ACGYF - Subsea 7: Don't Forget About Debt

2023-09-08 01:51:14 ET

Summary

- Subsea 7 is seeing progress on deliveries and, therefore, revenue, but also backlog coming from order intake.

- End markets are strategic and strong.

- The issue is Subsea 7 doesn't have super cash generative economics, and this means they carry more debt than other companies.

- Finance costs are a mounting and enduring problem and are the reason we are staying away from this cyclical play.

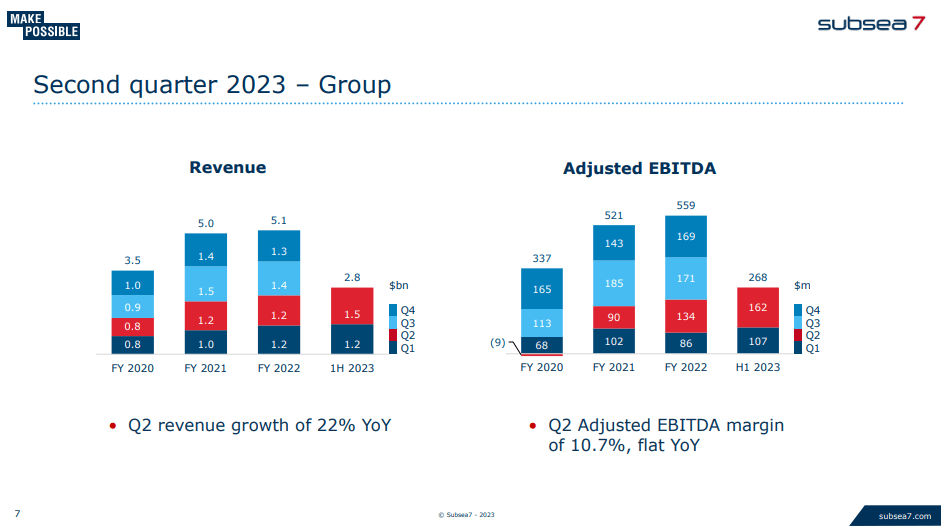

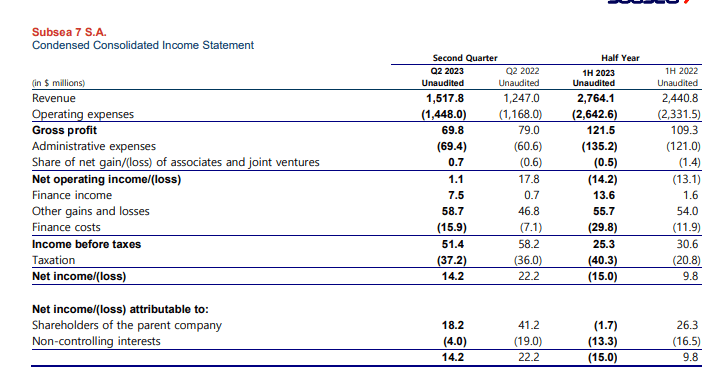

Subsea 7 (SUBCY)(ACGYF) is an EPC company that does various work related to oil rig infrastructure. We've been covering it for a while, and the situation continues to look good on the operating side. Backlogs are growing, deliveries are proceeding, and margin - for various reasons - is improving at the operating level. The issue is on the financial side of things, and it's a stark reminder of what is to come for the typical company in this economy of higher rates. Debt costs are making issues for the net income, and it's a problem for valuation considering risks.

Q2 Breakdown

Major projects continue to proceed into later stages, Sangomar being a good example of a pretty major project that is coming a long way, and this means that the margin on these major and older projects are tending upwards. EPC contracts, especially in the subsea industry, have higher margins at the tail end of the delivery.

{kind=link}

Backlog is also growing despite faster deliveries owing to the accelerating order intake. While this also means the initiation of newer projects which take a while to ramp up in margin, the baseline margin profile on newly originated projects are going to be higher thanks to pricing power due to the rush to develop energy assets and the fact that the inflation situation is now better mapped. There won't be any contracts that aren't inflation indexed at this point. As these mature, margins should expand even further.

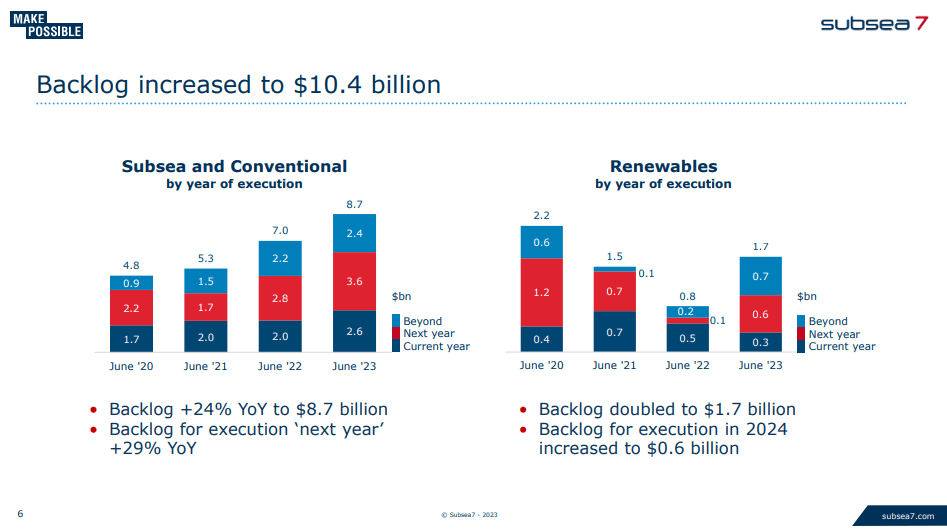

Backlog Subsea 7 (Q2 2023 Pres) Revenue (Q2 2023 Pres)

{kind=link}

{kind=link}

The renewable backlog was under pressure last year, but recent uptake in order intake recovered the backlog to healthier levels.

Bottom Line

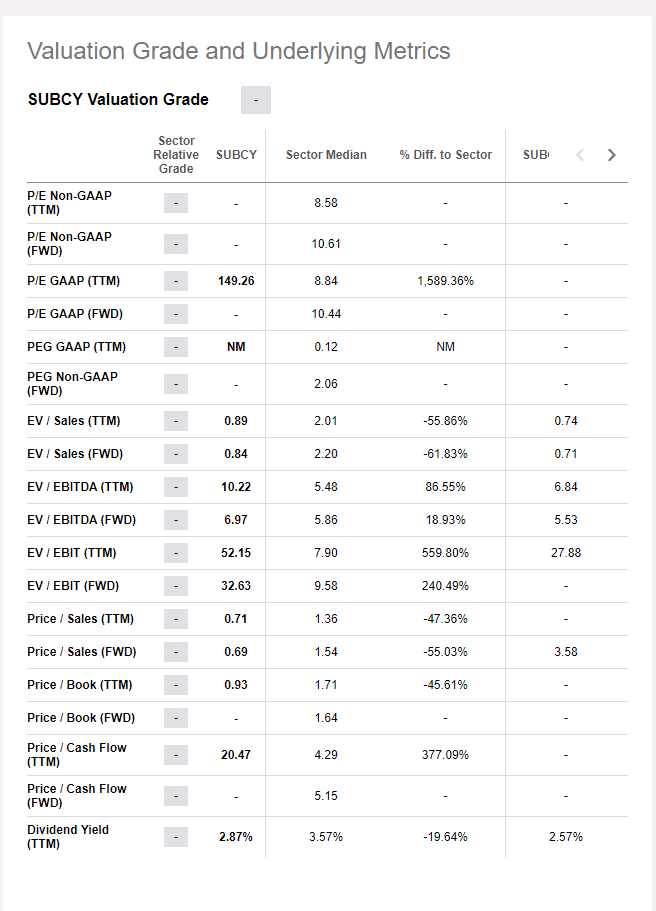

The valuation is pretty inexpensive for Subsea 7 when using above-the-line figures, and that's great.

SA Valuation Spread (Seeking Alpha)

{kind=link}

The problem is that the economics of Subsea 7 are not especially cash generative. The business is pretty working capital intensive as it doesn't receive that many advances on projects, and needs to put in a lot of legwork to actually hit project milestones. Things can get slow on the WC side if there are supply issues as well, which is something to look out for in general given that a lot of manufacturing will go back to China at some point. It's also aggressively fixed capital intensive, and they are doing a lot of the incremental investment for vessels in the renewable business . We do not like that at all, since we do not really believe in Subsea 7's renewable business, because it is exposed to offshore wind. We have had concerns over structural expenses in offshore wind, and with the performance of some key players recently, it looks like this won't be the solution people are hoping for. In general, we see it as negative when a company is CAPEXing for anything renewable related, as chasing the trend is expensive and risky.

The issue with the business not being particularly cash generative is that Subsea 7 has a lot of debt, and the debt load is growing. Net income is down around in the mid single digits even adding back expenses related to an impairment. It's coming from higher financing costs. This is a major issue for a lot of companies in the rate-hiking environment. Above the line metrics look fine, but ultimately cash does leave coffers to creditors. With new debt, finance costs will go up. When refinancing happens, it'll go up further. We have not yet seen the full effects for sure.

The situation is rates will likely endure due to underlying inflation from deglobalisation. The capital structure of Subsea 7 is not damning, but it isn't terribly safe considering the economics of Subsea 7 and the cyclicality of their markets. It's great while there's a rush again for oil assets to be developed, for both economic and strategic reasons, but looking further out than that you can imagine the potential dangers.

{kind=link}

With below the line multiples diverging meaningfully on very tightened net income, we are concerned about the ultimate value for shareholders, even in the face of an industry boom. Economics are slightly precarious. There are certain better deals on a quality/price basis in the cyclical space.

For further details see:

Subsea 7: Don't Forget About Debt