TCS - The Container Store: Weak Sales Trends And Lack Of Catalysts

2023-08-21 21:00:24 ET

Summary

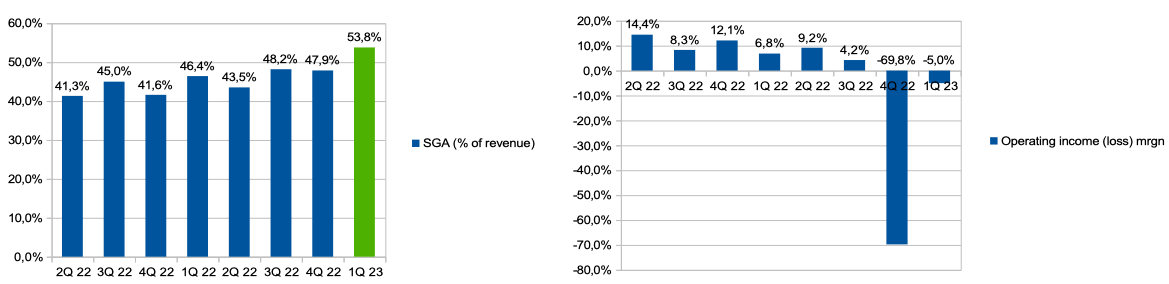

- The company's revenue decreased by 21.1% YoY, while operating loss (% of revenue) reached 5%.

- SGA spending (% of revenue) increased to 53.8% due to reduced economies of scale.

- I expect pressure on top line growth and operating margin to continue in the coming quarters.

Introduction

Shares of The Container Store Group ( TCS ) have fallen 43% YTD. Despite the fact that the company's stock is relatively cheaply priced by multiples, I believe it's still not the best time to go long.

Investment thesis

I believe that in the coming quarters we will see continued pressure on both the business's revenue growth and operating margins. First, I don't expect that we can see a quick recovery in traffic and average check in stores, because, in my personal opinion, consumer spending will recover with a delay, even if we see a decrease in inflation. Secondly, reduced economies of scale may lead to additional pressure on profitability, since a high proportion of operating expenses (rent, salaries) are fixed. In addition, the company provided weak guidance for 2023 (fiscal).

Company overview

The Container Store company sells specialized solutions (organizer for cosmetics, jewelry, etc.) for organizing spaces. The main business segments are The Container Store (94 of revenue) and Elfa (6% of revenue). The company operates in the US market.

1Q 2023 (fiscal) Earnings Review

The company's revenue decreased by 21.1% YoY due to a decrease in comparable sales by 19.9% ??YoY. In The Container Store segment (94% of total revenue), revenue decreased by 20.9% YoY, while sales in the online segment decreased by 10.6% YoY. Thus, the share of online sales in the retail segment increased from 21.3% in Q1 2022 (fiscal) to 24.1% in Q1 2023 (fiscal). In the Elfa segment, the company's revenue decreased by 24.4% YoY.

Gross profit margin decreased from 57.1% in Q1 2022 (fiscal) to 55.3% in Q1 2023 (fiscal) due to investment in prices and an increase in the share of online sales, which are less profitable for the company due to additional shipping costs.

Gross margin trend (Company's information)

SGA spending (% of revenue) increased from 46.4% in Q1 2022 (fiscal) to 53.8% in Q1 2023 (fiscal) due to reduced economies of scale. Thus, operating margin decreased from 6.8% in 1Q 2022 (fiscal) to negative 5% in 1Q 2023 (fiscal).

{kind=link}

In addition, I would like to note that the company has lowered its guidance for the next quarter and 2023 (fiscal). I would like to emphasize that the 2022 operating profit figure (fiscal) in the chart below does not include the $197.7mn asset impairment charge that the company incurred in Q3 2022 (fiscal). I made this adjustment for a more accurate comparison. You can see the details in the chart below.

Guidance 2023 (fiscal) (Company's information)

My expectations

Despite the fact that the company's guidance suggests a decline in revenue and profitability , I believe that the financial performance could be even worse. The company's revenue is under pressure both from traffic, which is under pressure due to macro headwinds, and from the average check, because the company operates in a highly competitive sector, where price increases can lead to additional pressure on traffic in the chain's stores and, accordingly , declining market share.

The expected decline in comparable store sales is reflective of a slower than expected start to the second quarter in terms of customer traffic and average ticket.

In addition, the effect of deleverage in the form of reduced economies of scale can have an additional negative impact on the level of operating profitability, because the company cannot effectively reduce most of the operating costs that are fixed (rent and salaries). In addition, the current guidance of the company suggests that spending on SGA (% of revenue) should be about 50% of revenue, however, if we look at the results for 1 quarter, we can see that spending on SGA (% of revenue) amounted to about 54%. So, I think that in terms of pressure on revenue in the coming quarters, operating income may be worse than investors' expectations.

Risks

Competition: the high level of competition in the sector can lead to pressure on both store traffic and average check, because price is one of the main competitive advantages in retail.

Margin: additional investments in marketing and pricing due to increased competition can lead to a decrease in the operating profitability of the business.

Macro (general risk): rising interest rates and a decline in real income may lead to a decrease in consumer spending in the discretionary segment, which may lead to a decrease in both the company's revenue growth rates.

Valuation

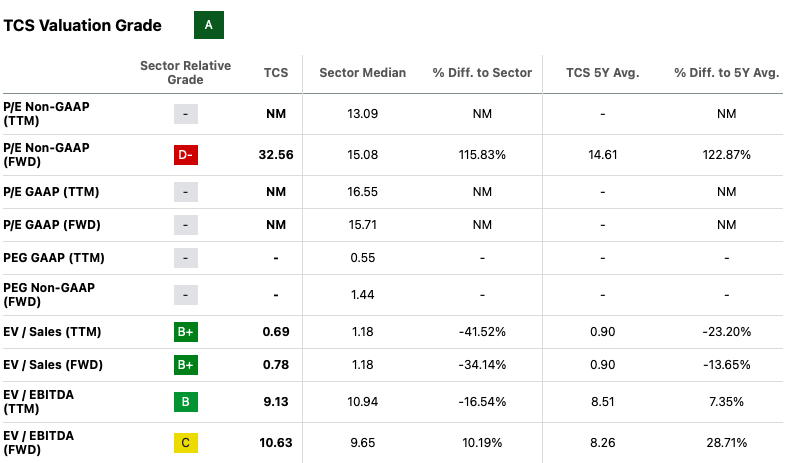

The current Valuation Grade is A. According to the P/S multiple ((FWD)), the company is trading at 0.15x, which is 83% lower than the media sector. However, according to the EV/EBITDA ((FWD)) multiple, the company is trading at 10.6x, which implies a premium of about 10% to the sector media, I think the multiple is at this level due to the abnormally low EBITDA forecast. I believe that the current level of discount fairly reflects the risks that come with investing in the company's shares, I mean negative revenue growth, operating loss, business size and the level of competition in the industry. Thus, I believe that at the moment, investors should not make a decision to buy shares based only on a relatively low valuation.

{kind=link}

Conclusion

Thus, I expect the company's financial performance to continue to be under pressure over the next quarters. I avoid a sell recommendation as the company's stock is not highly valued by multiples, however, I don't see any catalyst for the stock in the short term, so my recommendation is hold.

For further details see:

The Container Store: Weak Sales Trends And Lack Of Catalysts