TCBX - Ten Community Banks Trading At More Than 35% Below Tangible Book

2023-11-06 19:21:38 ET

Summary

- Bank stocks started rallying in May but then fell back creating new opportunities.

- Ten community bank stocks trading below 65% of tangible book value are reviewed, highlighting their risk factors and financial metrics.

- Territorial Bancorp is recommended if you expect a recession and Third Coast if you don't.

Background

On May 8th, not long after the collapse of 3 regional banks due to rising interest rates, I wrote an article titled Want To Buy A Beaten Down Bank Stock? Here's A List And Analysis. This article reviewed 13 beaten-down bank stocks. In that article, I mentioned:

I recommend keeping any investments with these higher risk banks relatively short as I expect bank earnings to decline this year and probably more next year"

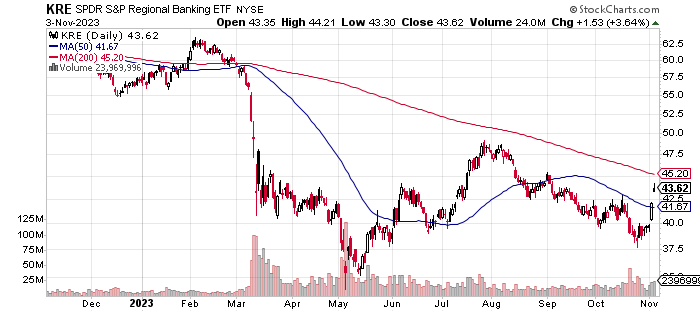

What I meant was that the window of opportunity was relatively short. Those who bought most of the 13 stocks listed should have done well over the next several months. If you look at the S&P Regional Banking ETF ( KRE ) shown below, May 8th was just about the low. There was quite a rally through early August. On August 5th, in a comment to my article, I mentioned I had sold all my bank stocks but one. I quickly sold that one too. From there the average bank stock dropped almost to the May lows. I believe there is another window of opportunity for certain bank stocks.

{kind=link}

Ten Community Bank Stocks Reviewed

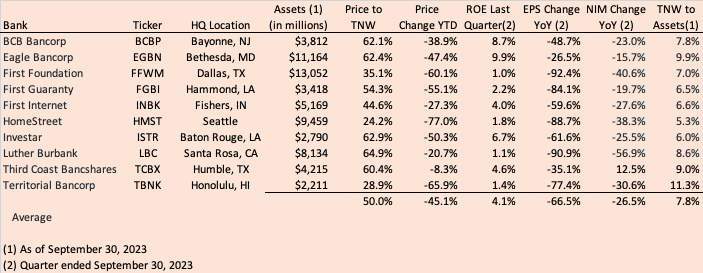

Ten community bank stocks trading below 65% of tangible book value are listed below. Their size, price to tangible net worth, year-to-date price drops, last quarter's return on equity (annualized), earnings per share ((EPS)) change, net interest margin ((NIM)) change in dollars, and leverage are also shown.

Yahoo Finance, Value Line, SEC filings

{kind=link}

A brief discussion of each of the banks in the chart above follows. I looked at the higher risk factors for each bank to see why they were trading so far below their peers. Risk factors I looked at include rapid loan growth, high brokered deposits, growth of nonperforming loans, unusual business segments, a high level of investment securities, and a declining net interest margin.

Rapid loan growth is usually an issue going into a recession. These loans are unseasoned and unseasoned loans go bad at a higher rate in a recession. Brokered deposits are an issue because they cost more in interest expense and often indicate the bank is having trouble holding onto its core deposits. That indicates liquidity issues. Nonperforming loans historically have been the cause of over 95% of all bank failures. This is the most important metric to track during economic weakness. Unusual business segments historically have been more problematic for banks. These are businesses outside of their traditional loans and deposits. Nine of these 10 banks have quite basic business models which I refer to as plain vanilla. They focus almost exclusively on loans and deposits. Only one even has a wealth management division. The other, First Internet, is very untraditional. The summaries are in alphabetical order.

BCB Bancorp ( BCBP )

BCB is based in Bayonne, New Jersey, just across the bay from New York City. Like most on this list, it suffers from a rapidly declining net interest margin caused by rising interest rates. Unlike most, it does not have many investment securities, which helped cause the bank failures last spring. The problem is the high concentration of real estate loans in its loan portfolio. It also has a faster-growing level of delinquent loans than most. Loans over 30 days delinquent were 1.0% of total loans as of September 30, 2023, up from 0.3% one year earlier. It also has had a recent surge of loan growth. The loan portfolio grew 19.2% over the past year. Earnings last quarter of $0.39, missed estimates of $0.50 and were well below the $0.76 one year earlier. Another issue is a high and increasing level of brokered deposits. These totaled $402 million or 14% of total deposits on June 30, 2023, up from $370 million 6 months earlier. Leverage is relatively high. Tangible net worth was 7.8% of total assets on September 30, 2023.

Eagle Bancorp ( EGBN )

Eagle is based in Bethesda, Maryland. It has a history of slow and steady growth. Investment securities were about 22% of assets on September 30, 2023, an average level. Its net interest margin has declined from 3.02% to 2.43% over the past year. Over the same period, nonperforming loans increased from 0.10% of loans to 0.89%. That is well above peer. As of September 30, 2023, it had a high level of commercial real estate loans. They totaled 67% of loans and most were rental properties. It also had a very large construction loan portfolio at 11% of total loans. Commercial construction loans are the riskiest real estate loans as they are often not yet stabilized with cash flow. Eagle also had a very high level of brokered deposits. As of June 30, 2023, brokered deposits were 32.1% of total deposits. Leverage is around peer group average. Tangible net worth was 9.9% of total assets on September 30, 2023.

First Foundation ( FFWM )

First Foundation based in Dallas has a large wealth management division but otherwise is a traditional bank. It had a large jump in loans in 2022 from $6.9 billion to $10.7 billion. About $1.4 billion was from an acquisition, the rest organically. Loans have since declined to $10.3 billion. Investment securities were only about 12% of total loans. High interest rate sensitivity is coming from the loan portfolio. It has a concentration in multi-family loans at 50% of the total portfolio. These are usually fixed rate loans. Brokered deposits were 12% of total deposits on December 31, 2022. The net interest margin dropped from 3.10% on September 30, 2022 to 1.66% on September 30, 2023. This was the main reason EPS dropped from $0.51 to $0.04 during that period. It will probably start losing money in this quarter. Nonperforming assets remain contained at only 0.10% of total loans on September 30, 2023. Leverage is relatively high with a tangible net worth ratio of only 7.0% on September 30, 2023.

First Guaranty Bancshares ( FGBI )

First Guaranty is a bank based in Hammond, Louisiana. It has one unusual activity that is about 11% of loans are commercial leases. This is a higher-risk loan type. It has grown rapidly over the past 7 years with an average loan growth of 17%. This is well above the peer group and indicates an above-average risk of going into a recession. Brokered deposits were 9% of total deposits on December 31, 2022, not a high level. The balance sheet does not appear to be overly interest rate-sensitive. Yet, the net interest margin has declined 19.7% over the past year and EPS dropped a whopping 84%. This was due to a combination of the NIM decline, Significant new high-cost borrowings to fund loan growth, increased expenses, and a low tangible net worth, which magnified the decline. Tangible net worth was only 6.5% of assets on September 30, 2023, well below the peer average. The bank did not list the level of nonperforming loans on September 30, 2023, in its earnings release. As of June 30, it was 0.99% of total loans, up from 0.59% six months earlier. Both levels were well above peer and a concern.

First Internet ( INBK )

First Internet is a very non-traditional bank based in Indiana. It operates mostly online and only has one office for deposits plus a loan production office. It has other non-traditional activities such as a large franchise finance operation and a very large single tenant commercial real estate loan operation. Single-tenant loans tend to be to stronger tenants but could be to anyone. Loan growth has been moderate. The interest margin is being squeezed but not by its smallish investment security portfolio. The problem appears more on the deposit side due to almost no non-interest-bearing deposits and a high level of high-cost CDs and money market accounts. Brokered deposits are mostly CDs. They totaled $671 million or 16% of total deposits, up from $413 million one year earlier. Leverage is high as tangible net worth was only 6.6% of total assets as of September 30, 2023. Nonperforming loans were not an issue at only 0.16% of total loans on September 30, 2023. First Internet did poorly in the 2007-2009 recession but has since changed its business model.

HomeStreet ( HMST )

HomeStreet is based in Seattle. Loan growth had been slow for years but popped up over 30% in 2022 before going flat again in 2023. Its stock has been battered more than the rest on this list. Its problems start with its interest rate sensitivity. The net interest margin declined 38% over the past year resulting in an 89% decline in earnings. The bank is close to going over to losses in future quarters. The investment securities portfolio is of normal size at 14% of assets. So, the problems are in the loan portfolio. There is a concentration of multi-family loans, which are almost always fixed rates. They were 53% of total loans on September 30, 2023. Single-family loans were another 15% and other commercial real estate was 8%. Both are usually fixed rates. Additionally, the bank had a very high level of construction and development loans, both of which are very high risk in a recession. These totaled $566 million or 7.6% of loans on September 30, 2023. This exceeds tangible capital of $498 million on that date, a level that usually concerns the regulators. Speaking of tangible net worth, it is very low versus the peers and even this group. It was only 5.2% on September 30, 2023. Nonperforming loans were 0.42% of total loans on September 30, 2023, up from 0.15% one year earlier. While it has increased a lot, the overall level is still moderate versus peers and historical levels. Brokered deposits were 14% of total deposits on September 30, 2023, but that is down from 19% nine months earlier. It won't take much in losses to violate regulatory capital requirements.

Investar ( ISTR )

Investar is based in Baton Rouge, Louisiana. Loan growth has historically been slow, but jumped up 12% in 2022, before flattening out in 2023. EPS declined to $0.28 last quarter from $0.73 one year ago. The decline was due to a lower net interest margin which declined by 25.5% over that period. Investar does not have a larger investment securities portfolio than its peers. Its loan portfolio is also relatively normal versus peers. Its interest rate sensitivity appears more on the deposit side with a low level of non-interest bearing deposits versus peers. Nonperforming loans were only 0.27% of total loans on September 30, 2023, down from 0.54% on December 31, 2022. Not a concern at this time. Brokered deposits jumped to $198 million or 9% of total deposits from $10 million or 0.5% on December 31, 2022. While this large increase is a concern, it is not at a high level yet. What is a concern is the low level of tangible net worth of only 6.0% of total assets.

Luther Burbank ( LBC )

This bank is located in Santa Rosa, California, which is north of San Francisco. It has a history of slow growth. Earnings were $0.04 last quarter down from $0.41 one year earlier. The decline was due to a large decrease in the net interest margin of 56.9%, larger than the others in this article. The decrease was not due to a large investment security portfolio. That was only 6.6% of total assets on September 30, 2023. The main problem is the loan portfolio which appears to be almost entirely fixed rate loans. On September 30, 2023, multi-family loans were 64% of total loans and single family were 34%. Another problem is an almost complete lack of non-interest bearing deposits. These benefit banks in a rising interest rate environment as they don't have increasing interest rates. Nonperforming loans were not a problem at only 0.08% of total loans. Leverage was not an issue either. On September 30, 2023, tangible net worth was 8.5% of total assets, slightly below average versus the peer. Brokered deposits totaled $442 million or 7.7% of total deposits on that date, similar to the level 9 months earlier. This is also not a concern.

Third Coast Bancshares ( TCBX )

Third Coast is rapidly growing bank based in Humble Texas. It went public in November 2021 at a price of $25 and currently trades at $16.90. Unlike the other banks in this article, its net interest margin has actually increased this year. Its stock price has dropped much less than the others because much of the drop occurred in 2022 from an IPO that was apparently too high. Third Coast has been a hyper-growth bank, which appears to be what has spooked the market. Its loans increased 20% over the past year (ended September 30, 2023) and a whopping 84% in the year before that. This type of growth has historically been a real problem going into recessions. Despite the higher net interest margin, earnings declined from $0.49/share in the September 30, 2022 quarter to $0.32 in the most recent quarter. This decline was due to a surge in operating expenses to support continued growth. Leverage is adequate. The tangible net worth ratio to assets was 9.0% on September 30, 2023. Interest rate risk appears moderate. The net interest margin percentage declined only slightly from 3.77% in the third quarter of 2022 to 3.71% in the third quarter of 2023. The loan portfolio has much less commercial real estate and much more commercial and industrial loans than the others on this list. That should be a positive in a recession. Nonperforming loans were 0.39% of total loans on September 30, 2023, up moderately from 0.29% one year earlier. Brokered deposits were 10% of total deposits on June 30, 2023, up from 8% nine months earlier.

Territorial Bancorp ( TBNK )

Territorial is as plain vanilla as it gets and is based in Hawaii. It is a throwback, a true thrift or savings bank. Most of these either went under in the massive interest rate rise (to over 20%) in the early 1980s, merged out, or converted to a bank model. It has a very high interest rate risk to rising interest rates. As of June 30, 2023, 97% of its loans were single-family mortgages, and most of those were fixed rates. In addition, it has a well above-average investment security portfolio at 32% of total assets on September 30, 2023. Non-performing loans are nominal at 0.10% on September 30, 2023. While it lost a branch in the Hawaii wildfires, only a handful of its loans were affected and they all had insurance. This lost-in-time thrift has had almost no loan growth over the last 10 years. Tangible net worth is quite good at 11.3% of assets on September 30, 2023. It recently cut its dividend from $0.23/quarter to $0.05 causing a stock price drop. It does not use brokered deposits.

Which To Invest In

To determine which if any you invest you have to ask one question first. Do I feel lucky? Sorry, visions of Clint Eastwood… Ask, do you expect a recession next year? If you do, the clear answer is Territorial. If you don't, go with Third Coast.

All of the 10 banks except for Third Coast are suffering from rising interest rates. Their margins have been squeezed, though all are still profitable. But in a recession, the Fed almost always cuts interest rates, usually considerably.

In a recession scenario, there is a clear difference between Territorial to its peers. It has a much lower-risk loan portfolio and a much higher tangible net worth ratio. Loan risk is very important to look at going into a recession since over 95% of bank failures are due to bad loans. It's also a better value, currently trading at 29% of tangible book value versus the peer average of 52%. Almost all of its loans are single-family mortgages. With the notable exception of the 2007-2009 recession, this loan type is usually the least risky loan type. Risk is a bit elevated currently due to a large increase in home prices nationwide. A home value decline could hurt. However, home prices in Territorial's main market of Oahu are only up about 21% from prior to the pandemic. That is less than the national average. The worst case is rates stay high or go higher. In that case, Territorial will likely bleed a moderate amount quarterly for a year or two until asset yields start to catch up to deposit costs.

Third Coast appears to be suffering from a combination of a high IPO price and hypergrowth. Investors are skittish about high-growth banks right now as they have a history of struggling in a recession. Third Coast has slowed its growth recently and laid off some staff. It expects to reverse some of the surge in expenses this quarter. It believes it is interest rate risk neutral. Loan performance has held up well so far, but most loans are unseasoned. In a recession, there will likely be elevated non-performing loans. The loan portfolio by loan type is actually less risky than the average peer as it has much fewer commercial real estate and construction loans. The 7.26% average yield on loans is well above peer, but probably due to most loans being recent since rates went up, and due to a lot of adjustable rate loans. What is more concerning is the average cost of interest-bearing liabilities was 3.91% as of September 30, 2023, well above the peer median of 1.83% on June 30, 2023. Management on its most recent conference call said they expect the deposit cost increase to be mostly done if the Fed does not raise rates again.

Of the others summarized in this article, if you expect a recession, avoid those with high leverage or well above peer nonperforming loan levels. BCB Bancorp, Eagle, and First Guaranty have rapidly growing and above peer nonperforming loans. HomeStreet's leverage puts it close to regulatory capital violations so I would avoid. Investar is also quite leveraged but otherwise doesn't have a lot of higher risks. It is worth considering. Luther Burbank is the most like Territorial and should rebound in a falling interest rate environment of a recession if its multi-family portfolio holds up. First Internet has a lot of risks in a recession such as its large franchise finance operation. It did poorly in the last major recession. I would avoid for now for that reason. First Foundation should rebound in a recession if its multi-family portfolio holds up. It is down so much, it may be worth a look if you have a portion of your portfolio for higher risk stocks.

If you don't expect a recession, all but HomeStreet are worth looking at, but keep in mind rates will likely stay higher for longer. That will cause many of these banks to lose money for a while as their interest margins get squeezed. Those most exposed to interest rates staying high are First Foundation, HomeStreet, Territorial and Luther Burbank. All will likely lose money soon if rates don't come down.

Other banks worth looking at, just over my cut off for discount to tangible net worth, are Metropolitan ( MCB ) and Medallion ( MFIN ). Medallion should do very well if there is no recession as it is discounted for a high risk high return loan portfolio. For larger banks Citi ( C ) trades at just under 50% of tangible book. It would take a whole article to analyze it so I'll leave that to you this time.

I expect a recession next year and am long Territorial Bancorp. I also have a large position in the iShares 20+ Year Treasury Bond ETF ( TLT ). A recession should force the Fed to drop interest rates benefitting TLT, which unlike banks has no nonperforming loan risk.

For further details see:

Ten Community Banks Trading At More Than 35% Below Tangible Book