SSLLF - TGV Compound Interest H1 2023 Shareholder Letter

2023-07-30 11:35:00 ET

Summary

- TGV Partners Fund is a fund company, more precisely a capital management company. So far, the investment stock corporation has launched eight sub-company assets (TGV) for long-term investors.

- The value of a fund unit is 138.51 Euro as of the reporting date. This corresponds to an increase of 5.2% in 2023, after all costs.

- The portfolio has experienced high turnover, with three new companies added and two sold due to changes in their margin of safety.

- Biontech, Paypal, and Siltronic were added to the portfolio, while Interactive Brokers and Stoneco were sold.

Dear fellow investors/compounders,

I am very pleased to provide you with the investor letter (TGV) Compound Interest as of June 30, 2023.

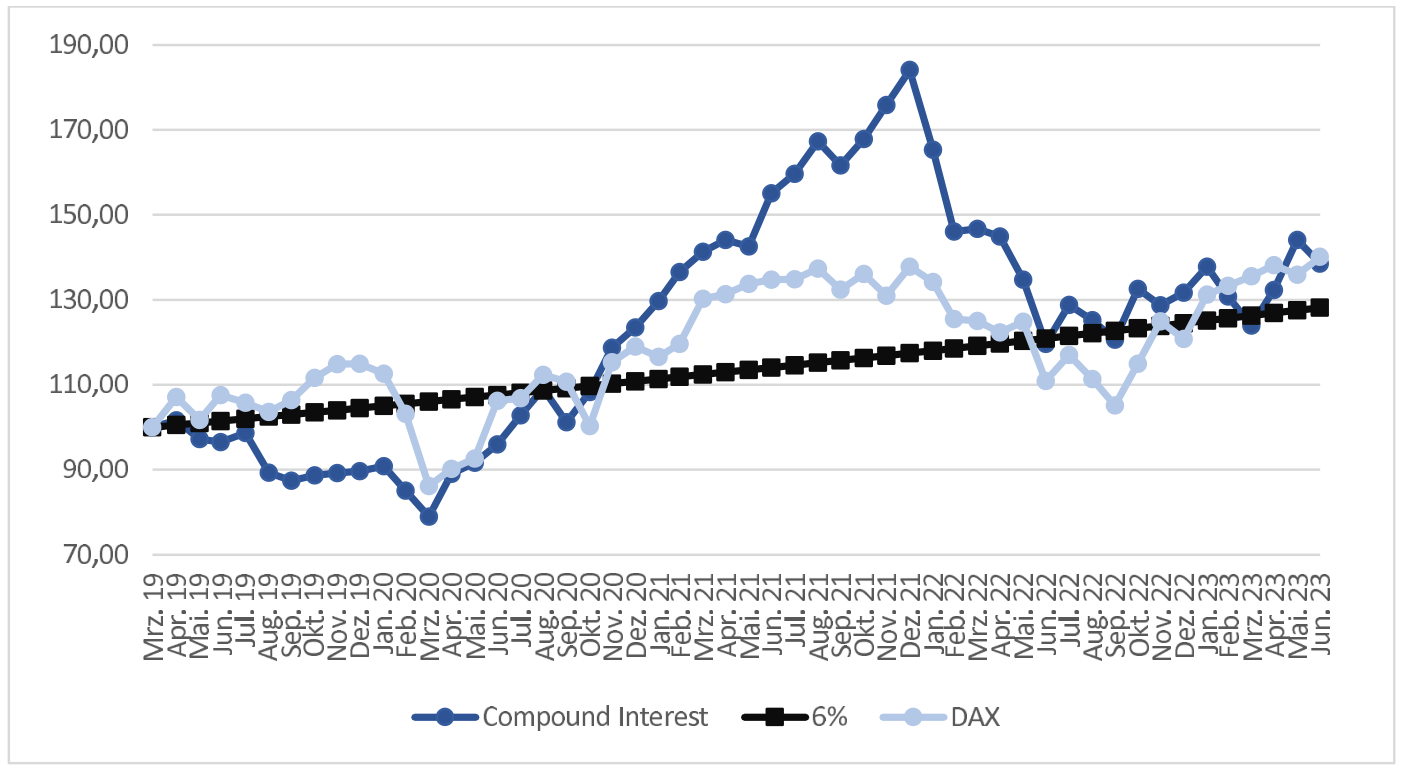

Overview of the development of the portfolio - graphic

{kind=link}

The value of a fund unit is 138.51 Euro as of the reporting date. This corresponds to an increase of 5.2% in 2023, after all costs. Since the launch of the fund, the annualised return of the TGV after all costs is 8.0% per year. The DAX has returned a historically high 8.2% per annum over the same period, without any costs.

I will refrain from comparing the TGV with the DAX in the next letter. The DAX is seen by many German investors as the easiest benchmark for comparison. However, the comparison has been flawed from the very beginning. Today it is straightforward to use the ISIN of the TGV in common online portals to make a comparison with an index that you consider relevant. The index that is relevant for you is the most important one for you.

Portfolio overview for the June 30 , 2023

| Assets in TGV / Net Asset Value |

| 13.516.542,60 Euro |

| Cash / liabilities as % of assets |

| 2.32 % |

| Number of companies |

| 9 |

The positions in the TGV as at June 30 , 2023 are in alphabetical order:

- About You

- BioNTech ( BNTX )

- CHAPTERS Group (Mediqon)

- EQS Group ( EQSTF )

- Intred ( INRSF )

- Mercadolibre ( MELI )

- Paypal ( PYPL )

- Siltronic ( SSLLF )

- Tucows ( TCX )

Location, location, lcoation price, price, price

In 2023, three new companies joined the portfolio. Two have left. This is an unusually high fluctuation for the TGV Compound Interest. What is the explanation for this? For a potential investment, I analyse all aspects of a company: the people managing it, the business model and the price. That is a complex task. To that end, I sift through a company's documents and finances; look at its market position and market development; visit the company, its competitors, suppliers and customers; conduct interviews with experts and much more. If the process is completed positively in terms of the people involved and the business model, the company is put on the list. This list includes more than a hundred companies. If the price of a company on the list becomes particularly attractive, I recommend investing in the company. In this letter, the focus is on the attractive price ? a very important but often underestimated element in investing.

The price of a company is its current market value. In contrast, the intrinsic value of a company is the discounted sum of all future, scenario?weighted cash flows, or put more simply: everything the company will ever earn. The ratio between market value and intrinsic value is the margin of safety. The higher the intrinsic value compared to the price, the larger the margin of safety and the more attractive the price. A higher margin of safety means higher potential returns, but also lower losses if risks materialise. In contrast to the real estate business, where location is everything, in investing an attractive price is everything.

The stock market is subject to strong price fluctuations and thus fluctuations in the margin of safety. These are driven by the expectations of market participants. But the expectations themselves are also often influenced by the fluctuations. I would like to explain this using the example of the former portfolio company Alphabet: at the beginning of 2023, the company's share price fell. Just when artificial intelligence and ChatGPT hit the media. The lower the share price was, the more headlines there were about ChatGPT being a big threat and that the company had missed out on artificial intelligence. Today the share price is higher and artificial intelligence is seen in the media as a great opportunity for Alphabet. The risks that still persist are hardly mentioned. I don't think the reality has changed as much in the last eight months as the share price and the news are signalling. The perfidious thing is that while a low share price and negative headlines seemed to signal high risk for Alphabet, the opposite is true. The lower the share price, all other things being equal, the lower the risk and the higher the opportunity. When conditions change, this statement no longer holds.

As an investor, one can take advantage of this pro?cyclical behaviour. This requires two ingredients: First, systems to minimise content, emotional and psychological errors, and second, a structure and capital that together provide the long?term peace of mind to use those systems and ride out fluctuations. This second ingredient can hardly be underestimated. In 2016, an article appeared entitled "Even God would be fired as an active portfolio manager" . The article analysed how a portfolio would have behaved by buying the stocks that would have generated the highest return over the next five years ? a perfect prediction. The return was very attractive at almost 30% per year, but the volatility of the portfolio was market?like and the maximum price declines were worse than the market. A portfolio manager can only ride out this volatility if the structure and capital are stable. Simply put, if the portfolio manager cannot be fired in between. But when these two ingredients come together, you have turned the problem of volatility into a benefit. A big part of that second ingredient is the fantastic investors of TGV Compound Interest. Thank you for your contribution!

Now you rightly continue to ask the question: Why was the portfolio turnover so high now? In the case of the sold portfolio companies, rising share prices and in some cases falling intrinsic value have led to a reduction in the margin of safety. In the case of the purchased companies, the prices have fallen and the margin of safety has risen accordingly. That is why I subsequently recommended reallocating. Here I present the major changes in alphabetical order in the portfolio for the first half of 2023:

Biontech was bought. Biontech is one of the two leading vaccine manufacturers for the infectious disease Covid 19. This disease will probably be with us for years to come and so will the vaccination. As long as that is the case, Biontech will continue to make excellent profits from the vaccine. Founders Özlem Türeci, U?ur ?ahin and their team have made a huge contribution to helping us overcome Covid 19. Their next target is cancer and other infectious diseases. They are supported by the Strüngmann brothers, well?known founders and investors in the pharmaceutical sector. Together, the four hold more than 62% of the company. This allows for large long?term investments in a promising drug pipeline. In addition to this pipeline and the profits from the vaccine Comirnaty, Biontech has almost as much cash as market capitalisation. Interest is also earned on this cash. I have been following the company since early 2020 and am now pleased to see TGV invested at a very attractive valuation.

Interactive Brokers was sold. The company has developed excellently operationally and benefits from the weakness of competitors such as Charles Schwaab and various banks.

However, the operational risk has also increased: The stronger and more violent the short? term fluctuations on the markets are, the higher the probability that Interactive Brokers' risk systems cannot react quickly enough. At the same time, the price has developed positively and the margin of safety has shrunk accordingly. I have been following the company since 2013 and will continue to do so. When the margin of safety increases again, I will recommend TGV to invest in Interactive Brokers again!

Paypal was bought. Paypal is one of the few global payment service providers that is very well positioned with both consumers and merchants. Paypal is the only company in the portfolio without a long?term owner and is also undergoing a management change. The role of owner is currently taken by the activist investor Elliott. Elliott entered the company at prices that were more than 40 per cent higher than TGV's entry prices. Paypal has been making money since it spun off from Ebay in 201L, and has made some smart acquisitions and share buybacks with it. Recently, Paypal sold its loan portfolio in Europe at attractive terms. The proceeds from the sale will be invested in further share buybacks. On a price? earnings basis, the company has never been cheaper. I have been following the company since the spin?off 8 years ago.

Stoneco was sold. Stoneco is a provider of payment services in Brazil. The company performed well operationally in 2023. The share price has performed even better, rising by over L0%. At the same time, the operational outlook has dimmed as open banking initiatives continue to gain momentum, the market is divided and competitors are getting stronger. Accordingly, my assessment of intrinsic value has fallen, the share price has risen and the margin of safety has consequently fallen. I have been following the company since 2018.

Siltronic was bought. Siltronic is one of three manufacturers of high?purity silicon wafers worldwide. These are needed for the production of state?of?the?art semiconductor chips. Silicon wafers are a good example of mission?critical C?parts: Without them, products like the iPhone or applications like artificial intelligence would not be possible. Despite this critical position, silicon hardly causes any costs in a final product: there is significantly less than ten euros of silicon in an iPhone costing just under a thousand euros. Because of the small contribution to the costs of the end product, the customers' focus is on the function of the product, not on possible savings. This usually allows for price increases.

The semiconductor industry can probably continue to grow for years to come. Digitalisation and electrification will see to that. The company's main shareholder is Wacker Chemie, which in turn is controlled by the Wacker family. Siltronic is the only wafer manufacturer outside Taiwan, South Korea and Japan. This gives the company strategic importance. Siltronic was almost sold to competitor Global Wafers for 14L euros per share in 2021. This was prevented because of its strategic importance. Viewed from a different angle: In order to rebuild Siltronic's facilities, an investment of at least 6 billion euros or about 200 euros per share would be necessary. After this investment, one would have the plants, but no customer relationships, no experience and no patents. Currently you can buy the stock for around 70 euros, get 3 euros in dividends per year and exciting business prospects. I have been following Siltronic for a year and the industry for over 20 years.

The position of Tucows was more than doubled. I have already introduced Tucows to you several times. Tucows is one of the largest registrars for domains and builds fibre in the US. The company's share price had roughly halved during the half?year. The margin of safety has increased and I recommended adding to the position. The reasons for the share price drop are complex, but the big issues have been removed in my view: My former board colleague at Alarmforce, Lee Matheson, is joining the board of Tucows. A large, long?term financing was also put in place to fund further fibre growth. In addition, a transaction in the domains market validated assumptions about the valuation of the domains business: Alphabet is selling its domains service to Squarespace. Operationally, this is unlikely to have much impact. However, if Tucows were to sell its domains business at the same valuation, the proceeds would more than cover its market cap and all debt. You then get the fibre business for free. I have been following Tucows since 2014.

That is all about the big changes in the first half of the year. However, there are two questions that I am often asked:

? How do you find the right time to enter and exit the market? ? Information is always desirable when it is important and knowable. If one knew the best times to enter and exit, the information would be worth more than gold. But that does not seem possible to me: Looking in the rear?view mirror, explanations can always be found as to how one could have found the points in time. Looking ahead is all the more difficult.

A better way of looking at the problem is to replace points in time with time: Over a long time, the entry point becomes increasingly irrelevant. Therefore, the length of time in the market that money works is much more important. For this, it is also important not to be thrown off the curve when compounding: Any sum, no matter how large, multiplied by 0 results in 0. Arriving is much more important in investing than being first.

? How is the economy developing? ? Again, this information is important but unpredictable. Recently I read the following quote from an unknown source: "An economic forecaster is like a cross?eyed javelin thrower. They don’t win many accuracy contests, but they keep the crowds attention.” This is a very apt description of the worlds obsession of economic forecasting. Now the observant among you will think to yourselves: surely if you value a business, you must also forecast the economy. That's right. I solve this dilemma by mainly recommending companies that can survive in almost all possible scenarios and achieve good operating results in as many as possible.

As always, if you have any comments, ideas or criticisms you would like to share with me, please feel free to email me at laurenz@lmncapital.de. I welcome every opportunity to learn!

Thank you for your trust and I look forward to continuing our partnership as investors / compounders in the TGV Compound Interest.

Laurenz Nienaber

Appendix: Explanation of the graphic on page 1

The chart on page 1 compares the performance of 100 Euro invested in the TGV at the closing prices of 29.03.2019 with the performance of a safe, annual interest rate of 6%. Why did I choose this benchmark? The benchmark represents the limit above which a performance fee is incurred in the TGV.

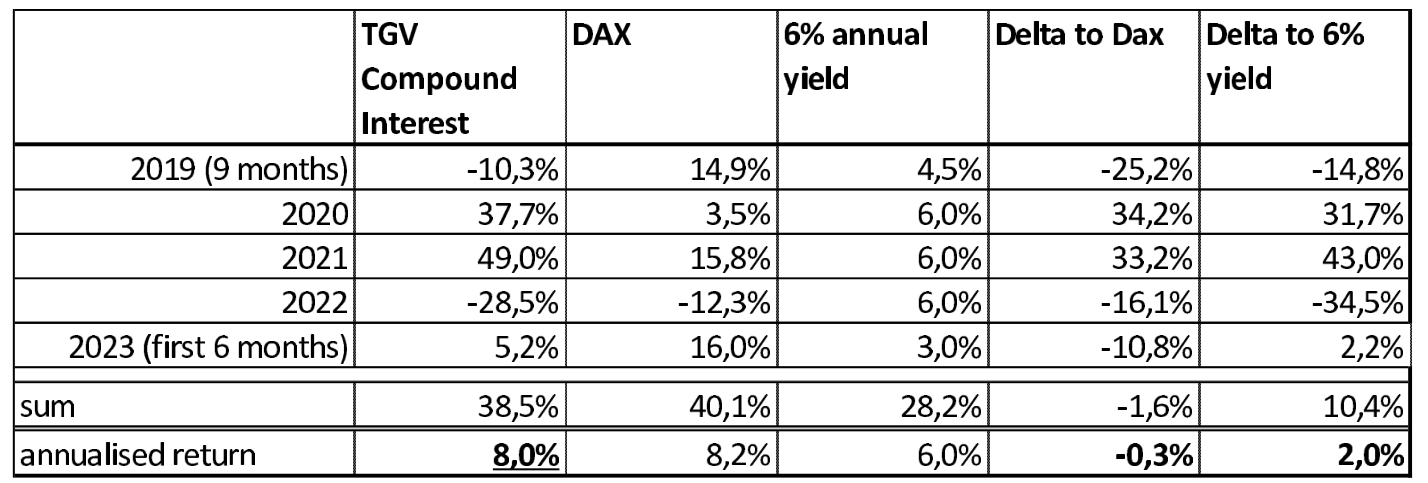

Tabular comparison on an annual basis of TGV, DAX and Hurdlerate

{kind=link}

On the removal of the DAX as a benchmark

As of this letter, I will refrain from comparing the DAX. The DAX is regarded by many German investors as the simplest benchmark. The comparison fell short right from the start. The right alternative would be a synthetic index that tracks the markets in which TGV is invested. However, the creation of such an index is complex: which markets are the right ones? Rather geographically mixed or sectoral? What should the mix be? How should the mix evolve over time? This complexity would have made it easy for me to create an easy comparison without being to obvious. I do not even want to expose myself to this temptation. In the end, it is very easy today to make a comparison with the ISIN of the TGV in common online portals. The index that is relevant to you is, by definition, much more important to you than anything I could come up with.

Editor's Note: The summary bullets for this article were chosen by Seeking Alpha editors.

For further details see:

TGV Compound Interest H1 2023 Shareholder Letter