AMX - Telecom Argentina: Improvements Don't Justify Its Premium Valuation

2023-10-27 10:24:00 ET

Summary

- Telecom Argentina has faced challenges in recent years due to the Argentine debt crisis and increased competition in the telecommunications industry.

- The company has managed to offset some costs despite extreme inflation levels in Argentina, and its leverage situation has improved.

- The valuation of Telecom Argentina remains elevated compared to its peers in Latin America, as indicated by the high multiples in forward P/E, EV/EBITDA, and Price/Cash Flow ratios.

Telecom Argentina ( TEO ) is a telecommunications company with over 30 years of operation in Argentina. The company has undergone significant changes, from enjoying legal monopolies in some regions for fixed telephone and broadband services to becoming a "quadruple-play" telecommunications provider, offering fixed telephone, broadband, mobile, and paid TV services.

Historically, Telecom experienced robust growth with solid financial performance, achieving an ROIC above 20% for a decade. However in 2018, the company faced challenges due to the Argentine debt crisis, leading to a significant drop in its stock price.

The telecommunications industry in Argentina has witnessed transformation, with technological advancements and the elimination of monopolies. Telecom's merger with Cablevision in 2018 aimed to address these changes, resulting in increased depreciation charges impacting the company's earnings.

The company competes in a highly competitive market where consumers are not necessarily loyal, switching providers to access discounts. Regulatory changes, such as declaring telecommunications an essential service and price increase restrictions, have further impacted profitability in the last couple of years.

The outlook for Telecom's future earnings is uncertain, with revenue recovery dependent on various factors, including regulatory decisions, especially in a hyperinflationary scenario in Argentina's economy. In an optimistic scenario with price increases, the company may generate profits, but the conservative value range suggests caution due to regulatory uncertainties and challenges in achieving a significant upside.

A Comprehensive Overview of Telecom Argentina

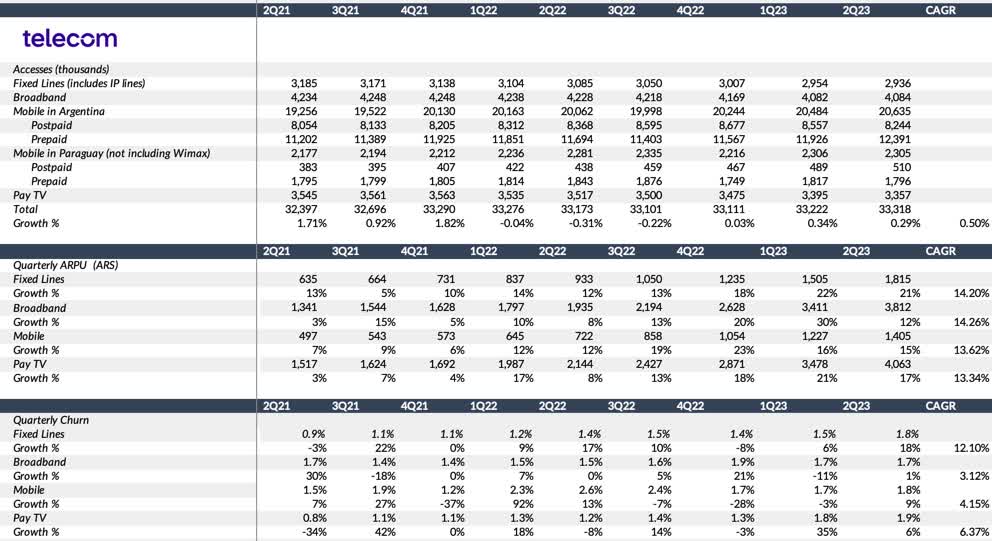

According to its most recent report , Telecom Argentina derives most of its revenue from mobile lines within Argentina, constituting 62% of its total revenue, with 60% originating from postpaid services. Broadband services contribute 12% of the total revenue, Pay TV accounts for 10%, fixed lines make up 9%, and mobile lines in Paraguay contribute a smaller share at just 7%.

The last three years have presented significant challenges for Telecom Argentina, with a noticeable decline in revenue. This downturn has consequently hurt the company's operating income and cash flow from operations.

Part of the company's struggle to generate revenue can be attributed to its difficulties expanding its customer base. Over the last two years, Telecom Argentina has experienced minimal growth, with an average increase of just 0.5%. However, it has managed to maintain an average ARPU growth of 14% across its various segments, which is a positive sign, though it falls short in the face of the country' s hyperinflationary environment . Notably, churn rates have remained low, especially in its primary segment, mobile, with an average of 4% over the past two years. This suggests that while the company has not significantly increased its customer base, it has successfully retained many existing customers.

{kind=link}

Company's data, compiled by the author

When examining Telecom Argentina's profitability, the last two years have witnessed a significant decline in its EBITDA, which has reached negative levels. This decline is attributed to reduced revenues and escalating costs, primarily due to the prevailing hyperinflationary conditions in Argentina. Additionally, the company has experienced an increase in its leverage. Notably, Telecom Argentina's debt-to-equity ratio exceeded 2x last year, indicating a substantial level of debt relative to the company's net worth. However, the company has subsequently managed to reduce this ratio to 1x as of today.

Due to its challenging financial position in recent years, Telecom Argentina has faced constraints on its capital expenditures (CapEx), which have also impacted the quality of services offered, resulting in stagnant company growth. In terms of CapEx, the company has devised a flexible plan where it has been making investments significantly exceeding its sector's typical and average CapEx-to-revenues ratio in recent years. Most of the company's CapEx is earmarked for investments in its access network and technology, primarily focusing on enhancing its infrastructure.

When examining Telecom Argentina's cash flows, it becomes evident that despite the challenges faced in recent years, cash generation remains strong, although declining. The positive free cash flow signifies a healthy financial position for the company.

Telecom Argentina's Results for the First Half of 2023

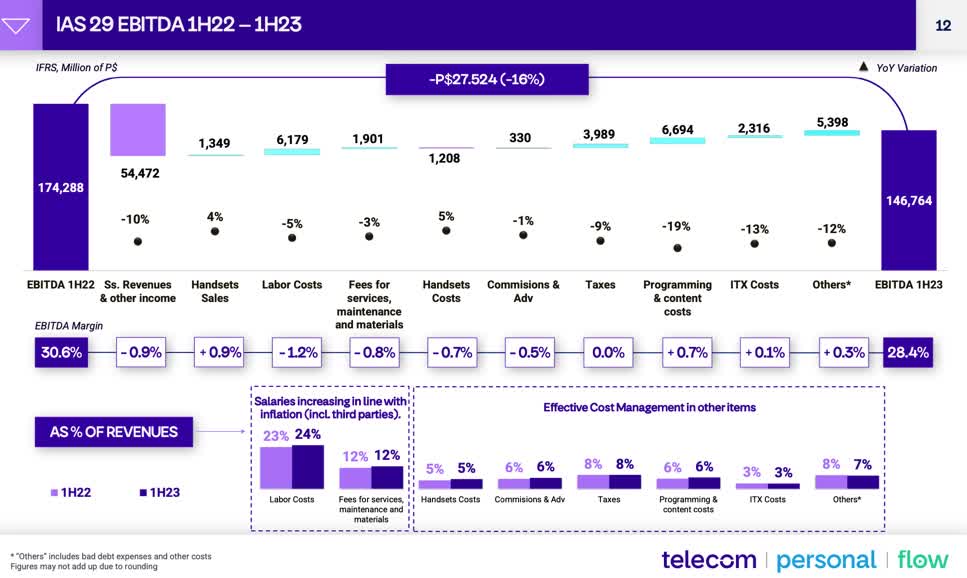

During the first half of 2023, Telecom Argentina attained an EBITDA margin of 28.4%, showcasing successful cost containment efforts, even in the face of labor cost pressures. In the past year, CapEx amounted to $655 million, equivalent to 16% of revenues, focusing on expanding the FTTH network. Strong cash flow generation led to approximately $308 million in free cash flow before factoring in dividends and interest payments, marking a $52 million improvement in the same period in 2022.

Telecom's IR

The company has responded to increasing inflation by implementing more frequent price increases, leading to service revenue remaining relatively stable in real terms year-over-year. Additionally, the mobile subscriber base saw an almost 3% year-over-year increase and a 15% growth in mobile data usage. The primary focus within the broadband sector has shifted towards FTTH technology, resulting in customer base stability and outpacing other technologies, while the HFC network has remained consistent.

How Is the Company Coping with Hyperinflation

Argentina is currently navigating a challenging chapter in its economic history, with its citizens contending with a complex situation brought on by the devaluation of the Argentine peso and soaring inflation. Over the last 12 months, inflation has increased to 138%, leading to a cost of living crisis that has left 40% of the population in poverty.

Telecom Argentina maintains its accounting records and prepares financial statements in Argentine Pesos (USD:ARS), its functional currency. The company manages the risk of ARS devaluation by periodically engaging in Dollar-Linked Financial Instruments (DFI) agreements and futures contracts to hedge some of its exposure to foreign currency fluctuations. Despite these risk mitigation measures, Telecom Argentina remains significantly exposed to the volatility of the Argentine Peso.

The depreciation of the Argentine Peso can have several consequences, including the impact on the company's capital expenditure program. Furthermore, it can increase the ARS equivalent of its trade payables and financial debt denominated in foreign currencies. As of the end of 2022, approximately P$443,099 million of the company's liabilities were denominated in foreign currencies, constituting about 35% of the company's total liabilities.

Amid this chaotic backdrop, Telecom Argentina, in my opinion, has adeptly managed its cost structure to mitigate the impact of rising costs attributed to the inflationary environment. During the second quarter of 2023, the company maintained its margins, holding them steady compared to the previous year's period. This suggests that their pricing and cost management strategies are on the right track.

This accomplishment becomes evident when examining Telecom Argentina's EBITDA year-over-year performance in the first half of the year and the influence of various components on revenues and costs. Throughout the first half of 2023, the company managed and contained the impact of inflation on most of its cost categories, as many of them either decreased or remained in line with the inflation rate.

{kind=link}

Telecom's IR

Most of Telecom Argentina's year-over-year margin contraction can be attributed to labor costs, people services, maintenance, and materials changes. The rise in contractor salaries also impacts these costs. In the first half of 2023, these costs accounted for 36% of revenues, compared to almost 35% in the first half of 2022. This increase in cost, while still evolving below the inflation rate for this quarter, highlights the effective cost-management efforts made by the company.

A Stretched Valuation Difficult to Justify

Although Telecom Argentina remains in a precarious financial situation, it continues to command significantly high valuation multiples compared to its primary competitors and other telecommunications firms in Latin America.

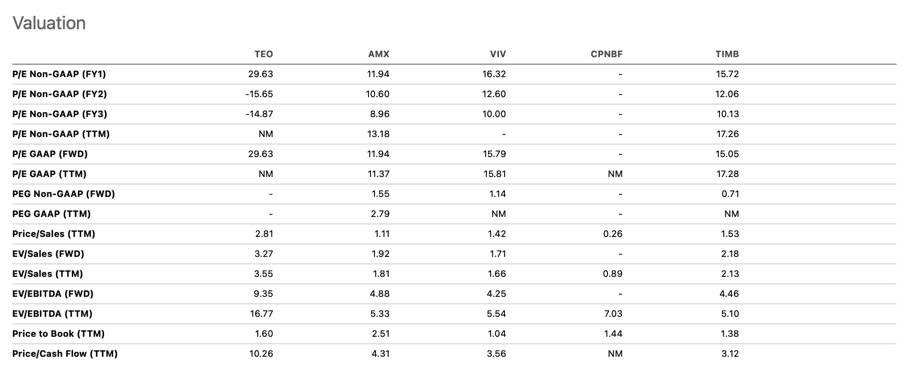

It is trading at a forward P/E ratio of 29.6x, a multiple nearly three times greater than its main competitor, Claro Argentina, which is a part of América Móvil ( AMX ). When assessed against Telefônica Brasil ( VIV ) and Tim Brasil ( TIMB ), Telecom Argentina still maintains a nearly double premium.

A similar pattern emerges when examining forward EV/EBITDA multiples, with Telecom Argentina trading at 9.35x, nearly double the valuation of Claro Argentina and the other Brazilian telecommunications companies.

Telecom Argentina's Price/Cash Flow ratio, currently trading at 10.2x, is also significantly higher than the industry average of 4x and the peer average of 3x. This elevated valuation appears unjustifiable in comparison to its peers.

{kind=link}

Seeking Alpha

The Bottom Line

Telecom Argentina has been experiencing a consistent decline in revenues and has faced considerable challenges in expanding its customer base over the past two years. Despite these difficulties, the company has offset some of its costs even through extreme inflation levels in Argentina. Its leverage situation has also improved compared to the previous year.

In a more optimistic light, Telecom Argentina has performed better than expected in controlling costs during the year's first half. This could help explain why its shares have seen a 7% increase over the year.

However, in my view, there hasn't been a significant improvement to justify the premium the company trades at compared to other players in Latin America.

In simple terms, to reach a forward P/E ratio of 13.25x (which aligns with the sector average) from an initial forward P/E ratio of 29.6x and a share price of $5.58, Telecom Argentina's share price would need to adjust to around $2.51 while maintaining an earnings per share ((EPS)) forecast of 0.19 cents for 2023.

Given an extremely concerning macroeconomic scenario, uncertainties surrounding a rapid recovery, and a stretched valuation, I hold a pessimistic outlook on Telecom Argentina.

For further details see:

Telecom Argentina: Improvements Don't Justify Its Premium Valuation