XRT - The Container Store Group: Bed Bath & Beyond Bankruptcy May Spark Rally

Summary

- The Container Store looks to benefit handsomely from the looming bankruptcy of competitor Bed Bath & Beyond.

- A 10-year low valuation could support a multi-year run higher for the share quote.

- Strong levels of operating profitability and store count growth are other positives to consider.

As investors and creditors prepare for the high likelihood of a Bed Bath & Beyond ( BBBY ) bankruptcy, talk of who would actually benefit from a reduction in competition has been increasing. My vote for the biggest winner would be The Container Store Group ( TCS ).

There are three reasons why I come to this conclusion. (1) Few national chains successfully compete in the focused area of organization supplies, containers, kitchenware, personalized office furniture, etc. Sure, a number of general merchandise companies like Target ( TGT ) and Walmart ( WMT ) sell a few related items. Amazon ( AMZN ) and Wayfair ( W ) compete on a long list of products, but without local showrooms with immediate personal choice out of inventory. If you want a pick that should see larger crowds in the store as a direct consequence of Bed Bath & Beyond closing its locations, look no further.

(2) The Container Store is quite small, so the impact of new foot traffic could be a major pull for sales and income. At an equity market capitalization of $280 million and enterprise value of $750 million (including $323 million in building leases), even a small rise of say 10% ($110 million) on $1.1 billion in trailing revenue through October 2022 could generate a very big jump in final income numbers ($63 million for trailing, after-tax, non-GAAP cash income).

(3) The share valuation is at a 10-year low, meaning no material bump in results is currently expected by Wall Street. In fact, investors appear to be preparing the valuation for a probable recession. Such opens up the mispriced and undervalued opportunity for new buyers.

The Bargain Valuation Story

Besides hitting one of my reversal quant-sort formulas in the last week, the most intriguing part of the investment argument for TCS is its incredibly inexpensive, sentiment blowout valuation in early 2023.

Below is a 10-year graph of the share price versus trailing earnings and sales, with forward forecasts also drawn. You can quickly determine The Container Store is today priced near its cheapest setup over the last decade. On price to sales, only a few months of COVID pandemic-related closures and investor fears were able to produce a lower reading on trailing results than now.

YCharts - The Container Store, Price to Earnings & Sales, Since 2013

Secondly, when we include existing debt and cash holdings, enterprise valuations can be argued as even less expensive for new buyers. Using both trailing and forward analysis, TCS is a deeper bargain today than at any point during the fateful retail year of 2020. It may be the sub-$5 prices of November to January prove to be the decade low-water mark for a valuation.

YCharts - The Container Store, EV to EBITDA & Revenue, Since 2014

Lastly, management appears aware free cash flow generation is the key to keeping the doors open at a physical retail business. The company has consistently been free cash flow positive since 2014.

YCharts - The Container Store, Trailing Free Cash Flow Yield, Since 2014

Technical Trading Shift Underway?

Since November, rumors that Bed Bath & Beyond was facing its last Christmas sales season have persisted. And, in January, BBBY missed debt payments and warned of an imminent bankruptcy filing.

Over the same span, The Container Store has reversed higher in price, after falling all of 2022. Below is a 3-month graph of total return performance from TCS and BBBY, plus the main SPDR S&P Retail ETF ( XRT ).

YCharts - Retailer Total Returns, 3 Months

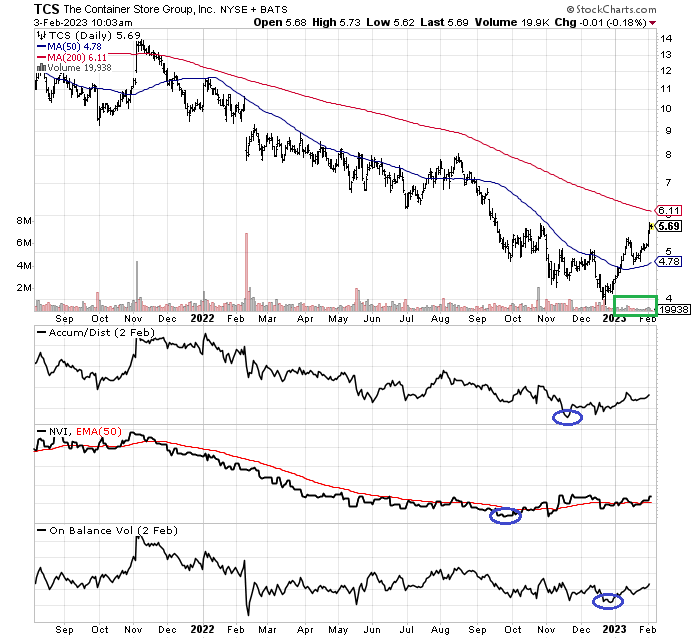

What I like most on the daily trading chart is volume sellers have disappeared since Christmas 2022 in The Container Store share supply/demand marketplace. I have boxed in green below on an 18-month chart, the super-low trading volume each session in January coinciding with a decent percentage price rise. This situation smacks of a shortage of sellers, meaning any good news put out by the company could push price straight up.

In addition, many of my favorite momentum indicators bottomed between September and December (circled in blue). Much better indicator performance may be hinting the bottom in price has been reached, and a long-term zigzag higher has begun.

StockCharts.com - The Container Store, 18 Months of Daily Price & Volume Changes, Author Reference Points

{kind=link}

Final Thoughts

The company is in the midst of substantial growth in store counts over the next four years, with an ambitious goal of opening 76 new locations by 2027 (from 95 today). Seeking Alpha contributor Malak Investment Ideas wrote a nice effort this week here explaining a modeled $10 fair value, share price for the company. Considering my undervaluation data, a $10 target by the end of 2023 seems within the realm of likely outcomes for investors. From $5.70 currently, such a rise would produce a total return of +75%.

Of course, the usual retail risks still apply to The Container Store. Expanding too fast with debt financing might prove a risky strategy. Rising labor costs and inflating wholesale goods pricing could be future profit margin issues. One point of good news is the company routinely scores as a top place to work in national surveys. Most importantly, a serious recession this year could prove a major headache for management.

My goal is to buy on any weakness appearing in February, perhaps back to $5.25 to $5.50. Such a retracement may not take place, for a variety of reasons. So, if you are interested in the upside logic, buying at $5.70 should work out just fine for a 1-year or longer time horizon.

I peg downside potential in a deep recession back to $4.00 a share, roughly -30% on the risk side of the equation over the next 12 months. However, upside potential may be well above $10, because of customers shifting dollars from Bed Bath & Beyond coffers to The Container Store, a steep undervaluation setup, and store growth picking up steam. This +75% in best-case scenario upside represents above-normal bullish potential vs. the vast majority of stocks available on Wall Street.

Thanks for reading. Please consider this article a first step in your due diligence process. Consulting with a registered and experienced investment advisor is recommended before making any trade.

For further details see:

The Container Store Group: Bed Bath & Beyond Bankruptcy May Spark Rally