TBLD - TBLD: A Discounted Income-Producing Focused Fund

2023-05-23 13:32:08 ET

Summary

- TBLD currently trades at a deep discount.

- The fund has the flexibility to invest just about anywhere.

- It currently sports an attractive distribution yield of over 8%.

Written by Nick Ackerman, co-produced by Stanford Chemist. This article was originally published to members of the CEF/ETF Income Laboratory on May 22, 2023.

Thornburg Income Builder Opportunities Fund ( TBLD ) launched in mid-2021. Suffice it to say, that was a pretty poor time to be launching a fund. Not only did investors have to take the ride lower due to discount widening that's almost always guaranteed from new funds, but also riding all assets lower. 2022 was a truly unique year that doesn't happen very often as both stocks and bonds fell sharply as interest rates were ramped up swiftly by the Fed.

Today, things have seemed to stabilize - at least for the time being. The Fed is anticipated to pause or at least be nearer to the end of rate hikes than the beginning. Although the market believes cuts are possible within the year, the Fed itself has continued to remain steadfast that rates will remain higher for longer.

That being said, as long as rates don't have to go sharply higher, this stability in interest rates means TBLD (and most other investments) also can stabilize. Since our last update , TBLD has been essentially flat on a total return basis. Most of the losses here were simply driven by an expanding discount since that update as well. Meaning that the actual underlying portfolio performed better.

TBLD Performance Since Prior Update (Seeking Alpha)

The flexibility of the fund and the discount continue to make TBLD an appealing choice for income investors.

The Basics

- 1-Year Z-score: -1.04

- Discount: 13.56%

- Distribution Yield: 8.31%

- Expense Ratio: 1.58%

- Leverage: N/A

- Managed Assets: $558.225 million

- Structure: Term (anticipated liquidation date August 2nd, 2033)

TBLD's investment objective is "to provide current income and additional total return." To achieve this, the fund will invest "in a broad range of income-producing securities to include both equity and debt securities of companies located in the U.S. and around the globe. The Trust additionally expects to employ an options strategy to generate current income from options premiums and to improve risk-adjusted returns."

This leaves the fund entirely flexible to invest in just about anything income related. 80% of the fund will be invested in income-producing securities "directly or indirectly." They aren't restricted to a certain market cap to invest in a company either but lean heavily toward large caps. At this time, those make up 94.5% of the portfolio.

They then mention that the global equity allocation should vary between 50%-90% - leaving the debt allocation with the remainder of the portfolio. The fund will typically be more tilted toward equity positions given the general weightings. The options strategy "will be approximately 10% to 40%" of the notional value of the portfolio. At only 8.9% of the portfolio being overwritten, they're slightly below their target. That would indicate they're fairly bullish, as they don't want positions called away.

The fund doesn't employ any leverage, and that can be beneficial during times of volatility, as it should be relatively less risky. With rising interest rates, that also pushed up the borrowing costs for most other leveraged CEFs. That was something else that TBLD could avoid. Though, it should be noted that they still leave the door open for leverage.

The fund's expense ratio of 1.58% is quite high. At the same time, given how flexible the fund is, it isn't completely out of the ordinary either.

Performance - Discount Deepens

When we last touched on the fund, the discount was right around 10%. I felt that was an attractive level to consider the fund. Being that it launched in 2021, it's still a relatively newer fund, but we're now coming up in two years. Most funds, even term funds, generally drop to significant discounts within a year or two of launching.

Given the struggle of the overall market when TBLD launched and Thornburg not being really a known CEF sponsor (though they have another fund in the works), this fund never really stood a chance. However, we're now near the lowest discount that the fund has been trading at since it launched. That could represent a fairly attractive time to consider this fund, even more, attractive than when we last touched on the fund.

TBLD Discount/Premium History (CEFConnect)

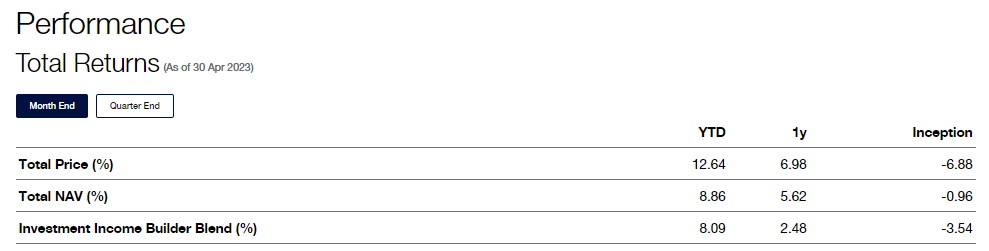

To touch on performance quickly, we can see that the fund is outperforming its benchmark on a year-to-date and one-year basis.

{kind=link}

The benchmark appropriately mixes in broad exposure that would mirror the fund's own type of exposure. I believe it would be unlikely that you will get ( SPY ) like returns. If you're an investor looking for that, you'll likely have to look elsewhere. The benchmark " comprises 25% Bloomberg Barclays' U.S. Aggregate Total Return Value USD and 75% MSCI World Net Total Return USD Index."

Distribution - Attractive 8%+ Distribution Rate

The fund carries a distribution yield of 8.31% currently. That works out to a fairly mild 7.18% on a NAV basis. Thanks to a meaningful discount, investors can collect a higher distribution than the underlying portfolio has to deliver. They launched with a monthly distribution of $0.1042, and that is where it remains today.

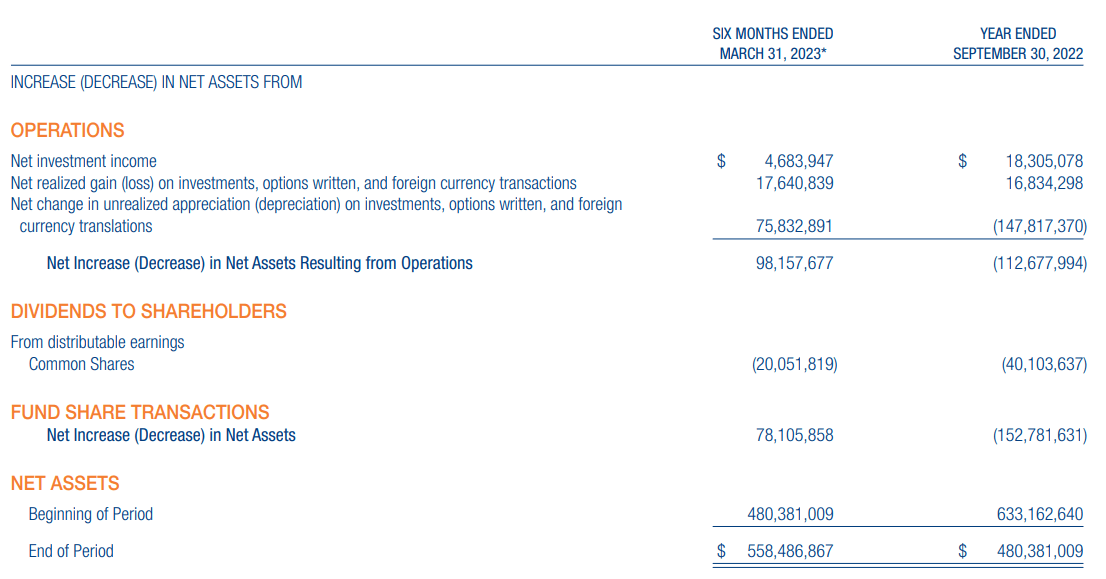

In their latest semi-annual report , we can see that they generated a net investment income coverage of 23.36%. That isn't too shocking, given the sizable weighting to equity positions. Most equity funds and those that invest heavily in equities will require significant capital gains to fund their high distributions.

{kind=link}

NII did drop quite significantly from last fiscal year if this latest semi-annual report were to mirror the next six months. Fiscal 2022 saw NII per share of $0.57, and now we're looking at $0.15 for the last six months or $0.30 if we annualized the current rate. This will be something to watch to see if there can be an improvement. NII isn't the only source required to cover the distribution, but it can help provide more regular support as dividends, and interest payments are generally more predictable than capital gains.

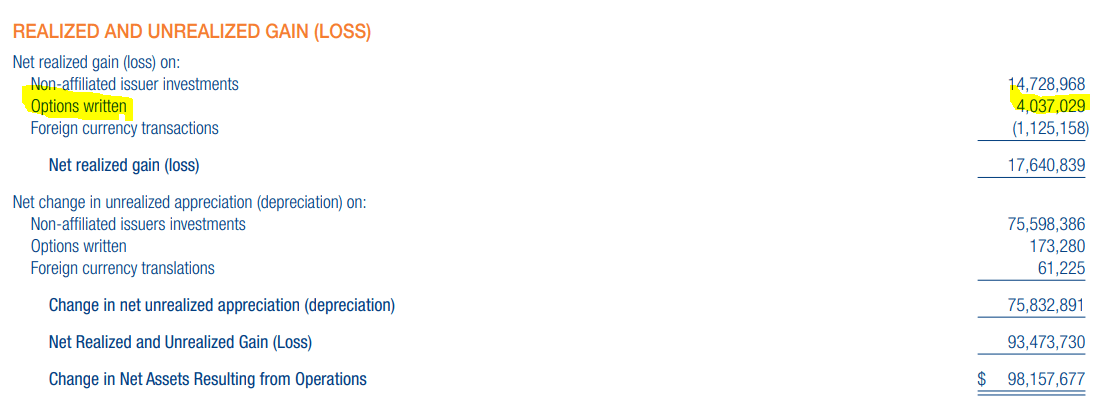

Helping to provide some of those gains was the fund's options writing strategy. Even while they were only overwritten to a small degree, most of the time I've been looking at the fund, they've still generated a meaningful amount of capital gains through this strategy. Losses on foreign currency transactions offset some of those gains. Substantial and the bulk of the gains still came in via the fund's underlying portfolio.

{kind=link}

This is the period that ended March 31, 2023. So we're essentially looking at the fund's results from when the broader market recovery started in October 2022.

Last year they reported that nearly 52% of the fund's distribution was qualified dividends. That can make it tax friendlier.

TBLD's Portfolio

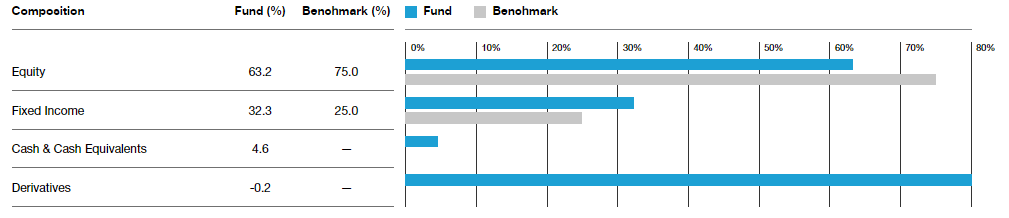

The fund is spread out across both bonds and stocks, with equities comprising just over 63% of the portfolio, with the last update at the end of April 2023.

{kind=link}

The fund reported a low turnover of only around 16% in its last report, so perhaps unsurprisingly, the fund's weightings are pretty steady from when we last updated the fund. This was a slowdown from the prior fiscal year when the fund was more active. Even when the fund was more active, they still saw a fairly consistent weighting going back even further .

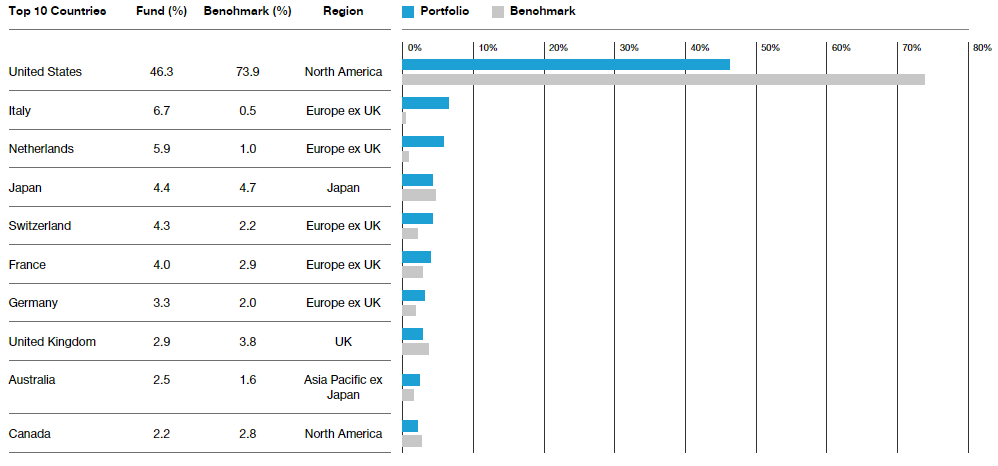

The majority of the fund's holdings are located in the U.S., but it's still at less than 50%. This can be beneficial for some investors who truly want some global diversification. This is somewhat consistent with the weighting in our previous update, but we have seen global exposure pick up as the U.S. weighting had been at 50.5%. Global investments are relatively more attractive than U.S. investments based on valuations . International investments have even been able to start outperforming the U.S.

{kind=link}

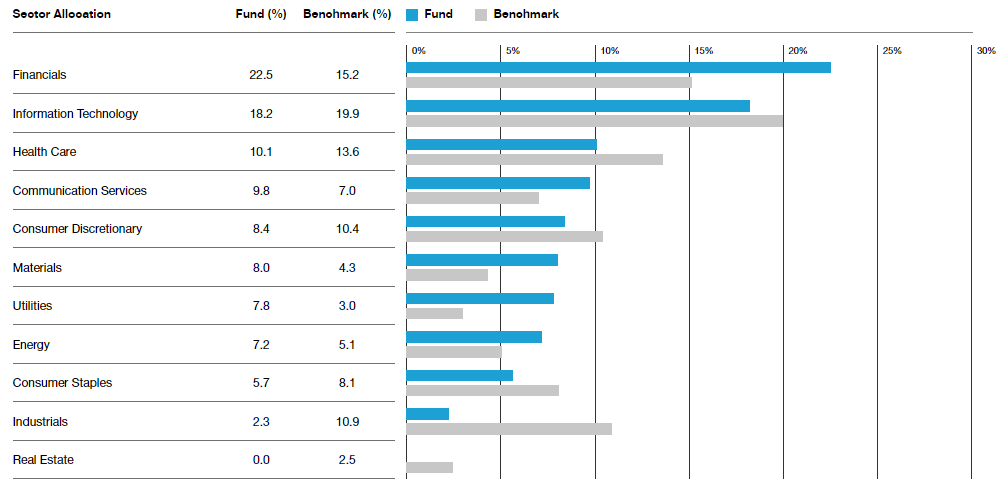

When looking at the fund's sector breakdown, we do have an interesting change to note. While tech and financials were the largest sectors previously, financials have now overtaken as the largest exposure to the fund.

{kind=link}

We know that most financials have been having a harder time due to bank failures. This would suggest that the management had actually been adding to their financial exposure to see this change take place.

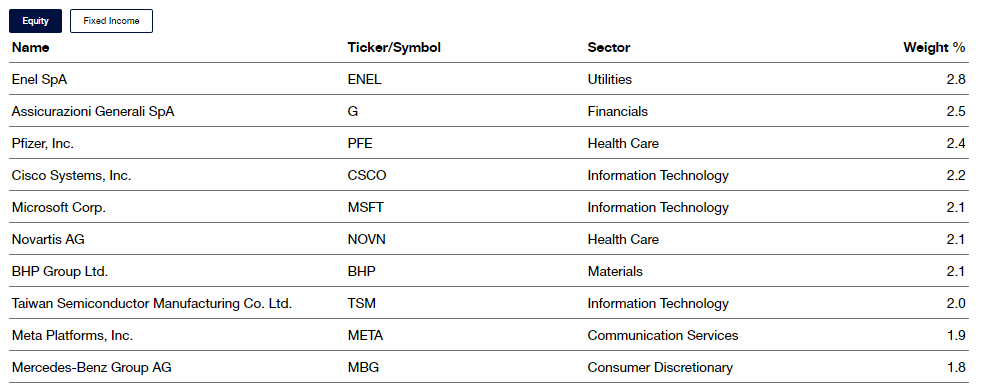

At the same time, the fund only lists one financial holding in the top 10. They carry 190 holdings, so there can be a lot of names under the surface. None of the top positions make up any overly large weighting.

{kind=link}

The forward P/E of the fund's portfolio is 10.9x, and the trailing P/E is 10.4x. That would indicate they are invested in more value-oriented securities. That's even though the tech sector still makes up a fairly meaningful allocation of the fund.

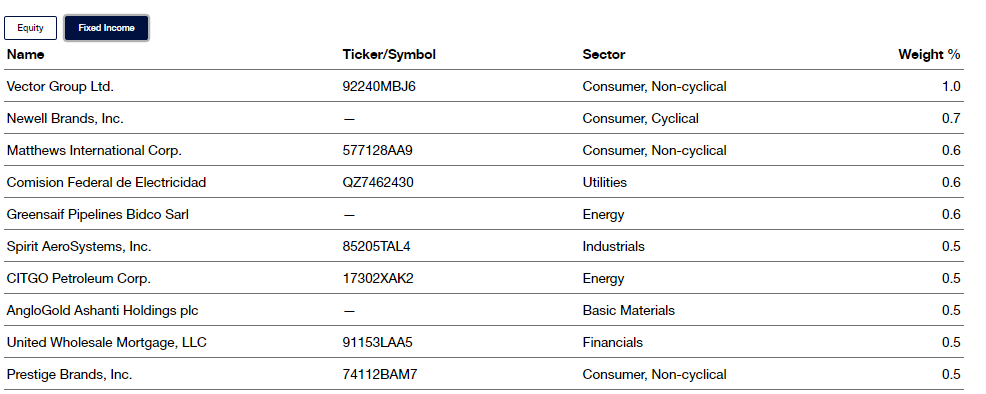

The top 10 fixed-income positions have even smaller weightings to each holding.

{kind=link}

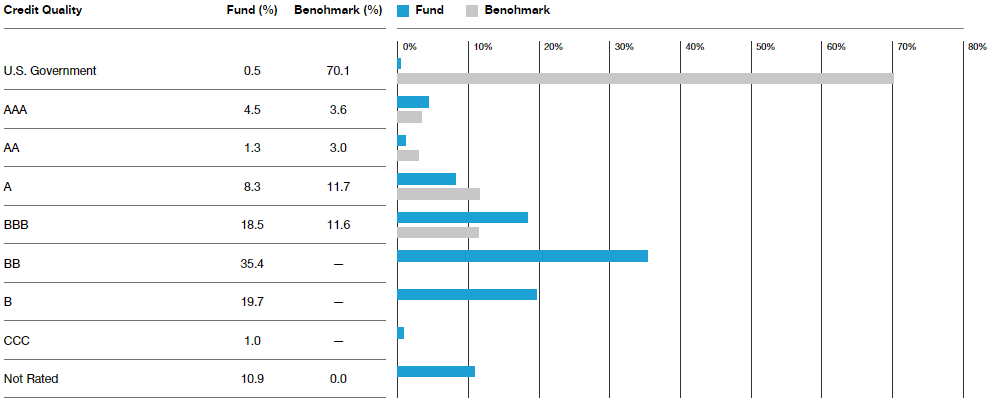

That's also something that is fairly typical when we see a debt portfolio that is weighted toward lower-quality or high-yield bonds. They spread out the number of holdings so each risky position has less of an impact in case it goes bad. Still, the fund carries a meaningful weighting to investment-grade debt too, at around 33%.

{kind=link}

Conclusion

TBLD is a multi-asset fund with tons of flexibility. They invest in income-producing securities, which tend to be mostly large-cap equities but also debt securities of both investment and non-investment grade. The fund doesn't employ any leverage, and that can be a positive in this uncertain environment. The fund's large discount presents an interesting opportunity to consider entering a position. Overall, this seems like a fairly diversified and compelling long-term income investment.

For further details see:

TBLD: A Discounted Income-Producing Focused Fund