THLLY - Thales: Not Valued For Its Long-Term Quality

2023-11-07 02:14:22 ET

Summary

- Thales is a French defense contractor with a strong focus on defense contracts, generating over half of its revenues from the defense sector.

- The company has solid sales trends and expects ongoing organic sales growth of up to 7%, with a solid operating margin of up to 11.8%.

- While Thales is a good business, the current valuation is not attractive enough to warrant a significant upside, making it a "HOLD" for now.

Dear readers/followers,

Thales ( OTCPK:THLEF ) ( OTCPK:THLLY ) is a French defense contractor I've been peripherally looking at in a few articles, but haven't really covered specifically before. That's something that I intend to change as of this article. I'm looking at a few defense companies, both in NA and in Europe. In this article, I'm going to offer you my first official article on the business.

Let me say this from the get-go Thales is not the cheapest operator out there. Despite being down very slightly, the best bet would obviously have been to "BUY" the company at significant undervaluation, as I did back in 2021.

Unfortunately, I can't take credit for superb returns here, because my position was incredibly small. Less than $2000 in total. Even with the company up almost 80% in less than 2 years, this is not something where I'm going to be taking a victory lap, as from a portfolio-wide perspective this is far too small a position. I meant to expand it - but then the company started climbing - and never really stopped doing so.

So, in this article, I'll show you my logic about Thales to see why and if you should "BUY" the company here.

Thales - A great European defense company

The Thales Group as the company is known, is a French multinational player in the designs of electrical systems, devices, and equipment in aerospace, transport, defense, and security. Its former name was actually Thomson-CSF, which is how some of you readers may know it - but it was rebranded in 2000, named after an ancient Philosopher because the company noted that its brand was not referenced all that positively, especially in recruitment - but also facilitating global expansion, which is exactly what the company has been doing.

The company is part-owned by the French state , and if you know my work, you'll know that generally speaking, I'm a fan of state-owned businesses for the security the ownership stakes offer. The company has tens of thousands of employees and generates annual revenues of around €18B per year.

It justifies being called a "defense contractor" because over half of its revenues hail straight from defense contracts, and because the company is one of the top 10 defense businesses on earth.

As of the 2022 period, 52.1% of the company's revenues came from Defense/Security, and 26.8% from Aerospace, with the rest from digital identity & security.

The company's business model has a COGS of around 74%, but like other defense businesses, it has a sub-12% SG&A, managing to keep the G&A and marketing expenses, and total OpEx below 18%. This results in an EBIT margin of 8.2% of a net margin of 6.4%. This might not sound all that good, depending of course on what you compare it to. But in terms of peers, both the operating and net margin levels for Thales are above sector peers (Source: GuruFocus), with only the gross margins being somewhat average, meaning Thales has some work to do in terms of the efficiency of COGS.

Like any industrial with significant defense exposure, Thales is primarily correlated to defense budget spending. That means that for a long time, the company has traded at relatively lackluster levels for a long time, and only relatively recently started to push upward. But for instance, between 2003 and 2014, the company only very rarely went above 15x P/E.

The company has a low yield - no more than 2.2% at current levels. It's however very conservatively leveraged at less than 32% long-term debt/capital, and the company is also A-rated, making it one of the safer defense businesses in Europe, and with a better mix than many others I review, including businesses like Rheinmetall ( OTCPK:RNMBY ).

The company is currently, as of 3Q23 which is the latest set of results, actively M&A'ing further companies and disposing of non-core assets. The company sold off its Aeronautical Electrical systems segment, and transport segment while completing the acquisitions of Tesserent and Imperva.

The current major trends include upward spending in the French military - of which Thales is getting plenty of new sales and traction.

Thales IR (Thales IR)

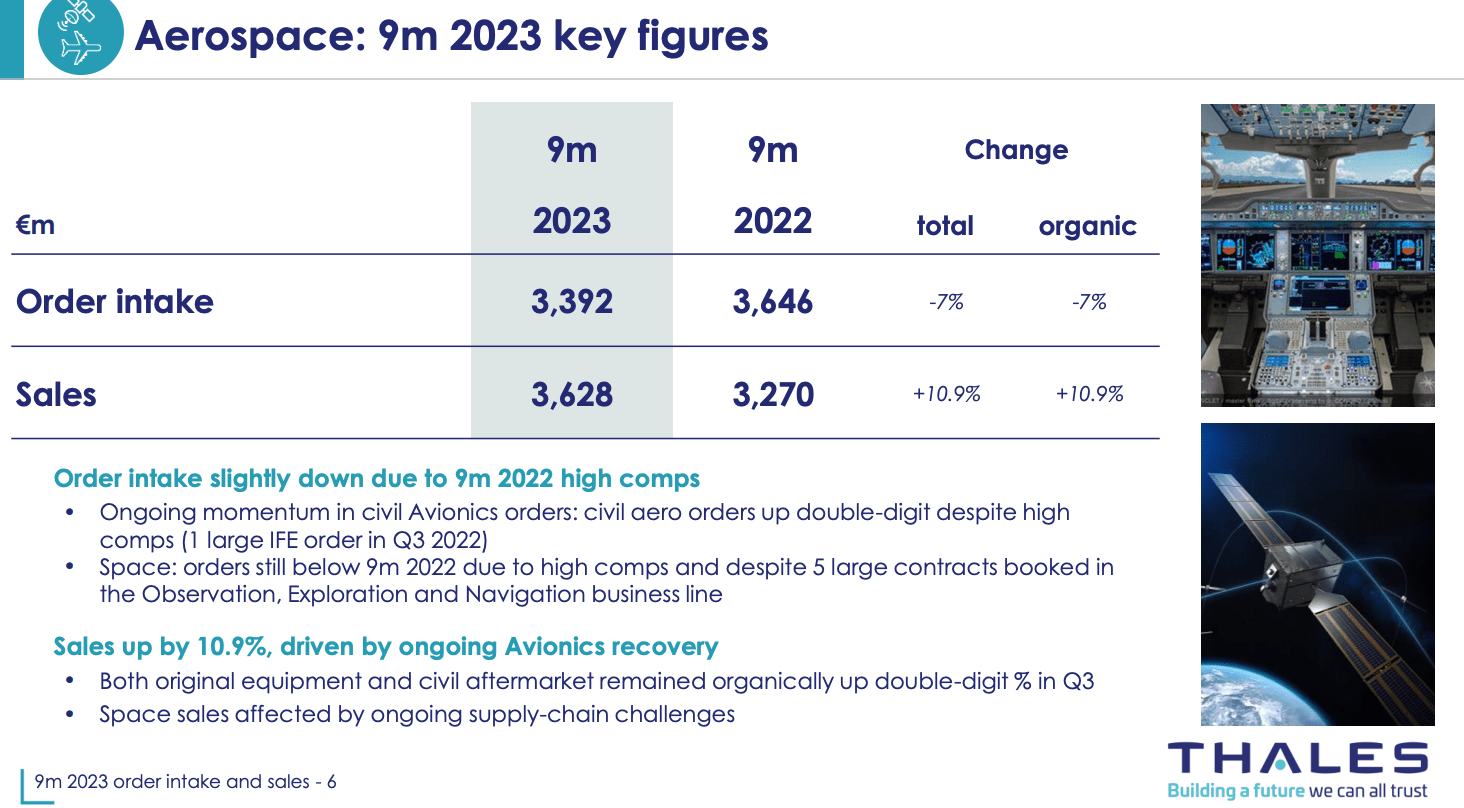

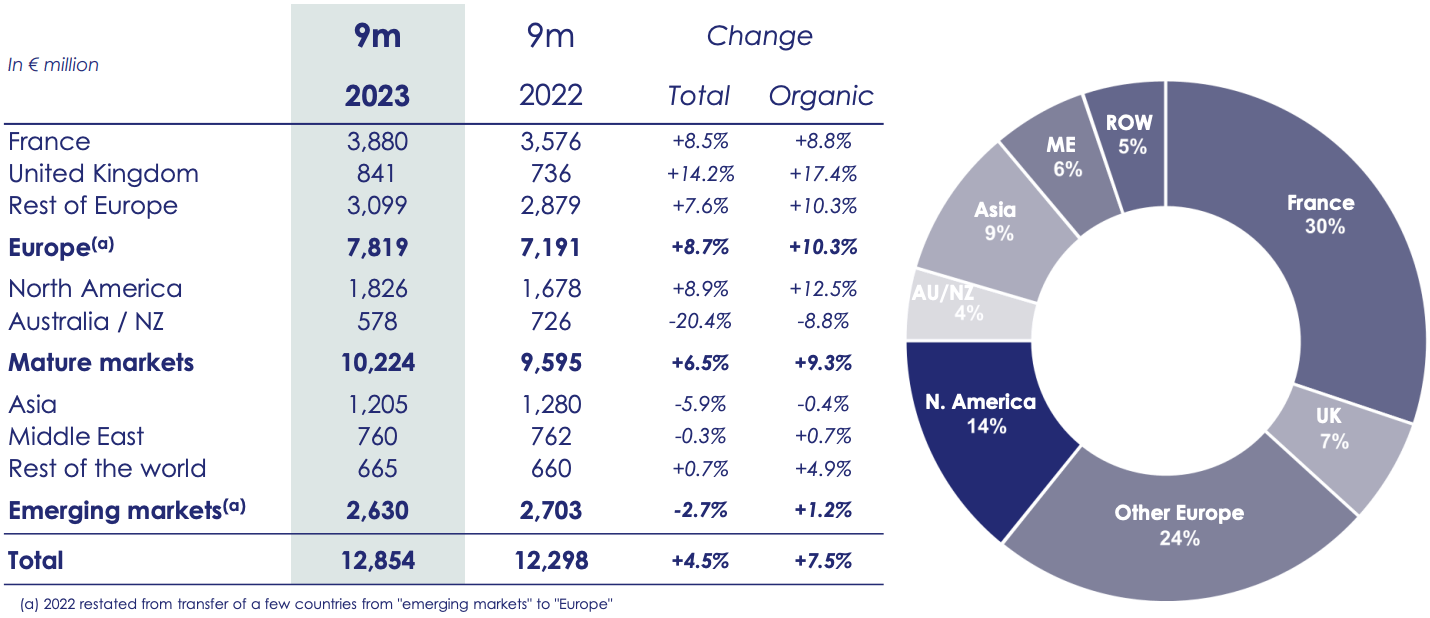

These trends have seen their reflection in the sales trends. Order intake for Thales is down - but the sales number is up, 7.5% organically for the 9M23 period and roughly the same sales trend for the quarterly period. And this is even with the significant negative currency impact that the company saw here. Aerospace saw a double-digit sales increase, driven by solid trends in avionics. The company's core markets, including France and Europe, were also responsible for some of the growth here.

{kind=link}

While the company's order growth was down for the defense sector, sales were actually up. There was an order for Rafale UAE with two larger orders during the period, as well as YoY, with board-based organic sales growth confirmed. Also, remember, Thales is a primary supplier of digital identity and security for many governments and institutions. This segment also saw organic growth, thanks to growth in cyber, biometrics, IoT, and smart cards. On a total basis, the sales are down versus the 9M22 period, but this is only due to a massively positive 3Q22 with exceptional results, a very difficult comp.

Overall, Thales has fully confirmed its 2023E results. The company now expects a Book-to-bill above 1x, ongoing organic sales growth of up to 7%, which means revenue might grow as high as €18.2B, and a solid operating margin of up to 11.8%.

Again, it's not sector-beating results, but it's above the sector average. The challenges with Thales are primarily two. First off, the sub-par dividend, the fact that it's a French company which means a respectable amount of withholding tax, and as we'll see in a bit, the company is also trading at a premium. The last part isn't all that strange - many defense companies have been trading at a premium for years now, but this doesn't make it easier to invest in Thales here.

The company has very solid ongoing sales trends but remains a France/EU-heavy company...

{kind=link}

...and also has the addition of its transport segment. While smaller than the other segments, it's still a good segment with very good order dynamics and large orders in signaling. The signaling and integrated communication systems subsegments are driving the segment positives here.

Thales is, simply put, a very appealing business with a lot of short- and long-term upside. The fact is that this company can claim a 7-10% near-double-digit long-term EPS growth rate, and for the past decade, it's always been a good performer - with the one exception of COVID-19 affected 2020.

It's a long-term sort of holding that you buy when it's inarguably cheap, and only sell off when it becomes too expensive, which I would say that it has been 3-4 times in the past 8 years.

Let's take a look at the valuation and see what we have going for us if we were to invest in Thales here.

Thales - the valuation dictates a higher valuation due to significant growth

Due to increases in defense spending, the expectations for Thales are currently to significantly increase its earnings as well as its earnings growth. The past few years have been double digits, and going forward, the expectations are for double digits as well.

In order to see a 15% annualized RoR, which is the minimum of what I'm looking for, you'd have to estimate an 18-19x P/E, at least 18.05x based on current estimates. What's the problem with this?'

{kind=link}

The problem is that Thales hasn't been averaging that sort of multiple for many years, and the current average P/E is closer to 16x on a 5-year average basis. Looking at it over the longer term, the case gets even less positive, because a 20-year average is at a 15x P/E, which means that a realistic upside for the company on that average is no more than 7.5% per year. This is not bad - but it's certainly not good enough for me, in an environment where I can get this in terms of yield alone if I were to look at pref shares or other income-based investments.

S&P Global investors followed the company, 17 of them, giving targets of €137 on the low side to €166 on the high side, with an average of €155/share. That's compared to a current share price of €135, which implies an upside of 14.3%. Out of 17 analysts, 6 are currently at a "BUY". I would point out, however, that the analysts have a tendency to overvalue the company by about 9-15%, and less than a year ago, that target was around €140.

I would go more conservative here, to make up for the yield, and for the premium. I would give the company a price target of around €125, which would make it possible to see a 15% annualized upside for Thales at around 16.5x on a forward basis, which would be good enough to compete with some of the other upsides I see on the market today.

Thales is a good exercise for valuation. You see, just because a company is a good business, does not make it a good investment. I cover plenty of great companies, that is still considered to be at a "HOLD" rating.

This is one such business.

I want to "BUY" more Thales. But if the company hits 19x P/E, I'll be rotating - if it goes down to €125 or below, I'll be buying more.

That's my strategy for Thales at this time.

Thesis

- Thales is an above-average defense company with excellent fundamentals and a large ownership stake by a government, in this case the government of France. It has an appealing sales mix with about 52% defense focus, giving it some of the appeal of a civil company and of a defense contractor. It's also one of the top 10 defense contractors on the planet.

- At the right sort of valuation, this company is a must-"BUY" with a 15% annualized upside coupled with the safety and quality of a business with a through-cyclic resilience and 5-7% EPS growth per year.

- However, that valuation would be 16-17x P/E at most. While some investors would say the company is currently at a good valuation, I would say the company is now at an "alright" valuation, offering barely a double-digit upside in a market that easily offers 15%.

- Therefore, I would say the company is a "HOLD" here, but will become a "BUY" if it hits below €125/share, at which point a conservative 15%+ annualized upside is very much possible.

- I hold a position in the company, but I have no plans to expand this position at this particular time.

Remember, I'm all about:

- Buying undervalued - even if that undervaluation is slight and not mind-numbingly massive - companies at a discount, allowing them to normalize over time and harvesting capital gains and dividends in the meantime.

- If the company goes well beyond normalization and goes into overvaluation, I harvest gains and rotate my position into other undervalued stocks, repeating #1.

- If the company doesn't go into overvaluation but hovers within a fair value, or goes back down to undervaluation, I buy more as time allows.

- I reinvest proceeds from dividends, savings from work, or other cash inflows as specified in #1.

Here are my criteria and how the company fulfills them (italicized).

- This company is overall qualitative.

- This company is fundamentally safe/conservative & well-run.

- This company pays a well-covered dividend.

- This company is currently cheap.

- This company has a realistic upside that is high enough, based on earnings growth or multiple expansion/reversion.

The company is not cheap enough at this time to warrant a solid upside, even if the company does have an upside here - but I don't consider that upside to be good enough.

This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

For further details see:

Thales: Not Valued For Its Long-Term Quality