SVOL - SVOL: Changes In Bond Holdings Are A Boon

2023-10-18 11:10:52 ET

Summary

- SVOL ETF has made major changes to its core bond holdings, shifting away from T-Bills and short-term corporate bond ETFs.

- The fund has increased its holdings in AGGH, LQD, and TIPS, indicating a change in strategy and macro outlook.

- The managers potentially expect reduced volatility, steady rates, and strength in corporate debt. The move to TIPS allows the managers to shift risks.

- The target 15% yield is difficult to maintain, but SVOL is positioned to continue achieving this level of income.

Introduction

The Simplify Volatility Premium ETF (SVOL) is an ETF that writes options against the VIX , the CBOE volatility index. This strategy has proved to provide a tremendous yield since its inception. Underlying the strategy is a core bond holding that the portfolio managers actively manage. Major changes to the core holdings give us insight into the expectations of the portfolio managers for the next quarter.

For those wanting a quick refresh from the SVOL prospectus :

Principal Investment Strategies : The Fund is an actively managed [ETF] that seeks daily investment results, before fees and expenses, that correspond to approximately one-fifth to three-tenths the inverse (-0.2x to -0.3x) of the performance of a short-term volatility futures index (the "Index") for a single day, not for any other period . In pursuing its investment objective, the Fund primarily purchases or sells futures contracts, call options, and put options on VIX futures. The Fund will hold cash, cash-like instruments or high-quality short term fixed income securities (collectively, "Collateral"). The Collateral may consist of (1) U.S. Government securities, such as bills, notes and bonds issued by the U.S. Treasury; (2) money market funds; (3) fixed income ETFs; and/or (4) corporate debt securities, such as commercial paper and other short-term unsecured promissory notes issued by companies that are rated investment grade or of comparable quality. The Fund seeks to engage in reverse repurchase agreements and use the proceeds for investment purposes. Reverse repurchase agreements are contracts in which a seller of securities, for example, U.S. government securities or other money market instruments, agrees to buy the securities back at a specified time and price. Reverse repurchase agreements are primarily used by the Fund as an indirect means of borrowing. The Fund also applies an option overlay strategy in seeking to mitigate against extreme volatility.

Over the last month, SVOL has made changes to its core bond holdings. Since August, the core position has been in T-Bills bought individually, iBonds purchased individually, and in short-term corporate bond ETFs, namely iShares iBonds Dec 2023 Term Corporate ETF (IBDO) and iShares iBonds Dec 2024 Term Corporate ETF (IBDP). These names are no longer held by the fund at all.

Instead, the fund shifted into Simplify Aggregate Bond ETF (AGGH), iShares iBoxx $ Investment Grade Corporate Bond ETF (LQD), and TIPS, namely this one , which is now 43% of AUM. These changes represent changes in the fund's strategy and the portfolio managers' macro outlook.

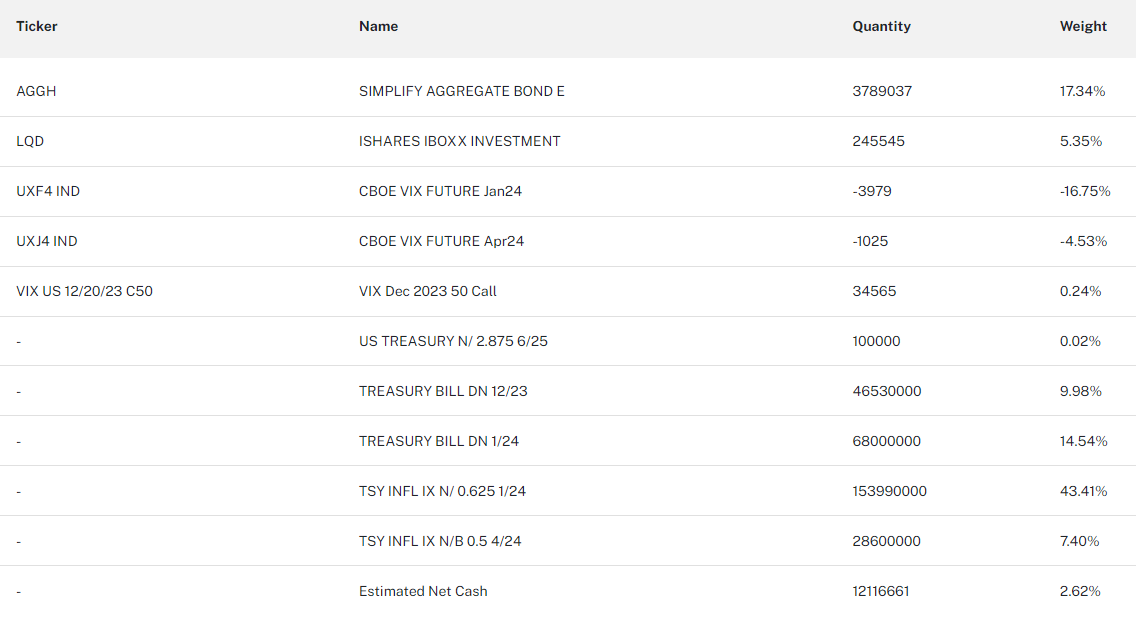

Current Holdings:

As of 10/17/23 (Simplify ETFs)

{kind=link}

T-Bills Need Not Apply

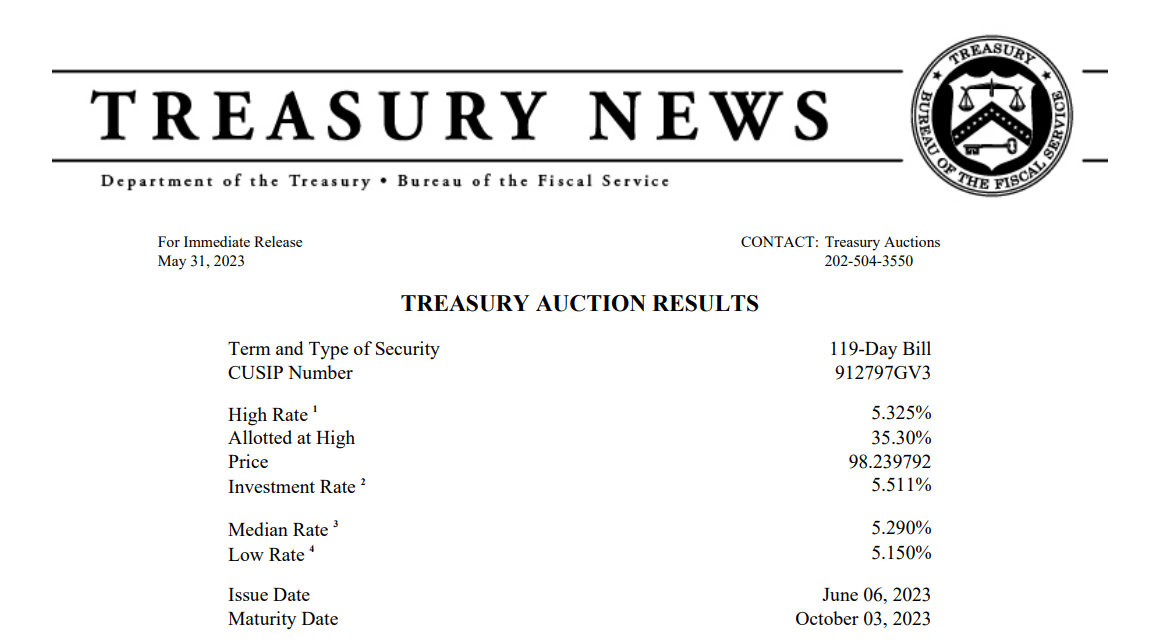

In June, SVOL bought June-to-October T-Bills as one of its largest holdings, 37% of assets. See the auction results below.

CUSIP 912797GV3 Auction Results (US Treasury)

{kind=link}

These T-Bills had a median rate of 5.29%. With a target yield of 15%, getting a third of the way there on T-Bills is fantastic. The rate on these bills has not changed much since then, with 0-3 month ETFs like ( SGOV ) offering yields of 5.31%. Similar four-month T-Bills are currently offering 5.64% .

In the US investing scene, these bills are considered "virtually riskless." With these yields at that little risk, and an uncertain future ahead in terms of rates, why not continue buying into the next round of T-Bills?

Instead, as this bill matured and the short-term corporate bond ETFs were sold off, SVOL added to three holdings: AGGH, LQD, and TIPS.

Simplify Aggregate Bond ETF ( AGGH )

This ETF needs its own article (one I intend to write soon, stay posted), but to summarize: Simplify actively manages this portfolio to have a similar risk profile to the US aggregate bond market while achieving significantly higher income via clever yield curve positioning, quant-driven option writing, and using treasury futures for leverage.

Here it is compared to its benchmark, the US Total Bond Market, which I use AGG to track. Below are the charts for: total return, yield, and risk.

While both funds lost since AGGH's inception, we can see some resilience where the options writing and other risk management tools have paid off.

The drastic rise in AGGH's yield also tells a story about the fund itself taking on more risk. AGGH's distribution rate is close to 11%, meaning future dividends may continue to climb. How much more risk do they have to take on for this kind of yield?

This is the interesting part. Using daily returns for standard deviation, we should expect to see almost three times as much risk taken on to compensate for the yield. Instead, we see less than double. To give some perspective, Long-term Treasuries ( TLT ) have an SD of 0.89%.

The move from T-Bills to AGGH clues us into a few things:

- Taking on more risk is acceptable in the bond holdings of the portfolio

- The volatility risk added by AGGH's options overlay isn't a concern, meaning they expect volatility to fall.

- This is not a perspective held by all Simplify managers, see the VIX options bet ( FIG ) made

- The portfolios managers are willing to double down on corporate bonds, as AGGH holds LQD and ( HYG ) as 10% of its own holdings

- More yield is needed, potentially to offset an expected loss in income from writing VIX options

iShares iBoxx $ Investment Grade Corporate Bond ETF ( LQD )

Corporate bonds are nothing new to SVOL's portfolio, but up until recently, they have been short-term bonds.

The biggest difference between the move from IBDO and IBDP to LQD is duration. The bonds held in LQD have maturities of at least three years, topping all the bonds held in the former funds.

Extending the duration of the holdings from 0.31 years to 8.04 years is dramatic. This gives the fund more exposure to interest rate changes, signalling that the portfolio managers expect rates to be leveling off and will be posing less of a threat moving forward. This is consistent with what the Fed has been saying .

This change in strategy signals:

- The portfolios managers are willing to take on some beta in the form of corporate bonds

- A top is being called at a 6% yield for A rated corporate bonds, at least for the next quarter, meaning there is little fear of rates rising

- With the most recent distributions coming in at a lower amount (shaving 6% off!), more yield may be needed to sustain future dividends

Recent Distributions (Simplify ETFs)

TIPS

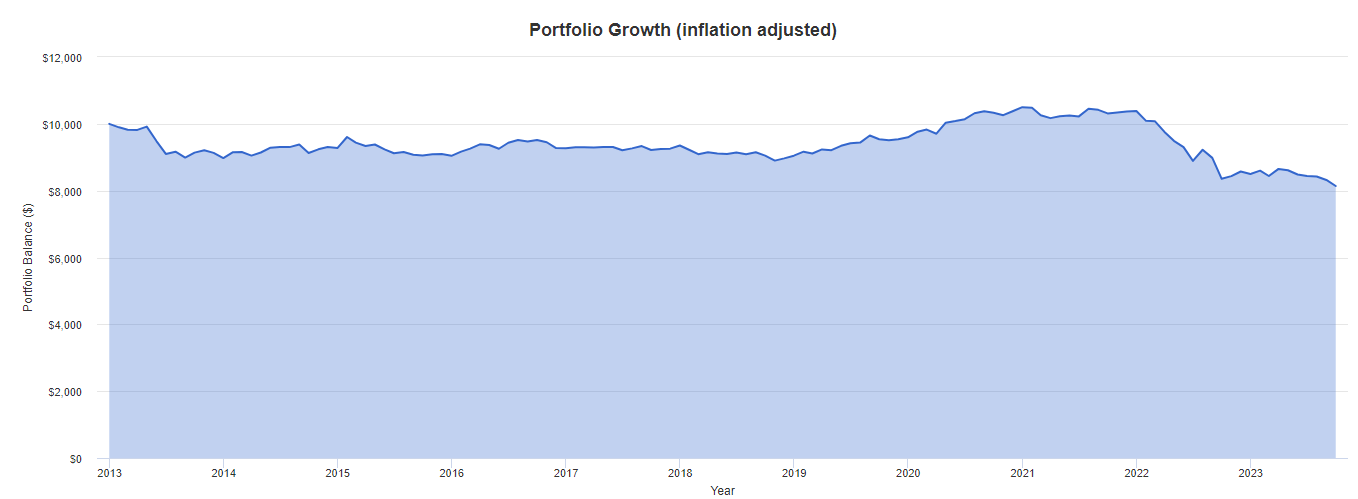

This change is very interesting to me, as half of the portfolio's holdings are now in TIPS. These, historically, have not fared well against inflation . Looking back to the last ten years, even with rolling reinvestment, the real-return of TIPS ETFs have been negative.

10Y TIPS Portfolio with DRIP (Portfolio Visualizer)

{kind=link}

How do we make sense of this bet? Looking at the chart above, we can see that TIPS have been particularly beaten down over the past year. The portfolios managers must see this pattern breaking.

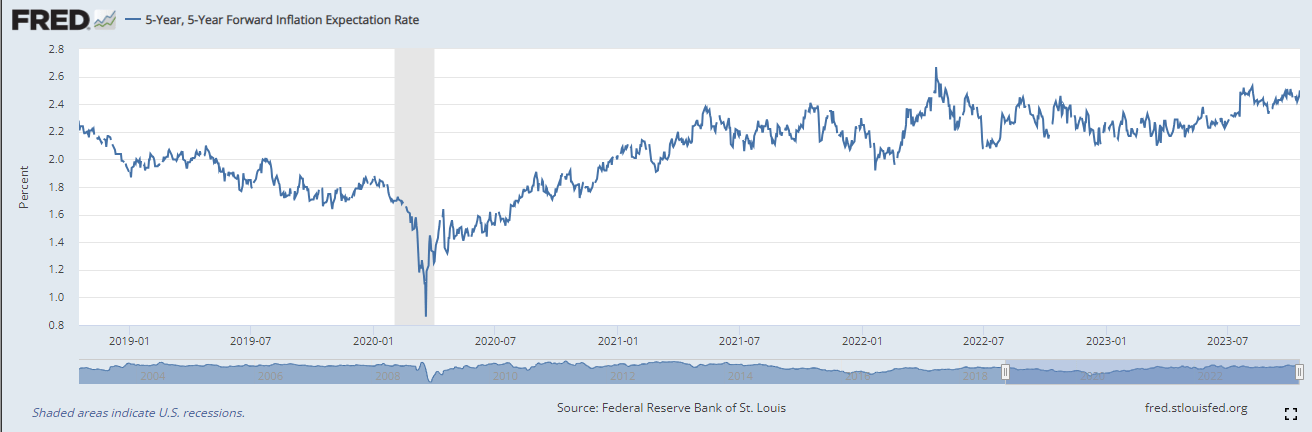

Assuming CPI projections are correct, these bonds are set to have some steady strength going forward.

5Y Inflation Rate Expectations (Federal Reserve Bank of St. Louis)

{kind=link}

With an expected positive real return, government backing, and a potential for price recovery if we see continued cooling inflation, it may make sense to take a lower current yield on these compared to T-Bills now for the benefit of being able to get positive real returns for a longer time.

This move shows us:

- The portfolios managers expect inflation to be persistent, again in line with the Fed

- There is a need for safety in real terms, at least from the largest core bond holding

- The increase in yield from AGGH and LQD allow for lower TIPS yields, shifting risk around in the portfolio

- This may be a short term play designed around capturing price appreciation in TIPS

VIX & Leverage Risks

The Simplify Volatility Premium ETF is a leveraged ETF providing -0.2 to -0.3x exposure to the VIX, reset daily. This means that there is risk of significant adverse moves in the VIX that could affect the fund.

SEC documents outline VIX Futures Risks :

VIX futures contracts can be highly volatile and the Fund may experience sudden and large losses when buying, selling or holding such instruments; you can lose all or a portion of your investment within a single day. Investments linked to equity market volatility, including VIX futures contracts, can be highly volatile and may experience sudden, large and unexpected losses. VIX futures contracts are unlike traditional futures contracts and are not based on a tradable reference asset. The Index is not directly investable, and the settlement price of a VIX futures contract is based on the calculation that determines the level of the VIX. As a result, the behaviour of a VIX futures contract may be different from a traditional futures contract whose settlement price is based on a specific tradable asset and may differ from an investor's expectations. The market for VIX futures contracts may fluctuate widely based on a variety of factors including changes in overall market movements, political and economic events and policies, wars, acts of terrorism, natural disasters (including disease, epidemics and pandemics), changes in interest rates or inflation rates. High volatility may have an adverse impact on the performance of the Fund. An investor in any of the Fund could potentially lose the full principal of his or her investment within a single day.

While this is not a fully leveraged fund that deals with value decay like ( SVIX ) or ( VIXY ), and SVOL has a positive expected return due to positive option convexity and a hedge against extreme VIX moves, there are still inherent risks.

Simplify explains better than I can, from the prospectus:

The option overlay is a strategic, persistent exposure meant to hedge against market moves and to add convexity to the Fund. If the market goes up, the Fund's returns may outperform the market because the adviser will sell or exercise the call options. If the market goes down, the Fund's returns may fall less than the market because the adviser will sell or exercise the put options. The adviser selects options based upon its evaluation of relative value based on cost, strike price (price that the option can be bought or sold by the option holder) and maturity (the last date the option contract is valid) and will exercise or close the options based on maturity or portfolio rebalancing requirements.

The Fund's returns are intended to possess convexity because the relationship between the Fund's returns and market returns is not designed to be linear. That is, if market returns go up and down in a linear fashion, the Fund's returns are expected to rise faster than the market in positive markets; while declining less than the market in negative markets. The value of the Fund's call options is expected to rise in proportion to the rise in value of the underlying assets, but the amount by which the Fund's options increase or decrease in value depends on how far the market has moved from the time the options position was initiated.

Investors need to be cautious about investing in any product they don't understand or are not prepared to take the associated risks with. While SVOL is on the safer side of these kinds of funds, since it is never more than 0.3x short and employs call options to hedge against black swan-like movements, we cannot deny these risks still exist and must be understood.

Conclusion

SVOL's managers have been busy shifting the core bond holdings around in the fund for the coming quarter. They shifted from short-term treasuries and short-term corporate bonds to their own in-house total bond solution, intermediate corporate bonds, and TIPS.

This change in holdings gives us insight into the managers' expectations, including reduced volatility, steady rates, and strength in corporate debt.

I welcome this change in strategy, though I am dubious of TIPS and would prefer SVOL to have those funds invested in short-term treasuries.

For further details see:

SVOL: Changes In Bond Holdings Are A Boon