SUNL - Sunlight Financial: Challenging Times

Summary

- Sunlight Financial has withdrawn its full-year guidance following the disclosure of its most significant impairment charge yet.

- The book value discount has widened, but pending visibility into the risk across its loan book, it’s hard to underwrite a bull case here.

- A takeout scenario could be on the cards should Sunlight Financial's valuation dip further, but pending a full re-underwriting, investors might want to sit this one out for now.

Sunlight Financial Holdings Inc. ( SUNL ), a residential solar point-of-sale financing platform, recently withdrew its full-year guidance after recognizing significant impairment charges related to a cash-strapped installer. Of note, this announcement comes right after the company's Q2 missed on another $85m write-down (related to a failed lender merger). While management has claimed that the latest impairment is isolated to this particular installer, there is a worrying pattern emerging on the credit front, which, coupled with the ongoing Fed rate hikes, could see loan production significantly impacted in the coming months.

Still, SUNL has some redeeming features, including its relatively low California exposure, which insulates it from the pending Net Energy Metering Scheme ((NEM)) 3.0 changes . Its growing direct loan business with depositary institutions should also help with the interest rate impact, although any offset is likely to be limited for now. All in all, I would hold off on SUNL stock on platform fee revenue headwinds due to the current interest rate environment, as well as future production losses as more installers come under pressure in the coming months.

Solar Installer Bankruptcy Drives Major Impairment Charge

SUNL’s announced $30-33m non-cash impairment charge (~$0.25/share or ~10% of the pre-announcement equity value) on advances made to an installer facing liquidity challenges came as a negative surprise. More worryingly, this was a major supplier as well – the charge represents >30% of total advances to tier 3/medium risk suppliers based on SUNL’s latest 10-Q filing .

The read-through is unclear at this point, but given the size of this installer, bank credit was likely involved, potentially driving contagion risks down the line. While management reassured that this is an installer-specific issue, this incident does come on the heels of an increase in loan loss provisions for a single contractor in the prior quarter as well as an ~$85m write-down in direct channel-funded loans related to a failed lender merger. For now, the prudent measure would be to write off the advance, even if a recovery remains possible, should SUNL achieve a settlement with the installer or if the installer’s customers are offloaded to a peer under the SUNL umbrella.

Negative Implications for the Guidance

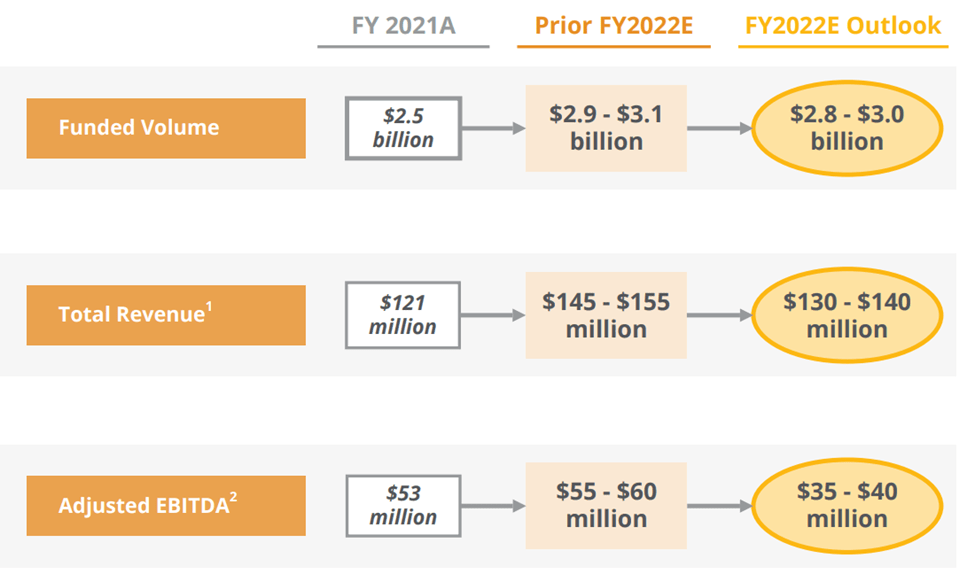

Adding to the uncertainty, SUNL has withdrawn its prior FY22 outlook, citing the installer liquidity event and interest rate volatility. Of note, this comes on the heels of a prior full-year guidance reduction – recall that in Q2 2022, funded volume was revised to $2.8-$3.0bn (down from $2.9-$3.1bn), total revenue to $130-$140m (down from $145-$155m prior), and adj EBITDA to $35-$40m (down from $55-$60m).

{kind=link}

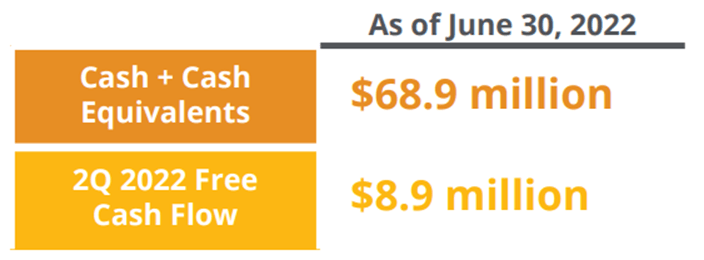

So, even though management views this as an idiosyncratic installer event, more downward revisions are very likely on the cards from here. Expect loan production to see the largest impact, driving near-term platform fee pressure and a deterioration in the P&L. I suspect SUNL could post more loss provisions as well should the macro deteriorate, although the next largest partner advances are much smaller at <$10m. In the meantime, SUNL has >$60m of cash on the balance sheet, which may or may not be an adequate cash buffer depending on the outcome of its re-underwriting process.

{kind=link}

Still an Outside Chance of a Takeout

While I am cautious about SUNL’s prospects, the company does operate in an attractive space (residential solar financing) with secular tailwinds. Thus, the upside here is that a potential buyer emerges should the stock get too cheap. On the one hand, the higher end of the SUNL loan portfolio could be appealing to a bank/depositary institution with access to lower-cost deposit funding. Solar manufacturers could also view SUNL as an inexpensive way of building out a captive financing unit, particularly at the current >80% book value discount (or an ~57% discount on tangible book).

{kind=link}

In the meantime, the pending Inflation Reduction Act and the multi-year extension of the solar investment tax credit offer volume upside to the current guidance numbers. On the flip side, any upside needs to be weighed against the prospect of an economic recession in the coming months, and pending clarity into the state of the SUNL book, potential buyers might adopt a "wait-and-see" approach. The recently authorized ~$50m buyback program (as of August 2022, SUNL has repurchased ~$5.6m) is a positive but will likely prove insufficient to support the stock ahead of a challenging next few months.

Challenging Times

SUNL’s latest impairment disclosure does not bode well for the near-term outlook. While management contends that this is an isolated event, profitability could come under increased pressure amid lower loan production and the prospect of more bankruptcies (and loss provisions) over the coming months.

To be clear, the long-term SUNL story of facilitating loans in high-growth markets (solar and home improvement) presents an extensive runway. Yet, the company will have to navigate the near-term turbulence from higher rates and a potential global recession. Both events not only imply a higher return hurdle for its bank partners but also weaker loan origination as SUNL is forced to increase pricing to consumers. The stock has de-rated significantly in recent weeks, but given the challenges across the value chain and the business execution risk ahead, the risk/reward remains unfavorable.

For further details see:

Sunlight Financial: Challenging Times