TC:CC - TGV Partners Fund 2022 Shareholder Letter

Summary

- TGV Partners Fund is a fund company, more precisely a capital management company. So far, the investment stock corporation has launched eight sub-company assets (TGV) for long-term investors.

- The value of a fund unit stands at 131.68 euros as of the reporting date.

- All portfolio companies should continue to increase their intrinsic value over the next few years.

Dear fellow investors/compounders,

I am very pleased to provide you with the investor letter (TGV) Compound Interest as of December 30 th , 2022.

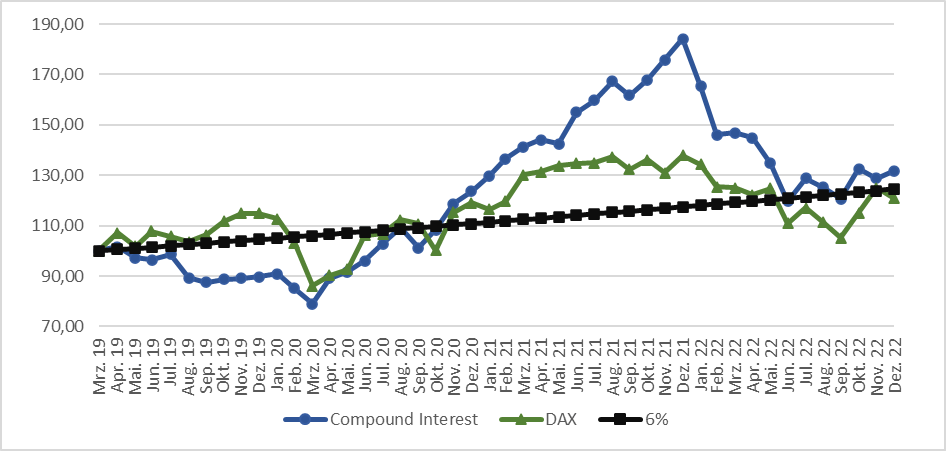

Overview of the development of the portfolio - graphic [1]

{kind=link}

The value of a fund unit stands at 131.68 euros as of the reporting date. This corresponds to a decline of 28.5% in 2022, after all costs. In comparison, the DAX has lost 12.4%. This is a very unpleasant result for 2022, after the two satisfactory preceding years. I share your experience: My private investment in TGV represents a large part of my liquid assets.

The fund's investment strategy is to invest over the long term in companies that generate the most attractive possible increases in value over a long period of time. With this strategy, years like this one are undesirable but unfortunately inevitable. Despite the negative stock market performance, the intrinsic value of the portfolio has increased over the past year, according to my assessment.

Since the fund's inception, the annualized return of TGV after all costs has been 7.6% per year. The portfolio has outperformed the DAX since inception. An investment in TGV at the start of the fund has outperformed the DAX by 9% after all costs.

Portfolio overview for the December 30 th , 2022

| Assets in TGV / Net Asset Value |

| 12,782,610.62 Euro |

| Cash / liabilities as % of assets |

| 8.04 % |

| Number of companies |

| 8 |

The positions in the TGV as of December 30 th , 2022 are in alphabetical order:

- About You

- EQS Group

- Interactive Brokers ( IBKR )

- Intred ( INRSF )

- Mediqon ( MDCKF )

- Mercadolibre ( MELI )

- StoneCo ( STNE )

- Tucows ( TCX )

Portfolio overview

In 2022, the stock and bond markets have partially corrected the exaggerations of the past years. The TGV has also been affected by this correction. Nevertheless, quite a few companies on and off the stock market are still sportily valued today, with high growth assumptions and low discount rates based on negative interest rates in real terms. On the other hand, I see more and more cheaply valued businesses.

Looking in the rear-view mirror, it feels easy to see that 2021 was characterised by exuberance. Niels Bohr, Nobel Prize-winning physicist, stated, "Predictions are challenging, especially when you're talking about the future." That was true then and it is true today. No one knows how the markets will develop. To address this uncertainty, I try to find companies and management teams that can outperform operationally in most scenarios. Furthermore, it helps TGV to make investments that appear cheap relative to their intrinsic value. This is because a favourable valuation additionally reduces the impact of realised operational risks on the investment result.

At this point I would like to give you a brief interim status of the individual investments, in alphabetical order:

I already presented About You to you in detail in the 2022 semi-annual letter. Since then, the company has had to scale back its targets for the 22/23 financial year and is in the process of reducing its high inventories. This is also affecting the rest of the fashion industry. The reason for this is the reluctance to buy, especially in the DACH region. On the other hand, the crisis has made the industry less attractive for potential new entrants and access to growth investments has dried up. The "gold rush" in e-commerce is over for the time being. This also applies to traditional retail: several long-established companies such as Görtz or Galeria Kaufhof had to file for insolvency in 2022. The declining competition gives hope for rising returns among the remaining big players, which also include About You. The company continues to have a solid cash position and is in the process of further strengthening its balance sheet as a precautionary measure to take even better advantage of opportunities. The company had a very difficult 2022, but the inventory clean-up will be completed in the coming months. Accordingly, the outlook for 2023 is better than the 2022 retrospective: About You continues to expect to become profitable in 2023. This is currently not priced in.

EQS Group is a software company. It offers products and services to other companies to meet regulatory requirements for capital market communication and compliance. Both are important components of ESG. This letter is unfortunately not the right format to go deeper into the company, as I have been appointed to the company's Supervisory Board. I therefore refer you to the company's reporting. The annual report is expected to be published at the end of March.

Interactive Brokers continues to grow very profitably with pre-tax margins well above 60%. The company is, in my opinion, the best fully automated broker in the world today. It offers leading prices, access to many trading venues and products, and high security through an excellent balance sheet. Rising interest rates have accelerated earnings growth in 2022. In addition, it has become apparent that competitors such as Robinhood, some of which are highly hyped, have a cost problem. Robinhood is the pioneer of the so-called neo-brokers and advertises the "democratization of the financial industry" and the abolition of direct trading costs. The customer ends up footing the bill, only then indirectly, by having his transactions passed on to high-frequency traders before execution. The client becomes the product and gets worse execution rates. Robinhood is far from profitable despite aggressive cost-cutting measures: In the last 12 months, every dollar of revenue was pretty much matched by a dollar of loss. Interactive Brokers is not perfect either: customer service and the mobile product experience need improvement. Overall, the positives outweigh the negatives, even against the backdrop of its unique market position.

Intred is investing in the expansion and operation of fiber networks in northern Italy. The company focuses on business customers and has laid 9,500 kilometres of fiber in Lombardy. The business continues to run like clockwork in 2022. The biggest supply bottlenecks were for bitumen to re-close torn-up roads. Since the end of 2021, the company has been investing in a major project with the Italian state to connect schools in Lombardy via fiber optic cables. This project offers the company the opportunity to significantly expand its presence at extremely attractive conditions. High returns on capital for further investments of well over 20% are one result. The company is almost entirely equity-financed and has an excellent competitive position in its region.

The investment holding company Mediqon invests primarily in entrepreneurial successions in micro-enterprises via several platforms. So far, Mediqon has been able to carry out and finance its acquisitions very favourably. The team's success speaks for itself and has attracted well-known US investors such as Mitchell Rales, one of the founders of Danaher. The people involved are, in my estimation, people of integrity, intelligence and energy - an excellent combination. Due to the demographic change, the potential to invest long-term capital in succession situations of micro-enterprises is gigantic. The company is conservatively financed and can therefore continue to take advantage of investment opportunities even in turbulent times.

Mercadolibre is the largest e-commerce marketplace and one of the largest payment service providers in South America. The company is led by the team around founder Marcos Galparin and offers its customers a unique platform for online shopping and online and offline payments. Online penetration in Latin America is still low and accordingly offers a lot of potential for both business areas. Many e-commerce companies saw sales decline for the first time in 2022. Mercadolibre's sales, however, increased by 54% in US dollars .

Recently, a major competitor, Americanas, filed for bankruptcy in Brazil. The reason is accounting and financing problems. Fraud cannot be ruled out at this stage. An Asian player, Sea Limited, which was pushing into the whole continent with the Shopee brand, is now concentrating only on Brazil and is discontinuing its activities in the other countries of the continent. This offers opportunities for Mercadolibre. Especially as money for financing new competitors is also becoming scarcer in Latin America. I estimate that Mercadolibre can invest well over one billion US dollars each year in profitable growth and innovation. Very few companies could raise these sums even in the best of times. In December 2022, I visited the company's development centre in São Paulo. The visit confirmed the extremely positive impression I had gained of the company's culture and ambition as a leading technology company in Latin America.

StoneCo is a payment services provider in Brazil. I introduced the company in the 2021 letter. Since then, the benchmark interest rate in Brazil has risen from 2% to 13.75%. This has cost StoneCo interest income, as the interest rate increase could only be passed on to customers with a delay. Contracts with customers had to be adjusted first. A stable or even falling interest rate would be very positive for the company, as absolute interest income would again settle at a level that is about 50% higher. A considerable part of the profit depends on the interest income. I also visited Stoneco and its direct competitors in Sao Paulo last December to gain a better understanding of the competitive situation and the potential changes brought about by the Brazilian Openbanking Initiative. The company is favourably valued compared to the rest of the industry.

Tucows is a Toronto-based holding company with three businesses: Domain reselling, fibre rollout and telecom operations software. The company has been hit hardest by rising interest rates as it is in a very capital intensive phase of fibre roll-out. The management team is working hard to secure funding for future expansion. The company's potential appears very high given its current valuation.

I visited six of the eight portfolio companies last year and am in touch with the important issues at each of them.

In my view, all portfolio companies have a differentiated business model with integer, intelligent and energetic management teams. The companies should continue to increase their intrinsic value over the next few years and should be able to take advantage of the opportunities presented by the current changes. The companies are valued with a very attractive risk-reward ratio

Investor Meeting on 20 th May, 2023

On 20 th May 2023, the annual investor meeting of the Investmentaktiengesellschaft für langfristige Investoren TGV will take place. We will meet again at the Godesburg in Bonn - Bad Godesberg. You are cordially invited and I hope to welcome you on site.

As always, if you would like to share your comments, ideas and criticisms with me, please feel free to email me at mailto:laurenz@lmncapital.de. I welcome every opportunity to learn!

Thank you for your trust and I look forward to our continued partnership as investors / compounders in the TGV Compound Interest.

Laurenz Nienaber

Appendix

Explanation of the graphic on page 1

The chart on page 1 compares the performance of 100 euros invested in the TGV at the closing prices of 29.03.2019 with the performance of an equivalent investment in the DAX and a safe, annual interest rate of 6%. Why did I choose these two benchmarks? A majority of the investors in TGV today are from Germany and will most likely continue to be from this country in the future. The German benchmark DAX is the simplest and most obvious investment alternative for most of these investors. The second benchmark is a safe investment with an interest rate of %6 p.a.. This represents the limit above which a performance fee is incurred in TGV.

Tabular comparison on an annual basis of TGV, DAX and Hurdlerate

| TGV Compound Interest |

| DAX |

| 6% annual yield |

| Delta to Dax |

| Delta to 6% yield |

| 2019 (9 months) |

| -10,3% |

| 14,9% |

| 4,5% |

| -25,2% |

| -14,8% |

| 2020 |

| 37,7% |

| 3,5% |

| 6,0% |

| 34,2% |

| 31,7% |

| 2021 |

| 49,0% |

| 15,8% |

| 6,0% |

| 33,2% |

| 43,0% |

| 2022 |

| -28,5% |

| -12,3% |

| 6,0% |

| -16,1% |

| -34,5% |

| sum |

| 31,7% |

| 20,8% |

| 24,5% |

| 10,9% |

| 7,2% |

| annualised return |

| 8,7% |

| 5,2% |

| 6,0% |

| 3,5% |

| 2,7% |

| [1] If you would like to see the graph as a table, you can find it on the last page of this document. |

Editor's Note: The summary bullets for this article were chosen by Seeking Alpha editors.

For further details see:

TGV Partners Fund 2022 Shareholder Letter