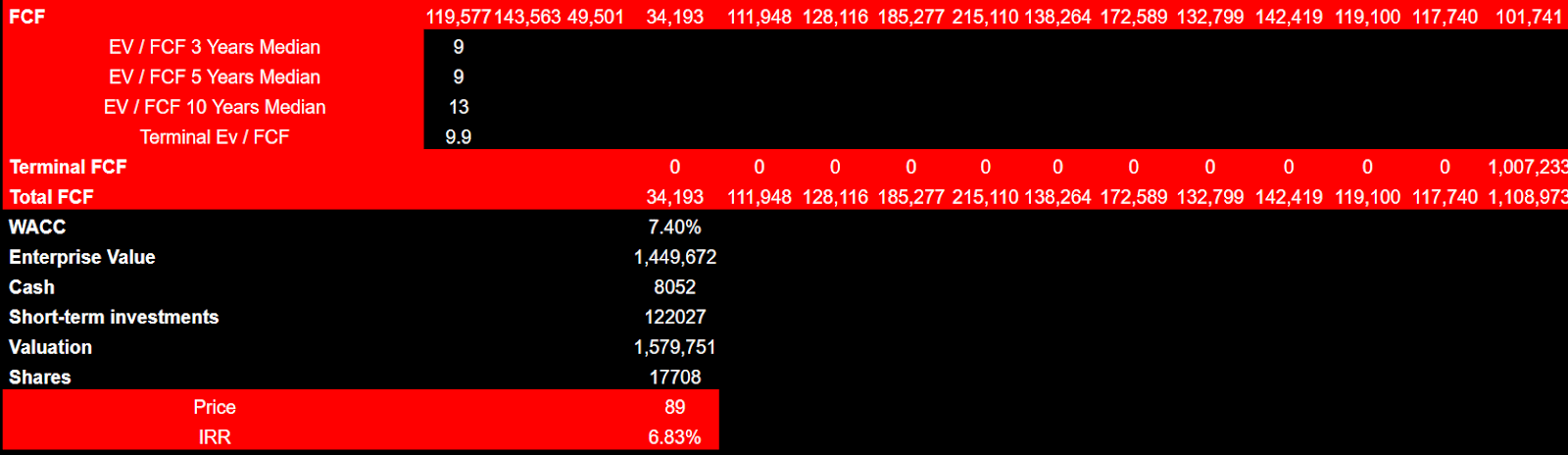

Considering that the EV/FCF 3 years median, EV/ FCF 5 years median, and EV/FCF 10 years median stand at about 9x-13x, I assumed terminal EV/FCF close to 9.9x, which I believe is reasonable and conservative.

Source: Ycharts

Also, with a WACC of 7.4%, the enterprise value would stand at $1.449 billion. If we add cash worth $8 million and short-term investments of about $122 million, the implied valuation would be $1.579 billion. Finally, the implied fair price would be close to $89.21 per share.

{kind=link}

Source: Ycharts

Competitors

The market is highly populated by local as well as foreign producers. Some of these offer products in a single line, such as rifles or pistols, while others, like Sturm, Ruger & Co, work in several product lines. Technological innovation in production capacities is a great differential within this industry, and this point is relevant above all in the ammunition segment. In this last segment, the competition is given by companies with greater resources, knowledge, and prestige, while in the sale of arms, the position of the company is within the average parameters of the market.

Risks

One of the biggest risks for this company due to the nature of the business involves possible changes in relation to the laws of trade and use of firearms. At present, a large part of American society has questioned the legality of this activity due to the large number of tragic events and mass shootings. The state jurisprudence in the country allows each state to have its own laws. In this sense, the commercial activity can be affected according to the geographical concentration.

In addition, as pointed out before, 90% of company’s sales are made to 15 federal distributors, and the company totally depends on these distributors representing its concentration, which is also part of the logic of this market. Ultimately, another of the current risks for the company is the management of the acquisition of Marlin and the integration of this brand into its business infrastructure.

So far, I believe that management successfully increased the price of firearms, which helped the company to fight the effects produced by inflation and increases in the price of raw materials. With that, I think that the company, in the future, may suffer from lack of components, certain raw materials, or inflation, which may lead to lower FCF margins.

Conclusion

Sturm, Ruger & Company recently delivered an increase in the average sales price of the ending backlog, which may have a positive effect in the coming quarters. Besides, further headcount growth, continued research and development expenses to support new innovative products, and more opportunistic acquisition of business or assets could happen. Under these conditions and taking into account risk from inflation or lack of raw materials, I believe that Sturm, Ruger & Company could trade higher.

For further details see:

Sturm, Ruger: Delivered Increase In Sales Price, And Headcount Growth Could Enhance Stock Price