RGR - Take Cover From Sturm Ruger

2023-10-13 13:55:23 ET

Summary

- Sturm, Ruger & Company's financial results have been poor, with a 24.6% decrease in gross profit and a 40% decrease in net income relative to 2022.

- While still very strong, the capital structure of the company has deteriorated substantially in the past four years.

- The stock is more expensive on a risk adjusted basis to risk-free alternatives. Prompting the question: why would you buy this?

It's been just over four months since I announced to the world that I'm neither adding to nor selling my stake in Sturm, Ruger & Company ( RGR ), and in that time the shares have returned about 0.3% against a gain of about 5.7% for the S&P 500. Underperformance always intrigues me, so I thought I'd review the name yet again to see if it makes sense to buy or not. I'll make that determination by looking at the latest financial results, and comparing that to the valuation. As is frequently the case now, my "buy, sell, hold" decision will be made against the backdrop of a risk-free environment where an investor can earn a fairly decent risk-free return. In my view, the world has changed in a way that not many investors seem to have picked up on, namely that the TINA narrative no longer exists.

Welcome to the "thesis statement" portion of my article. I put such paragraphs at the beginning of each of my pieces in order to give people more than what they get from a few bullet points and a title, but much less than they are obliged to endure in an entire article. You're welcome. Given the dividend policy here, it's obviously very well covered. Additionally, the capital structure at this firm is one of the strongest I've seen in years. The problem is that it's far less strong now than it was only a few short years ago. Additionally, the latest sales and income numbers have been very poor in my estimation. Over the past decade, it's been a great decision to buy this stock when sales and earnings are down as a way to play the inevitable improvement. As the saying goes, though, that was then, this is now. This stock was relatively attractive when rates were much lower. Today, an investor can receive a much better, more predictable, risk-free return in government bonds. This prompts the question: why would you buy this? While I'm not selling, I'm not buying, and I would urge others to stay away until the dividend yield spikes and/or the yield on the risk-free alternatives falls again.

Financial Snapshot

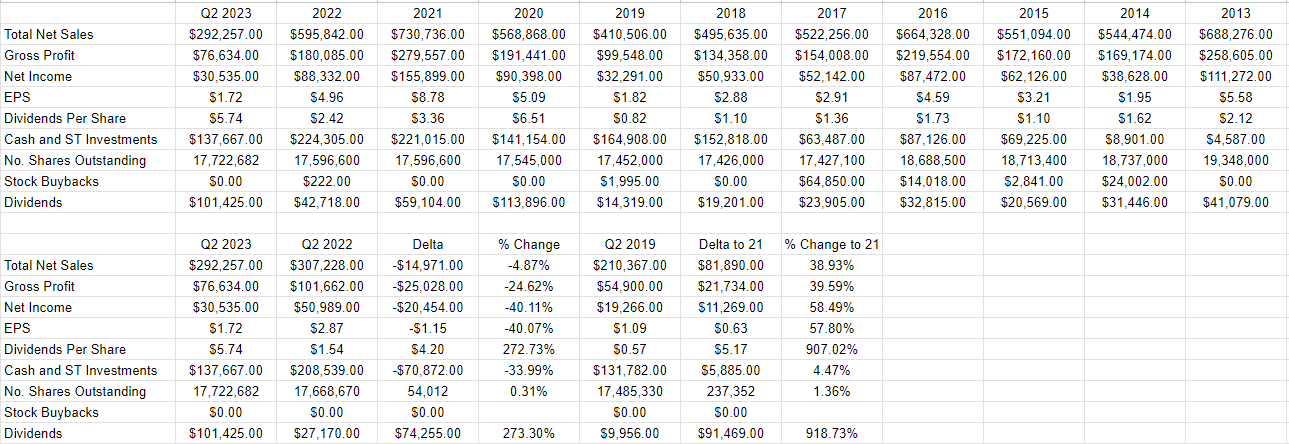

I can't think of a way to sugarcoat it, so I won't sugarcoat it. Relative to the same period in 2022, this year's financial results have been fairly bad. While revenue is down only about 4.9% relative to the same period a year ago, both gross profit and net income are down by an eye-watering 24.6% and 40% respectively. On the bright side, the capital structure remains quite strong, with cash and short-term investments representing about 2.16 times total liabilities. I wouldn't be me if I didn't sour the mood a bit by pointing out that this "bright side" is now far less bright than it was this time last year, when cash and short-term investments were about 3.67 times total liabilities. It's also the case that cash and short-term investments represented 4.67 times total liabilities in 2019. So, the capital structure is very strong at the moment, but that doesn't change the fact that it's deteriorated substantially in only four years.

I feel the need to end this section on a bright note, though, so I'll end it on a bright note. This business is cyclical. For instance, both revenue and net income at Ruger bottomed out in 2019, and recovered nicely from there. The year 2014, for instance, saw a 21% drop in sales from the previous year, and then went on to grow by 22% over the next two years. In other words, I would urge investors to not "freak out", as the young hippies say, and understand that this is a business that bobs up and down over time. This company, with its well-covered dividend, happens to be in yet another lull phase, which has traditionally been a great time to buy the stock. Given that, I'd be very happy to buy more of this business at the right price.

{kind=link}

The Stock

When I decide whether or not to make an investment, I like to consider the stock, and the business to be two distinct things. We all know that the business manufactures and sells firearms and various other items. The stock, on the other hand, is the aggregation of the crowd's ever-changing views about the long-term health of the business. Additionally, the stock can be influenced by a host of factors having little to do with the health of this specific enterprise. For instance, people may decide that a sideways glance from a central banker is relevant to this stock, in spite of the fact that it has virtually no debt. Additionally, the demand for Sturm Ruger shares may be affected by the demand for "stocks" as an asset class.

When you consider the stock of any enterprise, it becomes pretty obvious pretty quickly that the lower the price you pay for a business, the greater will be your subsequent returns. This is why I like to buy cheap stocks. They offer both lower risk and higher return potential. They're lower risk for the mind-numbingly obvious reason that they have less far to fall than some market darling. They offer greater return potential because any amount of good news may cause the shares to climb skyward.

Those who know my stuff know that I measure the cheapness of a stock in a few ways ranging from the simple to the more complex. On the simple side, I like to look at ratios, and I like to see a stock trading at a discount to both its own history and the overall market. When I last reviewed these shares, they were trading at a price to free cash flow ratio of about 21 times, and P/E ratio of about 13.14. The shares are now 7% cheaper on a price to free cash flow basis, but they're 6.5% more expensive on an earnings basis per the following.

I also consider "cheap" in the context of the nature of other investments available. So, rather than describe risk in terms of cash outlay, I think about the risks of cash flows of one business relative to the risk-free alternative, for instance. So, this stock may have been quite cheap on this basis when an investor would only receive 1% on a risk-free investment. At that time, there was no alternative. Today, though, the same stock, with the same dividend yield and PE multiple etc., may be quite dear.

So when I last looked at Sturm Ruger, the dividend yield was a relatively meager 2.43%, which was about 100 basis points below the then 1-Year Treasury Bill yield. Fast-forward to the present, and, although the yield is about 16.5% greater, the spread between the stock and the 1-Year Treasury Bill has jumped to 258 basis points . So in this regard, the stock is relatively much more expensive than it was previously.

For those who fret that it's unfair of me to compare this stock to a 1-Year Treasury Bill, since a stock is an asset that can exist infinitely long, in theory at least. When we compare the current dividend to the 10-Year Treasury Note, a similar story emerges. The risk-free rate is offering 177 basis points greater return than the stock at the moment.

You may recall from earlier in the article when I pointed out that I measure the cheapness of a stock in a few ways. I like ratios, and I like to think about units of risk, but I also want to try to work out what the market is "thinking" about a given investment. The way I do this is by employing methods described in books like Professor Stephen Penman's "Accounting for Value" and Mauboussin and Rappaport's "Expectations Investing." Each of these uses the stock price itself as a rich source of information. Penman, in particular, shows investors how they can employ a bit of high school algebra to isolate the "g" (growth) formula in a standard finance formula to work out what the market expects from a given company. Applying this way of thinking to Sturm Ruger at the moment suggests the market is assuming that this company will grow earnings at a rate of about 5% from current levels. Additionally, I feel compelled to point out that Wall Street seems to be forecasting EPS of $3.53 for the year 2023 . For those who haven't been keeping track, I'll remind you that for the first nine months of the year, EPS has been $1.72. Using the arithmetic skills I learned many decades ago under the supercilious gaze of the good sisters at Holy Spirit School many years ago, that means that Wall Street is forecasting final quarter earnings of $1.81. That is excessive in my view.

In closing, I'd remind investors that they're not seeking "returns." They're seeking "risk-adjusted returns", and on that basis, it's possible to get substantially greater, more predictable returns. For that reason, I can't recommend buying more. While I'm holding my shares, if you're just coming to this party, I would hold off until the risk-free yield drops and/or the yield on this stock spikes higher.

For further details see:

Take Cover From Sturm, Ruger