TMVWF - TeamViewer: Assessing The Lack Of Long-Term Potential

2023-08-17 21:30:22 ET

Summary

- TeamViewer is facing a significant growth slowdown and lacks a strong value proposition.

- The remote access industry provides less value due to the development of Cloud-based solutions, and TeamViewer's lack of other related products is also impacting its competitiveness.

- TeamViewer's billings are flatlining, its ASP in the Enterprise segment has declined, and churn is increasing. This will impact ARR improvement in the coming 5 years.

- Margins are also under threat, although are currently quite attractive, alongside cash flows. This should support aggressive buybacks.

- Although M&A remains a key uncertainty, we consider TeamViewer overvalued currently.

Investment thesis

Our current investment thesis is:

- TeamViewer operates an attractive business model but we believe the company is facing a significant growth slowdown. We are struggling to see the value proposition of a mass-market standalone remote access software given the developments in cloud-based and remote collaboration solutions.

- Further, businesses/consumers are more inclined to favor software that is packaged alongside other solutions (again a lack of value proposition from TeamViewer), allowing for greater integration into a company's operations, contributing to upselling opportunities and low churn.

- The company's financials are showing a concerning trend. Margin improvement and growth are softening, with the expectation that this continues in the coming 5 years.

- TeamViewer does have some very attractive qualities, such as high cash flow generation and high margins, which could mean a future takeover or a consistent period of share buybacks.

Company description

TeamViewer AG ( TMVWF ) (TMVWY) is a global software company based in Germany. It specializes in remote connectivity solutions, enabling users to access and control computers and devices remotely, facilitating remote support, collaboration, and virtual meetings.

Share price

TeamViewer's share price performance has disappointed since it was listed, losing over 50% of its value while the S&P and Technology sector have achieved strong growth.

Financial analysis

TeamViewer's financials (Capital IQ)

Presented above is TeamViewer's financial performance.

Revenue & Commercial Factors

TeamViewer's revenue growth has been impressive, with a CAGR of 31% in LTM Jun-23. Growth has been incredibly strong during this short period but at a far lower level than this 31% (biased by the performance in FY18 and FY19). Growth is seemingly slowing, with LTM shaping FY23 to be slightly below FY22.

Business Model

TeamViewer's primary offering allows users to remotely access and control computers and devices from anywhere, facilitating remote IT support, troubleshooting, and collaboration.

In addition to remote access, TeamViewer provides tools for online collaboration, including screen sharing, video conferencing, file sharing, and chat features. This is part of a wider diversification exercise to create an ecosystem for remote/virtual working.

TeamViewer operates on a subscription-based licensing model. It offers different tiers of subscriptions for individual users, businesses, and enterprises, with varying features and pricing levels.

The subscription model is superior, as it allows the business to focus on growing its user base, with greater comfort over forward revenues as subscriptions unwind, assuming the service is sufficiently attractive to ensure minimal churn.

Our view on the business model is that it is quite competitive in the current landscape and provides a service that historically has been incredibly desirable for a number of use cases.

Key financial metrics

TeamViewer's business is broadly assessed between its SMB and Enterprise clients.

SMB's revenue growth has been well below the company's current average growth rate, falling below 10%.

SMB Revenue growth ( TeamViewer )

Quarterly billings have grown at a reduced rate to prior years, with lumpy growth, particularly in FY22. This has improved somewhat in FY23, although when considering QoQ absolute billings, we are seeing a material slowdown.

Quarterly billings ( TeamViewer )

The driver of this has not been ASP, which has grown well since FY22. This has been achieved through a strong focus on upselling and achieving improved economics from SMBs, likely due to the slowdown in revenue.

Subscription growth on the other hand has been mild, with YoY improvement distorted by exceptionally low levels in FY22.

SMB ASP / Subscriptions ( TeamViewer )

The lack of material improvement in the SMB segment is due to what we consider to be high churn. Subscriber churn has gradually increased in recent quarters, reaching 15% in Q2. This is far too high for a high-quality growth business, even if the segment is more volatile (particularly during such economic conditions). This calls into question the attractiveness of the product relative to peers, and also how easy it is to switch to competitors.

SMB Churn ( TeamViewer )

Moving onto Enterprise, top-line growth is far better, although is slowing QoQ. This strong growth is a reflection of a focus on this segment, which is generally more lucrative (due to contract sizes) and less volatile due to the security of businesses.

ENT Revenue growth ( TeamViewer )

Billings have been equally volatile (which is not unusual for tech businesses), with a concerning decline in Q1 and a mild bounce back in Q2. This again implies future revenue will slow, particularly because the levels achieved in late 2022 (which will translate to revenue in 2023) are substantially greater.

ENT Billings ( TeamViewer )

The declining revenue and billings profile is a reflection of softening ASP, which has fallen from the company's Q2-22 level. Thus far, this has been offset by strong customer growth, with Management seeking to increase its customer base.

Enterprise ASP / Subscriptions ( TeamViewer )

This strategy has some merit, as TeamViewer can focus on future ASP improvement through upselling, relying on the quality of its product to keep customers around once they try it. This makes us very nervous, however, as the business has shown a high churn level in SMBs and growth in customers already slowing QoQ. Management does not disclose ENT churn but instead "Net Retention Rate" (NRR), which allows upselling to offset customer losses. This metric has declined from FY22, driven by what looks to be ASP primarily, but almost certainly an uptick in churn also, given the small movement in ASP and the high customer growth (which we assume will be at a higher average price to its existing customer base).

Enterprise net retention ( TeamViewer )

The net of these factors is an LTM ARR ("Annual Recurring Revenue") of $626.2m (+13%) and an NRR of 109%. We are very concerned about how TeamViewer's financial metrics have developed in the last year. To be clear, its growth remains in low double-digits and based on LTM ARR, will likely land at a YoY FY23 growth rate of 10-13%.

The key concerns for us are:

- Increasing churn which suggests, either customers are not wholly happy with the product, or are able/wish to shop around, or are taking advantage of the ease to which they can "untangle" TeamViewer's services from their operations and transfer across to competitors.

- Lack of ENT ASP development. It has yet to be seen if upselling can begin offsetting this following a large increase in customers but we are not confident.

- Inconsistency of billings. We are not seeing a clear directional improvement in billings, regardless of volatility.

Competitive Positioning

Over the years, the market for remote desktop and collaboration tools has become increasingly saturated with various competitors offering similar services. The industry has become somewhat "commoditized", with limited differentiation capabilities beyond widening the breadth of services. From our research, there are over 5 strong alternatives to TeamViewer's services, as well as a free option from Google ( GOOG ).

One of the big two issues we have with the business model, however, is the lack of ecosystem (we concede that TeamViewer has multiple products but it is essentially reliant on remote access). In a highly competitive industry, the ability to remain attractive is dependent on enhancing the value proposition. A classic example of this is Amazon Prime (AMZN). Amazon continues to bundle services into Prime to ensure they can justify further price hikes and sticky subscriptions. No single service within Prime is a monopoly, they all face heavy competition and in isolation, would struggle to compete (E.g. Prime Music). The issue we see with TeamViewer is that this is a standalone subscription which on a cost basis is difficult to justify. Further, it leaves the business limited scope for upselling beyond the number of users.

The other issue we have is the idea of remote access has fundamentally changed. The collaboration benefits in particular have materially diminished following the widespread integration of cloud-based solutions. The solution-based benefits are limited when you can easily upload files to the cloud, as well as access anything live alongside colleagues. This can all be done with a cheaper subscription via Microsoft Office ( MSFT ). This is not to say the industry is obsolete, many large businesses will continue to use this for troubleshooting and there is a range of other cases, just smaller in our view.

The COVID-19 pandemic accelerated the adoption of remote work tools. However, as work patterns evolve, organizations may shift to hybrid work models or adopt other collaboration tools, impacting TeamViewer's growth trajectory. This is likely a factor contributing to growth slowing.

Due to the competition issues, acquiring new customers and retaining existing ones requires continuous marketing efforts, customer support, and adaptation of the service. Unlike most tech businesses, TeamViewer's S&A spending as a % of revenue has increased during the historical period, illustrating this.

Margins

TeamViewer's margins have declined during the historical period but remain at an attractive level, with an EBITDA-M of 33%. GPM has naturally improved with scale, one of the key characteristics of a SaaS business (low marginal cost to provide an additional service), while S&A spending has offset this for the reasons discussed above.

Our expectation for margins is broadly uncertain, but we see it normalizing (at an EBITDA-M level) between 25-35%. This target is clearly very broad and is a reflection of the uncertainty around how the business will develop in the coming years. If subscriptions can continue to grow, we suspect upselling activities/price hikes will too, contributing to margin appreciation. Conversely, if this growth continues to slow, it is likely margins will rapidly soften and potentially decline.

Balance sheet & Cash Flows

One of the key threats to our thesis is the strong cash flow generation of TeamViewer. With limited debt and a streamlined operation, the majority of its profitability directly translates to cash.

Given the limited investment in Capex and R&D, we see Management capital allocation strategy to focus on shareholder distributions, which means aggressive buybacks. This will support the share price and potentially attract investors seeking an attractive short-term yield.

Industry analysis

Systems Software (Seeking Alpha)

Presented above is a comparison of TeamViewer's growth and profitability to the average of the Systems Software industry, as defined by Seeking Alpha (17 companies).

TeamViewer performs well financially when compared to the group of profitable peers. The company has achieved marginally superior growth in the shorter time frames, while margins are substantially better.

The weakness of TeamViewer relative to this group is the commercial concerns. This group includes businesses such as Oracle ( ORCL ), Qualys ( QLYS ), Microsoft, Palo Alto Networks ( PANW ), Fortinet ( FTNT ), and CrowdStrike ( CRWD ). These are all businesses with a significantly wider moat and a longer growth trajectory. For this reason, we believe a noticeable trading discount is required to reflect the commercial weakness.

Valuation

{kind=link}

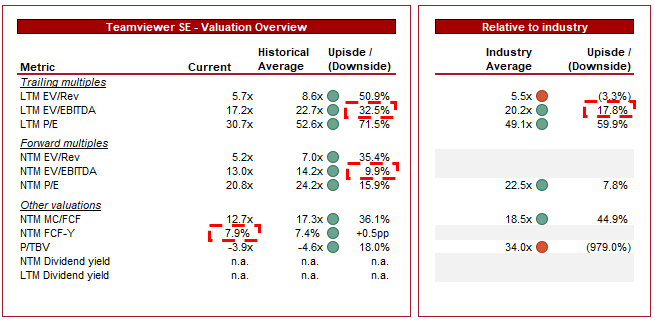

TeamViewer is currently trading at 17x LTM EBITDA and 13x NTM EBITDA.

This valuation represents an FCF yield of 8%, an attractive level given this is being directly committed to distributions. This also implies a discount to its historical average, which is not the most useful metric given the short history and rapid multiple contraction as profitability improved.

Relative to its peers, TeamViewer is trading at an 18% premium on an LTM EBITDA basis and an 8% NTM P/E basis relative to its peer group. This discount is not sufficient in our view, particularly due to the commercial weakness. Analysts currently have a target downside of (1.4)% ( Source: Capital IQ ), supporting this view.

M&A

In addition to heavy buybacks, another key risk to our thesis is a takeover. Firstly, TeamViewer's strong profitability and cash flows mean it is value accretive for most software companies. Secondly, it would fit perfectly with a business that offers a suite of business-focused software solutions (bundling remote access, similar to the Prime example above), such as SAP ( SAP ), Microsoft, Intuit ( INTU ), or many others.

Final thoughts

TeamViewer has provided a great service for many years. I used its software many years ago but like many, I see no reason for it today. We suspect the business will see a rapid slowdown in growth in the next 5 years, falling to single digits with issues improving ASP. At this point, the company's margins stagnate, and potentially decline, deteriorating the value proposition.

This sell rating is still slightly harsh despite this, as the business is generating strong cash flows and is a good takeover target.

For further details see:

TeamViewer: Assessing The Lack Of Long-Term Potential