TRGP - Targa Resources: Promising Growth Prospects But Almost Full Valuation

2023-12-05 17:10:43 ET

Summary

- Targa Resources is the largest natural gas processor in the Permian Basin and has strong business momentum.

- The company has transformed its business model to be more resilient to downturns and has a high percentage of fee-based contracts.

- Targa Resources is expected to continue growing its earnings per share and has a shareholder-friendly approach, but its stock is currently almost fully valued.

Targa Resources ( TRGP ) is the largest natural gas processor in the Permian Basin. It enjoys strong business momentum and has promising growth prospects ahead and thus the stock has rallied 26% this year, thus outperforming the energy sector (flat this year) by an impressive margin. As the company is expanding its infrastructure at a fast pace and operates with a somewhat defensive, fee-based model, many investors will be tempted to initiate a position in the stock. However, the market seems to have already priced a significant portion of future growth in the stock.

Business overview

Targa Resources is focused on gathering, processing, transporting and selling natural gas as well as natural gas liquids [NGLs]. It is one of the largest independent midstream energy companies in the U.S.

Targa Resources went through a fierce downturn in 2014-2016 due to a collapse of the price of natural gas during that period. The collapse was caused by the boom in the production of shale oil and gas, which greatly increased the supply of oil and gas. Due to that downturn, the company incurred a 55% plunge in its earnings per share in 2015 and reported losses per share of -$1.80 in 2016. Even worse, it more than tripled its share count and the stock plunged 90% in less than two years. Notably, although the stock has recovered from that downturn, it is still trading 35% lower than its all-time high, which was posted in 2014. This is a testament to the material risk of the stock.

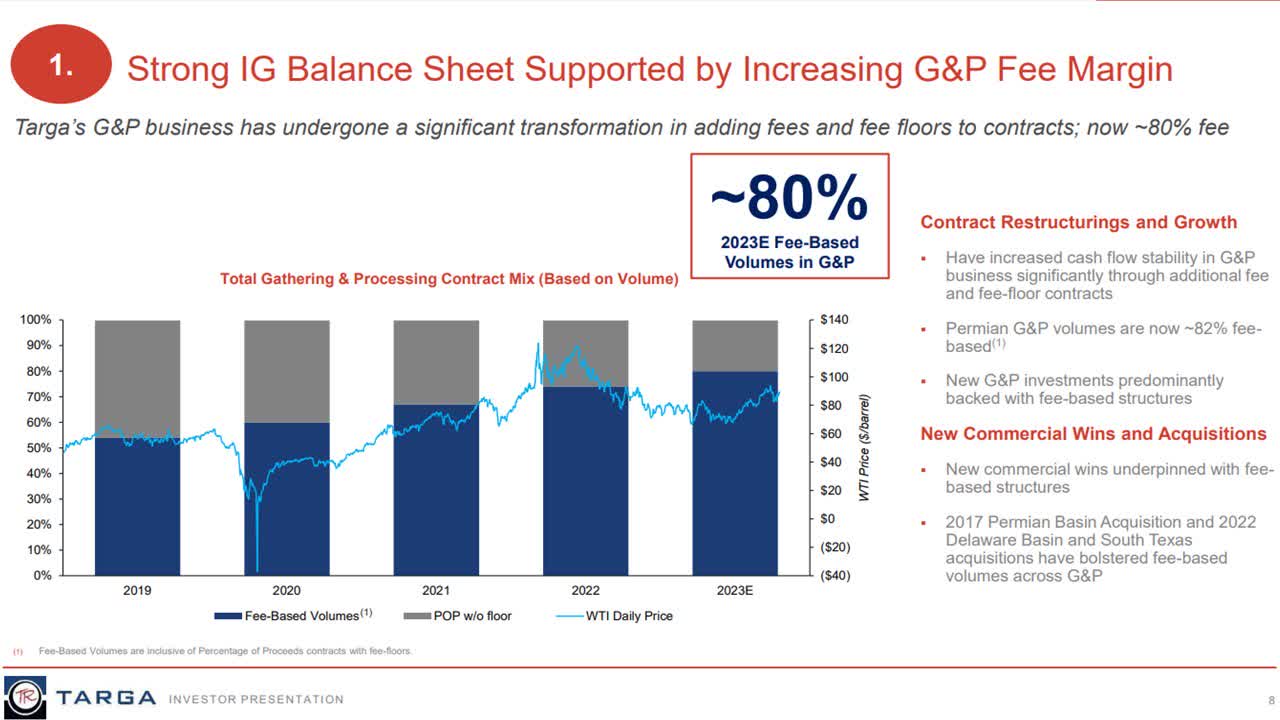

On the bright side, Targa Resources has gone through a major transformation in recent years in order to become more resilient to downturns. It has added many fee-based and minimum-fee contracts and thus approximately 80% of its gathering and processing volumes have become fee-based.

{kind=link}

Source: Investor Presentation

The fee-based and minimum-fee features of the contracts of Targa Resources have rendered the cash flows of the company more predictable and reliable than in the past. Of course, Targa Resources is still sensitive to the dramatic cycles of the price of natural gas, as it is a seller of natural gas, but its gathering and processing segment provides a strong buffer to the results of the company.

Targa Resources is currently thriving, primarily thanks to the contribution of a series of growth projects, which have come online in recent years. Another contributing factor is the acquisition of Lucid Energy for $3.55 billion in cash last year. Lucid Energy is a major processor of natural gas in the Delaware Basin, with more than 1,000 miles of pipelines, and thus it helped Targa Resources achieve significant economies of scale in the area.

In the third quarter, Targa Resources grew its adjusted EBITDA and its earnings per share 9% and 30%, respectively, over the prior year’s quarter, primarily thanks to record NGL transportation volumes. Notably, gas prices plunged vs. blowout levels in the prior year’s quarter amid the peak of the Ukrainian crisis. The strong growth of earnings in an environment of lower gas prices is a testament to the improved resilience of Targa Resources to low gas prices. It also shows the importance of the minimum-fee feature in the contracts of the company.

As there are no signs of fatigue on the horizon, Targa Resources is expected by analysts to grow its earnings per share 15% this year, from $3.88 to $4.46. Even better, the company is expected by analysts to grow its earnings per share by another 35% in 2024 and 24% in 2025, to $7.47, mostly thanks to growing production in the Permian Basin, fast-growing exports of LNG and LPG and some capacity expansion projects.

Debt

Targa Resources had a weak balance sheet for many years due to the aforementioned downturn that the company faced in 2014-2016 and its excessive investment in its infrastructure. It is remarkable that Targa Resources issued a 10-year bond at a 6.875% rate almost five years ago, when benchmark interest rates were near all-time low levels. The exceptionally high interest rate charged by the market was a confirmation of the weak balance sheet of the company back then.

Fortunately, many growth projects have begun generating cash flows in the last few years. As a result, the company has significantly reduced its debt load. It currently has a leverage ratio (Net Debt to EBITDA) of 3.7 , which is well within the target range of 3.0-4.0 of management. Moreover, interest expense currently consumes only 26% of the operating income of the company while its net debt (as per Buffett’s formula: net debt = total liabilities – cash – receivables) is standing at $14.4 billion . This amount is just 70% of the current market capitalization of the stock and about 10 times the annual earnings and hence it is certainly manageable.

Thanks to the strengthening of its balance sheet, Targa Resources has become markedly shareholder-friendly this year. In the latest conference call , it announced a 50% raise in its annual dividend, from $2.00 to $3.00, and thus the stock is now offering a 3.4% forward dividend yield. Even better, management stated that it expects to be able to grow the dividend even further in the upcoming years. The company has also reduced its share count by 2% in the last 12 months.

Thanks to the sanctions of the U.S. and European Union on Russia, the U.S. exports of LNG to Europe and other destinations is likely to remain on the rise in the upcoming years. In addition, the U.S. oil and gas production is likely to keep growing for years, particularly given the prolonged production cuts of OPEC and Russia in an effort to support the prices of oil and gas. As a result, Targa Resources is likely to keep thriving and remain shareholder-friendly for the foreseeable future, in line with the aforementioned analysts’ estimates.

Valuation

Targa Resources is currently trading at 20.0 times its expected earnings this year. This is an exceptionally high price-to-earnings ratio for a stock that belongs to the highly cyclical energy sector. However, as the company has promising growth prospects ahead, it is important to focus on its forward price-to-earnings ratios. The stock is trading at 14.8 times its expected earnings in 2024 and 12.0 times its expected earnings in 2025.

The median forward price-to-earnings ratio of the entire energy sector is 9.9 right now. Therefore, Targa Resources is trading at a richer valuation level than the average valuation level of the energy sector. On the one hand, the company seems to have better-than-average growth prospects and a more resilient business model than the average energy company. As a result, it probably deserves a premium in its valuation. On the other hand, given the high cyclicality of the energy sector and the valuation of Targa Resources at 12.0 times its expected earnings in 2025, it is safe to conclude that the market has already priced a significant portion of future growth in the stock. Overall, the stock appears almost fully valued right now.

Final thoughts

Targa Resources is thriving right now thanks to booming production in the Permian Basin and its fee-based business model. As long as U.S. gas production and U.S. LNG exports remain on the rise, the stock is likely to remain on its uptrend. However, due to its somewhat rich valuation, the stock will probably have material downside risk whenever it faces an unforeseen downturn, such as a plunge in natural gas prices or lower U.S. gas consumption. Given also the high cyclicality of the natural gas industry, the stock receives a “hold” rating.

For further details see:

Targa Resources: Promising Growth Prospects But Almost Full Valuation