RL - Tapestry: Navigating Luxury Retail Landscape Well

2023-08-04 03:32:14 ET

Summary

- Tapestry is positioned well in the fashion industry due to its strong brands Coach and Kate Spade, with Coach showing signs of improved growth.

- Margins have remained stable, but improvement in the performance of Kate Spade could lead to an overall improvement. This would further widen its superiority over peers.

- The business does have execution risk with delivering improvement and is facing slowing growth, but we believe this is sufficiently priced in.

- Tapestry is trading at 11x FCF, has a FCF yield of 9%, and is trading at a 37% discount to its peers. The business looks fairly undervalued.

Investment thesis

Our current investment thesis is:

- Tapestry (TPR) is positioned well in the fashion industry, owing to Coach and Kate Spade, both of which are strong brands. Coach in particular is showing signs of improved growth in the coming years, as interest in the brand improves.

- Margins have remained sticky during the current economic conditions, while its small brands continue to drag on Coach. If these can be improved, there is real scope for improvement.

- Relative to its peers, the business looks good. It's lacking in growth but margins are superior. Even if we assume the business warrants a discounted valuation to the group average, it still looks cheap.

Company description

Tapestry Inc. ( TPR ) is a leading luxury fashion company that owns renowned brands such as Coach, Kate Spade New York, and Stuart Weitzman. Headquartered in New York, USA, Tapestry operates a global network of stores and digital channels, offering high-quality handbags, accessories, footwear, and ready-to-wear products.

{kind=link}

Share price

Tapestry's share price has underperformed in the last decade, losing value during a period of expansion for the wider market. This is due to underwhelming financial results.

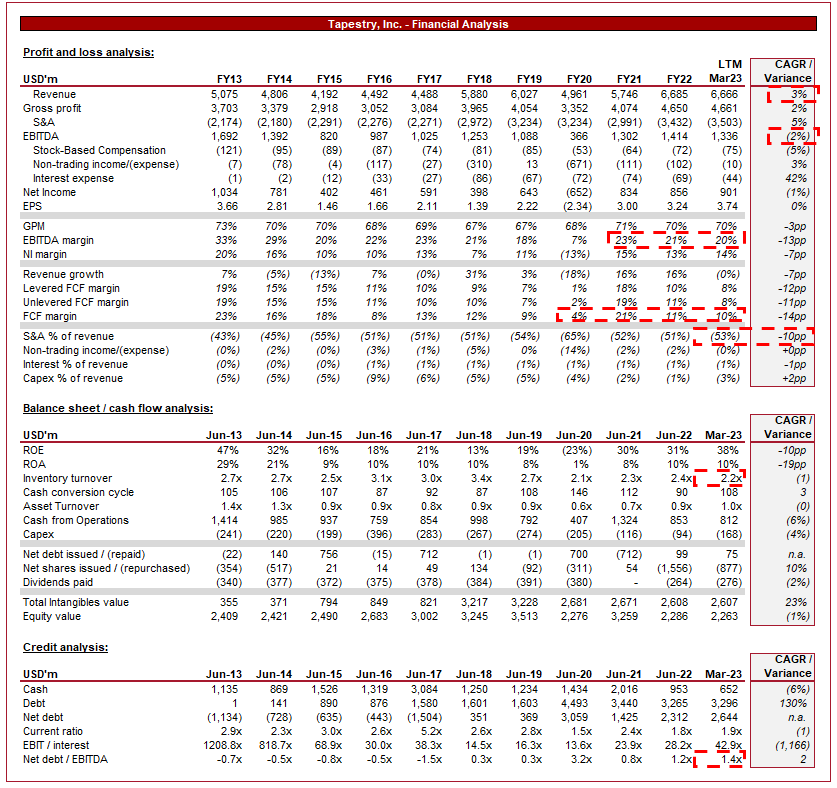

Financial analysis

Tapestry financial analysis (Capital IQ)

{kind=link}

Presented above is Tapestry's financial performance for the last decade.

Revenue & Commercial Factors

Tapestry's revenue has grown at a CAGR of 3% in the last 10 years, with a number of fiscal years of negative growth. This a poor return, especially when considering a large portion of this is due to the acquisition of Kate Spade and Stuart Weitzman. There is clearly an underlying issue with achieving consistent organic growth.

Business Model

Tapestry's business model is centered around designing, manufacturing, and marketing luxury fashion products through its three distinct brands. The company operates as a multi-brand entity, catering to various customer preferences and demographics. This multi-brand strategy is critical to long-term success in the fashion industry we feel, as tastes and trends change over time, making it difficult for a single brand to remain relevant. With 3 brands, Tapestry has a broad scope for design innovation, as well as the ability to target different segments. The net benefit from this is a diversified revenue profile and reduced risk.

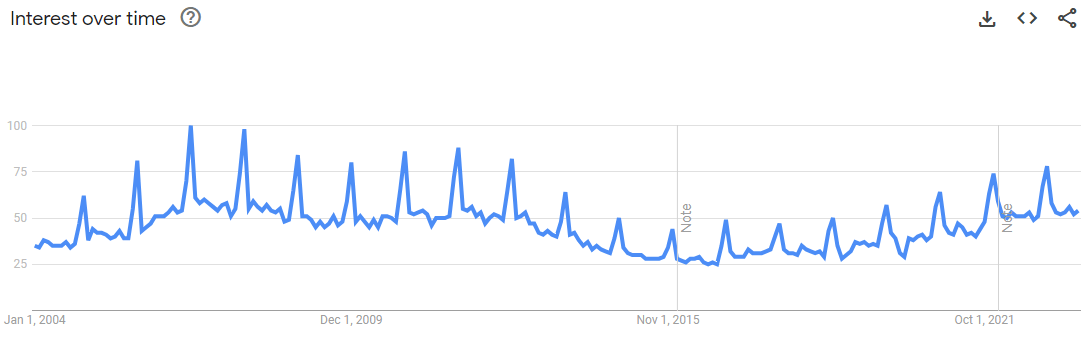

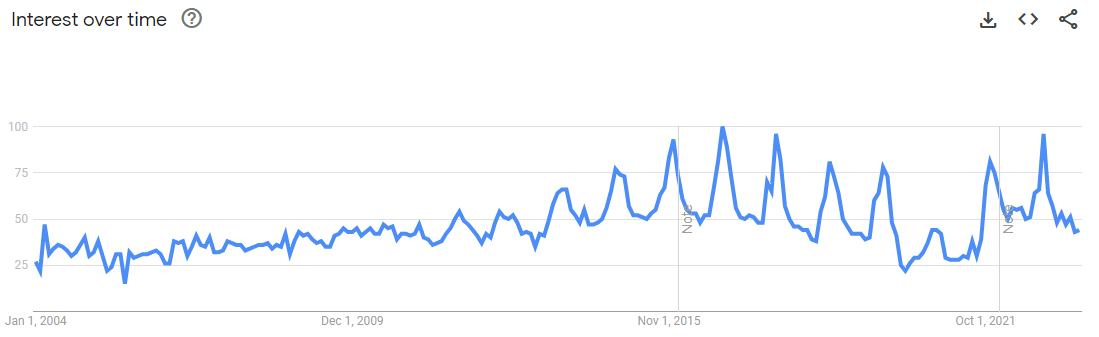

The Coach brand looks to be experiencing a resurgence following the pandemic, with strong revenue growth and a return to its pre-FY14 levels. This graph is almost identical to its interest over time as recorded by Google.

{kind=link}

The decline post-GFC to the pandemic is a reflection of increased competition and changing trends. With the rise in e-commerce, consumers are provided significantly more choices, allowing them to shop around and compare. The fight for consumer sales was no longer dictated by footfall. Further, there was the rise of fast fashion, with businesses taking strong inspiration from high-end/luxury fashion houses to produce similar products quickly.

This has made it difficult for Coach to develop its value proposition to consumers, contributing to softening sales. Unlike some of its peers, however, the business did not experience large declines. This implies an inherent strength in the brand, which we assign to its exposure to Handbags and Footwear. These are both segments that are notoriously difficult to disrupt by new entrants due to the importance of a strong brand and quality, clearly two characteristics Coach poses.

{kind=link}

The recent resurgence suggests Management has been successful with product innovation and effective marketing. The business is being more expressive with its designs and production process, seeking to capture a Gen Z audience which is quickly becoming the largest market segment. The Coach transition has been dubbed " from accessible luxury to expressive luxury".

More broadly, the Tapestry business has adjusted leadership in recent years, increased its use of data analytics to understand customers and the industry, improved operational capabilities, and shifted its culture to one of "customer first".

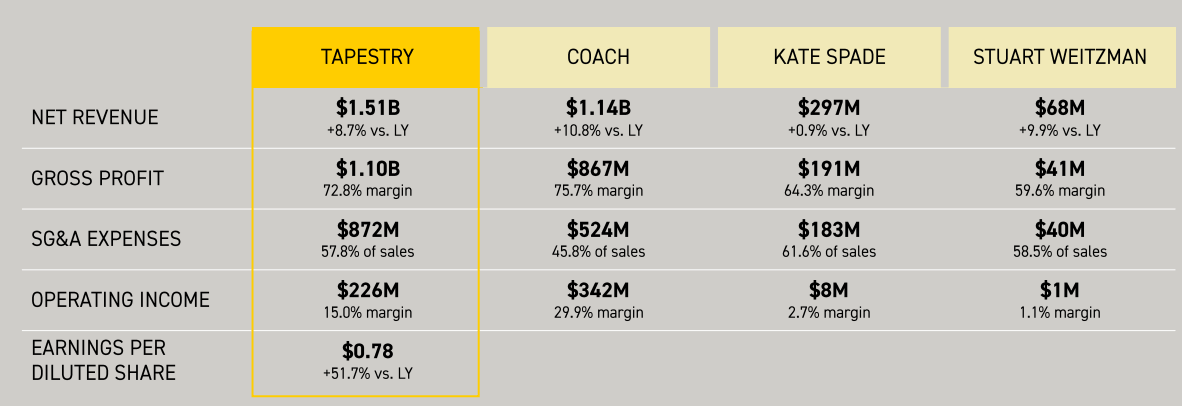

Coach is by far the largest brand in the group, contributing $1.1bn of revenue in Q3. This is followed by Kate Spade ($0.3bn) and Stuart Weitzman ($0.07bn). The dominance of Coach within the group is larger when considering the profitability, with over 90% at an OP level.

{kind=link}

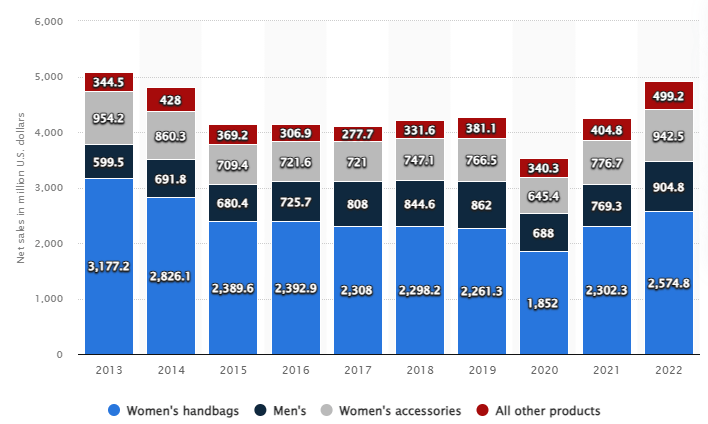

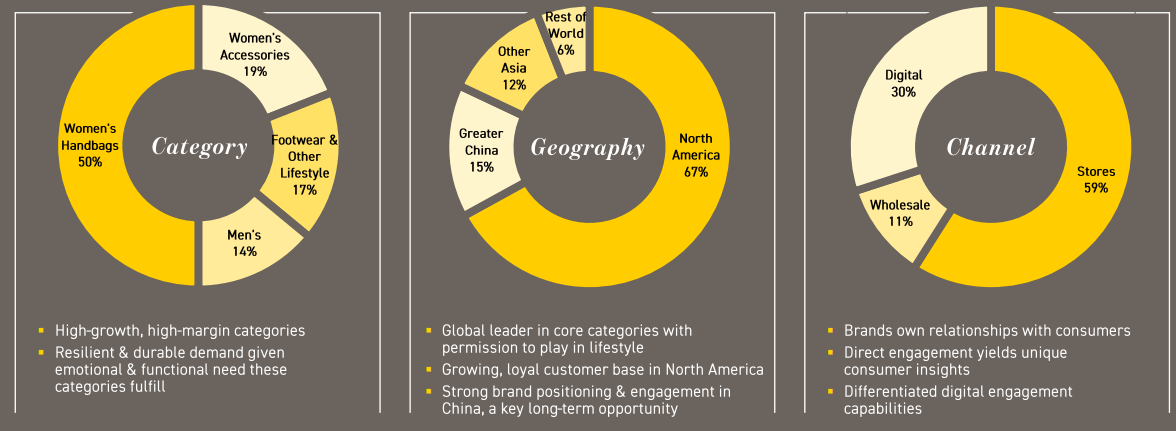

Tapestry primarily targets the female audience, with 50% of its sales being Women's handbags, and a further 19% being Accessories. It primarily operates within North America (67%) through Stores (59%), although is seeing strong growth in Asia (27%) and e-commerce (30%).

{kind=link}

Targeting Women is highly lucrative if successful, as Women comprise more than half of the US population and control/influence over 80% of consumer spending. Further, Asia is currently the largest fashion market, with an insatiable hunger for Western goods. We believe this trend will continue as economic development and growing middle-class support improving purchasing power. Tapestry is positioned well to benefit from this, as its 27% sales suggest a good brand presence in the region.

For these reasons, we believe the company's customer profile is highly attractive, and in particular, so is the Coach business.

Our concerns come with Kate Spade and Stuart Weitzman. The business paid a substantial sum for both ($2.4bn for KS and $0.5m for SW). Neither look to be paying off currently. Ironically, the acquisitions were likely made to support Coach's softening performance. Now, these businesses are dragging on a resurging Coach.

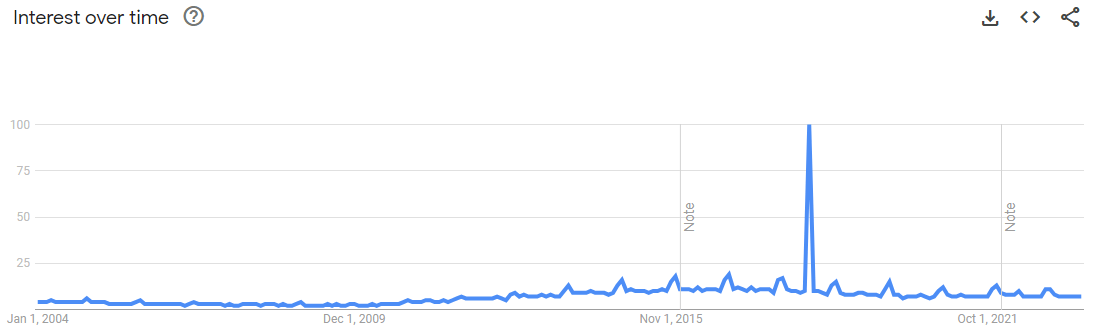

As the two following graphs illustrate, interest in the brands has not really developed in any meaningful way.

Kate Spade (Google ) Stuart Weitzman (Google)

{kind=link}

{kind=link}

We would like to see improved social media marketing and collaborations with influencers, seeking to improve awareness of the brands (acknowledging that Kim K is working with SW). Creating viral moments is key, such as with creative products and promotions.

Kate Spade has significant potential, with a quality design philosophy and a similar target market to Coach. It is growing well but its margins are terrible relative to Coach. With increased interest in the brand, marketing spending can soften and discounting can be reduced, allowing for margin appreciation.

OPM (Tapestry)

We would also like to see Tapestry invest in its e-commerce capabilities, driving sales through this channel. This will reduce the pressure to increase its footfall to improve growth, allowing for improved economics. With e-commerce at 30% of revenue, there is sufficient scope for improvement.

Tapestry faces competition from other luxury fashion companies and high-end retailers. Key competitors include Capri Holdings (Michael Kors, Versace, Jimmy Choo) ( CPRI ), Ralph Lauren ( RL ), and PVH Corp ( PVH ). To a lesser extent, the business also competes with the traditional luxury brands but at its price point, is clearly an entry-level/accessible offering. Said luxury brands include LVMH ( LVMHF ), Burberry ( BURBY ), and Kering brands ( PPRUF ). Tapestry has struggled to win market share in recent years but is positioned well we feel following the improvement in Coach.

Economic & External Consideration

Current economic conditions are uncertain, with high inflation and elevated rates. This is impacting the business in the following way:

- Discretionary Spending. The combination of these factors will lead to cautious consumer spending, as finances are squeezed. Revenue growth reflects this, with a flat LTM performance.

- Input Costs. Rising inflation has resulted in increased production and distribution costs, with margins sliding relative to FY21 levels. This said, the business remains in line with FY19, a good performance in our view.

Margins

Tapestry's margins have declined over the historical period, primarily due to softening demand for Coach products, as well as product mix change following the 2 brand acquisitions.

With S&A spending at 53% of sales, the company's customer acquisition cost is far too high. If demand does sustainably improve, we see this declining, allowing for margin improvement.

Balance sheet & Cash Flows

Inventory turnover remains below its pre-covid levels, acting as a drag on cash. We would like to see this improve as the business has good cash generation.

Tapestry is conservatively financed, with a ND/EBITDA ratio of 1.4x. At this level, the business is able to consistently distribute to shareholders while investing in growth.

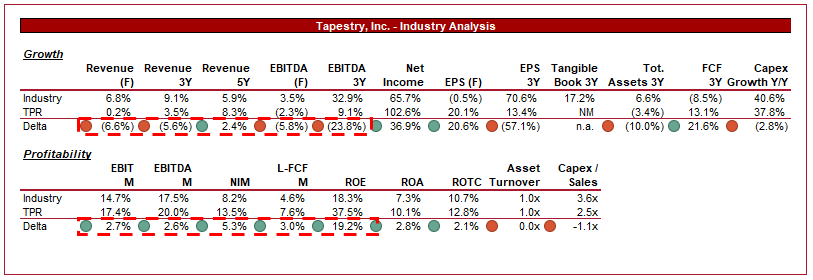

Industry analysis

Apparel, Accessories and Luxury Goods (Seeking Alpha)

{kind=link}

Presented above is a comparison of Tapestry's growth and profitability to the average of its industry, as defined by Seeking Alpha (27 companies).

Tapestry performs well relative to the group, while not standing out. Its growth is below average, although at a 5Y level is competitive. This growth delta is concerning but we expect it to close in the coming years. The forward metric is not overly concerning as Tapestry's year-end means a material difference in the periods considered.

From a margin perspective, the business performs extremely well. Tapestry has a moderate delta in every key metric, importantly in FCF and ROE. We believe FCF can improve further with better inventory management, widening the outperformance.

Our preference is to favor margins to growth in a mature industry but given the uncertainty around growth improvement and the margin delta being within a small range, we believe Tapestry should trade at a small discount to its peers (Conservatively).

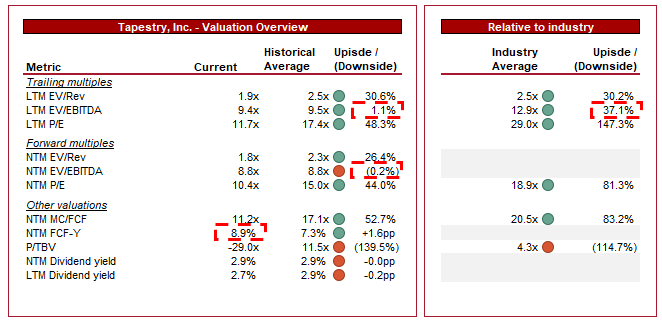

Valuation

{kind=link}

Tapestry is currently trading at 9x LTM EBITDA and 9x NTM EBITDA. This is parity with its historical average.

Our view is that parity/a small premium to its historical average is reasonable. The commercial profile of the business is improving, led by Coach, while margins have remained at pre-Covid levels. Importantly, its FCF-Y is higher relative to its historical average, as is its FCF multiple, implying some upside.

Relative to its peers, however, the business looks extremely cheap. It is trading at a 37% discount on an EBITDA basis. Even if we assume a 10% discount is warranted (which is likely extremely), this still leaves an upside of 27%.

Key risks with our thesis

The risk to our current thesis is:

- The business is facing some near-term issues with flat growth which could spook investors. This looks to be priced in, however, and is already forecast by Management (0.2% growth in FY23F and 3.5% in FY24F). This reduces the risk of any surprises we feel.

Final thoughts

Tapestry is a solid business. It owns 3 brands, two of which we feel are strong with good scope for long-term growth. Margins are attractive, especially when compared to peers, with a clear route to improvement through subsiding economic pressures and improvements with Kate Spade. The business has faced issues with growth but Coach is showing signs of revitalization.

Tapestry has clear risks associated with it but at its current valuation, these all look sufficiently priced in to imply upside.

For further details see:

Tapestry: Navigating Luxury Retail Landscape Well