ATVI - The Broyhill Q4 2022 Letter

Summary

- Broyhill Asset Management is a boutique investment firm guided by a disciplined value orientation. We operate outside of the fray and invest with a rational, objective, long-term perspective.

- For the full year ending December 31, 2022, the Broyhill Equity Portfolio gained 1.3% net of all fees and expenses.

- Contrary to today’s conventional wisdom, the worst bear markets don’t move from peak to trough in a straight line.

- Before signaling that the coast is clear, we expect to see additional financial stresses and maybe even a few financial accidents.

- We think value will continue to quietly outperform for years, just as it did during the last cycle.

“The young man knows the rules, but the old man knows the exceptions. “

- Oliver Wendell Holmes, Sr

For the full year ending December 31, 2022, the Broyhill Equity Portfolio gained 1.3% net of all fees and expenses, as a decade of easy monetary policy, record fiscal stimulus, and rock-bottom interest rates reversed course in dramatic fashion, sending animal spirits running for cover and global equity markets declining 18.0% as measured by the MSCI World Index. Individual returns will vary depending on asset allocation, legacy positions, and capital flows. Quarterly reports, including account and benchmark performance, portfolio holdings, and transaction history, have been posted to our investor portal.

Performance for the period ending December 31, 2022, net of all fees and expenses

| 1 Year |

| 3 Year |

| 5 Year |

| Inception |

| Broyhill Equity Portfolio |

| 1.3% |

| 8.7% |

| 10.2% |

| 12.3% |

| MSCI ACWI |

| -18.0% |

| 4.5% |

| 5.7% |

| 8.4% |

| MSCI ACWI Value |

| -6.9% |

| 4.0% |

| 4.2% |

| 7.2% |

| Performance figures included herein represent returns from strategy inception on September 1st, 2015. For additional important disclosures regarding this report and the performance figures included herein, please see the disclosures at the end of this report. |

For years, markets have rewarded rampant speculation and confused leveraged beta with brilliance, while prudence and caution were deemed old-fashioned and out of step with the “new world” order. As it turns out, the “new world” is not so different than the old world and still at the mercy of the laws of physics and the bounds of mathematical truths. In 2022, the new world came crashing down under the weight of old-world gravity. The predictable yet long-overdue result – value outperformed by the greatest margin in decades. Meanwhile, many “brilliant, new world” investors that never experienced the “old world” where profits are more valuable than promises gave back years of gains while keeping years of incentive fees for themselves. In contrast, a combination of patience, prudence, and good, old- fashioned common sense guided us throughout this period. A dash of humility – a rare trait in this business - certainly didn’t hurt, either.

Admitting what we didn’t or couldn’t know, rather than taking risks we couldn’t or wouldn’t understand, kept us comfortable generating reasonable gains during the preceding bull market, while others “bet the house” (or more accurately, those of their clients) to outperform overly concentrated, and overly speculative benchmarks. As it turns out, by refusing to play their game, we refused to suffer their losses and were rewarded with the best period of outperformance in our history. Years of underperformance evaporated in months. Since inception, the Broyhill Equity Portfolio has compounded at 12.3% annually, net of all fees and expenses, versus 8.5% and 7.2% returns for the MSCI ACWI and MSCI ACWI Value Indices, respectively.

The most impressive return streams (at bull market peaks) are often accompanied by equally impressive volatility. In a bull market, investors learn to live with this volatility as most of it is to the upside. A more conservative approach, such as our own, is not nearly as exciting. But that’s exactly the point. Investing shouldn’t be exciting. The most profits should accrue to the least activity over time. Doing nothing is often the best choice of action. And a lack of excitement doesn’t have to mean a lack of return. In fact, we’d argue, and our long-term returns would appear to support, that a lack of excitement is highly correlated to outperformance for those willing to stay the course.

WHAT REALLY MATTERS

At year-end, we shared a memo from Howard Marks, co-founder of Oaktree Capital Management, with a few of our investors. Marks’ recent memo - "What Really Matters?" - reinforced many of the concepts we’ve discussed in these letters over the years. It also inspired me to go back through those letters to identify patterns, common threads, and repeated truths largely ignored by the majority of investors blinded by soaring asset prices. We look forward to sharing those highlights in the coming weeks. In the meantime, below are a few key takeaways from Marks.

- Macro events are unpredictable , and not necessarily indicative of – or relevant to – a company’s long-term prospects. Most investors can’t do a superior job predicting short-term phenomena and can’t know for sure what macro events lie ahead or how the market will react to the things that do happen.

- Expectations matter. Security prices are largely a function of how events stack up against expectations, but it’s hard to know which expectations are already incorporated into them. Events - and how investors react to them – are unpredictable. So, in the short term, prices are influenced far more by swings in investor psychology than by changes in long-term prospects.

- In good times, those who take the most risk, enjoy the highest returns. There are three ingredients for success in good times – aggressiveness, timing, and skill. Those ingredients aren’t a mark of distinction – invest aggressivly during good times and little skill is required.

- Don’t just do something; sit there. Think more. Trade less. Make fewer, but more consequential, decisions. Over-diversification reduces the importance of each trade. What really matters is the performance of your investments over the next five, ten, or more years. Most people would be more successful if they truly understood this.

- Profit that is disproportionate to loss potential is the holy grail. This is what the industry refers to as “asymmetry.” For aggressive investors, this means avoiding giving back all of your gains in a bear market. (Few achieved this feat last year). For conservative investors, it means not missing out on too much of the gains during bull markets. Asymmetry shows up when an investor can do very well when things go her way and not too bad when they don’t.

- Your investment style should fit your personality. Do you want to focus on finding the “next big thing,” or do you want to focus on avoiding the next big loser? Do you want to make more on the way up or lose less on the way down? Remember, excellence lies between the results in good and bad times. Never confuse brains with a bull market.

At Broyhill, that choice is clear. We strive to make fewer, better decisions to construct concentrated portfolios of high-conviction, long-term investments. Over a full market cycle, we aim to generate above-average returns with below-average risk. Relative outperformance is more likely to be driven by better-than-average results in declining markets (such as last year). The trick, as noted above, will be to position portfolios to capture the majority of the gains during the next bull market. We are excited about that opportunity and confident in our ability to do so.

PERFORMANCE REVIEW

Over the past few years, we’ve felt largely out of step with the markets, as markets appeared to be completely out of step with reality. We feel as though we maintained a clearer head than most throughout this time period, but only with the benefit of hindsight, did we truly appreciate how insane investors had become. We worry that many investors have yet to reach that conclusion.

We are pleased with our performance, which was broad-based, throughout a treacherous market environment. In a year where the majority of stocks were down, fifteen of our twenty-four investments generated positive returns, with investments representing over 80% of our capital outperforming the broader market. 1

The largest contributors to performance during the year were McKesson Corp ( MCK ), Philip Morris International ( PM ), and Coca-Cola FEMSA ( KOF ).

MCKESSON

Shares of McKesson gained 50% for the twelve months ending December 2022, as opioid-related litigation concerns, which weighed on the stock for years, took a back seat to strong operating performance. When we first established the position in 2018, we explained that, “Although headlines remind us daily of growing threats to the business, the actual probability of this business dramatically changing in the next five years is much lower than the perceived probability. We are simply betting that the future might not be as bad as the price suggests.”

Consensus FY22 and FY23 EPS estimates at the time were around $17 - $18 per share. The company reported ~ $24 in earnings in FY22, and is on pace for $26 in FY23, even as consensus estimates for the broader market were repeatedly revised lower. We continued to trim our position throughout the year as shares rerated higher from ~ 8x earnings in FY18 to ~ 16x earnings at recent highs.

PHILIP MORRIS

Philip Morris advanced 11% for the twelve months ending December 2022. After scratching our heads for years, we have to confess to feeling a little bit of pleasure watching some of the previous nonsense get their just deserts. When we first disclosed our investment in Philip Morris, we highlighted the gap between the “haves” and the “have nots” using the Horizons Marijuana Life Sciences Index, which had gained 140% in a few weeks, as an example. The top five stocks in this index generated $1.6B in sales in FY20 and traded at a combined $37.3B market capitalization or more than 23x sales. In contrast, Reduced Risk Products (RRPs) at Philip Morris ( PM ) generated over $6.8B in FY20 sales, which was less than 20x PM’s then $135 billion market capitalization. So one could have bought the top five marijuana companies that burned a cumulative $1.2 billion in trailing twelve-month free cash flow for 23x sales or bought Phillip Morris’ RRPs for less than 20x sales and got over $9 billion in free cash flow generated by their traditional business for free! Since then, the Horizons Marijuana Life Sciences Index went on to shed ~ 85% of its value while PM returned ~ 55% over the same period.

COCA COLA FEMSA

Shares of Coca Cola FEMSA climbed 28% in 2022 as the Coca Cola bottler’s operations continued to benefit from the re-opening of LatAm economies and the continued shift to higher margin, on-premise sales. Curiously, despite the stock’s strong performance and steady increases in consensus earnings estimates which are more than 30% higher since we established the position, analysts appear to have soured on the name. Only seven of the seventeen analysts that cover the stock currently rate it a buy down from about 75% a couple of years ago. While this depressed sentiment gives us confidence that the market has yet to come around to our more positive view on the business, we did trim the position during the year to capitalize on the even greater discount we identified at parent company, Fomento Economico Mexicano.

The largest detractors to performance during the year were: Madison Square Garden ( MSGE ), Meta Platforms ( META ), and Activision Blizzard ( ATVI ).

MADISON SQUARE GARDEN

Shares of Madison Square Garden declined 38% for the twelve months ending December 2022. Since establishing the position, we have shared our thoughts on the business and the rationale for our investment on four separate occasions, including this one. In every single one of those instances, that writing appeared here, as one of the portfolio’s top detractors. The only positive thing that we can say about our investment at this point is that we no longer own it. As market volatility accelerated during the year, we re-underwrote every position in the portfolio with an aim towards measuring and testing our conviction. We scrutizined every assumption behind every investment with a single goal – to eliminate lower conviction positions and increasingly concentrate our capital in those investments where we had the greatest conviction and a narrower range of outcomes (particularly to the downside). Dolan and MSG missed the mark on both counts.

So where did we go wrong? We could point to a dozen factors, but I think it really boils down to two. First, our initial thesis rested largely on the value of MSGE’s irreplaceable, prime asset -The Garden. We believed that investor enthusiasm for “reopening” would close the gap between public and private value, but failed to recognize that once this enthusiasm dissipated, the stock lacked any real catalyst for getting paid. Equally important, while we identified management as a risk at the outset, the “Dolan Discount” lived up to its reputation. First buying MSGN to fund his pet project in Vegas, pissing off both groups of shareholders, then spinning it back out to “clarify” the story. Many investors are hesitant to sell positions held at a loss. It makes sense intuitively, as doing so repeatedly makes it difficult to generate gains. That said, I firmly believe that there is tremendous value in freeing up mental bandwidth, allowing the team to shift their energy to more constructive situations. It’s difficult (or impossible) to quantify, but the benefits are real. There's just something to be said about maintaining enthusiasm for the portfolio, and stale positions just eat up limited resources, better applied to fresh names and fresh analysis. This is also why a 3-5 year hold is typical for the portfolio.

META PLATFORMS

Shares of Meta Platforms declined 66% for the twelve months ending December 2022. It literally pained me to write that sentence. But despite the stock’s horrendous performance, which was the worst of the ( IN )famous FANG gang, we take some comfort knowing that we had sold most of our position at significantly higher prices during the COVID-fueled rally of 2020-2021 and more comfort knowing that we added to the position at year-end, ahead of the stock’s 55% gain this year, through the first week of February. We initially resisted the urge to add to the position after the company’s disastrous third- quarter earnings call, which sent shares down as much as 25% on the day. At the time, our internal recap of the report was straightforward: “Bottom line is that we need to see a clear shift in strategy for the market to value the shares closer to historical levels. This isn't going to happen while META is lighting real cash on fire in the imaginary metaverse.” A couple of weeks later, we got the first hint of what has since been labeled Meta’s Year of Efficiency when Bloomberg reported, “Meta to Lay Off Thousands of Staff.” 2 We doubled our position that day.

ACTIVISION BLIZZARD

Shares of Activision gained 14% for the twelve months ending December 2022, but we managed to lose money on our investment, purchasing shares after Microsoft’s announced acquisition. In hindsight, we were too quick to establish our position upon announcement of the deal. What we initially saw as an attractive spread became much more attractive throughout the year. That being said, we’ve learned by experience that passing up fifty cent dollars laying on the street because they may be later mistaken for quarters, usually results in leaving a lot of money on the table. Most of the time, it’s not long before others come to the realization that they were, in fact, dollars all along. While we have to sometimes remind ourselves of this particular market peculiarity, we’ve also learned that the best approach is to pick up some of those fifty cent dollars when you see them, leaving some on the street to be picked up later should they be mistaken for quarters. In the case of Activision, we continued picking up shares on weakness throughout the year.

While seemingly daily headlines concerning the trials and travails of the pending acquisition have captivated investors and driven short-term volatility in the stock, we think consensus has completely overlooked the exceptional fundamentals of the business, which have inflected sharply higher. Activision recently reported fourth-quarter earnings per share of $1.87 or nearly 25% higher than the average analyst estimate of $1.52, which barely budged over the past three months. Performance was largely driven by the company’s flagship Call of Duty franchise, as Modern Warfare II posted record sales for an opening quarter. Management expects full-year revenue growth of “at least high teens,” which will likely be an outlier in a market full of declining estimates (more on this next). Bottom line: while shares have been rangebound, held at the mercy of regulators, we believe our margin of safety has increased during the year as investors appear uninterested or unaware of the company’s increasing long-term intrinsic value.

PORTFOLIO COMMENTARY

At year-end, our top five investments in alphabetical order were Activision Blizzard, Altria Group, Dollar Tree, Fiserv, and Philip Morris. We made one new investment in the second half of the year and fully exited several positions where our confidence had diminished. For the most part, we remained patient, providing our theses with the runway to play out. Otherwise, simple adjustments around the edges constituted the majority of our activity during the year--trimming positions on strength and adding to others on weakness. A few of those adjustments are noted below.

We rebalanced our tobacco exposure during the year, reducing our investment in Altria as the future of the company’s combustible cigarette business became increasingly questionable given pending US legislation and a lackluster portfolio of reduced risk products. We reinvested the proceeds in Philip Morris so that relative position sizing is more consistent with our increased conviction. Since we shared our initial investment thesis in our mid-year letter to investors, the company completed its acquisition of Swedish Match, unlocking access to the world’s largest and most lucrative nicotine market. The US profit pool is valued at over $20 billion, increasing the company’s addressable market by ~60%. Importantly, this business is entirely incremental for the international manufacturer of Marlboro, as the only tobacco company without a legacy cigarette portfolio in the US. We think consensus estimates may also be overlooking the fact that the average margin on cigarettes in the US is more than 3x greater than PMs existing markets, which still represents quite a long runway for IQOS (see chart below).

{kind=link}

We also rebalanced our “FEMSA exposure,” reducing our position in Coca-Cola FEMSA ( KOF ), which we highlighted in our Q2-21 letter to investors, in favor of Fomento Economico Mexicano ( FMX ). FEMSA, founded in Monterrey, Mexico, in 1890, owns 47.2% of Coca-Cola FEMSA (with 56% of the company’s voting rights), holds a 14.8% stake in Heineken, and operates the third-largest convenience store chain in the world, with over 20,000 stores in five countries. After backing out the value of the company’s bottling and brewer holdings, we estimated that investors were valuing the FEMSA retail stub, Oxxo, at nearly a 50% discount to historical levels and almost a 60% discount to peer, Walmex. Given the company’s multiple pathways to unlock value and its heavily incentivized leadership team, we increased our exposure based on our confidence that management's pending strategic review would reward shareholders. Subsequent to year-end, the results of that review provided additional upside to shares. Management announced a plan to sell its entire 14.8% economic stake in Heineken, representing an after-tax cash inflow of around 24% of its market capitalization, returning excess cash to shareholders.

We eliminated several lower conviction positions during the year, liquidating investments in NVR Inc., Tencent Holdings, The Walt Disney Company, and Starbucks Corp. Smaller positions often complement our core investments in one of two ways. They can occassionally “test the waters” as a starter position while we continue our research efforts, aiming to increase our investment alongside increasing conviction. They can also remain as residuals of core positions that have been scaled back over time on strong performance. While there are benefits to this increased flexibility, there are risks as well. For one, it becomes much easier to generate losses in this business if you end up with a bunch of lower conviction names in the portfolio. As a result, the number of investments we hold at any given time tends to ebb and flow with the opportunity set and the market environment. At times, there are clear benefits to a Marie Kondo-like approach to portfolio management.

Speaking of fresh names, we established a new position in Netflix during the second half. We began accumulating shares after the company reported two consecutive quarters of subscriber losses, which brought the stock down by about 75% from peak to trough. Our investment in Netflix is a good example of what we categorize as a “temporary dislocation” and a great example of the historical investments we’ve made in the tech sector. Unlike other “value” investors, we don’t arbitrarily put tech in the “too hard” pile. We are comfortable and more than happy to underwrite investments in the industry. We just demand a margin of safety when doing it (something often ignored by other investors in the industry). That margin of safety opened up when consensus quickly concluded that Netflix’s growth was over, on the heels of two quarters of subscriber losses, which happened to follow years of surging lock-down-induced demand. The popular narrative was that by pursuing advertising revenue, Netflix was all but admitting that streaming television was completely saturated. We thought otherwise. With ~ 75MM subscribers in the US, even converting a small portion of those 100MM moochers would move the needle 3 . And given the superiority of the company’s technology and first- party user data, we think the consensus is completely underestimating the long-term potential of a Netflix advertising model.

In addition to Netflix, we also bought and sold shares of Twitter during the year. Our first foray with the stock was in early 2020 when shares were trading at unjustifiably low levels relative to soaring social media peers. We fully liquidated our investment as speculation went haywire over the next year or two, then reestablished a position last year after Elon Musk signed a deal to take the company private at $54.20 per share in April 2022. In typical Musk fashion, he quickly reversed course, attempting to back out of the iron-clad deal. With the market pricing the probability of the deal closing as a coin toss, at best, we liked our odds, which are outlined below.

A quick side bar on our process may be informative as this illustration is a good example of our overall approach to portfolio construction, although sadly, not every investment is accompanied by such amusing facial expressions. Nonetheless, we rank every name in the book and every name in the pipeline by a single metric – probability-weighted expected returns. In other words, for every investment in the portfolio, we estimate worst-case, base-case, and best-case fair values. Then we assign probabilities to each and size investments accordingly. For situations like Twitter, this exercise is relatively straightforward. The outcomes are well-defined, so our focus is on forecasting the probabilities of each outcome. For most other investments, we are constantly updating both our estimated probabilities as well as our fair value estimates under various scenarios. With each new piece of information, we consider how it impacts our estimates as well as our odds. And we adjust accordingly. To many investors, this may seem like overkill. It requires a level of discipline—and a consistency in the application of one’s investment process—that we find to be quite rare. Our sense is that the majority of our peers spend 95% of their time analyzing businesses, then essentially stick their thumb in the air when it comes to position sizing. This is a big mistake. While we understand the challenges of explicitly outlining and updating qualitative implicit assumptions – like the probability of being right on a name – the benefits are clear and pronounced.

A recent study by Alpha Theory concluded that investors who are most diligent in updating their assumptions also produced more than four times as much alpha as the least diligent investors. 4

The median update frequency for the top quartile was 25 days, meaning that the top investors updated their assumptions more than ten times as often as the bottom quartile. While that may seem unnecessary to most, the results are consistent with similar research performed by God Judgement Inc. and published in the phenomenal book, Superforecasters. 5 Consistent with Alpha Theory’s conclusions, the authors found that top forecasters updated their assumptions roughly four times as often as others. The frequency of updates is highly correlated with outperformance, and by incorporating even minor bits of new information that either support or detract from the probability of a given outcome, you can generate better results over time.

At Broyhill, this means putting in the work, day in and day out, to identify mispriced assets. It means constantly revisiting our assumptions and tweaking our estimates. It means making small changes at the margins and regularly adjusting for new information.

In other words, it’s classic value investing. It’s a rare breed because few have the patience or the discipline to stick with it. This is rather fortuitous for us because expected returns tend to be inversely correlated with the amount of competition in the marketplace. That’s precisely why it works.

MARKET COMMENTARY

Owning what everyone else owns leads to average performance. But when those indices and the most popular stocks in them are wildly overvalued, average performance can get you in a lot of trouble. We strive to invest in a fashion that generates acceptable returns in a variety of market conditions. That doesn’t mean we will make money every quarter. But we aim to minimize the risk of large losses, and that’s exactly what we did last year.

Many investors operating today have never experienced a proper bear market. And as such, many of them have only experienced V-shaped recoveries. In contrast to those quick recoveries, it typically takes about three years on average to recoup losses from a run-of-the-mill bear market. It takes a lot longer to get back to even after a bubble bursts. The last time the market was this concentrated in growth equities, it took nearly a decade to recover. The steeper the descent, the more difficult it is to climb your way back out. This is precisely why we place such great emphasis on capital preservation.

{kind=link}

Contrary to today’s conventional wisdom, the worst bear markets don’t move from peak to trough in a straight line. But, for many investors today, spectacular crashes - as we saw in 2008 or 2020 – are their only reference points. They have yet to experience the drawn-out, demoralizing process marked by years of painful losses and repeated frustrations.

Equity markets were quite chaotic in January. Fed comments on financial conditions were interpreted as a green light to buy crypto, meme stocks, and just about any other speculative corner of the market. Investors—or more accurately, speculators—would be well served by a quick history lesson. After the tech bubble burst, the NASDAQ saw seven rallies greater than 17% from 2000-2002. Some gained as much as 40% - 50%. Yet every single one of them was followed by lower lows. We imagine that investors at the time felt like the guy at the front of the ship here. We also imagine that many investors might feel like that after the recent rally as well.

{kind=link}

Unfortunately, for the guys at the front, big bear markets don’t bottom until we reach hopeless. And we are not at “hopeless” yet. Until then, we are monitoring several factors before getting more constructive on equities.

To start, we need to see the Fed and other central banks truly reverse course. That’s a lot different than simply slowing the pace of hikes. While investors are quick to celebrate any hint that the pace of interest rate hikes may be slowing, markets are unlikely to bottom until the Fed has actually begun cutting rates . Side note: markets fell another 41% and 55% after the Fed began cutting rates in 2000 and 2007.

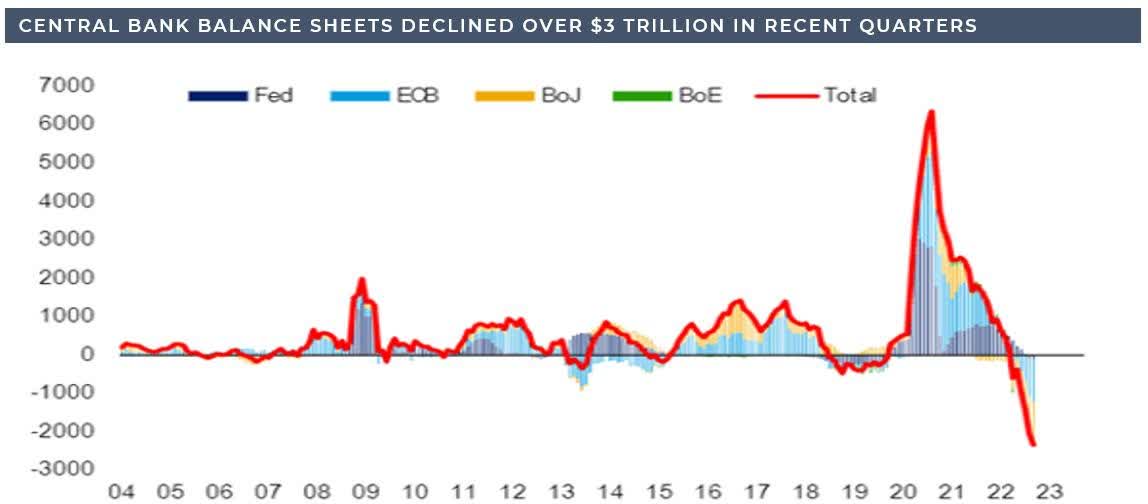

Complicating matters is the fact that central bank balance sheets are declining at the fastest pace in modern history, making financial conditions even tighter. Shifts of this speed and magnitude have historically presented large headwinds to the global economy and to risk assets, increasing the likelihood of a severe global recession and continued downward pressure on asset prices.

Tighter financial conditions point to a much sharper slowdown in economic growth. And while some claim this is the most expected recession in history, the NBER has yet to label it as such. This may just be semantics, but historically, markets have bottomed ~ 7-8 months after the start of recession. And according to the NBER, the recession hasn’t even started yet!!

Before signaling that the coast is clear, we expect to see additional financial stresses and maybe even a few financial accidents. They say that something usually goes through the windshield when the Fed taps the brakes. Today, global central banks are yanking on the e-break as hard as they can at the same time. We’ve already seen a sharp unwind in the most speculative corners of the tech sector, crypto markets, and UK pension funds. A continued rising cost of capital may create additional stress in housing, credit markets, and elsewhere this year. Until then, it’s just hard to see how markets find a bottom with liquidity being sucked from the markets and cash drained from consumers’ wallets. Bottom line: we think a march sharper contraction in economic growth is necessary before we claim that the coast is clear.

{kind=link}

We also think we are likely to see better prices before this is all said and done. All asset bubbles revert to trend. Every single one of them. Most overshoot to the downside. So, if the bottom is already in, this would be one of the most expensive bear markets in history. While last year’s sell-off was brutal, it doesn’t mean markets are cheap. Valuations outside of the US are more reasonable, but US valuations have only returned to levels last seen at the peak of the tech bubble (see chart below).

{kind=link}

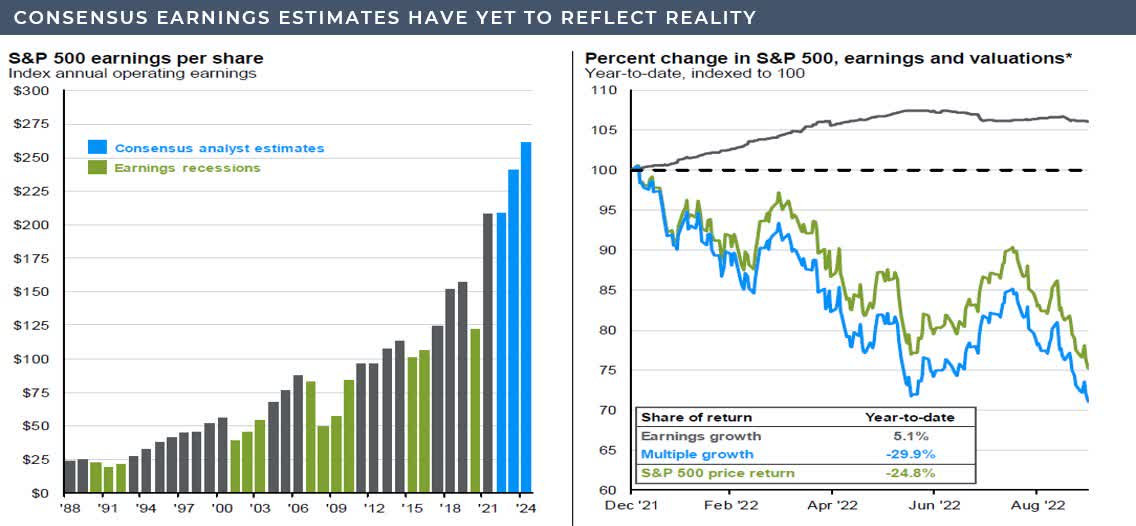

And historically, markets don’t bottom before earnings revisions have troughed and begun to accelerate. While Bloomberg Economics’ Probability of Recession in the next twelve months has reached 100%, consensus earnings expectations are still in la-la-land (left chart). Equity market declines to date have been entirely driven by multiple compression (right chart). The next leg of the bear market is likely to be driven by a sharp decline in earnings estimates.

{kind=link}

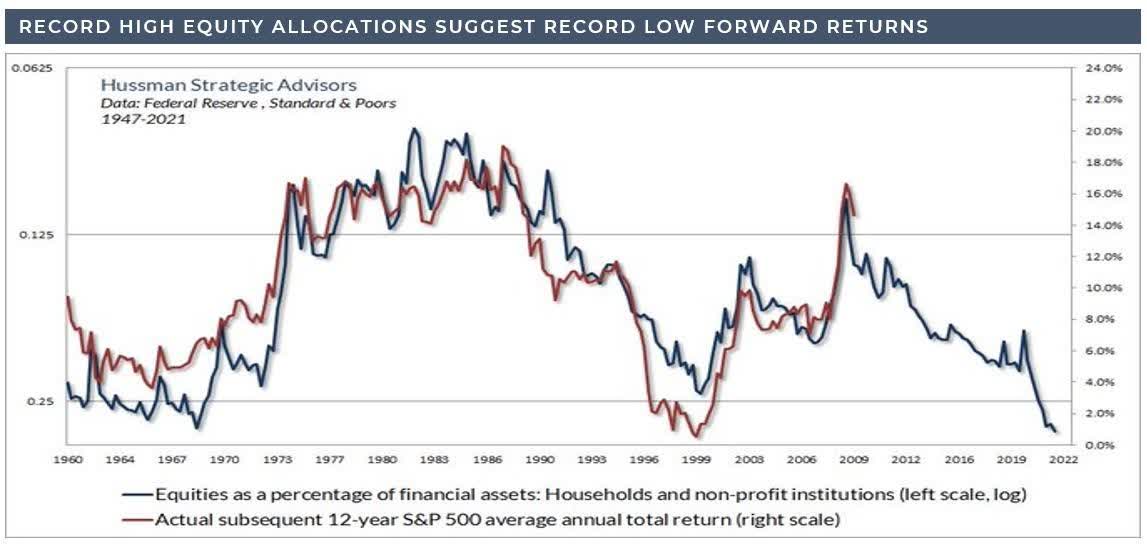

So, Wall Street still appears overly optimistic. That’s not exactly a dramatic shift in sentiment for the market’s permanent cheerleaders. More concerning, perhaps, is that, by most measures, Main Street remains all in. Consider that the share of household assets invested in stocks ended 2021 at the highest extreme in history. The last two times allocations approached these levels, equity markets were flat to down for the following decade (see chart below).

{kind=link}

We need to see much greater capitulation before a significant market bottom is in place, and household equity allocations much lower before expected returns move materially higher.

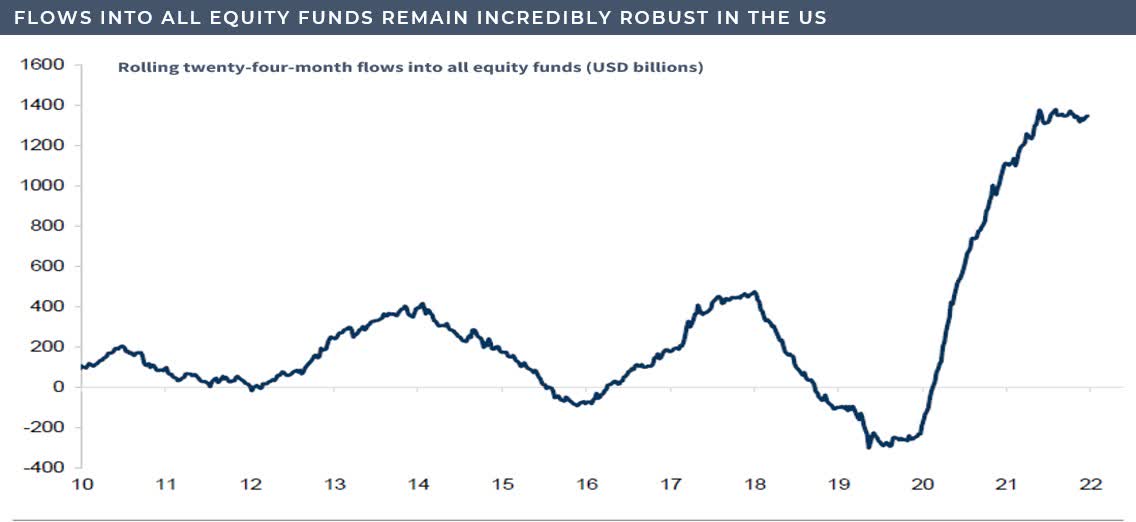

While a number of signs point to increased risk aversion, actions always speak louder than words. And curiously, inflows into equity funds have remained robust, even amidst last year’s decline, with continued flows into the most speculative corners of the market. Investors have yet to throw in the towel. Even Cathie Wood - down 80% - still saw cumulative inflows of ~$2B last year!!!!

{kind=link}

When your kids and grandkids ask you what the “Everything Bubble” of the early 2020s was like, you can just show them this clip from CNBC , during which an interview went sharply south following a seemingly simple question: “What kind of company is it? What do they do?” Well, apparently it’s the kind of company that peaked at $401 per share on October 15, 2021, and hit a recent low of $12. Guess when this clip aired?

I started my career in the late 90s. What we just experienced felt like the late 90s on steroids. Many investors during that period got carried out with the tide. But others survived and even thrived. Such extreme swings in investor psychology can create extreme opportunities. This occurs when market regimes evolve over a long enough timeframe that widespread beliefs become engrained in conventional wisdom. As a result, the consensus continues to chase the winners of the prior cycle.

After the tech bubble burst, with the NASDAQ down ~ 80% from its peak, many investors looked to buy beaten-down tech stocks. The same stocks that led the market higher for years. This may seem logical. Anything down 80% must be a better bargain than stocks that declined much less or even increased in value over that same period. But that’s not how this works. Price is not the same as value. Stocks that are down 80% can still be a bad investment.

Those who continued to chase growth stocks – last cycle’s winners – underperformed value for the better part of the next decade. As this cycle has played out in almost identical fashion to date, we think it’s safe to assume that the pattern will continue as markets revert back to reality.

It takes a long time for beliefs, ingrained over a decade, to change their course. This is why Cathie Wood, and other more aggressive investors, are still seeing inflows, even after last year’s devastating losses. Investors refuse to throw in the towel on what worked for so long. But throughout history, winners of the last regime have lost their luster in order to make room for a new cohort.

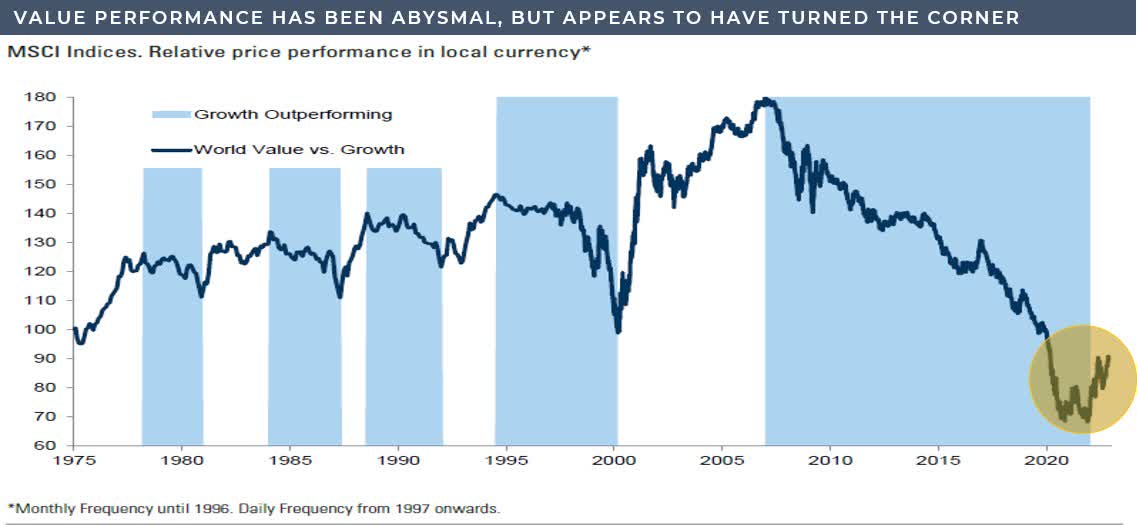

We don’t expect this time to be any different. We think value will continue to quietly outperform for years, just as it did during the last cycle. After underperforming by nearly 150% in the five years prior to the tech bubble’s peak, value indices went on to trounce growth as the bubble deflated. And despite the early pain, patient investors were ultimately rewarded for their perseverance: value outperformed over the full period by a wide margin.

{kind=link}

Markets have taken their first step toward normal, but we still have a long ways to go. After the longest and most severe period of value underperformance in history, we expect the next several years to look like the mirror image of the past. We believe Broyhill is well positioned for this environment and for the return of fundamental investing.

Value has pretty much been out of favor since the inception of our equity strategy, and yet we’ve managed to outperform by just about any measuring stick.

We are excited to see what we can do if that multi-year headwind transitions to a tailwind in the years to come.

{kind=link}

BOTTOM LINE

After such a challenging year, it’s natural to question what lies ahead. To us, the world has never looked better. The most extreme excesses have been cleared from the market. Although the broader indices remain expensive and may have further to fall, they are unquestionably cheaper than prices available twelve months ago. More importantly, for disciplined, value-driven investors, a lot more assets are available at a lot cheaper prices than those broad market indices.

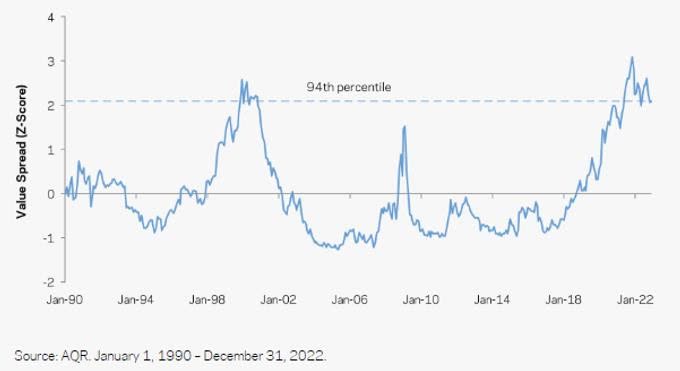

While cheap stocks can get cheaper during a bear market, the first leg down is usually the most unforgiving, with securities falling in unison under the heavy weight of gravity. As the bear market matures, valuation becomes an increasingly important driver of returns leading to greater differentiation and dispersion across assets. It is at this point that Mr. Market begins to separate the wheat from the chaff and active management can truly earn its keep. Having survived the initial leg down with our capital intact, we are well positioned to capitalize on the broadening opportunity set ahead, as the spread between value and growth still remains at historical extremes, even after value’s record, recent outperformance.

GLOBAL VALUE SPREADS

{kind=link}

We are grateful for your continued trust and partnership. We come into the office each day striving to earn it, and we realize just how fortunate we are to have such a wonderful group of like-minded, long- term investors who place their confidence in us. You enrich our network, strengthen our competitive advantage, and just make our work all the more enjoyable.

As always, please feel free to reach out at any time with questions. We enjoy hearing from you.

Sincerely,

Christopher R. Pavese, CFA

| 1 For the sake of simplicity and to maintain our sanity while trying to interpret the SEC’s new marketing rules, all reported performance on individual shares discussed in this letter, are reported on a time-weighted return basis for the relevant period (in this case, for the calendar year ending December 202), net of a 1.5% annual management fee, which is our highest stated management fee Broyhill’s internal rate of return on each investment may differ slightly from those reported here, depending on the timing of our investment and any subsequent sales or additions to the position. 2 Meta to Lay Off Thousands of Staff From This Week, WSJ Says 3 The word “moochers” here, is the technical term we use for those Netflix subscribers “borrowing” log-in credentials for friends and family. In our NFLX model, our “moochers” line item represents a considerable source of upside optionality, with the added benefit, of making us laugh, every time we update our assumptions for this line item in the model. |

DISCLOSURESBroyhill Asset Management LLC (“BAM”) is an investment adviser in North Carolina. BAM is registered with the Securities and Exchange Commission (SEC). Registration of an investment adviser does not imply any specific level of skill or training and does not constitute and endorsement of the firm by the Commission. BAM only transacts business in states in which it is properly registered or exempted from registration. A copy of BAM’s current written disclosure brochure filed with the SEC which discusses among other things, BAM’s business practices, services and fees is available through the SEC’s website at www.adviserinfor.sec.gov. Performance calculation methodology. The performance of the Broyhill Equity Portfolio illustrated here is representative of the fully invested strategies available through various TAMPs (Turnkey Asset Management Platforms). The majority of BAM’s SMAs include a significant cash allocation, which has averaged 30% - 40% in recent years, and also utilize options to compliment individual position sizing and to hedge the portfolio as appropriate for individual clients. As a result, we believe that the historical performance of our flagship strategy (which includes both options and a significant cash drag) is not representative of a pure equity allocation. As such, this data may be useful for an advisor evaluating Broyhill, although individual results may differ based on each account's investment objectives, the date of initial funding, the opportunity set available at the time, specific investment vehicles available to the accounts, and individual fee schedules. These historical performance figures are for our equity-only strategy. Performance is calculated using time-weighted rates of returns, net of fees. Since these platforms report returns to Broyhill gross of fees, in order to report net returns, a 1.5% annual management fee has been subtracted from gross reported returns. This methodology has also been applied to the extracted attribution returns. Average position size is calculated from average capital invested divided by average portfolio capital in fully-invested accounts. The investment return and principal value of an investment will fluctuate. Therefore, an investor's account, when liquidated or redeemed, will almost always have a different value than that shown herein. Current performance may be lower or higher than return data quoted herein. Past performance is not indicative of future returns. This information should not be used as a general guide to investing or as a source of any specific investment recommendations and makes no implied or expressed recommendations concerning the manner in which an account should or would be handled, as appropriate investment strategies depend upon specific investment guidelines and objectives. Information presented herein is subject to change without notice and should not be considered as a solicitation to buy or sell any security. This document contains general information that is not suitable for everyone. The information contained herein should not be construed as personalized investment advice. There is no guarantee that the views and opinions expressed in this document will come to pass. Investing in the stock market involves gains and losses and may not be suitable for all investors. No representations, expressed or implied, are made as to the accuracy or completeness of such statements, estimates or projections, or with respect to any other materials herein. Under no circumstances does the information contained within represent a recommendation to buy, hold or sell any security, and it should not be assumed that the securities transactions or holdings discussed were or will prove to be profitable. There are risks associated with purchasing and selling securities and options thereon, including the risk that you could lose money. Certain information contained herein constitutes “forward-looking statements,” which can be identified by the use of forward-looking terminology such as “may,” “will,” “should,” “expect,” “anticipate,” “project,” “estimate,” “intend,” “continue,” or “believe,” or the negatives thereof or other variations thereon or comparable terminology. Due to various risks and uncertainties, actual events, results or actual performance may differ materially from those reflected or contemplated in such forward-looking statements. Nothing contained herein may be relied upon as a guarantee, promise, assurance or a representation as to the future. Market value information (including, without limitation, prices, exchange rates, accrued income and bond ratings furnished herein) has been obtained from sources that Broyhill believes to be reliable and is for the exclusive use of the client. Market prices are obtained from standard market pricing services or, in the case of less liquid securities, from brokers and market makers. Broyhill makes no representations, warranty or guarantee, express or implied, that any quoted value necessarily reflects the proceeds that may be received on the sale of a security. Changes in rates of exchange may have an adverse effect on the value of investments. Indices represent unmanaged, broad-based baskets of assets. They typically used as proxies for overall market’s performances. Index returns typically assume that dividends are reinvested and do not include the effect of management fees or expenses. You cannot invest directly in an index. Without prior written permission of index owner, this information and any other index-related intellectual property may only be used for your internal use, may not be reproduced, or redistributed in any form and may not be used to create any financial instruments or products or any indices. This information is provided on an "as is" basis, and the user of this information assumes the entire risk of any use made of this information. Neither the index owner nor any third party involved in or related to the computing or compiling of the data makes any express or implied warranties, representations or guarantees concerning the index-related data, and in no event will index owner or any third party have any liability for any direct, indirect, special, punitive, consequential or any other damages (including lost profits) relating to any use of this information. Investing in some private funds are limited to persons who are “qualified purchasers” (as defined in the United States Investment Company Act of 1940, as amended (the “Investment Company Act”)) and “accredited investors” (as defined in Rule 501(a) under the Securities Act). Such securities will not be registered under the Securities Act or qualified under any applicable state securities. For additional information about other indices or strategies mentioned here, you may contact us at info@broyhillasset.com. No part of this material may be copied, photocopied, or duplicated in any form, by any means, or redistributed without Broyhill’s prior written consent. |

Editor's Note: The summary bullets for this article were chosen by Seeking Alpha editors.

For further details see:

The Broyhill Q4 2022 Letter