SVOL - SVOL: Trends Reverse Reinstating My Buy Rating (Upgrade)

2024-01-03 15:51:29 ET

Summary

- Simplify Volatility Premium ETF receives a buy rating after addressing concerns regarding dividend distributions and underlying holdings changes.

- Return of capital distributions have ended, signaling a shift in strategy by portfolio managers.

- SVOL has reduced its holdings of CYA and added VIX call options, improving its position in the market.

- A $0.308 dividend for December may be hinting at a return to higher dividends above the recent $0.30 trend.

Introduction

Last month, I issued the Simplify Volatility Premium ETF ( SVOL ) a downgrade to "hold" due to trends regarding their distributions and underlying holdings changes.

These trends have reversed and in this column, I will explain why I am changing my outlook to a "buy" rating again.

If you're not caught up on this saga, you can find the last article, here .

My buy-and-hold ratings so far have held up and been fairly timely, although my coverage didn't start until the last few months.

Figure 1 (Seeking Alpha)

Overview

The Simplify Volatility Premium ETF ((SVOL)) is an ETF that is short the VIX, a gauge of volatility in the markets. Typically, SVOL is 0.2x-0.3x exposed to being short the VIX, but may end up with dynamic exposure day-to-day because of its positioning along the term structure. More on that later.

The fund primarily aims to trade in a tight range and issue monthly dividends. Be wary of this when you see return charts for SVOL.

Trend Reversal

Here were the primary issues I raised in November:

- Changes to dividend distributions to primarily include the return on capital distributions

- Inclusion of the Simplify Tail Risk Strategy ETF ( CYA ) instead of the more capital-efficient solution, VIX call options

- With a low VIX, the need to push further out on the curve could provide for reduced future yields

These issues have begun to be addressed by the portfolio managers, with the changes to distributions being entirely reverted to ordinary income. There is progress being made on the tail hedging and term structure placement as well.

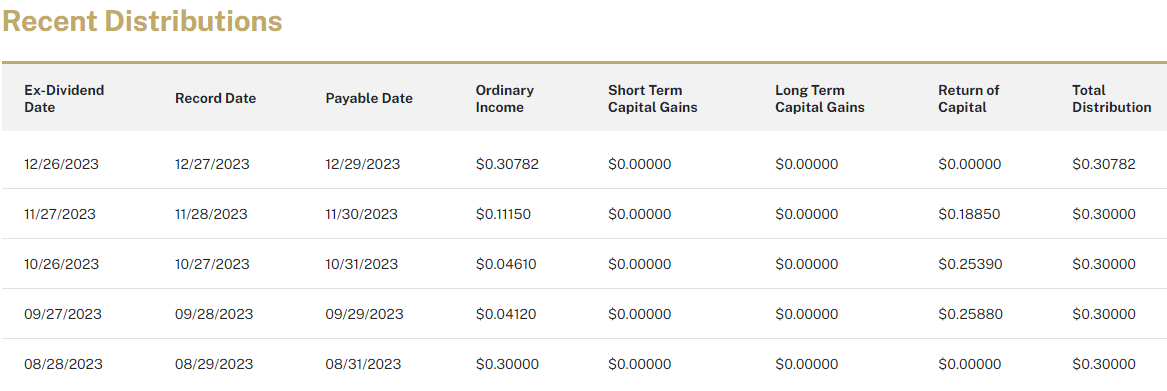

Changes in Dividends/Distributions

December's dividend was declared to be entirely ordinary income, indicating an end to the return of capital ("RoC") trend that has been ongoing since September.

{kind=link}

I am confident from seeing this that the return of capital distributions was a result of internal actions like rebalancing and was not a permanent shift in strategy done by the portfolio managers.

As a cherry on top, the distribution was almost $0.31 instead of the typical $0.30 that investors have gotten used to this year, down from $0.32 back in 2022 when the VIX was higher. I'll accept this token of goodwill from Simplify and hope it is signaling a return back to the $0.32 monthly distributions.

Reducing CYA, Adding VIX Calls

In November, I wrote :

The last time I covered SVOL, its only hedges against an adverse move in the VIX were far OTM VIX calls. The current strategy has incorporated one of Simplify's other funds, the Simplify Tail Risk Strategy ETF ( CYA) .

The more capital-efficient approach would be to increase the position in OTM VIX calls or create a ladder of calls to reduce some costs. SVOL could also employ the kind of call spreads used by CYA itself without needing to invest in CYA.

VIX call spreads are far more capital efficient to hedge adverse moves against the VIX than the hedges CYA employs because CYA includes equity hedges. These are not useful to SVOL's strategy, or at least not as useful as that same capital being used for more exposure to OTM VIX calls.

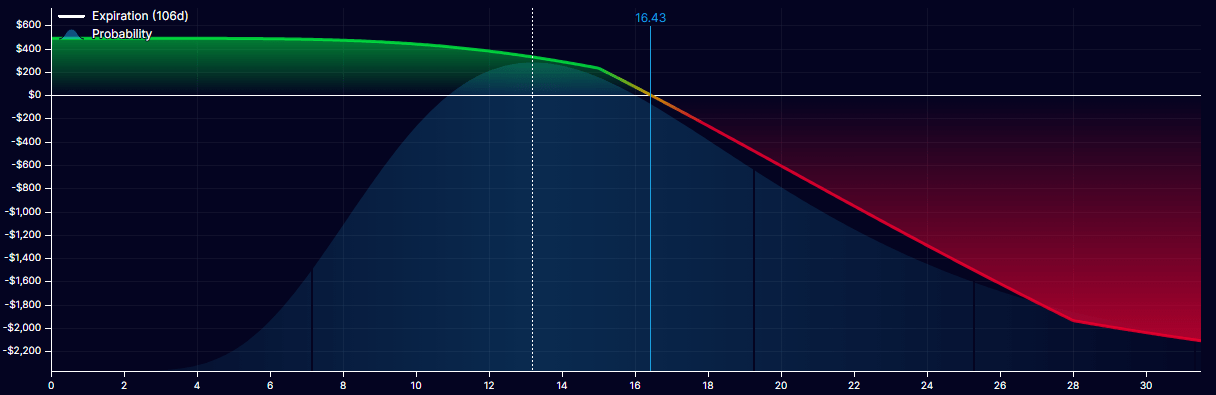

Compared to a traditional short-call payoff grid , adding in these hedges changes the slope and steepness of the downside, allowing for some hedging in a sudden crash. These OTM VIX calls do not have to complete spreads in line with the short futures but do need to have enough weighting to have a measurable impact during a crash.

{kind=link}

The people (or person, at least; I don't know if anyone other than me has been fist-shaking at Simplify for this) asked, and the people received: CYA's allocation has more than halved since that was posted.

I made a comment in one of my articles that I hope Simplify's portfolio managers read my column because I would absolutely love to take credit for this one. (They follow me here on Seeking Alpha, but the jury is still out.)

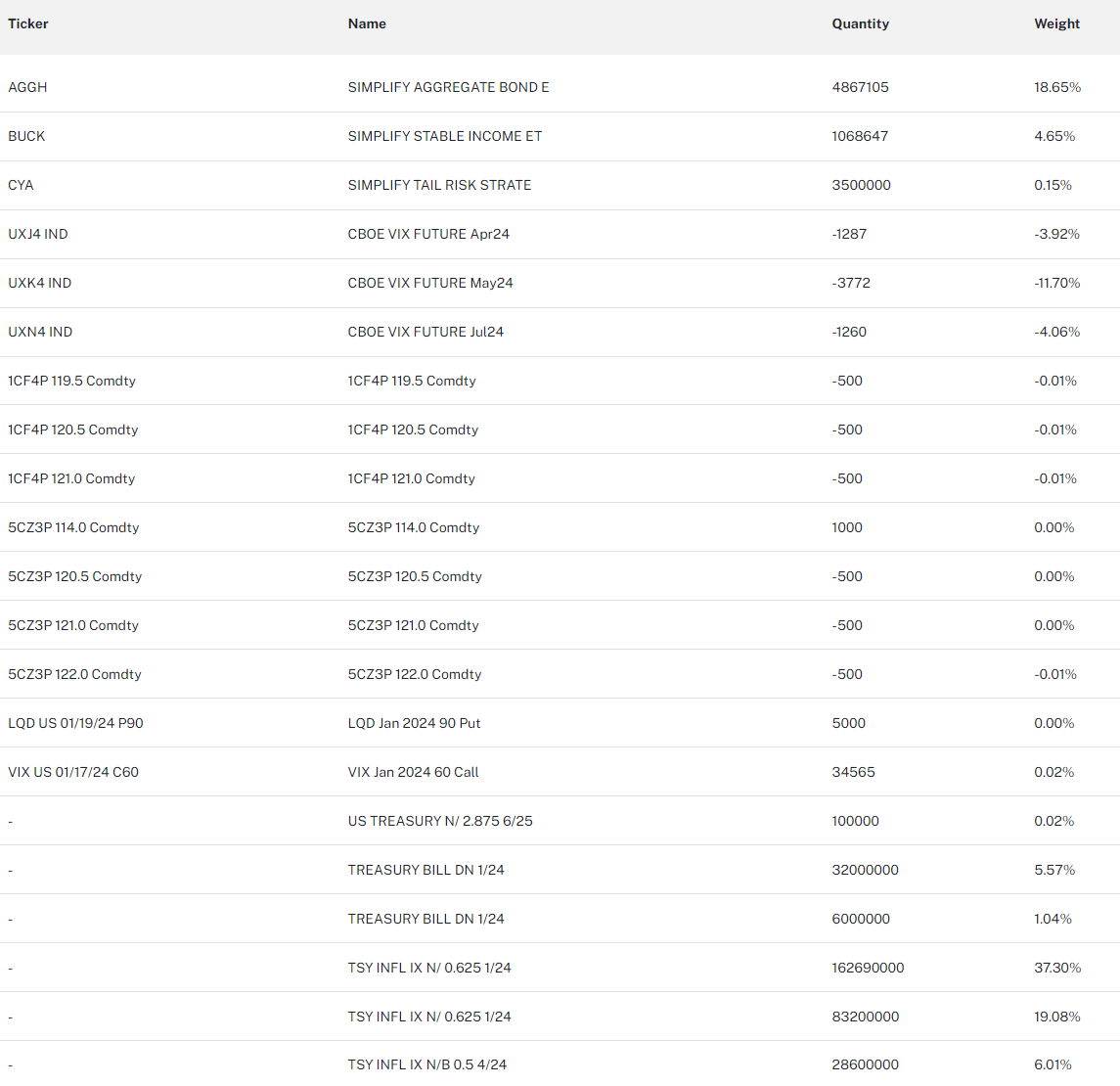

AGGH is also one of SVOL's incestuous holdings and SVOL's stake in AGGH is nearly 80% of AGGH's entire AUM. There's a lot of concerning inter-mingling going on under the hood, not just limited to CYA.

At the time my hold rating was published, SVOL's holdings of CYA represented about 0.36% of NAV. Today, that has dropped to 0.15%. Some of that has been moved into VIX call options, which you can see from today's holdings.

{kind=link}

While I'm still not entirely happy because I'm not a fan of the incestuous nature of Simplify's funds. SVOL still has a considerable position in AGGH, representing more than $106M of AGGH's $141M NAV.

That comes out to 75% of the NAV in AGGH coming from SVOL's holdings. However, that figure was even higher as of the last article, where it sat at 80%.

I do not like this kind of liquidity issue in my holdings, and this complaint remains somewhat unaddressed for now.

Rolling out to July

The keen-eyed may have spotted in Figure 5 above that we have a new position on the curve out in July.

{kind=link}

I agree with the portfolio managers that being further out on the curve is better for our current volatility environment than the front months. The position of the entire curve is too low to take on early expirations right now.

The VIX being so low does pose a risk to short volatility traders, but the portfolio managers are avoiding holding positions shorter than April to mitigate some of that risk.

SVOL would benefit immensely from a slow, grinding rise in the VIX, and would earn a strong buy rating from me in a better volatility environment.

Risks Still Linger

SVOL has yet to survive an event like a Volmageddon or March 2020 crash, since it didn't exist during these events. Because of this, it's unclear how the tail hedges SVOL employs will work in a real-world scenario.

The Simplify Volatility Premium ETF is a leveraged ETF providing -0.2 to -0.3x exposure to the VIX, reset daily. This means that there is a risk of significant adverse moves in the VIX that could affect the fund. SEC documents outline VIX Futures Risks :

VIX futures contracts can be highly volatile and the Fund may experience sudden and large losses when buying, selling or holding such instruments; you can lose all or a portion of your investment within a single day. Investments linked to equity market volatility, including VIX futures contracts, can be highly volatile and may experience sudden, large and unexpected losses. VIX futures contracts are unlike traditional futures contracts and are not based on a tradable reference asset. The Index is not directly investable, and the settlement price of a VIX futures contract is based on the calculation that determines the level of the VIX. As a result, the behavior of a VIX futures contract may be different from a traditional futures contract whose settlement price is based on a specific tradable asset and may differ from an investor's expectations. The market for VIX futures contracts may fluctuate widely based on a variety of factors including changes in overall market movements, political and economic events and policies, wars, acts of terrorism, natural disasters (including disease, epidemics and pandemics), changes in interest rates or inflation rates. High volatility may have an adverse impact on the performance of the Fund. An investor in any of the Funds could potentially lose the full principal of his or her investment within a single day.

While this is not a fully leveraged fund that deals with value decay like (SVIX) or (VIXY), and SVOL has a positive expected return due to positive option convexity and a hedge against extreme VIX moves (as discussed earlier), there are still inherent risks.

Simplify explains better than I can, from the prospectus :

The option overlay is a strategic, persistent exposure meant to hedge against market moves and to add convexity to the Fund. If the market goes up, the Fund's returns may outperform the market because the adviser will sell or exercise the call options. If the market goes down, the Fund's returns may fall less than the market because the adviser will sell or exercise the put options. The adviser selects options based upon its evaluation of relative value based on cost, strike price (price that the option can be bought or sold by the option holder) and maturity (the last date the option contract is valid) and will exercise or close the options based on maturity or portfolio rebalancing requirements.

The Fund's returns are intended to possess convexity because the relationship between the Fund's returns and market returns is not designed to be linear. That is, if market returns go up and down in a linear fashion, the Fund's returns are expected to rise faster than the market in positive markets; while declining less than the market in negative markets. The value of the Fund's call options is expected to rise in proportion to the rise in value of the underlying assets, but the amount by which the Fund's options increase or decrease in value depends on how far the market has moved from the time the options position was initiated.

Investors need to be cautious about investing in any product they don't understand or are not prepared to take the associated risks with. While SVOL is on the safer side of these kinds of funds, since it is never more than 0.3x short, we cannot deny these risks still exist and must be understood. Please be aware of them. Note that the lowered exposure to the VIX compared to traditional leveraged futures products sets SVOL apart from ((SVIX)), ( SVXY ), etc.

There are two major concerns that I will be watching moving forward, which could change my stance on SVOL:

- Further inclusion of higher-risk, higher-yield assets like AGGH and BUCK over the traditional TIPS and T-Bill holdings, which could indicate that the short VIX strategy cannot sustain the target 15% yield

- A return of the RoC distributions, which could indicate some "NAV cannibalism," which earned SVOL the downgrade in November

I will also re-evaluate the fund after the next two dividends to see if it is able to stabilize back at the $0.30 mark or, as mentioned earlier, return to the $0.32 dividend investors saw back in 2022. A return to this mark would earn SVOL an upgrade to a strong buy if the fund can show that the level of income is sustainable without returning capital to investors.

Expectations for Q1'24

If the VIX remains low, expect SVOL to continue to trade in a tight pattern, potentially even back down into the lower end of 21 like we did back in April, May, and October this year.

I believe the dividend will be sustainable, at least for $0.30, as we've seen with the strength in December's distribution. Expect consistency from SVOL unless we see a sudden rise in the VIX.

A steady grind might be very good for SVOL, as is evidenced by its 2022 performance.

That year left the VIX at an inflection point, one that it is still at now. Only time will tell, as it is almost always unclear what will spike the VIX until after it happens.

Conclusion

I am reinstating my buy rating for the Simplify Volatility Premium ETF ((SVOL)) because it addressed several of the concerns I raised in my previous downgrade article.

These changes were:

- Changes made to exclude return of capital from dividends, returning to ordinary income distributions.

- A cut back of the Simplify Tail Risk Strategy ETF ((CYA)) instead and inclusion of VIX call options.

- With a low VIX, the managers pushed out to the July expiration to avoid being caught short a sub-13 VIX.

SVOL continues to hold a place in my income portfolio, and with a current distribution yield of 15.88%, it's hard to not overweight it.

For now, I caution investors not to place more than 15% of an income portfolio in this asset, as it may be too risky in a VIX spike.

Currently, SVOL has a 10% allocation in my income portfolio, which I wrote about in more detail here .

I will be keeping an eye on future distributions for changes, as well as where the managers decide to roll out from here. By positioning in July, we are setting up for a sustained low VIX for the next few months. If this plays out, income should remain steady.

Thanks for reading.

For further details see:

SVOL: Trends Reverse, Reinstating My Buy Rating (Upgrade)