NTCT - The Bottom Fishing Club: NetScout

2023-12-16 05:09:35 ET

Summary

- NetScout Systems, a cybersecurity firm, has experienced stable sales, returns/margins, and cash flows despite limited revenue growth since 2017.

- The company's declining share price and low valuation now make it an attractive takeover target for Big Tech firms or private equity investors.

- A 10-year low on sales, earnings, and cash flow generation is now available to new buyers of the stock.

- Technical indicators suggest NetScout is reaching for a bottom, with a favorable risk/reward setup.

NetScout Systems, Inc. ( NTCT ) is a top cybersecurity firm for large companies running computer networks. The organization hasn't grown much on the revenue side since 2017. On the other hand, sales, margin returns and cash flows have been relatively stable, something you can count on during fluctuations in the overall economy. One attraction for me is the consistency of operations, as we slide toward recession in 2024.

Another attention grabber in late 2023 is price has declined dramatically. NetScout has dropped enough to start showing up on my strong valuation screens. The company is selling around 11x cash-adjusted EPS and sports a unique low-leverage balance sheet. Yet, investors seem to be completely uninterested. The share quote is assuming zero for growth prospects, which sets the stage for upside surprises next year.

To me, the company makes a great takeover target for a number of Big Tech outfits. At the very least, private equity might be interested in the inexpensive valuation, especially if interest rates (borrowing costs for a deal) actually backpedal significantly during 2024.

For existing shareholders and potential buyers, the best news is NTCT's beaten down price is showing technical signs of a bottom. It may be a slow turn higher, but I think the risk/reward setup is worth a look.

NetScout Homepage - December 15th, 2023 NetScout Homepage - December 15th, 2023

{kind=link}

{kind=link}

NetScout Homepage - December 15th, 2023 NetScout Homepage - December 15th, 2023

{kind=link}

{kind=link}

The Business

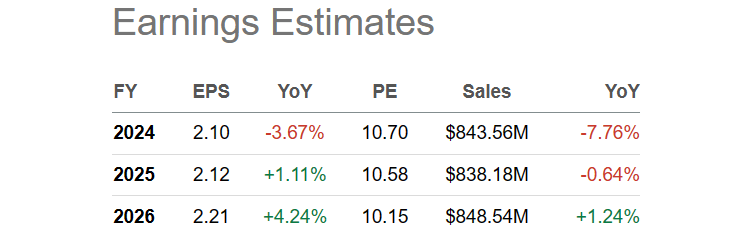

The excuse for much of the price dip since September is somewhat weaker business results have appeared vs. the lofty growth expectations put out by management earlier in the year. On October 16th, a press release revised guidance for sales about 5% lower and EPS closer to 10% less than previous company estimates for the fiscal year, with the majority of this drop centered around the upcoming December and March quarters.

Seeking Alpha Table - NetScout, Analyst Estimates for FY 2024-26, Made December 14th, 2023

{kind=link}

Definitely a bummer, but is the stock worth a good -40% less than 12 months ago? I believe the answer is - of course not, which has created a mispriced opportunity for new share buyers.

Free cash flow in total is averaging around $150 million annually the last few years (on $1.6 billion in equity market capitalization), about a 20% margin on sales. The balance sheet included $328 million in cash and $540 million in total current assets at the end of September. This is measured against $100 million in debt and $658 million in total liabilities. So, NetScout runs a very conservative balance sheet with well above average margins vs. the typical U.S. business enterprise.

The first six months of fiscal year 2024 ending March were actually very solid for reported results. Below are the earnings highlights provided by the company a few weeks ago, with the robust 20% margins boxed in green.

Company Q2 FY 2024 Results - Earnings Presentation, Author Reference Point

{kind=link}

Subtracting employee stock compensation and other items, stripped-down free cash flow generation of around 7% at today's $22 share quote is now available. With most risk-free Treasury interest rates in the 4% to 5% range during December, and inflation in the 3% to 4% area, I am projecting a weaker economy with even lower rates soon could actually help support the buy logic for NetScout.

Valuation Stats

The valuation story effectively highlights a company priced at 10-year lows. Looking at price to trailing GAAP earnings, the current 25x ratio is far below the 50x average over the last decade. A high multiple, yes, but one deserved because of its stable operating profile with high margins. Again, when we look forward at cash-adjusted earnings, new owners are getting shares at closer to 10.7x for a ratio (including high levels of non-cash depreciation and amortization, plus stock-based compensation for workers). Where else can you find a leading technology name with plenty of cash coming in the door at rates approaching 9% of the stock quote?

YCharts - NetScout, Price to Trailing GAAP Earnings & Forward Estimated Cash EPS, 10 Years

Then, when we consider the large cash position of $328 million vs. $100 million in debt, the enterprise valuation statistics really pop out. The EV to FCF multiple of 13.5x works out to better than 7% you could put in your pocket annually (after taxes, mind you), while still maintaining the business and its potential growth future. A similar calculation for the S&P 500 norm is closer to 4% for a FCF yield.

YCharts - NetScout, Enterprise Value to Trailing Free Cash Flow, 10 Years

Reviewing EV to trailing cash-generated EBITDA and basic revenue ratios, it's easy to argue a real bargain is developing at NetScout. Both are at decade lows, a good 40% discount to long-term averages.

YCharts - NetScout, Enterprise Value to Trailing EBITDA & Sales, 10 Years

How does the EV to EBITDA number stack up against the top cloud and computer-networking leaders? It's fallen from a middle of the road valuation to one of the cheapest you can find in the industry.

YCharts - NetScout vs. Major Networking Leaders, EV to EBITDA, 12 Months

Improving Chart Pattern

You have to go back to October 2022 to find another instance of price above its 50-day moving average, alongside a nicely rising/positive trend in On Balance Volume plus the 20-day Chaikin Money Flow and 14-day Ease of Movement indicators. I have drawn this setup below on a 2-year chart of daily price and volume changes.

StockCharts.com - NetScout, 2 Years of Daily Price & Volume Changes, Author Reference Point

{kind=link}

Final Thoughts

Acquiring a high-margin, low-leverage business delivering a solid 7%+ free cash flow yield, that could surprise for growth over time, might prove a brilliant long-term decision today. You are basically purchasing a stock at a discount to past valuations and the U.S. stock market generally, that might deserve a nice premium valuation again in 12–18 months.

If the selling related to a minor slowdown in business results has run its course, bottom fishing right now could be quite rewarding for outperformance returns in the near future. Any uptick in operations should eventually cause a rerating in the stock quote back above $30-35, using a free cash flow yield target of 5% in the not-too-distant future (depending on any unexpected company growth). Without a dividend payout currently, we are talking about the potential for +30% to +50% in price appreciation over 12–18 months.

What could go wrong? The biggest operating worry is competition eats away at the desirability of its cybersecurity product line and expertise. The absence of significant revenue growth since 2017 is a clue this has already been taking place. The biggest weight on sales is networking leaders are doing more and more monitoring, servicing, and protecting with teams developed in-house. However, with a customer base including 90% of the Fortune 500 businesses in America for size of sales, 90% of the largest cloud computing firms, and the vast majority of Big Tech names, the attrition of business has been slow.

In all truth, a major cyberattack on the U.S. internet (especially one hitting non-customer computers hardest), would be the news event to spike extra sales and income at NetScout. Such might coexist with heightened political friction between the U.S. and Russia or China.

Balancing all the pros and cons, I rate NetScout Systems a Buy and own a small position. I believe the share quote will stay above November's low of $19.74, absent a major bear market on Wall Street during early 2024. Assuming all of the operating business variables remain the same, I peg prices of $18 or $19 as Strong Buy territory.

Thanks for reading. Please consider this article a first step in your due diligence process. Consulting with a registered and experienced investment advisor is recommended before making any trade.

For further details see:

The Bottom Fishing Club: NetScout