TMVWF - TeamViewer: Manchester United Out Of The Picture (Rating Downgrade)

2024-01-12 18:03:02 ET

Summary

- TeamViewer SE expects reduced marketing spend from the Manchester United partnership, leading to significant savings in 2024 as it terminates that deal.

- The company's AR solution, Frontline, is still in the early stages, but shows promise for future growth and continues to generate enterprise interest.

- TeamViewer's valuation is favorable with decent cash flow yields and profitability tailwinds from the unwinding of the Manchester United partnership. A quite surefire pick.

TeamViewer SE ( TMVWF ) should see incremental benefits from reduced Manchester United plc ( MANU ) related partnership spend in marketing. Frontline is apparently still also in its early innings. It takes time for the initial trials for their AR solutions to result in more scaled orders, but the SAP and other channel partnerships seem to be working out. On the valuation side, things look decent, with free cash flow ("FCF") yields at around 10%. Not a bad pick.

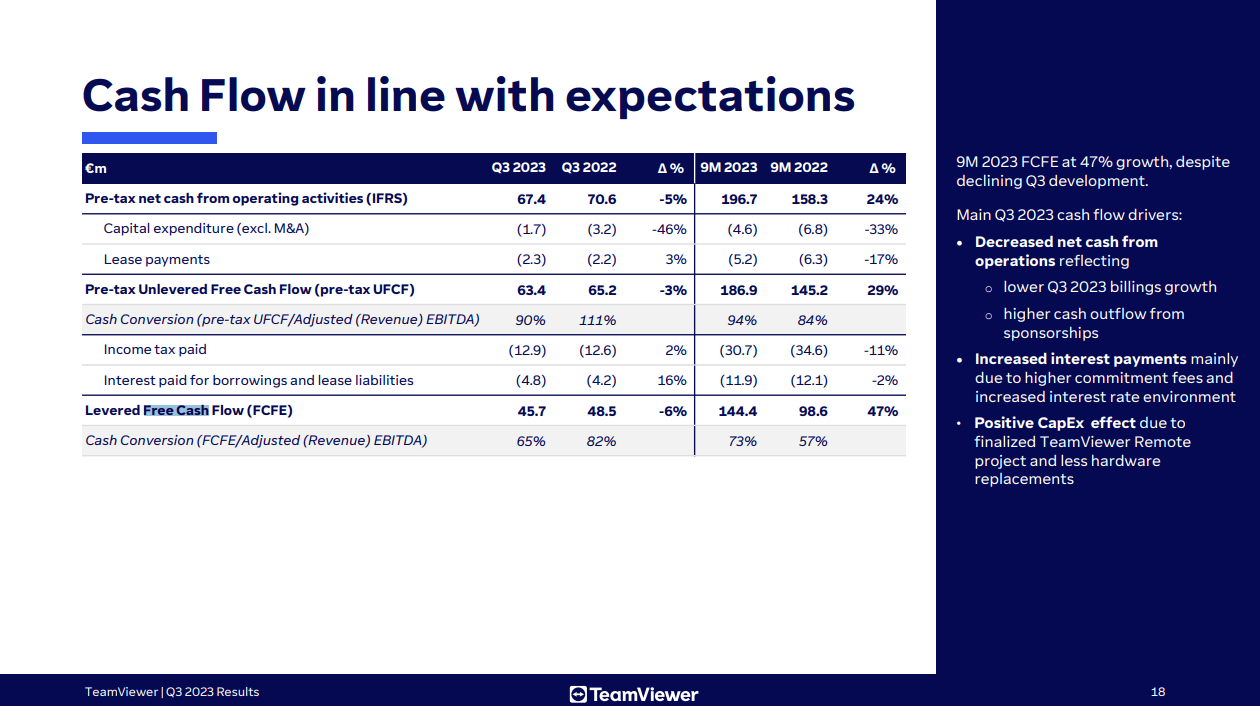

Q3 Earnings

We now communicated that from the start of the 2024-2025 season, so mid next year, we will see a reduced level of marketing spend for the Manchester United partnership.

The MANU partnership accounts for the majority of their current marketing budget, which is in turn around 20% of revenue , so a massive needle-mover. However, some of these savings will be invested in alternative marketing and product development activities, so while it matters it won't be a full savings benefit.

As we said before, we will invest some of the savings in other branding activities and other marketing activities, and of course, also in our product.

Oliver Steil, CEO.

Nonetheless, any dial-down in marketing expenses will obviously benefit profit, although the major benefit will come when the partnership expires in a couple of years' time.

The expected benefit in 2024 is going to be around 17 million EUR in savings, which is around 6% of the annualized adjusted EBITDA, so substantial. Those savings double in 2024.

Markets always hated this MANU deal, worth around 50 million EUR annually in marketing expenses. The dial-down in marketing expenses has to do with a mutual agreement to terminate the agreement in the coming seasons. This is great news for the company's profits and is one of the big reasons why the stock is likely being rediscovered by analysts and performing well.

On Frontline, the AR solution, they made some breakthroughs in previous quarters, but it's mostly at the pilot stage, and the real needle-moving activity has yet to happen.

And we do see the interest we see traction. It just takes a longer while and then customers try the solutions, there's a proof of concept. And then from there, it scales. So early days, and we're very, very positive on these partnerships, but we also need to be patient there.

Oliver Steil, CEO.

Nonetheless, we think that around 10-15% of EBITDA is coming from AR based on figures from a few years ago. It would have grown in the meantime since the company reported in previous quarters that that's where the billing activity was concentrated. It's not insignificant.

Conclusions

TeamViewer still looks like a decent proposition. It is able to finance the development of AR without much issue, both on the business and R&D side and produce substantial free cash flow yields at around 10% for the company based on annualized figures.

{kind=link}

While there are signs of deceleration with general macro pressure - indeed the sales growth is 10% YoY for the 3 months while 12% for the 9 months, and surprisingly North America was the weaker geography with negative billings - a 10% FCFY is low for a growing company with quite a lot of secular theses in its favor.

The other regions, namely APAC, are performing nicely. This is again on some adoption of a Frontline solution called Vision Picking. Enterprise (larger ticket) continues to lead in billings growth at 13% to the small and mediums at 11%.

In all, TeamViewer SE has a pretty compelling valuation. There are good cash flow metrics, a growth story still outstanding with Frontline, and also major profitability tailwinds with the unwinding of the Manchester United partnership. These all spell a good coming set of quarters for TeamViewer. However, general macro pressure, especially on industrials, is something we are a little worried about as far as the Frontline solution garners uptake.

For further details see:

TeamViewer: Manchester United Out Of The Picture (Rating Downgrade)