TEAF - TEAF: Discount Widens Substantially Making This An Interesting Speculative Bet

2024-01-19 02:25:46 ET

Summary

- Ecofin Sustainable and Social Impact Term Fund is trading at a substantial discount of around 24% to its net asset value per share.

- The fund has a unique focus on infrastructure, including not only your traditional MLPs and pipeline companies but also education and senior living facilities.

- TEAF's performance hasn't been great, but the current discount presents an enticing opportunity, and the monthly distribution can make it easy to hold.

Written by Nick Ackerman, co-produced by Stanford Chemist.

Ecofin Sustainable and Social Impact Term Fund (TEAF) has seen its discount to net asset value per share widen out to particularly wide levels. The fund's discount is pushing to the ~24% area. This fund is quite unique in terms of its infrastructure exposure. The fund positions itself not only in more traditional infrastructure plays, such as MLPs and pipeline companies but also in education and senior living facilities.

They orient the portfolio to these infrastructure plays, but these aren't your usual publicly available investment securities. They have over half their portfolio in private investments. This likely makes it not an investment for everyone but a more interesting and speculative infrastructure play that could be worth considering.

Since our prior update , the fund's performance has been rather poor. This was right before the broader equity market entered into a very brief correction territory in October. The fund started to make a rebound like most everything else, but that quickly faltered.

TEAF Performance Since Prior Update (Seeking Alpha)

The fund's discount widening further was one area that kept this fund's recovery more muted. Simply put, the fund's NAV has been acting much better than the fund's share price. That said, admittedly, the rebound from the October lows has been relatively muted, too, and that definitely played a role in the results.

TEAF Basics

- 1-Year Z-score: -2.81

- Discount: -24.03%

- Distribution Yield: 9.54%

- Expense Ratio: 1.85%

- Leverage: 11.30%

- Managed Assets: $231 million

- Structure: Term (anticipated liquidation date around March 27, 2031)

TEAF was launched with the goal of "attractive total return potential with emphasis on current income and uncorrelated assets." Additionally, "access to differentiated direct investments in essential assets" and "investments intangible, long-lived assets and services." TEAF is also targeting a "positive social and economic impact."

The fund is modestly leveraged, and that can be beneficial in a higher-rate environment. Not only that but given that some of the underlying securities of the portfolio are fairly volatile enough in the energy space, They probably don't need too much more in terms of added volatility. On the other hand, the portfolio isn't all equity investments either; a good portion of their portfolio is invested in fixed-income securities.

The fund's total expense ratio climbs to 2.66% when including the leverage costs. The fund pays rates on its leverage that are based on a 30-day average SOFR plus 0.80%. As of their last semi-annual report , that came in at 5.52% on average and 6.087%. However, that was as of May 31, 2023, though the rate today should be around a similar amount, 6.11%.

The operational expense ratio is already high on its own, but that is often the case with private investments. Often, the advisory fee is higher than the usual standard of ~1%. That's no different for TEAF, which sports the highest advisory fee relative to its sister funds.

{kind=link}

Massive Discount

A sizeable discount on its own doesn't always mean anything, but on a relative basis, TEAF's discount is quite massive here. Its 1-year z-score being close to -3 is generally not something that is seen on a regular basis outside of generally higher volatility.

That said, TEAF has not been in a place of higher volatility, and neither is the overall market. Looking back over the life of the fund, the fund is trading well below its even generally deep discount.

Ycharts

That doesn't mean that it can't get wider, and we even saw that during the Covid pandemic. Additionally, with such high allocations to private investments, there will always be some skepticism. At the same time, I believe that this rather speculative play has moved to a level where the upside reward is definitely worth considering.

Historically speaking, the performance of the fund hasn't been great either. 2023 wasn't any different, adding another mediocre year in terms of performance.

{kind=link}

That said, to circle back to the fund's discount - should the fund even go back to its average discount, one could be looking at a fairly significant upside. That could soften some downside moves or strengthen a potential upside move from here.

The fund is a term fund, and that could add another potential angle despite being so far out. Thanks to the impressive discount at this time, the annualized alpha comes to 3.34%. If the fund liquidates as it should at whatever the future NAV is, this is a guaranteed alpha relative to a non-term fund that would be invested exactly the same. This means that the discount is so large that even with it not coming due for termination until 2031, there is still a meaningful upside potential.

There are, of course, ways for this term to be extended or terminated to switch to perpetual. In addition, guaranteed alpha does NOT guarantee positive performance results. It simply just means that this is what returns would be above and beyond a hypothetical fund that was invested the exact same way but didn't have a termination date.

I think since the very beginning of my coverage on TEAF, I have been mostly consistent with not knowing exactly what to expect. The first article titled on this fund from me was "Unique Opportunity With Unique Risks."

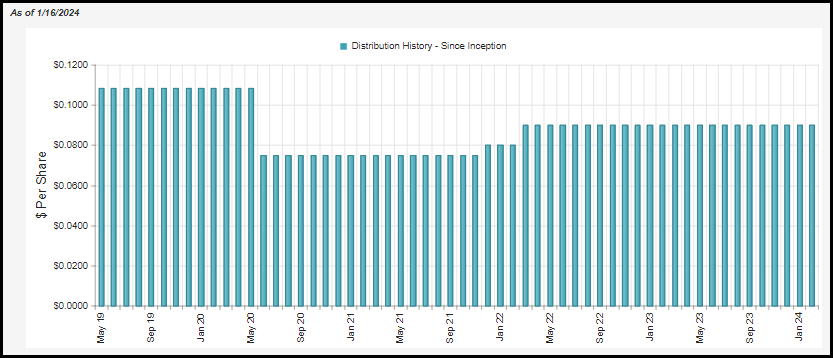

Distributions Along The Journey

Making a potentially speculative play easier to hold to in one's portfolio, I believe, is the monthly distribution. It might not be being earned, as we can see from most of the standard time frames of measurement, but every month, you did get a bit of a liquidation back. If you don't reinvest, which I don't for this fund, then that's basically a return that can never be lost. Once you have some of your investment in cash, that's not money they can simply take back from you.

Thus, in the worst-case scenario, your entire investment can't be lost because you've already taken partial liquidations along the way. To be clear, I don't expect this investment to go to zero. It isn't that speculative, but I could easily see this producing zero total returns in its entire existence (kind of like we already saw, unfortunately.)

Mileage will vary as well depending on when you buy the investment, buying at say, a 24% discount compared to a 10% discount could set one up for a much better future return potential.

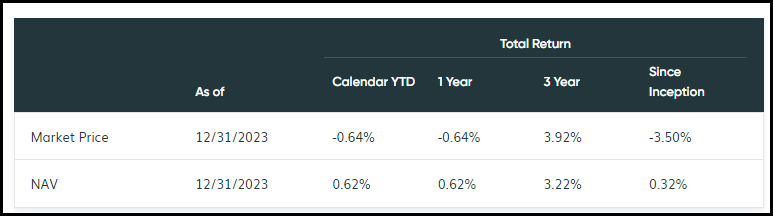

Based on the current rate, the fund pays an attractive 9.54% complement to the sizeable discount to 'juice' it up. On an NAV basis, the rate comes to 7.25%.

{kind=link}

We don't have the next annual report yet, which should be due in a month or so, but we can take a quick look at the coverage discussion in our previous article for a quick recap.

When looking at distribution coverage, one of the first places we would look is at the net investment income.

In this case, we'd see NII coverage come to 29.19%, which is fairly attractive for an equity fund. We would anticipate that capital gains would fund any shortfalls, at least as long as they are investing successfully. However, for a fund that holds energy investments, NII really isn't enough to look at.

Some of the underlying portfolio companies will pay distributions classified as return of capital. These cash flows are subtracted from the NII figure. In the case of TEAF, in the first six months of the fiscal year, they had ROC distributions of $1,217,856. When we include that in the NII, we would get the distributable cash flow ("DCF"), and that provides higher coverage of nearly 46%. Again, that's not bad for an equity CEF, as most coverage isn't even that high.

{kind=link}

Given the above summary of ROC, we will, in fact, see ROC in its distribution classifications. This will be both non-destructive and destructive variety.

With return of capital distributions it receives, it's only natural that some of the distributions that TEAF pays will also be classified as return of capital. This means that not all of the ROC we see in TEAF would necessarily be considered "destructive" ROC.

TEAF Distribution Tax Classifications (Tortoise (highlights from author))

{kind=link}

TEAF's Portfolio

The turnover rate for this fund in the last semi-annual report came to 16.51%, which would have put it on pace to be over last FY's 18.08% rate. However, it would also be down from the FY 2021 and 2020, which came in at 68.31% and 73.22%, respectively.

As mentioned, the fund's unique focus on a broad array of infrastructure and private investments sets it apart. Additionally, the equity and fixed-income investment approach also makes it a fairly unique fund, and it actually has a little bit of exposure to quite a handful of different security types.

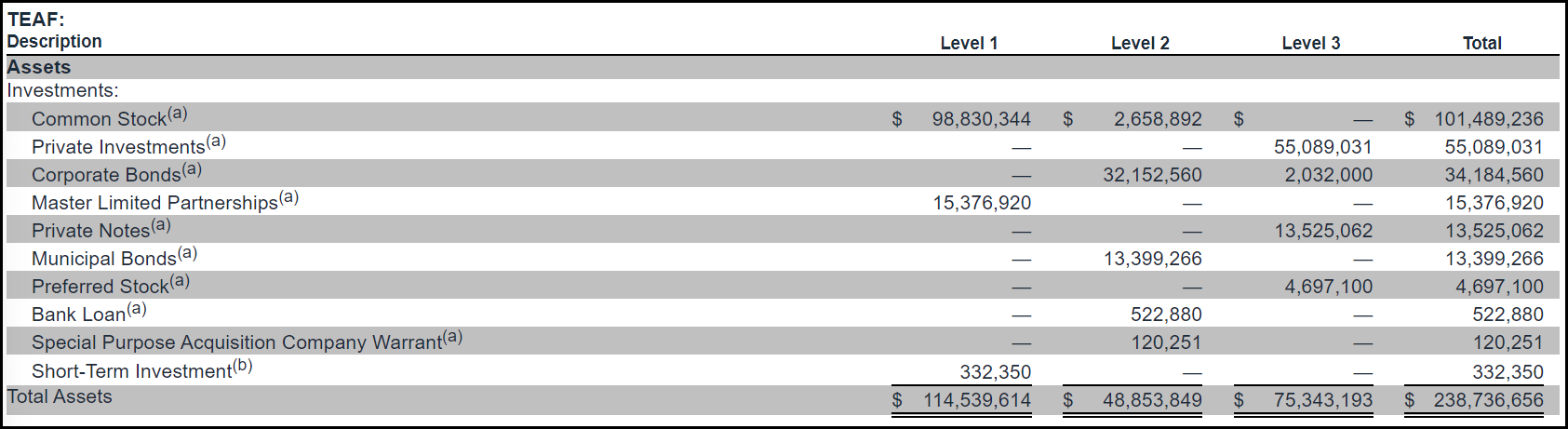

That said, in total, across the various investment instruments, we arrive at around 31.6% of the fund's portfolio in level 3 securities.

{kind=link}

This comes largely thanks to the fund's private investments. The valuations here can sometimes cause some skepticism based on how or how often these fair values are calculated. However, there is more in terms of restricted securities being 45.2% of the total fair value of net assets, as mentioned in their semi-annual report. More recently, private investments are listed as 57% of the fund's total assets, with the rest being public.

{kind=link}

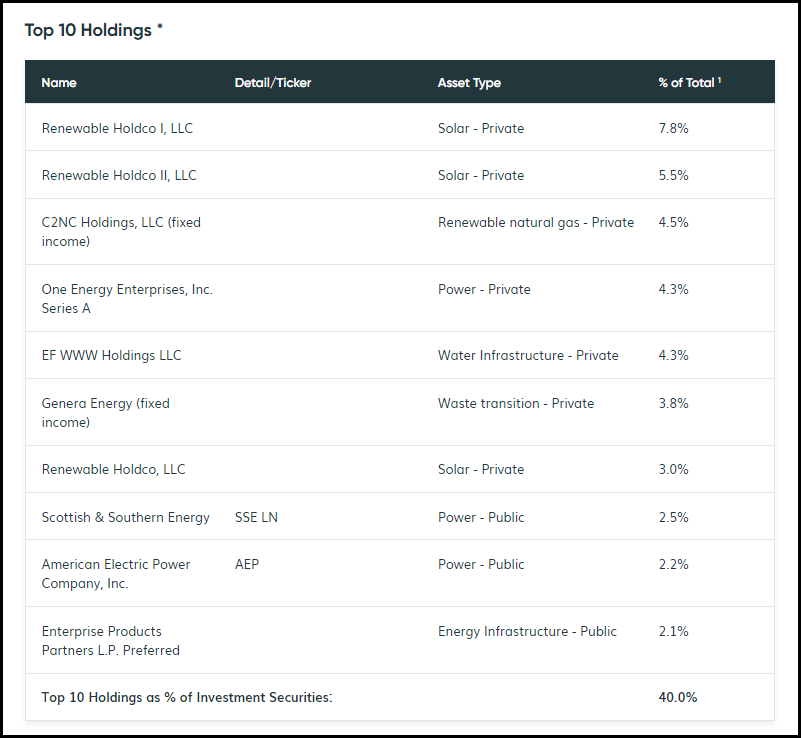

Further, despite the fund's variety of investment instruments, which would seemingly add significant diversification, the fund isn't overly diversified. There is a fair bit of top-ten concentration.

In particular, going back to the private investments. In TEAF, these are largely in several Renewable Holdco entities. These are private solar investment projects.

{kind=link}

Looking further at the acquisition cost versus the fair value, these Renewable Holdco projects seemingly have held up their valuations quite respectably. In fact, we can see these have contributed to some gains in the portfolio.

{kind=link}

Where the caution would be that most publicly traded renewable companies have taken it on the chin in the last few years. To be fair, these are publicly traded equity investments that we are referring to below. They also tend to be more diversified renewable infrastructure plays rather than dedicated specifically to solar.

Ycharts

Additionally, the fair value of the Renewable Holdcos listed above is as of May. The real hit for these companies didn't occur until later in 2023. That's where the next report could give us a better idea of the valuations and the potential changes in valuations we could see.

This is sometimes where some skepticism can come from with such large private investments within closed-end funds. It's not that something illegal is going on, and to be quite clear, the whole formula is laid out on what valuation techniques are being used.

{kind=link}

At the end of the day, though, something is only worth what someone/some entity is willing to pay. They can estimate the value until then, but level 3 securities simply take some guesswork.

Finally, since our last update , the fund has provided investments in another 6 private investments. This was substantial and could have been likely the driving factor in why the private investment sleeve of the portfolio climbed materially since our last update.

Belton Prep was 2 of these, which is a charter school that they had previously invested in April 2023. Though these latest two are materially higher investment amounts than the first. They are also tax-exempt bonds, where the first was taxable.

This wasn't the only charter school that they have more recently invested in either. There was also the City View Charter School, Northeast Ohio Charter Academy and Libertas Academies. Several of these investments were also tax-exempt bonds they were investing in besides the Series B issuances that were taxable in both cases. Given these were all further debt investments, the portfolio could have shifted further into fixed-income exposure.

TEAF's Recent Private Investments (Tortoise)

Conclusion

TEAF is trading at a significant discount to its NAV per share. The fund slumped along with the broader markets in October 2023. The recovery from that level in terms of its underlying portfolio didn't necessarily come back with the same steam as public investments, but even still, the fund's share price was even more muted, and that resulted in a substantial widening of the discount. Now, at such a deep discount on an absolute and relative basis, TEAF looks like an interesting speculative bet.

For further details see:

TEAF: Discount Widens Substantially, Making This An Interesting Speculative Bet