SWDBF - Swedbank: Looking For Yield (Rating Upgrade)

2023-11-16 07:13:00 ET

Summary

- Swedbank is in a decent position compared to its peers, but caution is advised for long-term investment.

- The bank's earnings forecast for this year and 2024 is strong, with a potential yield of around 8.7% based on the current share price.

- Swedbank's conservative strategy, cash flow, and solid costs make it an attractive investment option with potential upside.

Dear readers/followers,

Now it's time to update on Swedbank (SWDBF) as well as look at updating my stances on other Swedish banks, such as Handelsbanken (SVNLF). Swedbank is in a decent position, though not as good as its peers. I use the same strategy that I use on Handelsbanken when it comes to Swedbank - a substantial long added to by covered calls, and cash-secured PUTs when the price allows. This has enabled me to annualize about double digits between a superb overall yield, and some good options premiums - which unfortunately are no longer as easy to find now, 9 months later after the fact. My long-term stance on Swedbank is mixed - and I'll present to you why I'm cautious when it comes to adding and keeping shares for the long term.

However, Swedbank is a fairly sizeable position in my portfolio, and I am in no way "scared" or worried about where Swedbank is, or might be going.

The bank is still, despite the risks we can see in the company and with the thesis, far too central and important for that to be the case.

Let me illustrate this with 3Q22 and what we might expect for 2024. This is an update article, with my recent thesis found here.

Swedbank - Plenty of Yield from One of Sweden's Largest Banks

Despite forecasting a truly "epic" year in terms of earnings, Swedbank is being traded very "meh" here. One of my popular strategies for this company is to use my substantial holding of shares and when the company hits above 200 SEK, start selling conservatively and long-dated call options to add to my YoC of over 9.5% and make it around 11-12%. I've done this twice - then bought the options back at a substantial discount when the company is punished back to below 180.

Swedbank is estimated to bring in adjusted EPS of over 30.5 SEK this year. That's compared to an adjusted EPS of 11.51 back in 2020. Even the 2024E, despite a small decline, is still expected to bring in over 28 SEK per share on an adjusted basis. If this materializes, and given the company's dividend policy , a current likely YoC for this company is around 8.7% based on the current share price of about 181 SEK for the native.

Remember, Swedbank rarely "misses" its estimates. On a 10-year basis since GFC, the company beat estimates 25% of the time and missed only 8%, giving the company a 90%+ historical chance to either do better or meet its expectations with a 10-20% margin of error.

And then you take into account that we're in a rising interest rate environment.

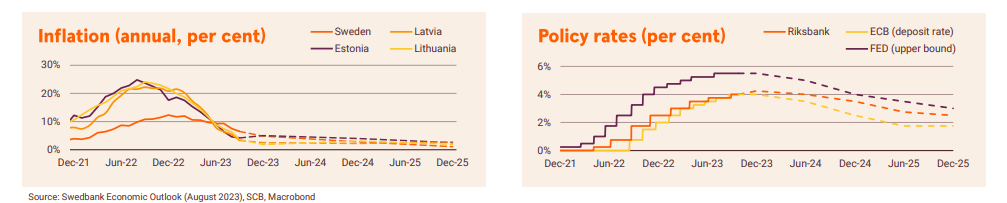

Swedbank is essentially a cash-printing machine in this sort of environment. While we can very clearly confirm the fact that the recovery is going to be a slow process, that inflation is high, and that we're likely to see high rates for a longer time period, this is not necessarily a negative for this bank - and it also doesn't mean that Swedbank isn't going to be performing well. Take a look at both inflation and policy rates as well as forecasts.

{kind=link}

I by the way still believe these targets to be well in excess of what I consider likely - in this case, I believe inflation to stay higher, and rates to stay higher as well. A policy rate below 4% is something I consider likely perhaps in 2026, but not in 2025.

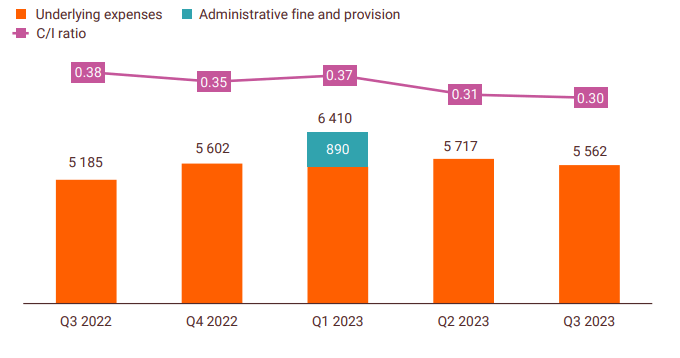

However, Swedbank continues printing cash. The company's income grew even sequentially to 18.4B SEK, with a net profit of 9.1B which marks an ROE of 19.3%, and a C/I of 0.3x. Show me 5 other banks that can do this, and you'll have a hard time doing so. The bank did record a number of credit impairments, but like other banks, the current focus is on a structural conservative strategy.

Lending volumes are up, but the company is more conservative with offering lending. Corporate is most of what was up - and the company saw a deposit decline of 1.7% as households are starting to drain savings to come to rights with the current pricing levels in society. However, NII continues to rise, with an NII of 12.9B, and net commission income was up as well, seeing an increase to 3.8B SEK. These latter results came from strong and stable card payment trends, asset management trends, and good performance from securities and corporate finance.

Despite inflation and increasing costs, Swedbank managed to lower its expenses. QoQ, it's down 2.7%, leading to a C/I at record levels.

{kind=link}

You can also see here how little impact an administrative fine has for the company, even if it's over 800M SEK. Swedbank remains one of the largest businesses in the sector here in the geography.

Credit impairments, to move to the negatives, are increasing. The company was impaired at almost 350M due to updated macro for casts and model adjustments. The company still has high property management exposure. It's in no way dangerous - the exposure comes at interest coverage ratios, or ICR's of 2.9x, which is down from 3.3x but still good, but as rates increase, so will risk here. It's now up at 7.8%, which is the highest the number has been in years.

Still, on a conservative perspective, Swedbank boasts a CET-1 of 18.7%. It's not the best in the world, not even the best in Scandinavia, but it's quite literally one of the best in Europe, only a few of its close peers are marginally better.

With a net profit of over 9B SEK for a single quarter, an RoE of over 19% and solid costs - and you can see what net interest income has done to this bank in as little as a year.

Swedbank IR (Swedbank IR)

This literally writes the story in what is going to be happening in the coming year when it comes to deciding the company's dividends. Also, Swedbank continues to have an over 650B SEK liquidity reserve, over 282B held in cash/balances at central banks, and around 55% in SEK with 40% in EUR and some 5% in USD. Swedbank boasts a liquidity coverage ratio of 159% and over-collateralization of 195%.

Swedbank Valuation - Houston, We have an Upside

Swedbank has a conservative upside here. If we consider that the bank is likely to see significant outperformance over the next few years, given NII trends.

Even if we forecast Swedbank at a very conservative 10x P/E multiple, this implies 2024E an annualized rate of return of 60% per year, and a share price of almost 290 SEK/share. I do not consider this type of share price likely - the company rarely manages it. But I do believe it could go higher.

When I write my calls, I typically write them at strikes of around 235-250 inclusive of premium, to ensure that I only sell at the prices I want to sell at. I want to remind you that Swedbank has a TEV of almost 1T SEK, and a credit rating of A+ - not many banks and financial institutions worldwide manage this sort of premium and upside.

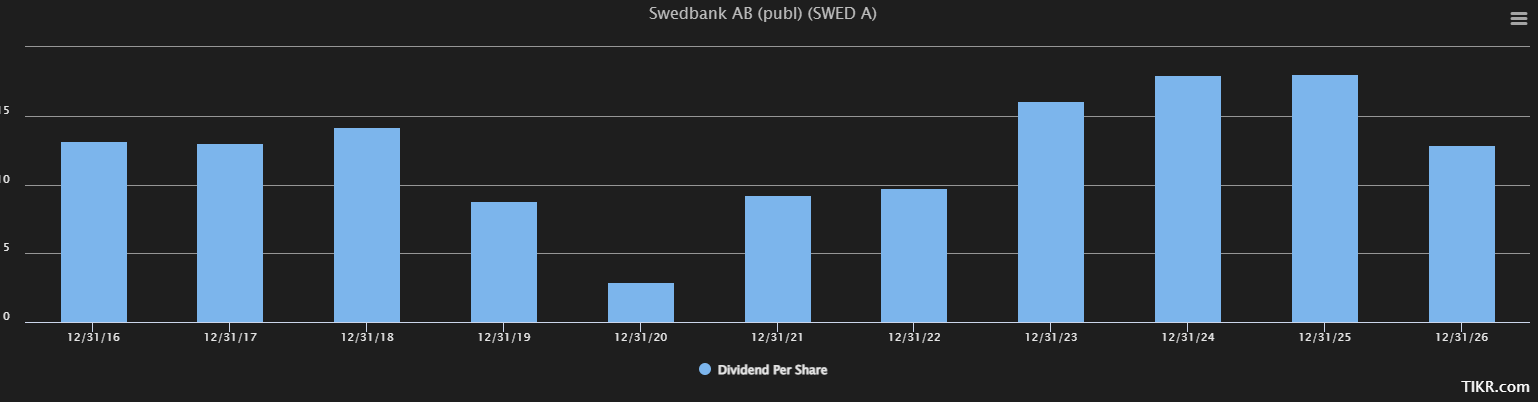

When taking into account the company's dividend policy meaning 50% of the company's earnings, you have forecasts for the dividend that call for 16 SEK next year, a top of 18 SEK in 2024 and 2025. If this materializes, then it could mean some very significant things for people such as me, who loaded up Swedbank at below 135 SEK/share.

Swedbank Dividend Forecasts (TIKR.com)

{kind=link}

And the thing is, this is almost a bit of a player piano. bank's income will continue to grow as the NII grows. And given the rate environment, this is not going to come down soon. I expect the dividends forecasted here to be close to the actual dividend payouts. My position, which is large despite everything, is already significantly in the green, and I expect to make a very good rate of return over the next few years.

Valuation targets confirm this. In less than 2 years, the average PT for Swedbank has changed from a mean of 145 SEK/share in 2020, to a mean of over 235 SEK/share as it currently stands. out of 19 analysts, 13 are at either "BUY" or outperform, and the lowest possible target from a following analyst from S&P Global is 185 SEK - which is also my current target.

I justify this target by saying that despite everything, this certainly isn't the "best" Nordic bank out there - but it's still a very solid one. Regardless of which of the incumbents you invest in, I believe a yield of 6-9% at a good price for each of them is a very likely scenario for the 2023 and the 2024 dividends.

Remember, I invest in a lot of finance - and what I try to do is buy them all at extremely cheap valuations. That's why I recently added to my positions in business like Lincoln National ( LNC ), Truist ( TFC ), and others, as well as Canadian and other European banks. I hold non-trivial positions in many institutions like these, and despite that some are still in the negative, I hold no worries about any of these investments and am of a high conviction that they'll reverse.

Here is my November 2023 thesis on Swedbank.

Thesis

- Swedbank isn't exactly massively overvalued here, but is it massively undervalued. The company can best be called decently attractive, especially when we consider what may happen to the underlying geography where Swedbank operates within the next couple of months or years.

- Given this potential pressure but also the potential advantages, I rate Swedbank conservatively and would "BUY" the company at this valuation - but only insofar as other alternatives are not attractive.

- I consider it time to raise my PT on Swedbank given what we're seeing here and what may happen I the coming year.

- I give Swedbank a target of 185 SEK here, which is above my previous one, and below the current share price for the bank. That means Swedbank is a "BUY", and I am updating my rating for the bank here.

Remember, I'm all about:

1. Buying undervalued - even if that undervaluation is slight, and not mind-numbingly massive - companies at a discount, allowing them to normalize over time and harvesting capital gains and dividends in the meantime.

2. If the company goes well beyond normalization and goes into overvaluation, I harvest gains and rotate my position into other undervalued stocks, repeating #1.

3. If the company doesn't go into overvaluation, but hovers within a fair value, or goes back down to undervaluation, I buy more as time allows.

4. I reinvest proceeds from dividends, savings from work, or other cash inflows as specified in #1.

Here are my criteria and how the company fulfills them (italicized).

- This company is overall qualitative.

- This company is fundamentally safe/conservative & well-run.

- This company pays a well-covered dividend.

- This company is currently cheap.

- This company has a realistic upside based on earnings growth or multiple expansions/reversions.

I will say that the company has an upside, but I will also say that the upside isn't as big as some of the others available here. It is, however, a risk I consider worth taking with the right expectations, which is why despite my not rating the company as cheap, I consider it to be a "BUY" here.

This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

For further details see:

Swedbank: Looking For Yield (Rating Upgrade)