ARGO - The E&S Market Star: Kinsale's Success Story

2023-10-12 08:16:54 ET

Summary

- Kinsale operates in the thriving Excess & Surplus (E&S) insurance market, which has historically outpaced the Property and Casualty (P&C) segment in terms of growth.

- Kinsale exhibits efficient operations, strong underwriting, and prudent credit quality, leading to exceptional returns on equity.

- My primary concern lies in Kinsale's steep valuation, which, while justified by exceptional growth prospects, poses a significant risk to investors if not carefully considered.

Introduction

A wise man once said that change is the constant in life.

Change in our personal lives, change in the world around us, change in the market, and change in our investment strategies. Change is all around us, all the time.

Perhaps as a response to this, there is an ever-present demand in the market for companies that provide both stability and growth.

Can an investor really get both? Fantastic growth and a modest debt load?

I believe they can.

Enter Kinsale Capital Group (KNSL) with its modest 18.5% debt-to-capitalization ratio (as of June 2023), and best-in-class growth rates. This is an insurance company that has carved a lucrative niche in the Small Account Excess and Surplus (E&S) market, specializing in handling hard-to-place risks with in-house underwriting expertise.

However, what truly sets Kinsale apart is its extraordinary growth trajectory and conservative debt management, offering a compelling investment opportunity that warrants a closer look… Especially in light of their phenomenal stock performance, having delivered total returns of over 600% in less than 5 years.

Context: Thriving in the Lucrative E&S Market

First, for you to understand why Kinsale wins, let's examine the industry it operates in, the E&S Market (Excess & Surplus). E&S represents a specialized insurance market that fills the gaps where standard carriers hesitate to tread, addressing a wide spectrum of challenging or high-risk exposures, from mobile homes and daycare centers to multinational oil companies and everything in between.

In this ever-evolving specialty market, E&S companies must exhibit agility and adaptability to swiftly respond to shifting industry dynamics. A core facet of E&S insurance lies in the in-depth expertise expected from professionals concerning coverages, terms, and exclusions. It's these features which contribute to Kinsale's success as they do all of their underwriting in-house keeping their cards close to their chest, and away from competitors.

{kind=link}

The Excess and Surplus (E&S) market, known for its agility and willingness to underwrite unconventional risks, has historically outpaced the Property and Casualty (P&C) segment in terms of growth. Since 2011, the E&S category has boasted an impressive 10% compound annual growth rate ((CAGR)), whereas the P&C segment has lagged at 4.8%.

In this space, Kinsale holds a mere 0.9% market share, while the largest competitor, Lloyd's, commands a formidable 16.8%. Kinsale's small size and strategic position in the E&S market reflects a substantial growth runway, that is a unique prospect in the insurance landscape.

Efficient Operations and Strong Underwriting

{kind=link}

Kinsale's impressive journey is marked by its exceptional combined loss and expense ratio, which stands at a remarkable 81.1%. To put this in perspective, industry stalwarts like Markel ( MKL ) and Argo ( ARGO ) report ratios of 96.6% and 105.5%, respectively. The lower this ratio is, the more cash flows down to the bottom line for investors. Kinsale's ability to maintain such operational efficiency is a testament to its underwriting prowess and risk management strategies.

Furthermore, Kinsale has displayed an exceptional growth trajectory in Net Premium Written (NPW), soaring at a 40% CAGR from 2020 to 2022, significantly outpacing its second-fastest competitor, ACGL, which recorded a 22% CAGR. This stellar performance underscores Kinsale's remarkable ability to identify and capitalize on market opportunities.

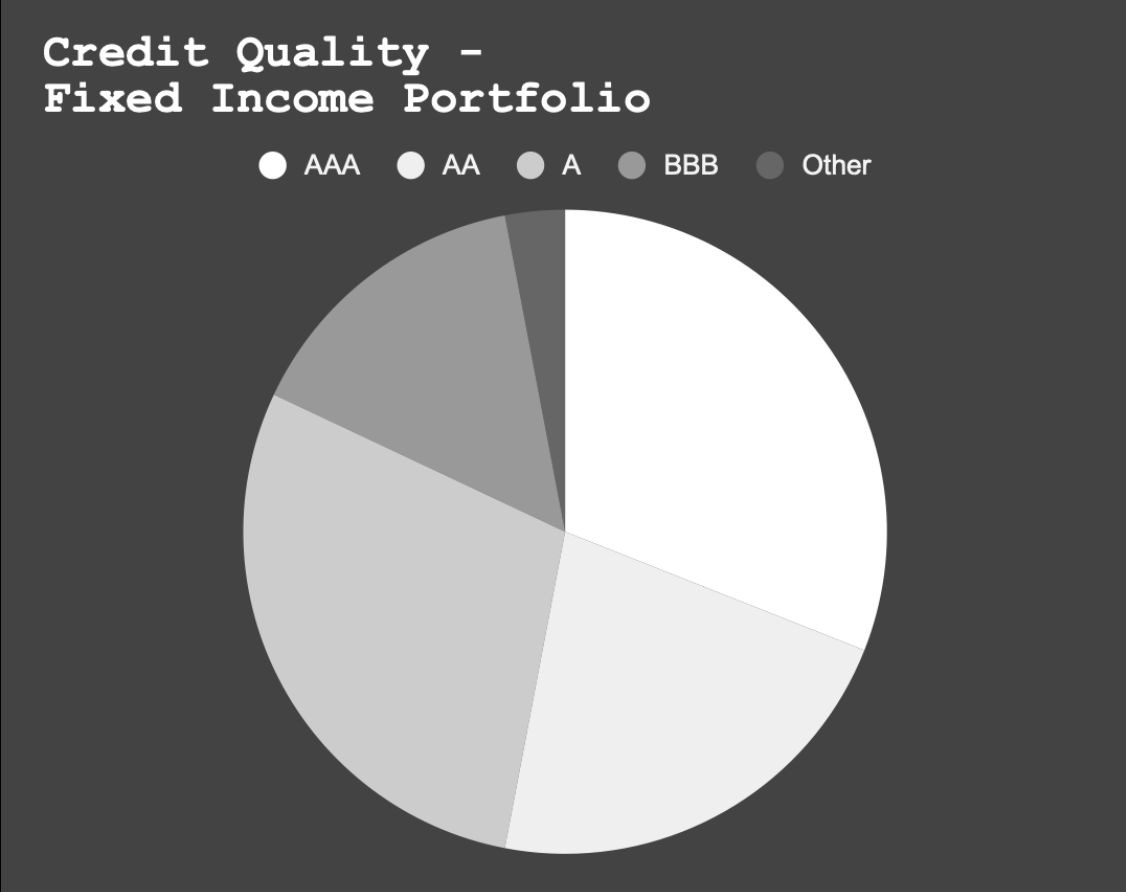

Credit Quality

{kind=link}

Kinsale also prudently manages its investment portfolio, with more than three-quarters of its fixed-income investments allocated to A, AA, and AAA-rated securities. In contrast, the exposure to the risk-laden Commercial Mortgage-Backed Securities sector is a mere 2.5%. As investors grow increasingly concerned about corporate debt and defaults seeing the company manage its debts in such a conservative way is a big plus.

Exceptional Returns on Equity

{kind=link}

Kinsale's journey is further accentuated by its impressive growth in Operating Returns on Equity, surging from 15.4% in 2018 to an astonishing 30.6% in the first half of 2023, this speaks to Kinsale's ongoing commitment to efficiency and prudent risk management.

Perhaps unsurprisingly, the improvements in ROE were, in part, driven by increased scale as a large base of growing revenues has helped to improve efficiency over time at many organizations.

Looking back to 2016 the company had revenues of just around $150M and earnings per share were just a mere $1.50... Boy have things changed!

The company now generates almost $10 in earnings per share annually and revenues just crossed the $1B mark, what's more is that revenues and EPS growth appear to be accelerating, not slowing down as analysts are forecasting an EPS of $14.09 for 2024.

And beyond that, there may still be a long runway for growth ahead...

Looking Forward: The Changing Landscape of the Insurance Industry

The insurance industry is in the midst of a profound transformation, catalyzed by a range of external risks that are increasingly shaping its dynamics. Among these risks, viruses and infectious diseases have taken center stage, with the COVID-19 pandemic serving as a stark reminder of the importance of comprehensive coverage.

Insurers are grappling with the need to adapt quickly to emerging risks, and the ability to underwrite and respond to novel threats is now a pivotal success factor in this evolving landscape.

{kind=link}

Geopolitical tensions have added another layer of complexity to the insurance sector. As the world witnesses shifting alliances, trade disputes, and political instability, insurers find themselves navigating uncharted waters. This volatility can significantly impact the financial stability of insurance companies, necessitating a reevaluation of investment strategies and risk assessments.

NOAA

But the challenges keep coming. The insurance industry grapples with a significant, ongoing issue: how to assess the risks associated with climate change. As we see a rise in the number and intensity of natural disasters, including hurricanes, wildfires, floods, and droughts, insurance companies find themselves dealing with more claims and a growing sense of uncertainty.

But those risks don't impact all insurers equally.

Kinsale's focus on E&S insurance allows them to be selective with the risks they are exposed to and when. While the risks will continue to evolve, Kinsale's small size makes them nimble putting them in a position to be first to market with different insurance solutions.

Valuation

Before I get to the conclusion let's discuss the greatest risk I see facing Kinsale, its valuation.

You see, it's not enough to be a great business, great businesses can lose investors lots of money all depending on the valuation. Does anyone remember Microsoft ( MSFT ) during the dot-com bubble? Investors were deep in the red for years after the bubble burst, yes Microsoft has recovered (and then some!) from the lows of the dotcom crash but it helps to illustrate the importance of valuation. If you buy at the wrong time you can be deep in the red for years to come.

Keeping that in mind let's look at how Kinsale's valuation stacks up. Understanding that much of the reason why Kinsale is valued so highly is due to future growth expected I pulled the future earnings estimates of 2024 for Kinsale along with a number of its peers.

| Company |

| Current Stock Price |

| EPS 2024 Est. |

| 2024 P/E |

| KNSL |

| $443 |

| $14.09 |

| 31.4 |

| MKL |

| $1,487 |

| $93.55 |

| 15.9 |

| ARGO |

| $30 |

| $2.02 |

| 14.7 |

| ( JRVR ) |

| $15 |

| $2.41 |

| 6.1 |

| Average PE (excl. KNSL) |

| 12.2 |

Source: Created by Author using data from Seeking Alpha

As you can see in the chart above, Kinsale has far and above the highest PE ratio among this peer group at 31.4x 2024 Earnings. James River Group on the other hand sports the lowest PE ratio of the group at just 6.1x 2024 earnings. To illustrate the impact these ratios have on the stock prices take a look at the table below.

Created by Author using data from Seeking Alpha

{kind=link}

If you were to apply the valuation of some of Kinsale's peers to its share price its share price would be dramatically cut. In the bear case scenario, applying James River Group's forward PE of 6.1 would imply a share price of $86 for Kinsale. This is not to say that I believe we will see such a drop, far from it, I believe Kinsale has a far superior business model, this is simply meant to illustrate the valuation risk that exists.

Conclusion

Kinsale Insurance's journey through the insurance landscape is indeed impressive. It's a company that has shown exceptional growth, maintained efficient operations, and prudently managed its investments. However, the allure of growth is not without its caveats, and a critical note of caution must be sounded.

While Kinsale has delivered phenomenal stock performance with total returns of over 600% in less than five years, its valuation, in my view, is far too rich. The high price-to-earnings ratio, especially when compared to its peers, raises concerns. Although Kinsale's growth trajectory is stellar, the market appears to have already priced in a considerable amount of that future growth.

Considering the exceptional growth and conservative debt management, Kinsale's shares are undoubtedly tempting. However, the rich valuation is a significant factor that must be weighed against the company's pluses.

Therefore, for prospective investors, I would recommend a cautious "Hold" position, keeping a keen eye on valuation metrics and future developments. It's a company with substantial potential, but its current price might not fully align with the realities of the market.

For further details see:

The E&S Market Star: Kinsale's Success Story