TCS - The Container Store: 3D Testing Lower Costs And Undervalued

2023-10-13 08:40:38 ET

Summary

- The Container Store Group, Inc. is undervalued but has taken steps to lower expenses and enact a stock repurchase program.

- The company offers storage and space management services to homeowners and has a national reach within the United States.

- Analysts expect positive net sales growth and improved financial figures in 2025 and 2026, which could lead to an improvement in stock performance.

The Container Store Group, Inc. (TCS) trades right now even more undervalued than when I wrote in my previous article . However, I believe that management recently reacted well by lowering its selling, general, and administrative expenses and stock-based compensations as well as enacting a stock repurchase program. I also believe that the 3D facilities for product testing and further efforts to deepen relationships with clients will most likely bring FCF growth. There are challenging macroeconomic conditions, and interest expenses have increased recently. However, like other investment analysts, I believe that future financial figures in 2024 and 2025 will most likely improve.

Business Model

With a portfolio that includes storage and space management services with customized functions for each client, Container Group Store is a company with national reach within the United States that has more than 50 years of uninterrupted activity today.

Clients are primarily homeowners who hire the company through its various brands for space and storage solutions, although its services also extend to other specialty areas. The company's stores include 14 lines of lifestyle products that aim to attract a wide range of customers with different payment capabilities. Among its products we can find a wide variety of final applications such as suitcases, clothing storage products, shoes, kitchen utensils and desk chairs among others.

The activities are distributed in two business segments: Elfa and The Container Group Store. First of these segments is a subsidiary under its ownership and with facilities located in Sweden that dedicates its production to shelving for use in kitchens, bathrooms, and closets among other applications. In addition to two production facilities in Sweden, it also has one production facility in Poland.

On the other hand, the segment that bears the same name of the company is the one that covers the historical businesses of this company. It currently has 27 stores distributed in 34 states throughout the United States. Products are marketed through outsourced channels. The Container Group Store has direct channels to its customers through its distribution stores and mobile devices and online commerce stores.

Beneficial Market Expectations

I believe that the expectations of other market participants are quite beneficial, and should be mentioned.

Most analysts out there are expecting positive net sales growth in 2025 and 2026, along with positive net income and FCF in 2026. Overall, in my opinion, the company is expected to deliver better financial figures in 2026 than that in 2023 and 2024. As a result, if the final figures are as expected, I believe that we could see an improvement in the stock performance.

More in particular, 2026 net sales are expected to be close to $962 million, with net sales growth of about 6%, 2026 EBITDA of close to $94.05 million, and 2026 EBIT close to $41.8 million. Also, with operating margin of about 4.39%, 2026 net income would be close to $14.65 million, with EPS of 0.3 per share and 2026 FCF of $24.8 million. My figures are not very different from the expectations of other market participants, so I believe that investors may want to have a look at them.

Source: S&P

Deepening Customer Relationships, Executing Geographic Expansion, And Lowering Manufacturing Costs Will Most Likely Lead To FCF Growth

I expect that Container Group Store will be able to deepen the relationships with its customers, expand its geographical base through the opening of new stores, and increase its sales through digital channels.

Besides, further increase in its productive capacities along with the reduction in general costs in the manufacturing of its products may bring FCF margin growth. In this sense, the adaptation of its stores to approach its customers with different facilities such as 3D facilities for product testing and the training of its salespeople may also play a fundamental role.

New Catalyst: Further Decreases In Selling, General, And Administrative Expenses As Well As Stock-based Compensation May Bring FCF Growth

We saw how net income fell in 2023 as well as total sales. In addition, it should be noted that the maintenance costs of sales channels have increased, which is why operating results are having a decrease over the year. I believe that this is largely justified by the recent economic conditions and the lack of consumer access to liquidity or credit.

Source: Ycharts

With that, there is new information that I did not include in my previous article. Like other analysts, I believe that 2024 may also bring negative net income, however financial figures, in the coming future, may be better than that in 2023. In the last quarterly report, we already saw a decrease in selling, general, and administrative expenses in the thirteen weeks ended July 1, 2023 as compared to the thirteen weeks ended July 2, 2022. Besides, Container Group Store decreased its total stock based compensations. In my view, further reduction in these costs may bring a positive profit margin in the coming years.

Source: 10-Q

The Stock Repurchase Program Could Accelerate The Demand For The Stock

Container Group Store reacted to recent lower net income figures by lowering selling, general, and administrative expenses. The Board of Directors approved a stock repurchase program, which may enhance the demand for the stock in the coming months.

Our board of directors approved a stock repurchase program with authorization to purchase up to $30,000 of our common stock. Source: 10-Q

We expect to fund repurchases with existing cash on hand. As of July 1, 2023, $25,000 remains available to repurchase common stock under the share repurchase program. Source: 10-Q

Considering the recent destruction of value, I believe that making a stock repurchase program when the stock price is around $2 per share appears brilliant. Let's keep in mind that the company traded at $15 per share in 2021.

Source: Ycharts

With The Previous Assumptions And A Conservative DCF Model, I Believe That The Stock Is Quite Undervalued

In my previous article , I did not include recent cost decreases and other new catalysts like the stock repurchase program. With these new assumptions, I included a cost of capital that is slightly better than that mentioned in the article published in February. Besides, my EV/FCF multiples are close to 8x-11x, a bit better than what I assumed a few months ago, because other competitors seem to be trading at those valuation multiples. With that, the median price forecast obtained is a bit lower than what I reported previously because my FCFs expectations are a bit lower. In any case, given my figures in my previous report and the figures published now, the company continues to remain very undervalued.

I obtained equity of $204.67 million, a fair price of $4.05 per share, and an internal rate of return of -6.88%. Source: The Container Store: Store Growth Could Ignite Stock Price

My financial model includes 2032 net income of about $15 million, depreciation and amortization worth $61 million, and stock-based compensation less than $1 million. I did not include impairment charges, losses on disposal of assets, or losses on extinguishment of debt because I think that these are extraordinary events.

{kind=link}

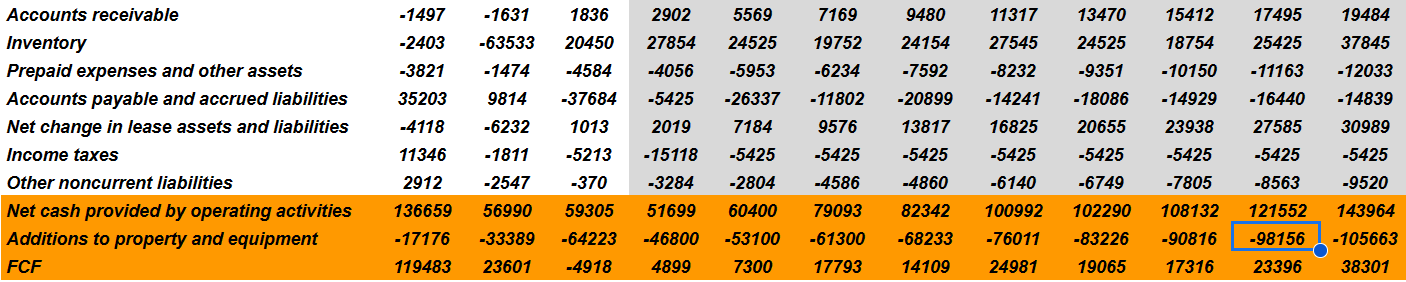

In addition, with changes in accounts receivable of close to $19 million, changes in inventories of $37 million, and prepaid expenses and other assets worth -$13 million, I assumed changes in accounts payable and accrued liabilities worth -$15 million.

Besides, assuming net change in lease assets and liabilities worth $30 million, changes in income taxes of close to -$6 million, and changes in other noncurrent liabilities worth -$10 million, 2032 CFO would be worth $143 million. Finally, with additions to property and equipment of close to -$106 million, 2032 FCF would be worth about $38 million.

{kind=link}

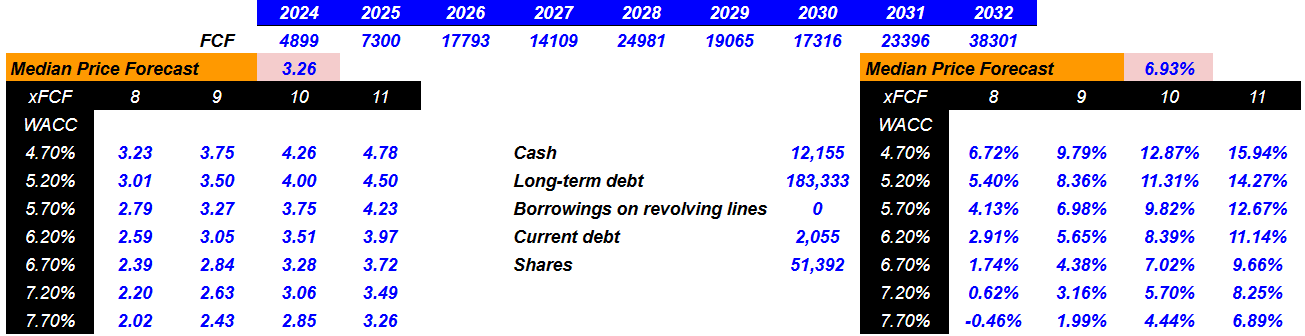

Now, my forecasts include future FCFs of close to $4 million and $38 million from 2024 to 2032. Note that I included a WACC of about 4.7%-7.7%, so I believe that my figures are conservative. If we also include an implied terminal EV/FCF of 8x-11x, which appears close to the sector median multiples, the implied forecasted price would be $4.78-$2.02 per share, with a median price forecast of $3.26 per share. The median IRR would stand at close to 6.9% with a maximum IRR of 15%-16%.

Source: Ycharts Source: DCF Model

{kind=link}

Balance Sheet

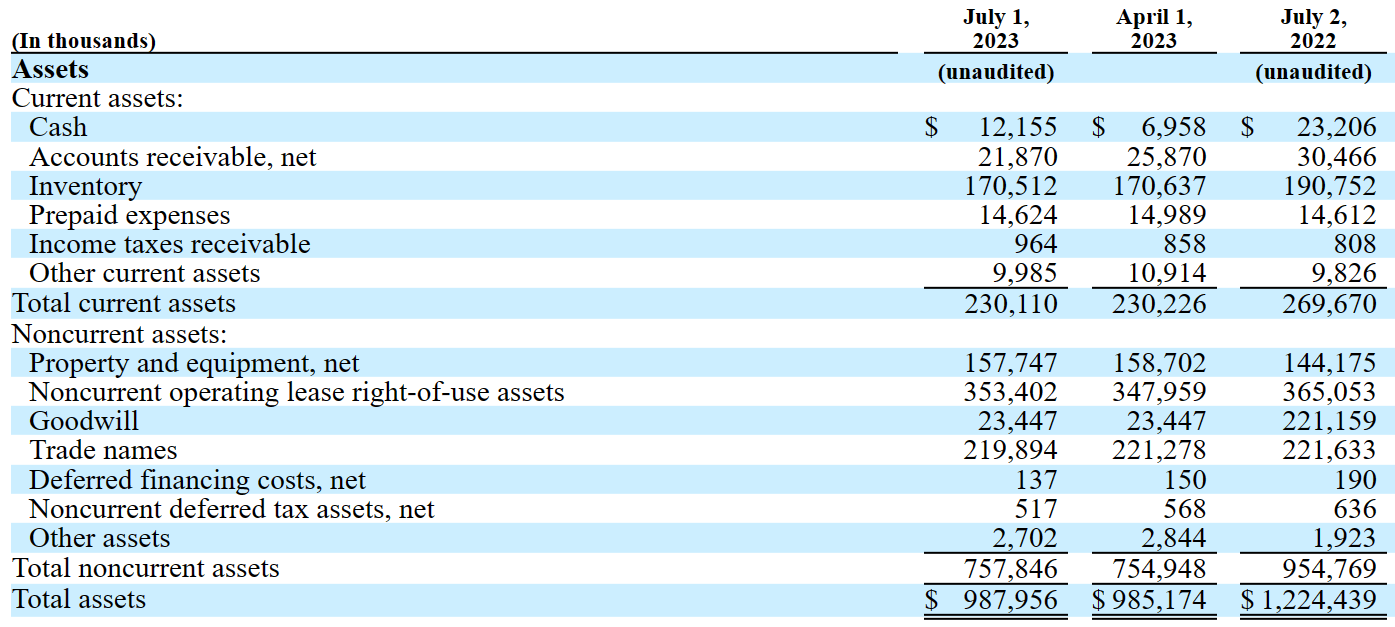

As of July 1, 2023, Container Group Store reported cash close to $12 million, with accounts receivable of about $21 million, inventory of $170 million, and prepaid expenses worth $14 million. Total current assets stood at about $230 million, and the current ratio was larger than 1x. I would not expect liquidities issues here.

Besides, with property and equipment worth $157 million, noncurrent operating lease right-of-use assets of about $353 million, and goodwill of $23 million, total assets stand at close to $987 million. The asset/liability ratio is larger than 1x, so I believe that the balance sheet appears quite stable.

{kind=link}

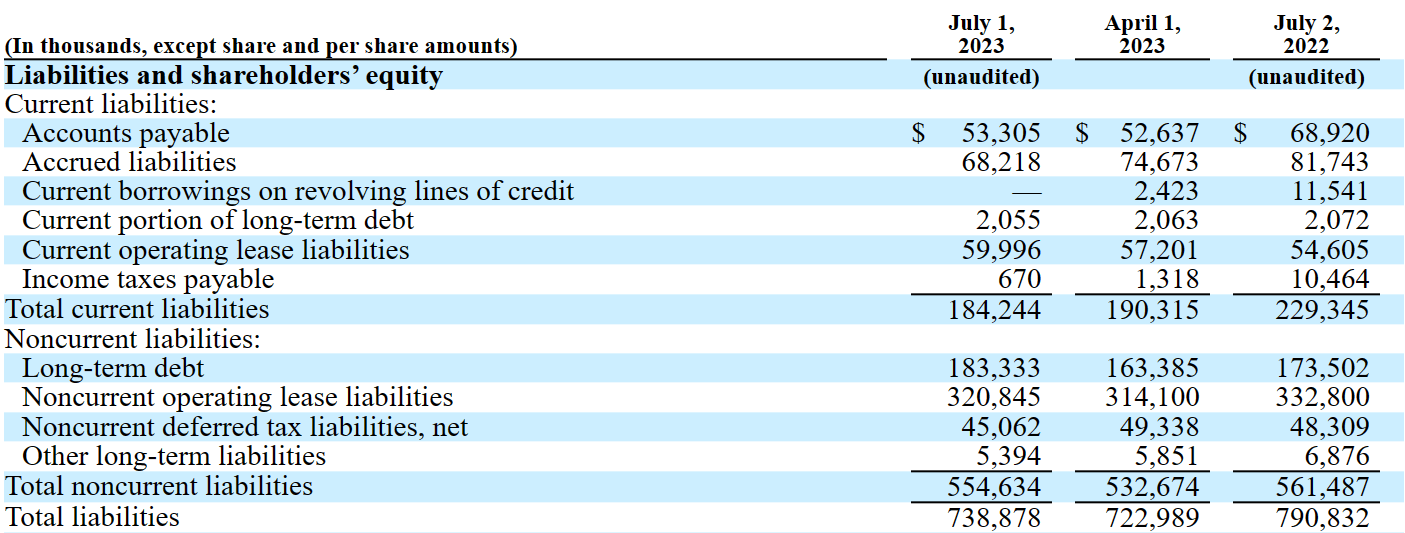

Container Group Store reported accounts payable worth $53 million, accrued liabilities of $68 million, and current borrowings on revolving lines of credit of close to $2 million. Besides, with long-term debt of about $183 million and noncurrent operating lease liabilities close to $320 million, total liabilities were equal to $738 million.

I really do not think that the total amount of debt is an issue, however I studied a bit the cost of capital to include some assumptions in my financial model.

{kind=link}

Container Group Store reported debt related to the LIBOR and interest rate close to 4.7%-5%. With this in mind, I believe that assuming interest rates at a bit more than 4.7% makes sense. In this regard, Container Group Store reported the following text.

Prior to the date of delivery of a compliance certificate for the fiscal year ended April 1, 2023, the applicable interest rate margin for LIBOR loans was 4.75%, subject to a LIBOR floor of 1.00%, and 3.75% for base rate loans and, thereafter, may step up to 5.00% for LIBOR Loans and 4.00% for base rate loans unless the consolidated leverage ratio achieved is less than or equal to 2.75 to 1.00. As of April 1, 2023, the aggregate principal amount in outstanding borrowings under the Senior Secured Term Loan Facility was $160,312, net of deferred financing costs, and the consolidated leverage ratio was approximately 1.4. Source: 10-k

Competitors

Although Container Group Store may declare itself as the only company that is dedicated exclusively to storage and space management services in homes, competition is high, and in many cases, the competitors who only allocate part of their efforts to these areas of sales have greater resources and reach over their marketing capabilities. Along with these companies of international reach, there are also a number of independent builders, real estate companies that develop homes, and smaller companies with regional reach to specific markets.

Risks

Changing macroeconomic conditions play an important role in the risk analysis of this company. As a result of the inability of consumers to pay and necessary price changes of the company's products, the company may suffer decreases in both net sales and the profit margins.

Macroeconomic conditions have caused and may continue to cause the need to adjust prices to offset the effect of these changes, and we may not be able to do that without negatively impacting consumer demand or our gross margin. Source: 10-k

The company may also fail to open new stores, or new stores may not be profitable for a variety of reasons. Lack of personnel could also significantly affect Container Group Store, which may lower efficiency, and may also harm FCF margin growth.

We must successfully choose store sites, execute favorable real estate transactions on terms that are acceptable to us, hire competent personnel and effectively open and operate these new stores. Our plans to increase our number of retail stores will depend in part on the availability of existing retail stores or store sites. Source: 10-k

We can add the risks involved in the international exposure due to the management of its Elfa subsidiary. In my view, the company may find that what works well in some countries does not work that well in others. Besides, new types of competitors or regulations may show up in new jurisdictions.

I also believe that increases in interest rates may lower FCF margin growth. As a result, the cost of capital could increase, which may lower the stock valuation of DCF models executed by investment analysts. In this regard, it is worth noting that we saw an increase in interest rates in the last quarter.

Interest expense increased by $1,744, or 54.1%, in the thirteen weeks ended July 1, 2023 to $4,967, as compared to $3,223 in the thirteen weeks ended July 2, 2022. The increase is primarily due to a higher interest rate on the Senior Secured Term Loan Facility. We expect to incur higher interest expenses during fiscal 2023, as compared to the previous fiscal year, as a result of rising interest rates. Source: 10-q

Conclusion

Container Group Store recently reported a promising decrease in selling, general, and administrative expenses as well as stock-based compensations. I believe that further cost reductions along with 3D facilities for product testing and deepening relationships with clients will most likely bring FCF growth. I do see risks from further increases in interest expenses, failed opening of new stores, or changing macroeconomic conditions, however I continue to believe that the stock is undervalued.

For further details see:

The Container Store: 3D Testing, Lower Costs, And Undervalued