TMVWF - TeamViewer: Manchester United Exit Is A Positive Step But May Not Be Enough

Summary

- TeamViewer has negotiated a potential exit from its front shirt sponsorship deal with Manchester United.

- Finding a replacement sponsor willing to match the >EUR50m/year terms will be challenging, though, and any P&L benefit could be delayed.

- The stock isn’t cheap heading into an uncertain Q4/FY23; I remain neutral.

Connectivity platform TeamViewer ( TMVWF ) recently disclosed a potential exit from its Manchester United ( MANU ) sponsorship deal, offering the club buyback rights to the shirt sponsorship should it successfully land a replacement sponsor. On paper, drawing the line on what has been a dilutive marketing contract marks another positive step by the new CFO in optimizing the financial profile. Whether the club can find an alternative sponsor is another matter entirely; given the ongoing pressure on marketing budgets amid a macro/consumer slowdown, I would hold off on underwriting a full P&L impact anytime soon.

In the meantime, management’s reiterated FY22 guidance could still see downside heading into Q4 amid headwinds from a post-COVID demand slowdown for remote solutions, as well as higher competition across its predominantly small/medium business client base. TeamViewer is pinning its hopes on price hikes in Q4 2022, but given the price-sensitive nature of its clients, the company could see higher churn as well. At ~8x fwd EBITDA (~17x trailing), this is still priced like a growth stock, and any disappointments ahead could lead to a further de-rating.

Costly Manchester United Sponsorship Agreement Revised

TeamViewer ended 2022 with a brief release announcing it had reached an agreement with Manchester United for an added buyback option related to its shirt front sponsorship rights. Recall that back in 2021, when a COVID-driven demand spike had driven record profit growth, the company had embarked on a strategic global marketing push, including a costly marketing partnership with the English Premier League football club. While the sponsorship may have increased brand awareness since then, the cost-benefit has been hard to justify. With the company revising its EBITDA margin guidance lower throughout 2022, investor sentiment has reached new lows, as reflected in the falling stock price and multiples.

With the introduction of new CFO Michael Wilkens last year, TeamViewer appears on course for a reversal of the ‘growth at all costs’ strategy. This latest release is his most important move yet, allowing the company to be released from a massive >EUR50m/year sponsorship obligation should the club find a replacement sponsor. The company will remain a part of the Manchester United partner ecosystem, though, given the original contract agreement stipulates a five-year term from the 2021/2022 season.

A Potential P&L Boost but Near-Term Impact Likely to be Limited

The latest revision could lead to a substantially reduced partnership expense - from a total annual run-rate spend of >EUR50m, the company could eventually see a reduction to <EUR10m/year (a “single-digit USD million” amount per management). So, while TeamViewer will not fully exit from this contract post-revision and will still be a sponsor until the end of 2026, its margins should benefit accordingly. The catch is that the company remains on the hook until Manchester United finds a new sponsor. My expectation is that signing on a new shirt front sponsor at similar financial terms won’t be easy, given the current economic backdrop is likely pressuring marketing budgets across the globe. In a best-case scenario, TeamViewer could exit in H2 2023, though a more realistic scenario would be sometime in FY24/FY25, in my view.

{kind=link}

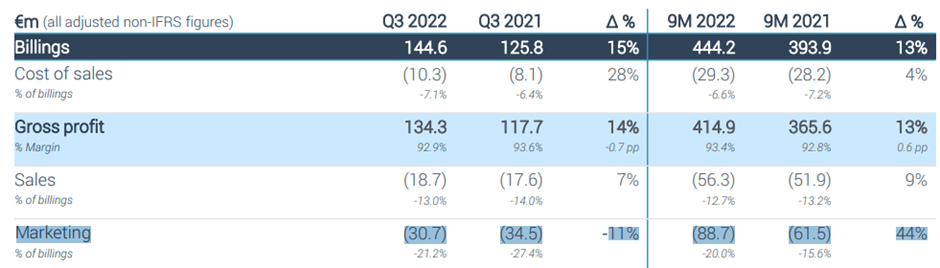

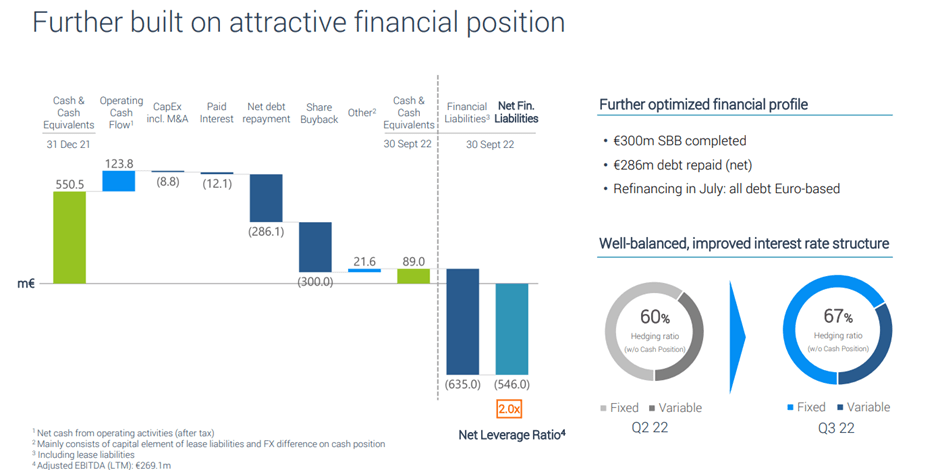

More broadly, I view this announcement as a positive signal of intent by the new CFO. The Manchester United sponsorship, while promising, has had little discernible impact on growth despite the major marketing costs. In effect, this was a value-destructive expense, and thus, this exit will be well-received by investors heading into a challenging operating environment ahead. Having recently ended the EUR300m buyback program and completed ~EUR286m of debt repayment as well, the company has bought itself some extra breathing room. With the cash balance running low, though, there remains ample work to be done, particularly on the cost side. Recent cost containment measures under Project ReMax and further cuts to marketing expenses should help in this regard.

{kind=link}

More Price Hikes on the Horizon, but Elasticity is a Concern

Heading into Q4, usually a seasonally important quarter for the company, the unchanged FY22 guidance and growing economic uncertainties in TeamViewer’s key regions leave estimates vulnerable to downward revisions. To recap, management has guided for EUR565m-580m of revenues (up mid-teens % YoY) on the back of ~EUR630m of billings. Embedded in the guide is the assumption that higher than anticipated price increases will benefit the P&L. Management believes its customer base is more ‘sticky’ than before and is, thus, open to paying more for value-add.

I am less certain about a favorable outcome – with inflation at multi-year highs, its customers (mainly small/medium businesses) likely have limited room in their budgets for price increases, and the result could instead be additional churn. Pending visibility into customer acceptance in Q4, I would hold off on underwriting the FY23 outlook.

Manchester United Exit is a Positive Step but May Not be Enough

TeamViewer’s new CFO has been making all the right moves in recent months, with the planned exit from a >EUR50m/year Manchester United sponsorship deal via a buyback option representing another positive step. The full savings likely won’t flow through to the P&L for a while, though – a sponsor replacement on similar terms will be challenging, given the ongoing macroeconomic challenges and pressure on marketing budgets.

This leaves the full-year guidance vulnerable to competition and slowing post-COVID demand for remote solutions as more workers return to the office. To mitigate these headwinds, management is pushing through price hikes in Q4 across a price-sensitive client base. Whether this increases churn into FY23 is the key unknown here, particularly with the stock still priced for growth at the current EV/EBITDA multiple; pending better visibility, I remain neutral.

For further details see:

TeamViewer: Manchester United Exit Is A Positive Step But May Not Be Enough