MONRY - Surprise Second Request Threatening Tapestry's Acquisition Of Capri

2023-11-07 13:59:39 ET

Summary

- Tapestry's acquisition of Capri Holdings is subject to a second request by the FTC, raising potential antitrust concerns.

- The merger would create the fourth-largest luxury goods firm with a market share of 5.1%.

- The FTC may focus on MRP mechanics or other practices the companies utilize to protect their luxury status.

- These issues are relatively minor and should be able to get resolved by the parties if they are considered to be present.

Yesterday we learned that the Tapestry ( TPR ) acquisition of Capri Holdings ( CPRI ) is subject to a second request by the Federal Trade Commission. In my last article , I noted that HSR should have expired, but since that wasn't announced, there could be an antitrust issue. I'm still of the opinion complying with the second request by the FTC and perhaps a symbolic gesture to mitigate concern will likely satisfy the agency. I don't see the antitrust issue here. Although it's a horizontal merger, it's also a very fragmented market.

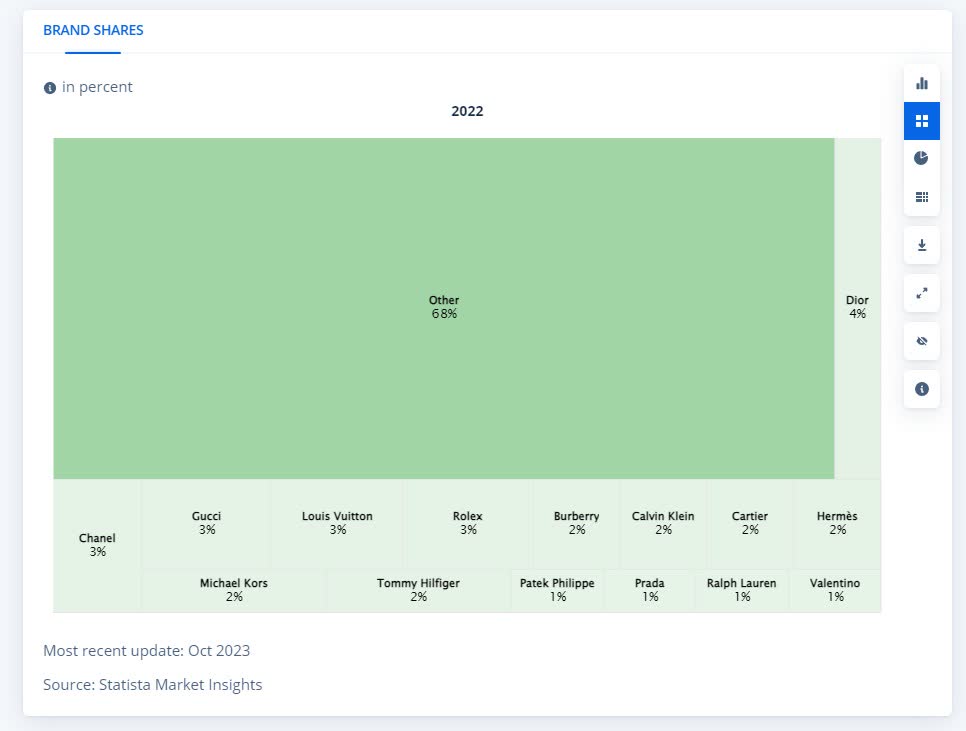

Commonly, regulators use the Hirfindahl-Hirschman Index as an objective measure of how a merger impacts the competitive landscape. If the HHI value goes over 2500, that's pointing toward a highly concentrated market. Here, two relatively small firms are merging. Yet, together, the combination will be the fourth-largest luxury goods firm with an estimated market share of 5.1%.

The HHI index adds up the squared market shares of players within an industry. Let's assume, for simplicity's sake, the independent market shares were 2% and 3%, and the new market share is 5%. Under the previous scenario, the firm added 4 + 9 = 13 points to the HHI. The new firm will be worth 25 points under the HHI. We're talking about an increase of roughly 12 points here.

Another test regulators sometimes use is whether there are at least four firms. Luxury is a much smaller market than premium so I've focused there. LVMH (LVMH) is the big one, with a market share of 22% in luxury. It was forced to acquire Tiffany's ( TIF ) in 2020-2021. Then there's Kering ( OTCPK:PPRUF ), Burberry ( OTCPK:BURBY ), Prada ( OTCPK:PRDSY ), Dior ( OTCPK:CHDRF ), Richemont ( OTCPK:CFRHF ), Moncler ( OTCPK:MONRF ), and many other smaller companies. Of course, there also are the companies themselves. I've left out sunglasses, jewelry, cars, and watch-focused companies like Chow Tai Fook, Ferrari ( RACE ) or the Swatch Group ( OTCPK:SWGAY ). I've also left out all premium brands. If you argue the combined firm competes in luxury in a court (and I think that's hard to argue for the majority of its revenue), then you would have to let in jewelry producers as well OR leave out Jimmy Shoo's revenue, for example. To make things worse, the largest luxury companies own many different luxury brands (often making different goods from watches to hotels champagne houses and they even do pastries ).

{kind=link}

If you could establish that the combination makes the HHI index go up too much, it's relatively easy to solve by selling a brand.

If you ask me luxury houses will sell anything with a perceived aesthetic (that's beyond my ability to pinpoint) and then square the price tag. The latter is part of the experience or product. Which is my final point on this antitrust issue - what are you going to protect the luxury consumer against? High prices?

There's one issue I can see the FTC take up. Some brands within this combination eroded some of their value by discounting too much and selling too widely. This tends to hurt the exclusive image required to compete in luxury.

The most recent Tapestry earnings call is riddled with references to increasing Average Unit Retail or AUR prices. The company is basically telling analysts we're keeping prices high to protect/strengthen our brands even though that's hurting revenue. One particular illustrative example is the following answer (emphasis mine):

Yes. Thanks for your question, Mark. We did drive handbag AUR increases at Kate ( PH ) in North America . So it was not mix benefited and it's based on deliberate strategies. We are not chasing every last dollar of top line in our business. We're protecting brand health and we see a lot of runway ahead at Kate, both top line growth and in margin and AUR growth. They're a little bit earlier on the journey, although now we've got two years of consistent AUR increases under our belt.

So we feel good about our ability to continue to drive AUR increases based on brand positioning. And that's the result of - our disciplined operations are leveraging our platform with data and analytics and applying that to the business, but also driving innovation. And we're incredibly focused at Kate Spade at driving innovation...

What fashion houses sometimes do is require resellers to apply minimum resale prices. This could be included in what's referred to in the above example as "our disciplined operations." Another good example is the following:

Now touching on revenue by channel for the quarter. Our direct-to-consumer business grew 2%, fueled by a low-single digit gain in stores. And in wholesale, revenue was 5% below the prior year, reflecting growth in international markets, offset by a decline in North America, which included a strategic reduction in off-price shipments as well as overall wholesale market pressure.

Antitrust consultant Darrell Prescott has extensive and educational writings on antitrust in the fashion industry, available on his blog . To quote him:

In an effort to better control their brands and images, many fashion and luxury goods makers wish to implement price controls to restrict the prices at which retailers may sell their products. These controls often take the form of a suggested retail price policy or a required minimum price policy. The law on these restrictions has evolved significantly over time and become more permissive. However, because the law in this area is still relatively unsettled, companies do expose themselves to the risk of antitrust liability when they implement such programs, especially in certain states in the U.S., or at the federal level if the resale pricing policy is part of a horizontal price restraint among competitors.

My non-lawyer read is that it will still be very hard for the FTC to win in court on such an issue. However, the companies probably prefer not to end up in court, and it could offer the FTC some leverage against the merging companies. Probably not to try and stop the merger altogether but perhaps to squeeze them to make some concessions. For example, to drop RPMs. The companies could work around that by using minimum advertising prices instead or finding another creative and lawful solution.

Ultimately, all of the above is speculation because we don't know what the FTC sees or expects to find here that drove it to issue a second request. The request isn't transparently motivated like it is in Europe. It remains hard for me to see this as an anticompetitive deal. Perhaps there are business practices that need amending. I will be surprised if the second request results in a suit. I will be even more surprised if arising issues from the second request can't be cured by the merging parties. What slightly worries me is that the merger can get delayed and we end up in a recession and Tapestry's resolve to get this done may waver. On the Aug. 17 call the company was still very confident it would get done:

Before turning to our go-forward expectations, I want to touch on the recent exciting announcement outlining the planned acquisition of Capri Holdings. This acquisition positions us to create significant value for shareholders with immediate accretion to adjusted earnings, enhanced cash flow and strong financial returns. While our current focus remains on the existing business, we've hired Ernst & Young to lead our integration efforts alongside a dedicated internal team ahead of the estimated transaction close in calendar 2024.

There's now a 14.9% upside to the deal closing as planned. This could still happen within the next three months. The merger doc did anticipate possible challenges as the outside date is as far out as Aug. 10, 2024, and that's before two extensions of six months total. If the deal fails, Capri likely falls back somewhere in the $30 to $38 range or a 20% - 40% loss. Even if it takes until August, the upside of 14.9% looks quite good. My baseline expectation is that it will still close in 2-3 months. The FTC could potentially find issues, but most likely ones that the companies could resolve. It's certainly not a deal without risk, especially because of the size of the target and acquirer, but I still think it's worth it to retain exposure after this setback. On Thursday both companies report and we'll likely learn more.

For further details see:

Surprise Second Request Threatening Tapestry's Acquisition Of Capri