QVCC - The Curious Case Of Qurate Retail

2023-03-28 08:55:23 ET

Summary

- Qurate Retail's stock price has been decimated in the past two years after a horrible warehouse fire and deteriorating financial results.

- Bond prices for Qurate suggest significant chance of bankruptcy and loss of principal for bondholders.

- If Qurate is able to achieve their Project Athens cash flow goal, returns to equity holders will likely be substantial.

For enterprising investors considering buying a highly levered and shrinking retailer into a consensus recession , have I got a situation for you! Qurate Retail ( QRTEA )( QRTEB ) has been a devastating value trap for over a decade, recently trading back to 2008 lows and down over 90% from 2015 highs. Each of the three chunky dividends in 2020 and 2021 now exceed the share price. Today, ~$350m of equity sits atop a mountain of preferred stock and debt. Let’s dive in.

What is Qurate?

Qurate is the holding company for QVC®, HSN®, Zulily®, Ballard Designs®, Frontgate®, Garnet Hill®, and Grandin Road® (collectively, “Qurate Retail GroupSM”) - the largest US player in “video commerce”. Qurate is part of John Malone’s Liberty empire – Liberty SiriusXM ( LSXMA ), Liberty Broadband ( LBRDA ), Formula One ( FWONA ), the Atlanta Braves, etc.

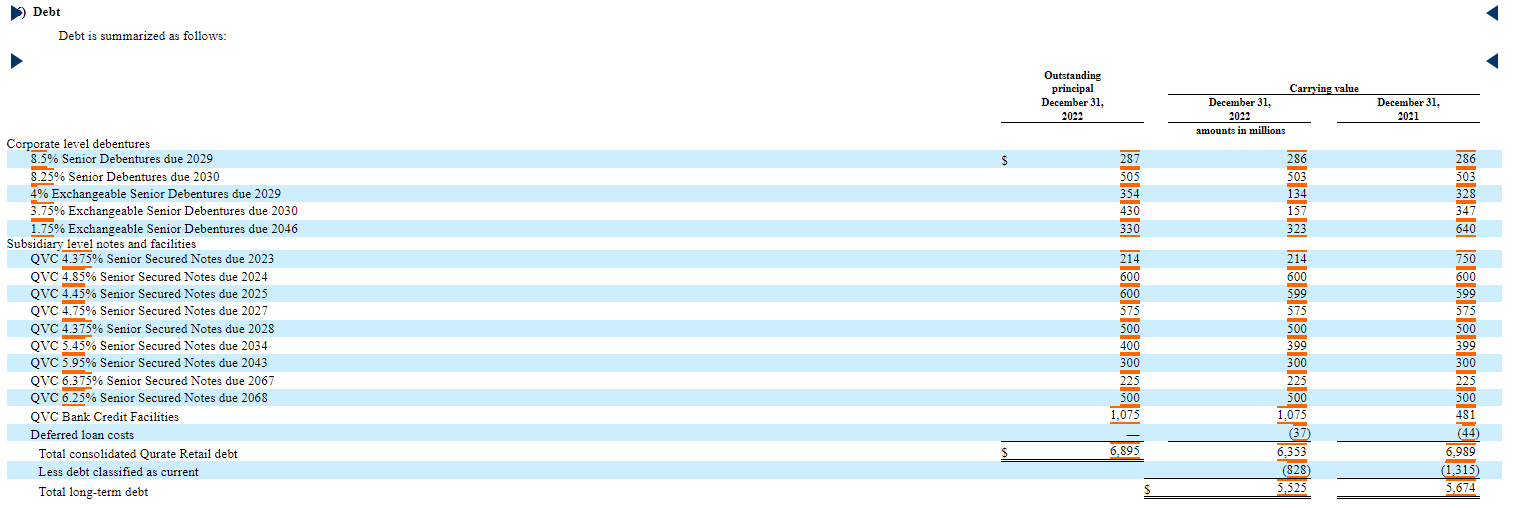

Qurate also is in possession of one of the more interesting publicly traded capital stacks around. There’s $350m of equity (QRTEA & QRTEB), $1.3B face value of 8% preferred shares ( QRTEP ), and $6.9B of bonds, some of which trade on the Nasdaq ( QVCC ) ( QVCD ):

{kind=link}

{kind=link}

But wait, there’s more! The 2029 and 2030 exchangeable debentures can be swapped for shares of T-Mobile ( TMUS ), Lumen ( LUMN ) and the 2046’s can be swapped for shares of Charter Communications ( CHTR ). Or you could look at the unsecured bonds due in 2029, yielding 35% and trading at 20% of face value. Other issues trade poorly too. They at least make more sense than buying the subordinated preferred which yield ~23% (~31% to maturity). There seems to be a pretty interesting, but likely volatile, arbitrage .

There remains $1.275B of cash on the balance sheet at the end of Q4-22 and $182m of real estate proceeds arriving in Q1-23. Management indicated they can sell significantly more real estate if needed but are comfortable with the current liquidity. Business interruption insurance claim discussions are “ongoing” and likely to be material. The company even owns a large chunk of comScore ( SCOR ) preferred shares ( bought for $68m in 2021 ).

How is Qurate Doing?

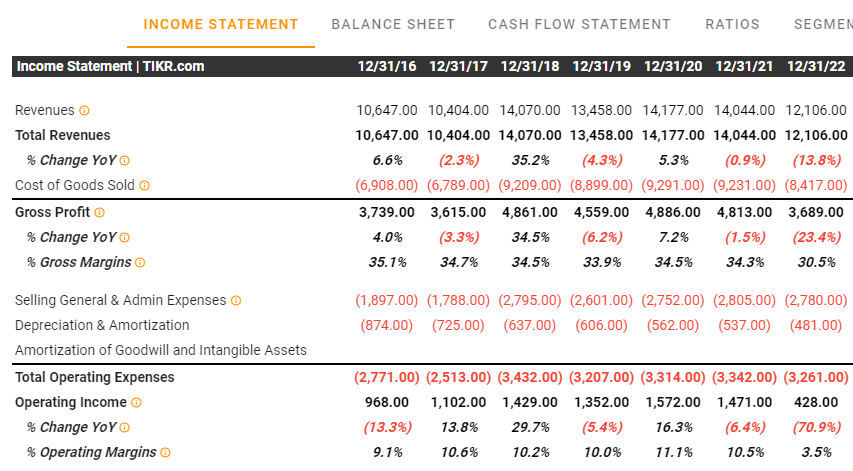

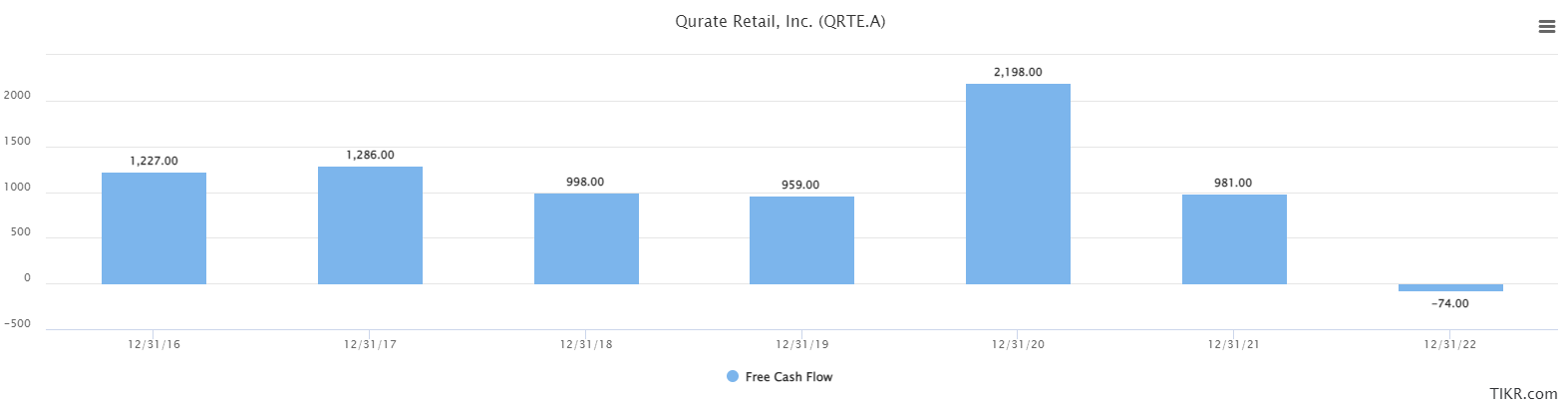

With bonds yielding over 30%, the short answer is “not well”. Right after paying out $1.7B of dividends in the post-Covid fever dream for TV retail, Qurate had a terrible warehouse fire in Rocky Mount, NC. The business has gotten significant insurance proceeds from the fire but spent 2022 with a constrained inventory position inside an already challenging retail backdrop. Management has been clear that they made adverse business decisions to clear stale inventory during 2022 so they could better be positioned for recovery in 2023 and beyond. They have dubbed the turnaround “Project Athens”, and project $300m-$500m of Free Cash Flow ((FCF)) by 2024. Is this realistic? The business operating history suggests it’s possible:

{kind=link}

{kind=link}

Qurate reported essentially flat FCF in 2022, but this was boosted by $693m of sale-leasebacks and $280m of insurance proceeds from the fire and hurt by $150m-$200m of working capital headwinds. So “actual” FCF was closer to negative $800m. There are more levers to pull with owned real estate, and working capital is expected to be a tailwind in 2023. Nevertheless, much work remains to be done to hit the Project Athens targets.

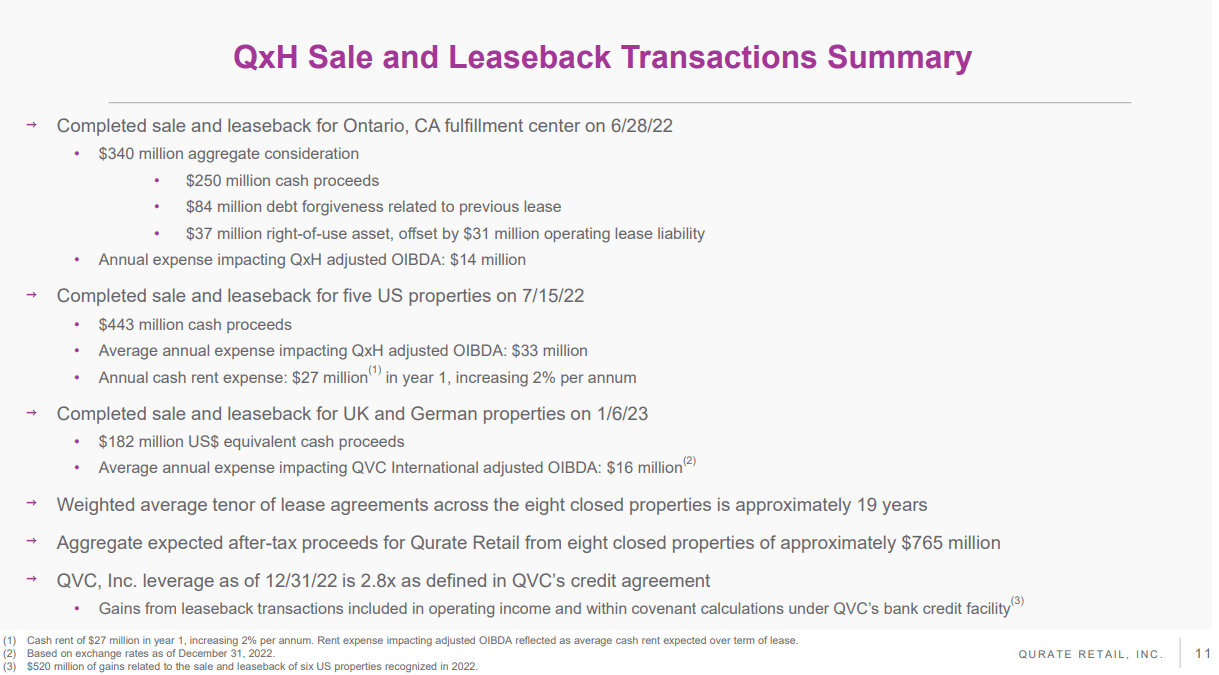

{kind=link}

These transactions improve liquidity and optical cash flow generation but create another $57m of future earnings headwinds (7.5% cap rate: $57m/$765m aggregate proceeds above). If the proceeds can partially be used to retire debt at a discount, the return should be much higher than the headwind. Unfortunately, until more clear evidence of a turnaround is present, Qurate will be constrained to funding their interest payments and maintaining covenants. The cash burn did finally stop in Q4, but it is seasonally their best quarter by a country mile.

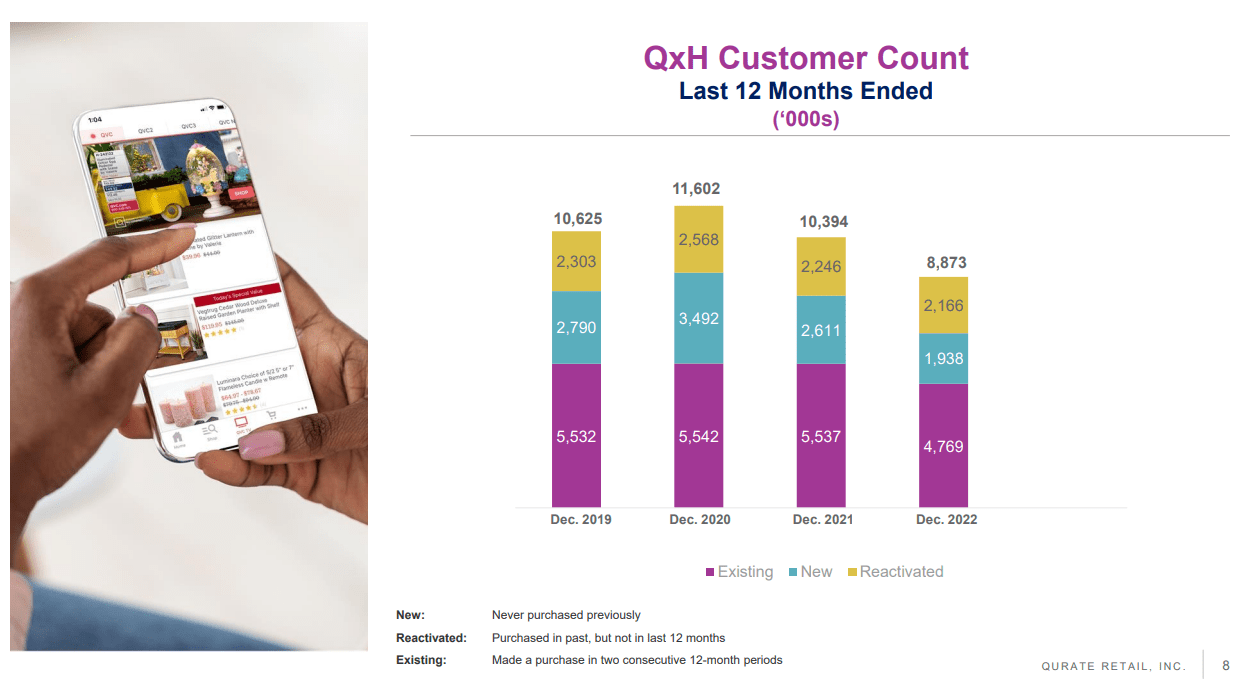

One metric to track carefully is customer count. One of the core arguments for owning the stock is their loyal customer base, and that took a direct hit in 2022 as they worked through stale inventory:

{kind=link}

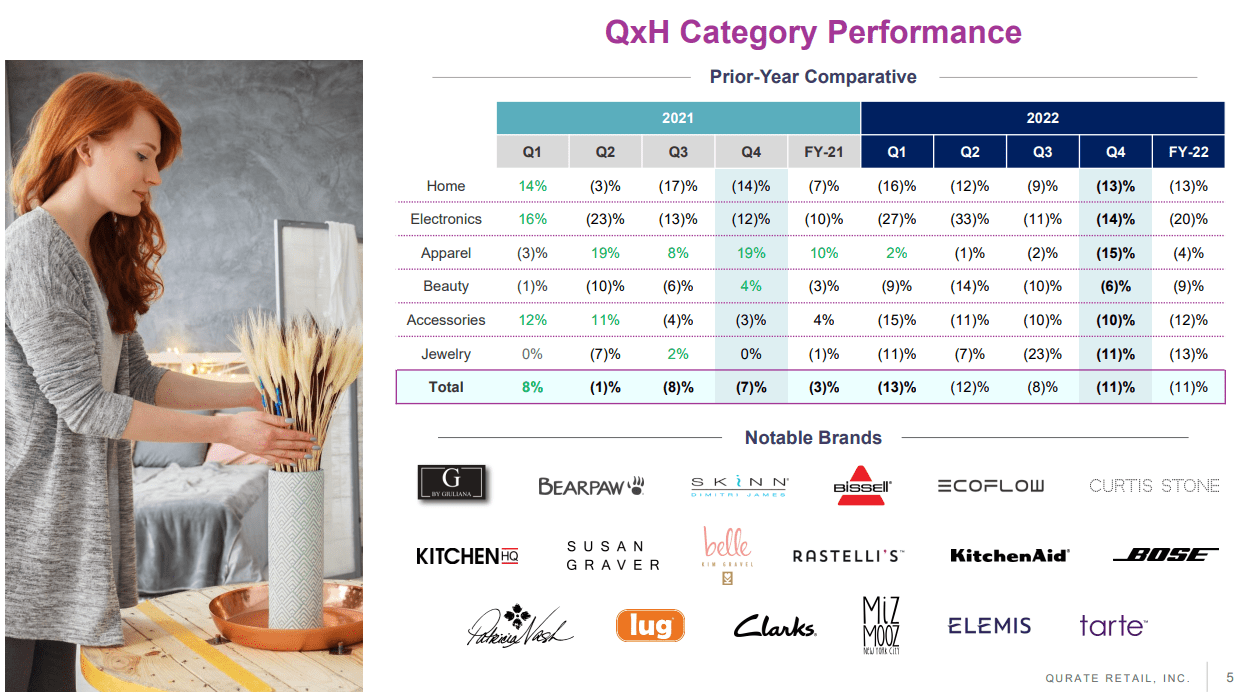

Investing in Qurate requires faith in their ability to regain the lost customers. Given cord-cutting being cited as the primary source of lost customers, I have significant doubts this metric will fully recover, and every key metric is down from pre-Covid times. Qurate does at least seem to have an impressive moat, after fending off attempted entry by Amazon (AMZN) in under a year . Current performance is brutal across categories, providing little hope that the retention issue is contained to a subset of customers:

{kind=link}

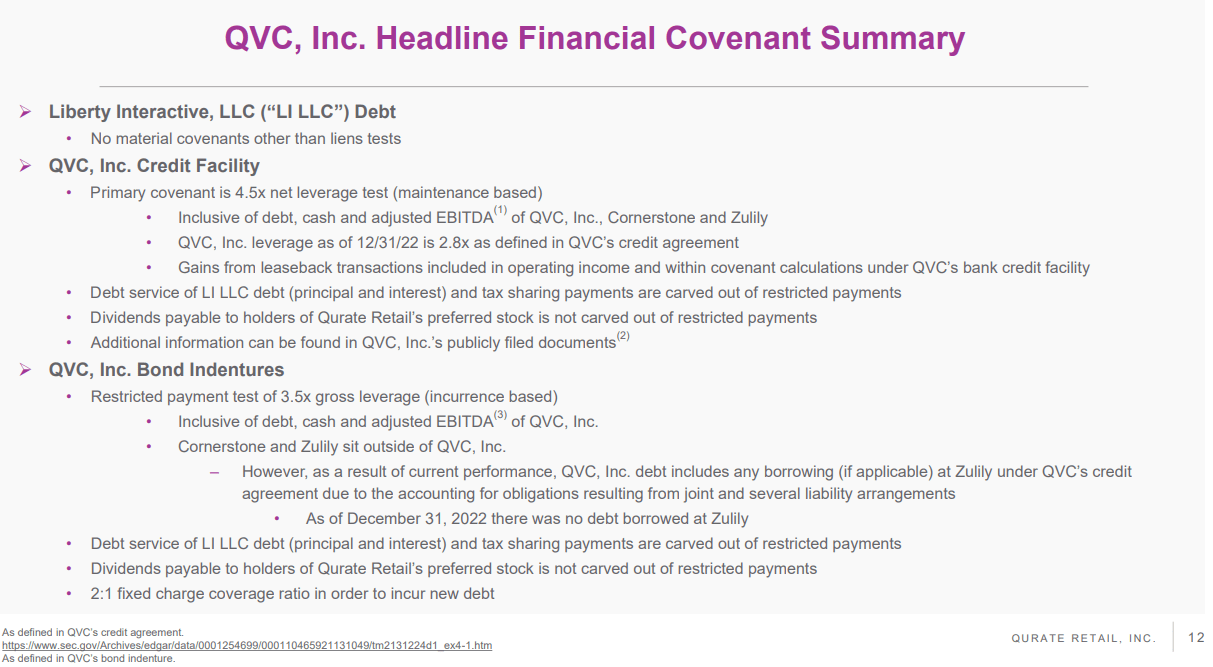

Covenants

Qurate noted in their release that sale-leaseback transactions are allowed as part of their debt covenant calculations. This is particularly concerning, as these were significant one-time gains that will roll off over the next year, and without these gains it appears Qurate would trip covenants, including the key 4.5x covenant on their credit facility:

{kind=link}

They have used up about $1B of the $1.4B of total allowance under the credit agreement, after which this lever will be exhausted for leverage ratios. If business prospects improve, these gains may no longer be necessary, or waivers may be obtained in the event that recovery begins to meaningfully progress.

Brand Sale?

One option Qurate may evaluate would be the sale of Zulily, which has been a drag on earnings, and revenues have declined 45% since 2020. With $906m of sales and a $97m adjusted loss in FY22, I’m not sure how much they would be able to get for the brand, but at the current time it remains a drag on cash. Given they paid $2.4B to acquire the brand in 2015, a sale today would conclude significant value destruction.

Divesting Cornerstone’s $1.3B of 2022 sales and $78m adjusted earnings may also be an option for reducing leverage. It was acquired along with the HSN brand in 2017 for an implied $2.6B . A transaction would likely result in reduced leverage, but also the loss of an asset near trough valuations that could reduce future Qurate upside.

Possible Future Outcomes

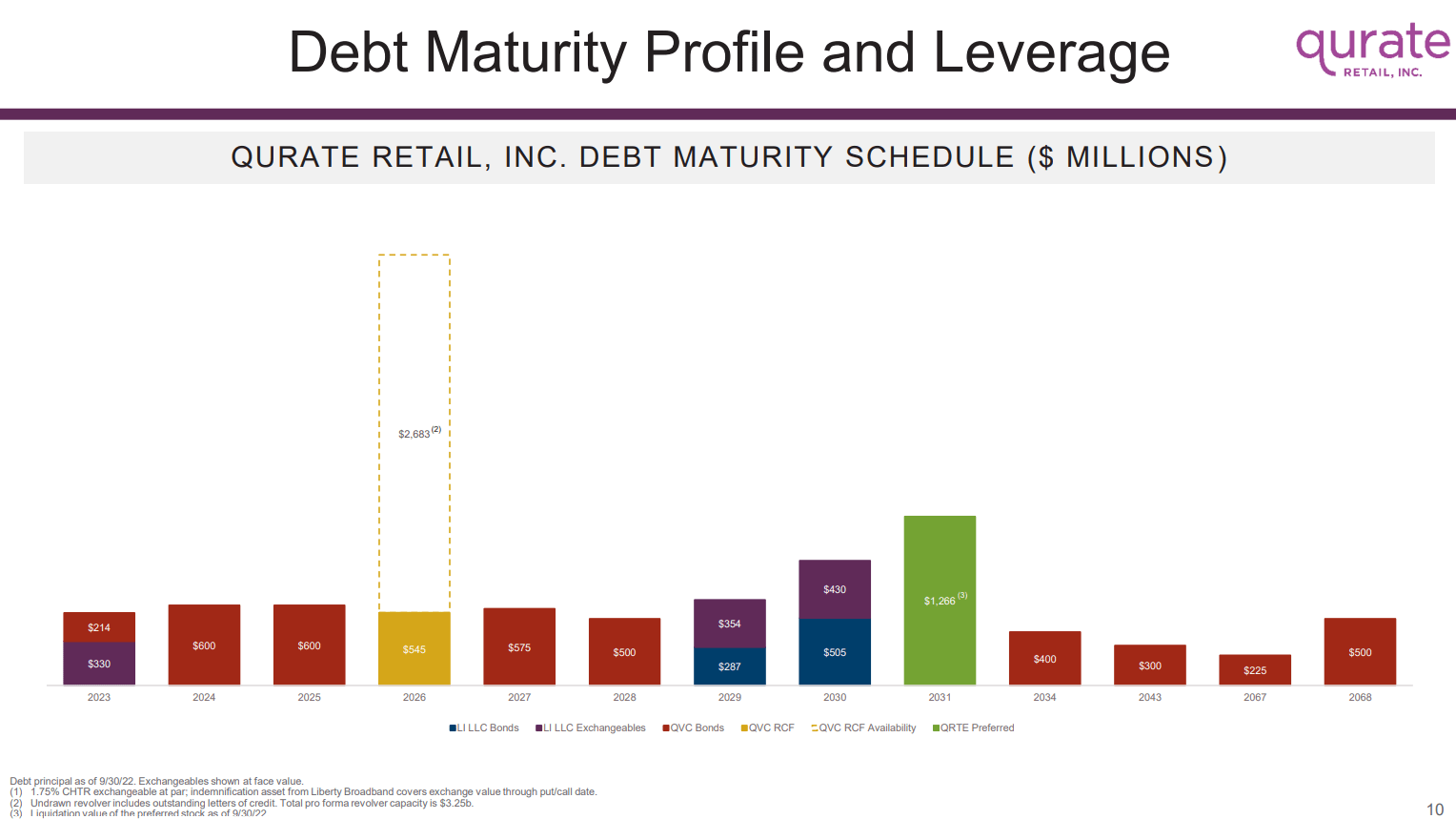

Upside : Project Athens works, Qurate threads the needle on debt covenants, and by 2024 they are earning $500m FCF. Bond maturities are fairly well staggered, with over $4B of bonds and preferred not due until 2030 or later, and $2B of credit available on their facility if they can maintain compliance. Hundreds of millions could be received from business interruption insurance. With the business recovered, Qurate can buy back some debt at discounts, refinance near term maturities, and get back to stock repurchases with any residual cash (over $6B spent since 2013). $500m of FCF on top of a $8B EV remains precarious but the equity yield is over 100% on today’s trading price. I don’t expect shares exceed $10 the way they did when the business consistently cranked out $1B of FCF per year, but $5-$8 in 2024 seems reasonable in this scenario. Significant cash seems likely to be devoted to deleveraging before shareholder returns become material, given the step up in future interest payments if they are refinanced at current rates.

Base : In a more middle-of-the-road outcome, Qurate sells some more assets or brands to stay afloat, but most cash flow is eaten up by heavy interest expense and CapEx requirements. Business is still alive in two years but significant questions exist about how they can refinance debt maturities as they roll in. Shares likely trade higher than today but continue to price in significant bankruptcy risk. Bonds probably do well as they are slowly paid off and rolled forward.

Downside : The bad outcome is obvious – Qurate drowns under its mountain of debt. Stock and preferred holders likely get no recovery if they file, but bonds should see significant recovery given the business value sans leverage. Will Liberty inject enough cash to maintain control out of bankruptcy, or let lenders try to operate or sell the business?

Liberty Backstop??? Therefore a fourth outcome should be considered, where Liberty wants to avoid a bankruptcy filing in their “family”, and orchestrates some sort of buyout or recapitalization to stabilize Qurate. The core business has significant value and a loyal core customer base, but maybe not enough to justify the current EV. If additional capital injection can set up Liberty to benefit from stabilization, they seem well-incentivized to do it. This scenario still may not work out well if you’re buying today – Liberty might let things get worse before they get better, and only inject cash at a significant discount to the face value of debt and preferred securities or buy new equity at a material discount.

The Trade

I don’t own any pieces of Qurate at this time (long or short), and plan to watch for signs of recovery before wading in. The QRTEP issue seems least attractive, when bonds trade at higher yields . Buying the equity seems like a rather binary bet with possible multi-bag upside, but I doubt the market quickly rerates them again as they are forced to begin rolling debt into more expensive issues. I don’t know how much of the deterioration in 2022 remains salvageable.

I think the most interesting trade is buying QVC bonds – some of the maturities this decade offer > 20% yield to maturity . The QVCC/QVCD issues yield double digits as well but represent significant bets on long-term interest rates on top of bets about Qurate’s future. If you buy the 2027 issue and the business survives, you clip a nice coupon while doubling your purchase price in 4 years. Qurate still appears to have $1B+ of EBITDA power, suggesting bonds would be well covered in bankruptcy.

I don’t feel great about a long/short trade here, given the underlying business could recover and have an outsized benefit to the equity versus the debt, and Liberty could inject a lifeline at any time. If I had to short something it would be the preferred stock.

Conclusion

Qurate has been decimated by a combination of poor capital allocation and bad luck. Now selling off real estate to avoid default, it remains to be seen if they can maneuver quickly enough to avoid a bankruptcy filing. Their bond prices suggest disaster is imminent. On the other hand, Liberty has deep pockets and may choose to throw a lifeline. Bonds yield double-digits and seem like the best way to play an expected recovery with decent coverage if they have to file.

For further details see:

The Curious Case Of Qurate Retail