TCEHY - Tencent: Only Chinese Tech Giant You Should Own (Via A Dutch Holding)

2023-11-29 10:55:28 ET

Summary

- Tencent is the leading provider of social media, video games, fintech, cloud computing, and artificial intelligence products and services in China.

- Tencent is a high-quality business with a high-quality management surfing on a secular growth wave in China.

- Tencent's slowdown is temporary and will likely pick up once China returns to growth.

- Invest in Tencent with a discount via Prosus.

Introduction

Tencent (TCEHY) (TCTZF) is the only Chinese company I would consider investing in. The business is highly qualitative with strong growth, high margins, high free cash flow yields, robustness to economic downturns, and a strong management team. Additionally, you can currently buy Tencent at the lowest valuation multiples in more than a decade. My preference goes to indirectly buying into TenCent via Prosus, a heavily discounted holding mainly invested in Tencent.

Company Introduction

Tencent is a Chinese multinational technology and entertainment conglomerate headquartered in Shenzhen, China. It is one of the largest technology companies in the world by market capitalization, and one of the most valuable brands in Asia. Tencent is the leading provider of social media, video games, fintech, cloud computing, and artificial intelligence products and services in China.

Tencent's core products and services include:

- Social media: QQ, WeChat, Qzone

- Video games: League of Legends, Honor of Kings, PUBG Mobile

- Fintech: WeChat Pay, Weixin Pay, Tencent Cloud

- Cloud computing: Tencent Cloud

- Artificial intelligence: Tencent AI

Here are some key facts about Tencent:

- Founded: 1998

- Headquarters: Shenzhen, China

- Revenue: RMB 545.6 billion (2022)

- Net profit: RMB 188.7 billion (2022)

- Employees: 108.4 (2022)

Tencent has a strong presence in China, with over 1 billion active users of its social media platform, WeChat. Tencent has a growing international presence with offices in over 10 countries. They are also the latest Chinese tech company to launch a ChatGPT-like AI chatbot called HunyuanAide.

What most investors overlook is that Tencent is also a major investor and is one of the largest venture capital tech funds with an investment portfolio of $113 billion. Tencent has strategic investments in other leading technology companies :

- Meituan (MPNGF): A Chinese food delivery and e-commerce company

- JD.com (JD): A Chinese e-commerce company

- Nio (NIO) : A Chinese electric vehicle manufacturer

Financial position & Investment portfolio (Tencent Investor's Kit)

Business evolution

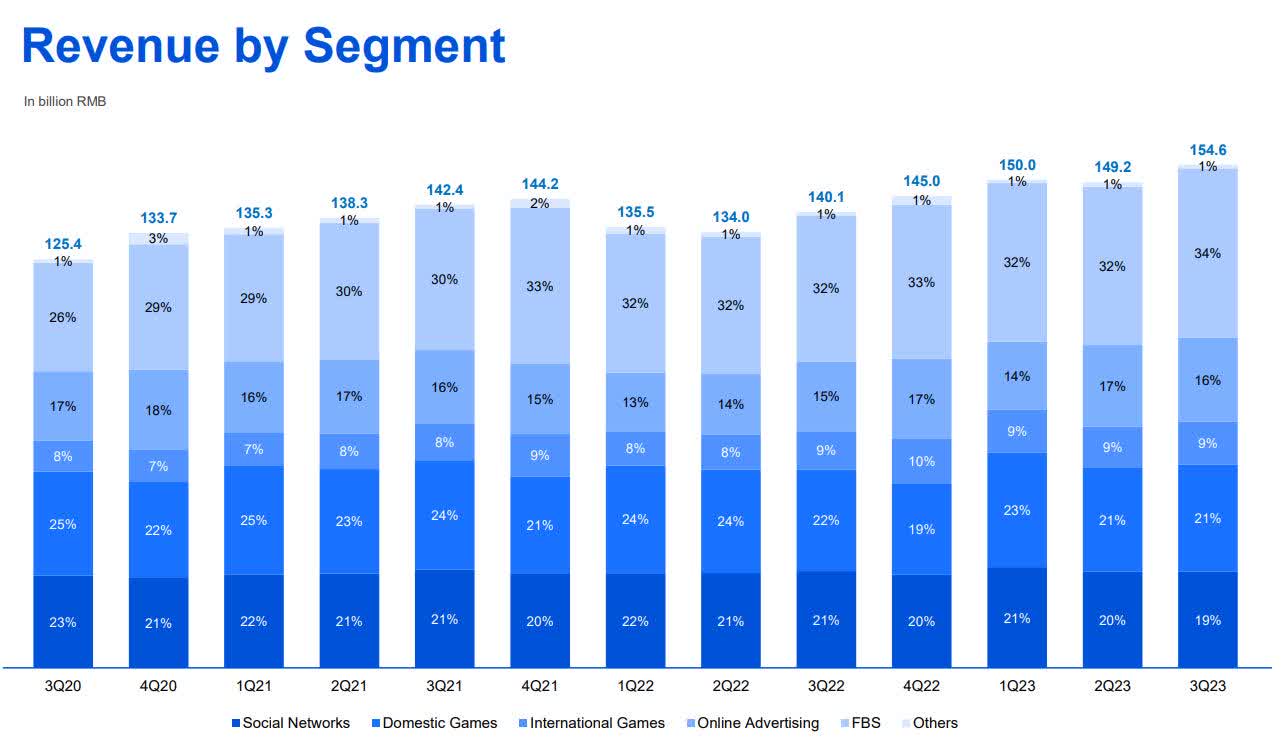

TenCent's quarterly revenue per business segment immediately exposes the massive scale of this tech giant. What is immediately notable is that revenues from the social media division are quite stable and provide a solid basis for Tencent's income. Revenues from gaming are growing, yet not linear. Their fintech division (FBS) is the largest grower in the most recent period but is also the most fluctuant.

TenCent's quarterly revenues per business segment (Tencent Q3 Earnings Presentation)

{kind=link}

All in TenCent's revenue growth has been quite spectacular over the last decade (averaging around ~30%).

TenCent's revenue evolution (Ycharts Fundamental Chart Creator)

In the most recent period, growth has been slowing down significantly since Q3 2021.

TenCent's Quarterly Revenue Growth (YoY%) (Ycharts Fundamental Chart Creator)

{kind=link}

Reasons for the slowdown include:

Economic slowdown : The Chinese economy has been slowing down in recent years, and this has hurt Tencent's advertising and gaming businesses. Chinese consumer spending is low and has impacted advertising and in-app purchases.

Regulatory scrutiny : The Chinese government has been cracking down on large technology companies, especially Alibaba (BABA). The government has been concerned about the company's size and power and has taken steps to reduce its influence. This has included tightening regulations on the company's fintech business and requiring it to share more data with the government. Tencent has however been very cooperative and also divested several stakes in JD.com, Meituan, and Nio.

Increased competition : Tencent is facing increased competition from other technology companies, both in China and internationally. For example, Alibaba is a major competitor in the fintech and cloud computing markets, and ByteDance (TikTok) is a major competitor in the social media and video games markets.

Tencent is taking steps to address these challenges. The company is investing in new growth areas, such as cloud computing and artificial intelligence. It is also working to improve its compliance with government regulations. However, it will likely take time before Tencent's growth returns to its pre-2021 levels.

Another headwind for TenCent is the semiconductor trade restrictions, that were imposed by the United States. The US imposed a ban on selling the newest and most advanced chips to China, which already impacted Alibaba's cloud division . Ironically, China and the CCP are now looking at Tencent and Alibaba to decrease their dependency on Western semiconductor technology.

Profitability

The evolution of net profit and free cash flow has been equally impressive:

TenCent's Income & Free Cash Flow (Ycharts Fundamental Chart Creator)

Thanks to profit margins that expose the quality and the strength of Tencent's underlying businesses.

TenCent's EBIT margin & Net profit margin (Ycharts Fundamental Chart Creator)

We can see that recently the company has compensated weak profit growth with cost-controlling and expansion of its margins.

Video Games Business

Probably the most promising business segment is their video game segment. Tencent is one of the largest video game companies in the world, owning or having a stake in a wide range of popular titles. Here are some of the most popular games that are (partly) owned by Tencent:

| Game |

| Estimated Daily Active Users (DAU) |

| Revenue (2023) |

| Source |

| Honor of Kings |

| 100 million |

| $10.1 billion |

| App Annie |

| League of Legends |

| 115 million |

| $2.2 billion |

| SuperData Research |

| PUBG Mobile |

| 50 million |

| $1.9 billion |

| App Annie |

| Call of Duty: Mobile |

| 20 million |

| $1.2 billion |

| Sensor Tower |

| Fortnite |

| 25 million |

| $1.5 billion |

| SuperData Research |

| Valorant |

| 14 million |

| $1.0 billion |

| Sensor Tower |

Honor of Kings : A multiplayer online battle arena (MOBA) game that is the most popular mobile game in the world by revenue. It has over 100 million daily active users and is known for its fast-paced action and competitive gameplay.

League of Legends : A MOBA game that is one of the most popular esports titles in the world. It has over 115 million monthly active users and is known for its strategic gameplay and high skill ceiling.

PUBG Mobile : A battle royale game that is one of the most popular mobile games in the world. It has over 1 billion downloads and is known for its realistic gameplay and tense last-man-standing matches.

Call of Duty Mobile : A mobile version of the popular first-person shooter franchise. It has over 100 million downloads and is known for its intense gunplay and competitive multiplayer modes.

Fortnite : A battle royale game that is one of the most popular games in the world. It has over 350 million lifetime players and is known for its building mechanics and colorful characters.

Valorant : A first-person shooter game that is one of the most popular esports titles in the world. It has over 14 million monthly active users and is known for its competitive gameplay and unique character abilities.

These are just a few of the many popular games that are owned by Tencent. The company has a diverse portfolio of games that appeal to a wide range of players. The games market is expected to grow significantly in the coming years with a CAGR of 9.06% (CAGR: 2023-2028). And Tencent is well-positioned to benefit from this trend.

Global Gaming Revenues per Segment (Statista Market Insights)

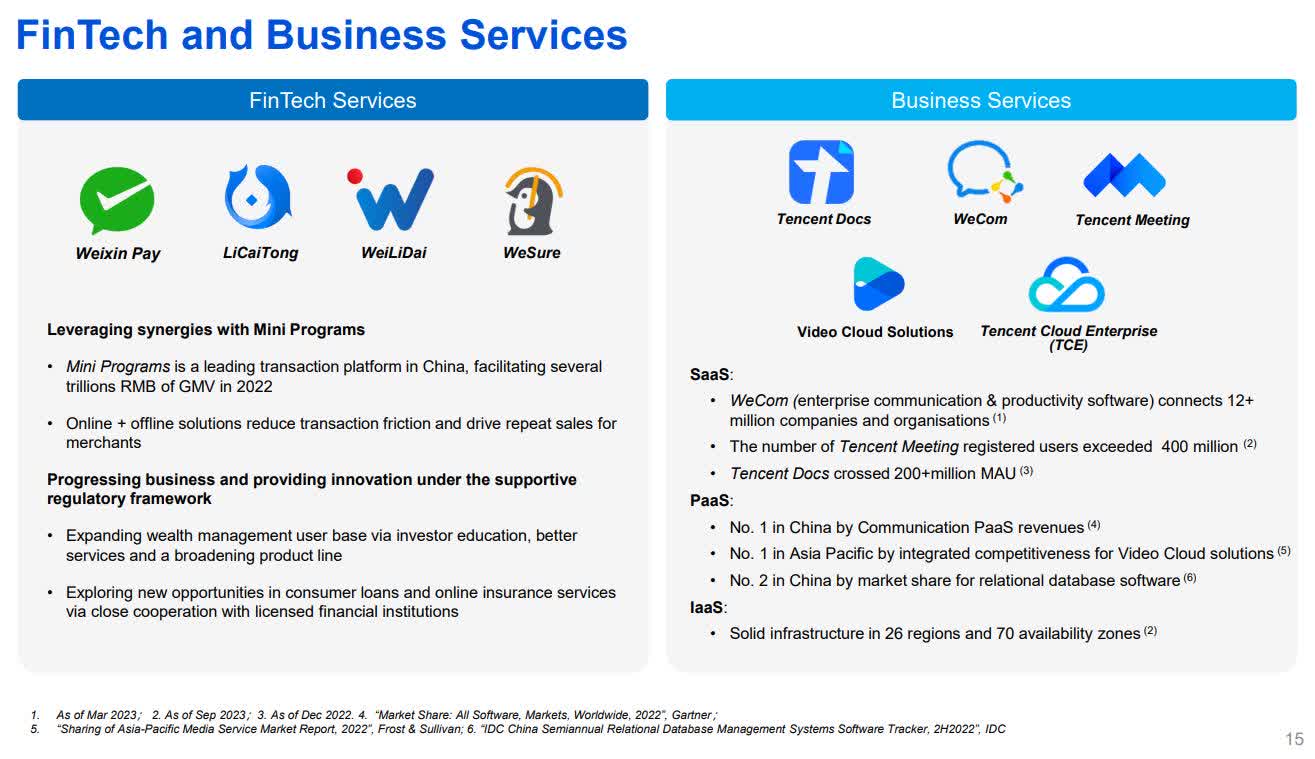

Fintech and Business Services Segment

Tencent's FBS (Fintech and Business Services) segment is one of the company's fastest-growing and most profitable businesses. The segment includes a wide range of financial services including mobile payments, wealth management, and consumer loans. It also includes cloud computing and other enterprise-facing services such as eCommerce services. FBS is a highly profitable business for Tencent. In 2022, FBS generated RMB 177.1 billion in revenue.

Mobile payments are a key driver of growth for FBS. Tencent's WeChat Pay and Weixin Pay are the two most popular mobile payment platforms in China, with over a billion users each. The popularity of these platforms has led to a surge in mobile payments, which has benefited both Tencent and its merchants. Together with Alibaba's AliPay, Tencent & Alibaba have a duopoly in this market. This is not to the liking of the CCP, who tries to break it open by introducing the Digital Yuan.

Wealth management is another area of growth for FBS. Tencent offers a variety of wealth management products, such as mutual funds, insurance, and investment advisory services. These products are becoming increasingly popular among Chinese consumers, who are looking for ways to save and invest their money.

Cloud computing is another growth area for FBS. Tencent Cloud is one of the leading cloud providers in China, and it is expanding rapidly into new markets. Cloud computing is a key enabler of digital transformation, and it is expected to be a major driver of growth in the years to come.

Tencent is well-positioned for continued growth in the FBS segment. The company's strong brand recognition, large user base, and innovative products give it a competitive advantage in the market. Additionally, the Chinese economy is expected to continue to grow in the years to come, which will benefit Tencent's businesses.

Tencent's Fintech & Businesses Segment (TenCent Investor's Kit)

{kind=link}

Management

Tencent's management team is composed of experienced and successful executives who have a deep understanding of the technology industry. The team is led by Pony Ma, Tencent's co-founder and CEO, who is widely respected for his vision and leadership.

Pony Ma, has a complex relationship with the Chinese Communist Party [CCP]. On the one hand, he is a successful entrepreneur who has benefited from the CCP's policies of economic liberalization. On the other hand, he is also a critic of the CCP's censorship and control of the internet.

It is likely that Ma's relationship with the CCP is neither black, nor white. He is a pragmatist who knows that he needs to cooperate with the government in order to be successful in China. However, he is also a man of principle who is unwilling to compromise his values.

Pony Ma and Tencent's management team has earned the deepest respect and it's highly qualitative. Pony Ma was able to grow Tencent from a small tech company, worth only a couple of millions, to the most valuable tech giant in China with a market cap of ~$ 400 Bn. Ma is therefore one of the most successful entrepreneurs of all time in my view.

Valuation

Tencent's valuation is significantly lower than its historical averages (historical PE ratio of ~40x versus ~15x currently). In my opinion, this is too low for a company of this size and quality, even when applying a China discount. The economic slowdown in China, slowest revenue growth in a decade, CCP's crackdown on large tech companies, US trade restrictions, and other uncertainties have all had their impact. In my opinion the slowdown is caused by a more general post-COVID downturn in China and is not related to the specific performance of the company. If you are a believer that Tencent is well-positioned for future growth in its key markets, it is certainly worth picking up at current valuations. In my opinion, Tencent deserves an earnings multiple of at least 25x, resulting in an upside of around 65%. Tencent is therefore rated "Buy". When growth finally returns, earnings multiple can expand further closer to historical levels of ~40x while at the same time growing its earnings.

TenCent's valuation multiples (Ycharts Fundamental Chart Creator)

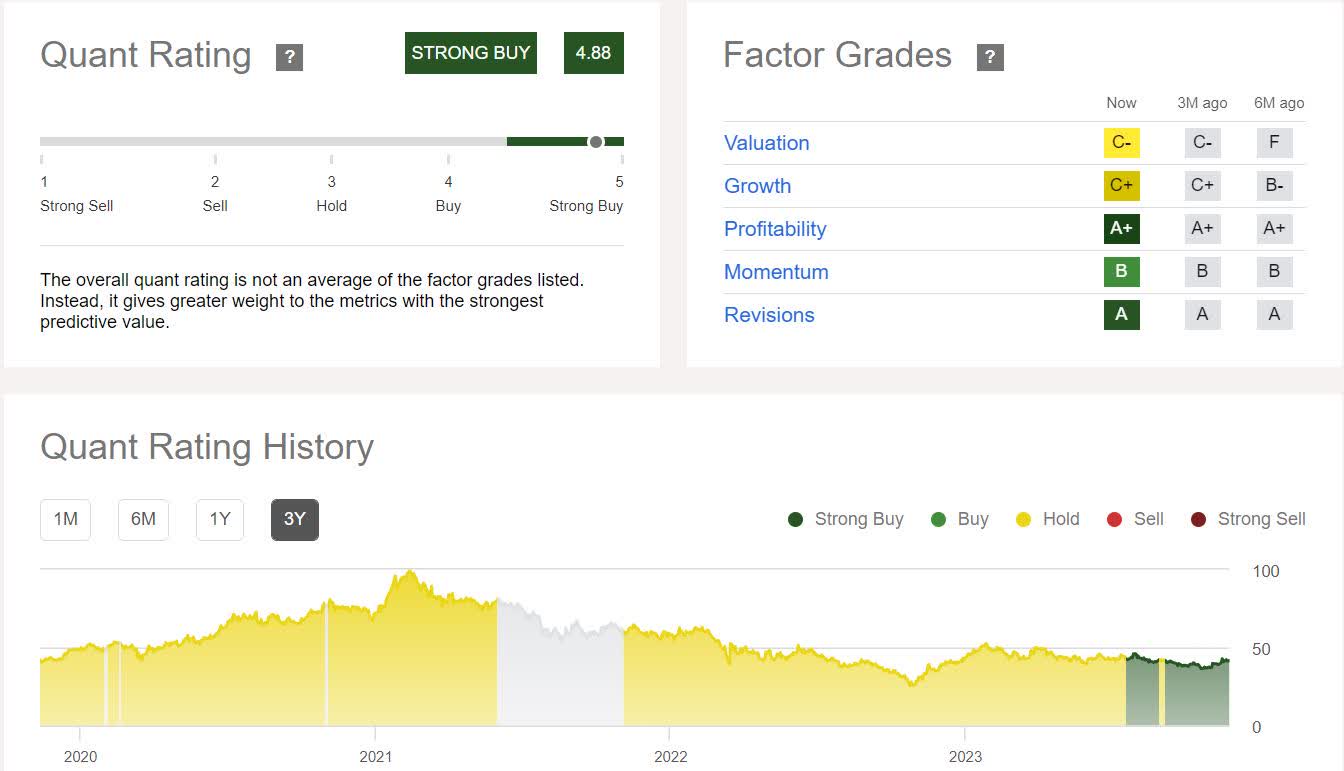

Seeking Alpha's Quant rating also suggests a Strong Buy based on profitability, momentum, and revisions:

TenCent's Quant Rating (Seeking Alpha)

{kind=link}

Prosus Holding: Discount on Discount

For deep-value investors, I would consider buying Tencent via Prosus Holding (PROSY). Prosus is a multinational technology investment group headquartered in Amsterdam, Netherlands. The holding is listed on the Euronext Amsterdam stock exchange and is a constituent of the STOXX Europe 50 index. Prosus IPO'd in 2019 as a spin-off from Naspers (NPSNY), headquartered in South Africa. Naspers still holds the majority of Prosus shares today. A remarkable fact is that back in 2001 Naspers acquired a 46.5% stake in Tencent for only $34 million , a most successful investment.

Prosus Holding is one of the largest technology investors in the world, with a portfolio of investments worth $130 bn. of which $98 bn. worth of Tencent shares (~75% of its investment portfolio). The other $32 bn. (~25%) of its holdings is invested in food delivery, payment & fintech, educational technology, and e-commerce (almost exclusively in private equity). Considering the lion's share of its portfolio still consists of Tencent shares, Prosus can be considered as a Tencent proxy trade (price movement is very similar). Apart from its exposure to Tencent, an investment in Prosus has an additional risk of fluctuating holding discounts and exposure to other tech (ex-Tencent) holdings.

Share performance of Tencent & Prosus (Yahoo finance)

{kind=link}

The reason why investors should consider investing in Prosus instead of Tencent directly is twofold:

1) Shares are trading at a large discount to NAV. At the current share price of $32 (€30) discount stands around ~35%. Although the discount will probably never fully disappear, a holding discount of ~25% seems more fair considering the size and liquidity of the tech holding. In fact, one of the main reasons why Prosus was spun off from Naspers, was to decrease the enormous holding discount (>50% at that time). Management bonus depends on how successfully they compress the holding discount.

Prosus Discount to NAV (Prosus Annual Report 2023)

2) The second reason why I would consider buying into Prosus is because the holding is aggressively buying back shares in an open-ended buyback (meaning a share buyback without a limit in time or amount) for as long as the discount to NAV is at elevated levels. Prosus is financing share buybacks by selling shares of Tencent. This might sound contradictory to my investment case for Tencent, but is not necessarily so as I will explain below. It is important to understand that Prosus is increasing value for shareholders by doing the buyback, while at the same time increasing (or maintaining) the value per share in Tencent.

I will elaborate with numbers. NAV per share for Prosus is € 46.4 of which Tencent-value is € 35 per share. When one Prosus share is bought for € 30 (or $32) €30 worth of Tencent shares needs to be sold to finance the purchase. Therefore with each swap of Tencent shares for Prosus shares, €30 of Tencent is sold, while at the same time €35 of Tencent shares is bought indirectly. Additionally, such a swap also adds €10 of value in ex-Tencent holdings.

In conclusion, Prosus is effectively arbitraging between its own share price and the underlying value of its holdings, which is quite unique. Consequently, Prosus also diversifies away from Tencent as the relative weight (percentage-wise) of Tencent decreases versus its other holdings. But again, the nominal value per share in Tencent increases slightly, while disproportionately increasing the value per share for the ex-Tencent portfolio.

In conclusion, Prosus' sale of Tencent shares should not be seen as a bearish signal for Tencent. It makes perfect sense in the perspective of value creation for Prosus shareholders.

For further details see:

Tencent: Only Chinese Tech Giant You Should Own (Via A Dutch Holding)