KRUS - Sweetgreen: Positive Signs Of Traffic Recovery In SG Urban Areas

2023-09-06 03:48:11 ET

Summary

- I am positive on the business growth due to signs of recovery in urban traffic and the launch of the Sweetpass loyalty program.

- The launch of Sweetpass is expected to drive further traffic to SG's stores. This loyalty program offers discounts, which might impact SSS initially but is likely to increase overall foot.

- SG's infinite kitchen model, with increased production efficiency and reduced labor costs, is a potential growth driver with higher profit margins, positioning SG for long-term success.

Summary

Sweetgreen ( SG ) manages a chain of salad restaurants in the United States. Like many other casual restaurants, the growth strategy is to open more stores and grow same-store sales [SSS]. As of 2Q23, there were 205 Sweetgreen restaurants. This post is to provide my thoughts on the business and stock. I am recommending a buy rating for SG stock as I see visible signs of recovery for its urban traffic and believe that the launch of Sweet p ass should drive further traffic. I am also positive about SG’s infinite kitchen model , which should lead to a higher margin profile in the long term.

Investment thesis

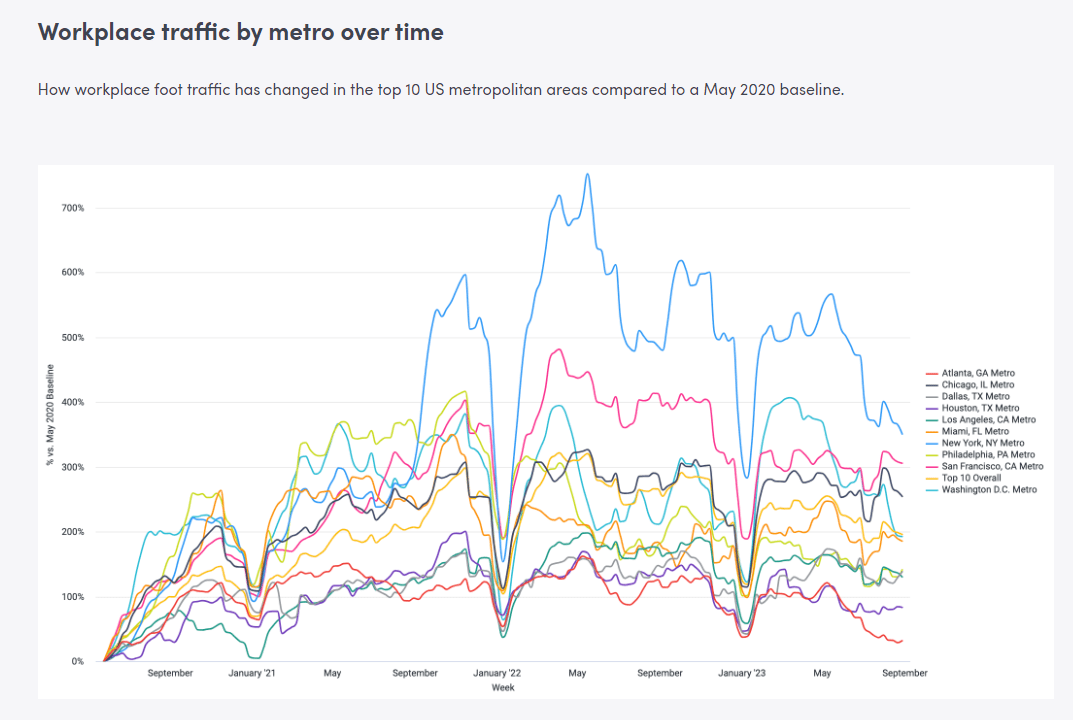

While SG has been a clear winner since March, in which the stock has risen by more than 100% (from $6 to $14), I don’t think the end of the rally is here yet. Reviewing the 2Q23 quarter earnings suggests that comp sales are still slow; however, I see that SG is on the right track to recovery. Firstly, urban SSS grew high single digits [HSD], and the good news here is that, based on Envoy’s data and comments from major companies requiring employees to return to the office, urban area (workplace) traffic has certainly picked up since the COVID period, which I expect to help drive more traffic to SG’s urban stores.

{kind=link}

My analysis and expectations seem to tie well with what management is commenting as well, where business has become steady from Monday to Thursday (vs. previously, where it was only Tuesday to Thursday). Additionally, I anticipate growth to see additional traction and increased throughput with the launch of the Sweetpass loyalty program on April 24 . In light of management's emphasis on the program's successful pilots and opportunities in personalization and marketing to increase frequency and comps, I have no doubt that Sweetpass would result in increased foot traffic. However, given that high-frequency customers tend to be early adopters, this could have an immediate effect on SSS due to the increased demand for discounts that will be placed on SG.

So I think your comment about the dynamics of price mix in the quarter, it sounds like maybe we're at the point or at least in the second quarter where Sweetpass was like net-net a little bit of a net comp headwind in terms of giving the discount, but not seeing the full benefit of potential frequency increases or even new people coming into the brand. 2Q23 earnings results call

As the urban area continues to drive growth with the help of Sweetpass and work from home ending, and as suburban traffic eventually recovers, I expect SSS to gradually return to mid-single-digit [MSD] levels (seen in 2018). Since many workers who used to commute into the city are now stranded at home, I suspect that the rise in suburban traffic can be partially attributed to the rise in the number of people who work from home. Since they can no longer work from home, these employees are "leaving" the suburbs, creating a drag on the performance of SG in the suburban areas.

“For example, the COVID-19 pandemic has significantly impacted our financial results in these urban locations far more negatively than our suburban locations, and as of the end of fiscal year 2021, our AUVs for our urban locations were still materially lower than our AUVs for our urban locations as of the end of fiscal year 2019.” 2022 10K

Additionally, I anticipate that the new infinite kitchen business model will give SG yet another growth driver, potentially with higher margins. Management has stated that the infinite kitchen can produce 400-500 bowls and salads per hour, which is a 50 percent increase over the current store layout and requires 30 percent fewer workers. Since the majority of F24 openings will use this kitchen (as per management), I anticipate fewer restaurants opening next year but higher profit margin due to increased efficiency.

Valuation

Own calculation

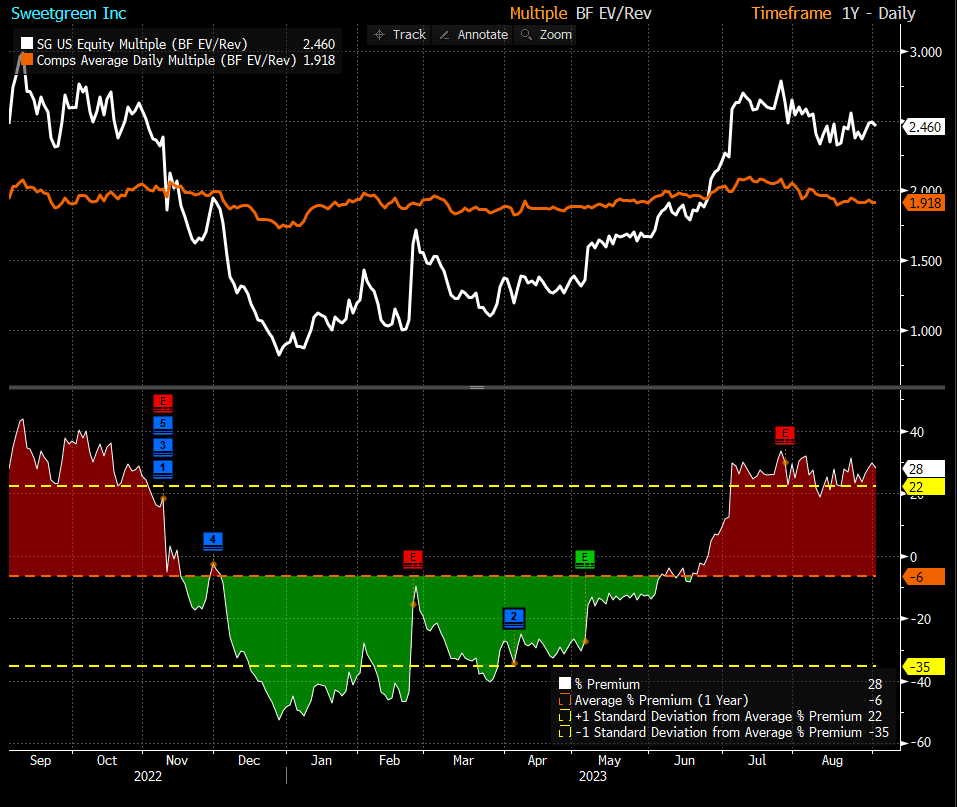

I believe the fair value for SG based on my model is $18. My model assumptions are that SSS will grow revenue in the teens for the next 2 years after meeting its FY23 guidance of $585 million. The high teens growth will be driven by MSD SSS growth of 5% and new store openings at an MSD-to-HSD growth pace (lower than the 10 in 2Q23) as I expect more infinite kitchen concepts to be rolled out. As I expect SG to grow much faster than other casual restaurant peers due to the reasons stated above, I believe it should trade at a premium. Assuming SG maintains its current premium, trading at 2.5x forward revenue, the stock is worth $18. I sense-checked my price target against SG's historical performance and noted that this is merely a recovery to 4Q22 levels.

Peers include: Kura Sushi USA ( KRUS ), Jack in the Box ( JACK ), Dine Brands Global ( DIN ), Portillo’s ( PTLO ), Krispy Kreme ( DNUT ), First Watch Restaurant Group ( FWRG ), and Papa John’s International ( PZZA ), etc. The median forward revenue multiple peers are trading at is 1.9x, the expected 1Y growth rate is 8%.

{kind=link}

Risk

Businesses that have invested heavily in the "healthy food" movement may face difficulties due to the trend's uncertain longevity. If this trend were to reverse, it could be bad news for these businesses. The current branding of SG, which centers on salads, is a major roadblock to entering the alternative food segment.

Conclusion

In conclusion, SG presents a compelling investment opportunity. Despite its recent impressive stock rally, I believe there is still room for growth. The signs of recovery in urban SSS are promising, especially with the resurgence in workplace traffic as employees return to offices. The launch of the Sweetpass loyalty program is also expected to further boost foot traffic, although it may initially impact SSS due to increased demand for discounts. As urban areas continue to drive growth and suburban traffic gradually recovers, I anticipate SSS returning to mid-single-digit levels. The introduction of the infinite kitchen model is poised to enhance efficiency and profitability, potentially providing another growth driver.

For further details see:

Sweetgreen: Positive Signs Of Traffic Recovery In SG Urban Areas