RYF - T. Rowe Price: Attractive Valuation And Dividend Yield

- T. Rowe Price is one of the leading asset managers in the U.S. The company's funds perform well versus peers and benchmarks.

- The 2022 bear market has increased the yield to 4%+ and brought down the valuation. Dividend safety is excellent.

- The firm is a Dividend Aristocrat and Dividend Champion with 36 consecutive years of increases.

- T. Rowe Price stock is undervalued.

T. Rowe Price Group, Inc. ( TROW ) is one of my favorite asset managers. Most of the other ones I like are privately held, like Vanguard and Fidelity. However, TROW is publicly traded, allowing small investors to hold shares of a successful company in the asset management industry.

Asset manager stocks have been hit hard during the 2022 bear market because revenue and profitability are tied to stock prices. TROW's stock price is down nearly 39% year-to-date as of this writing. But the stock's historical declines during down markets are well known. In any case, TROW is attractively valued, trading below its average P/E ratio in the decade, and is now yielding 4%+. The combination does not occur often. Furthermore, TROW is a well-known Dividend Aristocrat and Dividend Champion . Therefore, I view TROW as a long-term buy.

Overview of T. Rowe Price

T. Rowe Price was founded in 1937 and is headquartered in Baltimore, Maryland. The firm operates globally, with offices in major financial centers worldwide. The company offers retirement plans, mutual funds, and sub-advisory services to retail investors and institutions. TROW offers equity, fixed income, and multi-asset funds but focuses mainly on equity funds. In addition, the firm recently acquired Oak Hill Associates, expanding into alternate strategies and private markets. TROW had about $1.4 trillion in assets under management ((AUM)) at the end of May 2022. Total revenue was ~$7,708 million in the last twelve months and ~$7,672 million in 2021.

{kind=link}

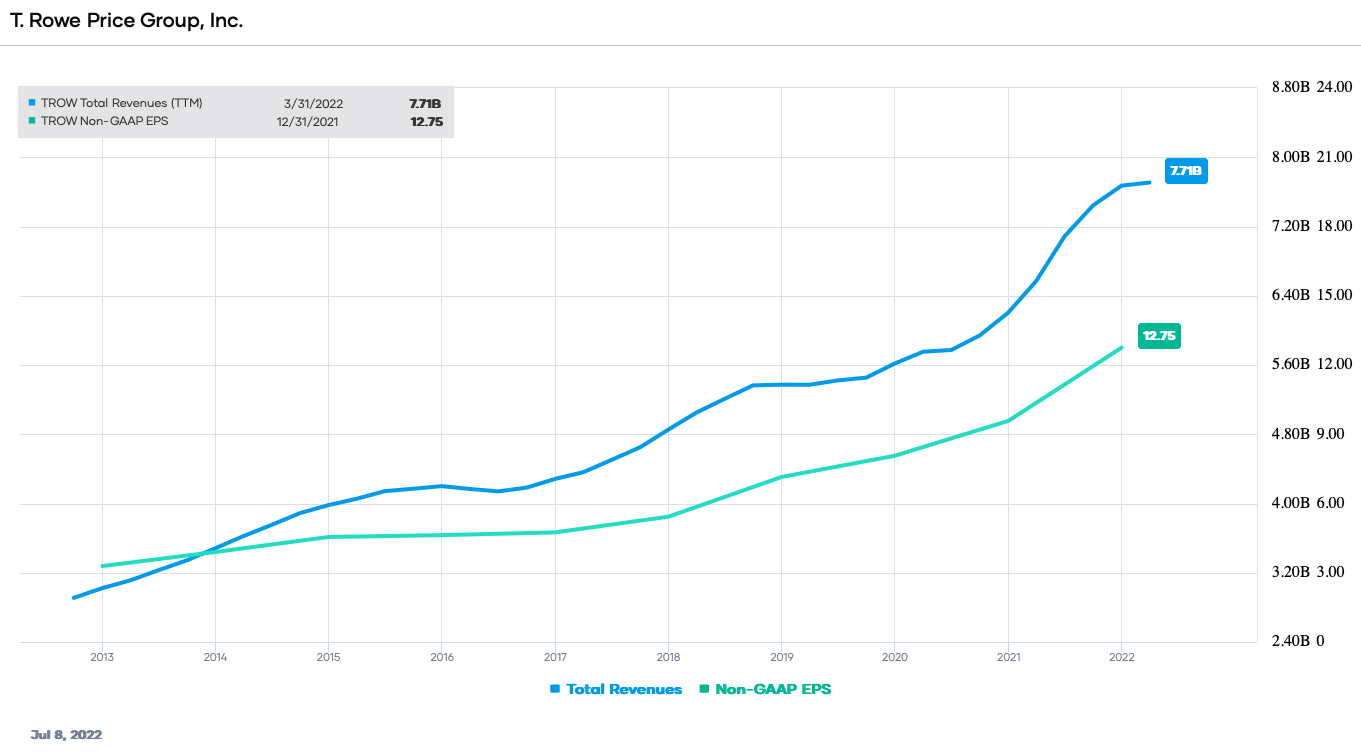

TROW's Growth

TROW has dramatically increased revenue and earnings per share in the past decade, pointing to its success as an asset manager focusing on retirement plans. Revenue has more than doubled from about $3.02 billion to around $7.71 billion, while diluted adjusted EPS increased more than three times from $3.20 in 2012 to $12.75 in 2021. Notably, revenue has increased despite industry-wide fee compression.

{kind=link}

In the trailing 5 years, revenue has grown at a 12.4% compound annual growth rate [CAGR], while EPS has grown faster at a 21.8% CAGR. In the past decade, revenue has grown at 10.8% CAGR, while EPS has grown at a 15.9% CAGR. One must go back to the sub-prime mortgage crisis for consistent declines in both.

TROW has grown in part over more prolonged periods because of successful mutual funds that perform better than peers and benchmarks. Retail and institutional investors are attracted to successful funds. The combination of a bull market and better fund performance is a powerful force for increasing AUM and thus revenue and profits.

Year-to-year fluctuations are not as important as long-term performance, which is where TROW excels. At the five-year and ten-year marks, the majority of the firm's funds outperformed the Morningstar median, passive peer median, and their benchmarks. For example, in the trailing five years, 64% of TROW's equity funds performed better than the Morningstar median, 55% performed better than the passive peer median, and 59% performed better than their benchmarks. Moreover, the equity funds do even better after ten years.

{kind=link}

Notably, the multi-asset funds are the top performers. TROW has a significant presence in retirement plans, and many workers are attracted to target-date funds and multi-sector funds for their simplicity.

Dividend Analysis

TROW is a well-known dividend growth stock and a favorite amongst investors. The dividend yield is currently 4%+, and according to Dividend Radar , the company has increased the dividend for 36 consecutive years. Hence, the stock is a Dividend Aristocrat and Dividend Contender.

The forward dividend yield is currently approximately 4.04%, based on an annual dividend rate of $4.80 per share. The yield is roughly the highest in the past decade, but dividend safety has not been sacrificed. In fact, dividend safety is outstanding, as we discuss below.

{kind=link}

The mixture of dividend yield and growth makes the stock attractive to investors. TROW last raised the quarterly dividend in February 2022 to $1.20 from $1.08 per share. The trailing dividend growth rate is consistently in the double-digits and was ~15.6% CAGR in the past five years and ~13.3% in the past decade.

Moreover, TROW has not materially increased the payout ratio to achieve such high growth rates. The relatively conservative payout ratio of ~48% likely means more double-digit increases in the future. However, investors must remember that in years when the market underperforms, dividend growth may slow, but it is usually better in bull markets.

{kind=link}

TROW has historically had excellent dividend safety based on earnings, free cash flow ((FCF)), and the balance sheet.

Consensus estimates in fiscal 2022 for TROW are $9.98 per share, and the dividend is $4.80 per share. These numbers produce a payout ratio of ~48%. Our cutoff payout ratio is 65%, meaning TROW's dividend is safe with a decent buffer. Importantly, this payout ratio is during a bear market and declining AUM. During a bull market and rising AUM, revenue and earnings are usually higher, and the payout ratio is lower.

TROW had around $3,326 million in FCF in the past 12 months. The dividend required approximately $1,029 million, giving a dividend-to-FCF ratio of roughly 31%. This value is significantly below our cutoff of 70%, meaning there is little risk of a dividend cut based on FCF.

The firm is known for its fortress balance sheet. It is one of the few companies that have no debt. At the end of Q1 2022, TROW had no short-term or long-term debt. The company had ~$1,998 million in cash and equivalents and $2,879 million in investment. Consequently, debt is not a risk to dividend safety.

Valuation

TROW's stock price has been punished in 2022 due to the sensitivity of revenue and earnings to market movement. Consequently, the stock price tends to be more volatile than the broader market, with a beta of about 1.33 in the past year. As a result, the stock price is down more than the S&P 500 Index and Nasdaq. However, the company has solid dividend and return perspectives. TROW's forward earnings multiple is about 11.9X, below its range in the past five years and ten years.

The consensus analyst 2022 earnings are now $9.98 per share. We will use 14X as a reasonable value for earnings multiple. This value is below the average in the past five years and the past decade. However, we account for a higher beta and fee compression affecting the industry.

Our fair value estimate is $139.72. The current stock price is ~$116.63, suggesting that the stock is undervalued based on earnings.

Applying a sensitivity analysis using price-to-earnings ratios between 13X and 15X, we obtain a fair value range from $129.74 to $149.70. Thus, the current stock price is ~78% to ~90% of the reasonable value estimate.

Estimated Current Valuation Based On P/E Ratio

| P/E Ratio |

| 13 |

| 14 |

| 15 |

| Estimated Value |

| $129.74 |

| $139.72 |

| $149.70 |

| % of Estimated Value at Current Stock Price |

| 90% |

| 83% |

| 78% |

Source: dividendpower.org Calculations.

How does this analysis compare to other valuation models? An EV/EBITDA multiple analysis from finbox gives a fair value estimate of $169.88 per share. The model assumes a forward multiple of 9.9X. Portfolio Insight's blended fair value model accounting for the P/E ratio and dividend yield gives a fair value of $158.12 per share. We do not use the Gordon Growth Model here because of the high dividend growth rates.

The average of these three models is ~$155.91, suggesting TROW is undervalued at the current price.

Final Thoughts

TROW is a popular dividend growth stock to own. The combination of consistent double-digit dividend growth rates and dividend safety is appealing. In addition, investors tend to like an excellent balance sheet with no debt. On the downside, investors must tolerate a higher beta and volatility than the broader market because revenue and EPS are sensitive to stock market movements. But when markets reverse, TROW often does well. The stock is undervalued today. I view TROW as a long-term buy.

For further details see:

T. Rowe Price: Attractive Valuation And Dividend Yield