IEI - The Fed Has To Solve The Problem It Created

2023-04-11 13:18:35 ET

Summary

- The Fed was quick to keep rates near zero when the pandemic struck. However, it made a mistake to see inflation as transitory and kept rates low for too long.

- As a result, the Fed needed to raise rates at an aggressive pace and magnitude to keep inflation within its target.

- Due to the low rate environment after the Great Financial Crisis, the financial markets and the economy were not ready for such an aggressive hiking of rates.

- That has resulted in unintended consequences like the regional banking saga and increasing the likelihood of a recession.

- The Fed needs to solve the problem it created with all the tools it has.

In this article, I highlight how the Fed's actions before the pandemic, during the pandemic and after the pandemic have resulted in unintended consequences. As a result, the Fed needs to use all its tools to solve the problems at hand, including elevated inflation levels, rising risk of a recession and the regional banking turmoil we see today.

Before the pandemic

As can be seen below, after the Great Financial Crisis, the Fed kept rates low for almost a decade, raising them for a short period of time before the pandemic struck and the Fed needed to cut rates once again.

Federal Funds Effective Rate (St. Louis Fed)

{kind=link}

This low interest rate environment encouraged risk taking. Specifically, when interest rates are kept low for extended periods of time after the real economy has made considerable progress and recovery can lead to problems down the road.

The pandemic happened

As a result of the unprecedented Covid-19 pandemic that saw restrictions globally, the Fed took actions to ease monetary policy by once again reducing rates.

However, the Fed kept interest rates low for a rather long period of time, preferring to ensure that an economic recovery was well underway before they started to consider hiking rates. As a result, the Fed kept benchmark short-term rates pegged near zero and continued to buy treasury and mortgage bonds to control longer-term borrowing rates.

However, as a result of keeping rates low for the most of 2021, inflation started to rise and reach elevated levels. Despite this, the Fed made its call that inflation was transitory , which was probably one of the mistakes that the Fed made during the Covid-19 pandemic.

At the end of 2021, the Fed turned hawkish as the term transitory was no longer used for inflation and the Fed started to see the need for rate hikes.

One of the most aggressive rate hikes ever

As a result of its mistake on seeing inflation as transitory, the Fed had to hike rates at an accelerated and aggressive pace.

In 2022, we saw the Fed Funds Rate rise from 0.25%-0.50% to 4.25%-4.50% in December of 2022. Today, it stands between 4.75% to 5.00%.

From one mistake, the Fed has potentially made another as the financial markets and the real economy have not experienced such aggressive and rapid rate hikes in more than a decade. There could be unintended consequences as a result of the fast pace and magnitude of the rate hikes we have seen in 2022 and 2023.

Weakening economy in the US

We are increasingly seeing weakness in some important leading indicators. The ISM new orders less inventories fell below 0 while the ISM manufacturing PMI composite index fell below 50 . As a result of the falling new orders and rising inventories we are seeing, this is a leading indicator that we could likely see a manufacturing downturn later in 2023.

US new orders less inventories predicting ISM downturn (Bloomberg)

At the same time, young, unprofitable companies are still struggling and could struggle even more as liquidity in the market tightens. These are the very companies that continue to have large and increasing negative free cash flows. They have also suffered severe multiple contractions on their valuations and some of these companies with unsustainable business models could reduce spending or even go out of business, resulting in a worsening economic scenario.

Increasing net losses of young unprofitable companies (Factset)

Adding to the difficult conditions, we have seen lending standards increase in both the US and Europe. Some experts refer to the sudden decline in US banking system loans in the week ending March 29 as "the largest decline ever". Most of the weakness was driven by commercial real estate lending and commercial and industrial lending. Based on the tight credit standards we see today; the US and Europe are seeing credit standards rising to levels seen in the 2001 and 2008 recessions.

Tightening of lending standards in US and Eurozone (Bloomberg)

Last but not least, as a result of monetary policy tightening globally as part of efforts to combat inflation, this is adding to the risk of a recession in the US in 2023. As can be seen below, apart from China, money supply is contracting everywhere else. With restrictive money supply in the US down to levels not seen in the past two decades, this drastic decline in money supply in the US is adding to risks for businesses in the US in 2023.

Global M2 money supply growth: China is an outlier (Bloomberg; JPAM)

In the ten years after the Great Financial Crisis, the US saw negative real rates and 10-year US treasury yields at less than 1%. In just two years, the Fed's balance sheet doubled from $4.5 trillion to $9 trillion as a result of the Covid-19 pandemic.

Banking sector turmoil

One unintended consequence of the Fed's monetary policy was the turmoil we saw in the US regional banking sector.

First, the Fed flooded the market with liquidity in the Covid pandemic period, resulting in huge deposit inflows to banks. As banks were flushed with more deposits, they also had more problems as unrealized losses on securities and loans led to lower capital ratios.

More money, more problems: Decline in pro-forma capital ratio due to unrealized losses on securities and loans, % (JPAM, Bloomberg)

Second, as a result of the Fed's aggressive rate hikes, banks saw significant unrealized losses on their securities as a result of the higher interest rate environment. After taking into account the unrealized losses on securities and loans, we can see the impact of this adjustment on capital ratios below.

Impact of unrealized securities and loan losses on capital (JPAM, 10K reports)

One trigger is all it takes for deposit concerns to rise again

Unrealized losses on bank balance sheets have never really been a problem.

This is because as long as these losses are unrealized, they are not deemed a threat to the US financial system.

However, in the Covid pandemic period when the Fed eased monetary policy drastically and resulted in excess liquidity in the markets, this happened at a time of low interest rates. As a result, banks that had an influx of deposits from stimulus invested those deposits at low rates, resulting in low yielding assets. When the Fed decided to raise rates rapidly, these low yielding assets, especially the ones with longer duration, experienced significant unrealized losses.

These unrealized losses on securities are not a problem usually, unless there are large deposit outflows, which was deemed to be a low probability event. As we all know now, when panic enters the financial and banking system, a low probability event could happen and the banks least prepared for the deposit outflows are the ones that will suffer the most.

However, when a bank run happens to one bank, the entire financial system is at stake. As a result, we saw one of the largest drawdowns in US commercial bank deposits since 1970.

Drawdown of US commercial bank deposits ( Bloomberg, JPMAM)

The chart below shows the pace of drawdown. As can be seen, since the middle of March, the pace of this drawdown has slowed. At the peak in the middle of March, 1% of system deposits fled in just one week.

Change in drawdown of US commercial bank deposits ( Bloomberg, JPMAM)

The Fed implemented new rules for the Discount Window as a result of the banking turmoil. It will allow banks to borrow against securities at book value rather than market value, which will help banks with any liquidity issues they may have in the short-term when the market sentiment is poor.

The chart below shows the bank borrowing from the Fed. It spiked in earlier March at the peak of the banking saga. Since then, the Discount Window and Bank Term Funding Program borrowing has stabilized.

Bank borrowing from the Fed (Bloomberg, JPMAM)

While the Fed can do this much in helping improve liquidity for the banks, there continues to be a large part of the bank balance sheets that have unrealized losses. Furthermore, the trend of deposits leaving banks for higher money market fund yields is also posing a threat to the US banks.

Federal Home Loan Bank borrowing also shows a similar trend. The peak borrowing activity was in the middle of March at the peak of the regional banking crisis. The borrowing has since declined from the peak and stabilized.

Federal Home Loan Bank daily debt issuance in 2023 ( Bloomberg, JPMAM)

One of the biggest winners of the banking saga has to be the Money Market Funds. These funds have seen large inflows although there are signs that it is slowing. Balances at Money Market Funds reached a new high at $5.2 trillion , with $348 billion of inflows since the SIVB failure.

At the same time, there is still a large gap between deposit rates and money market fund rates. This will bring greater risk to deposit outflows in banks if the gap continues to persist.

How you can invest your cash (Crane Money Fund Data, Bankrate.com , JPMAM)

While many system indicators and financial metrics seem to indicate that the situation is stabilizing, all it takes is one bank to announce bad news and the entire financial system could be at stake.

Final thoughts

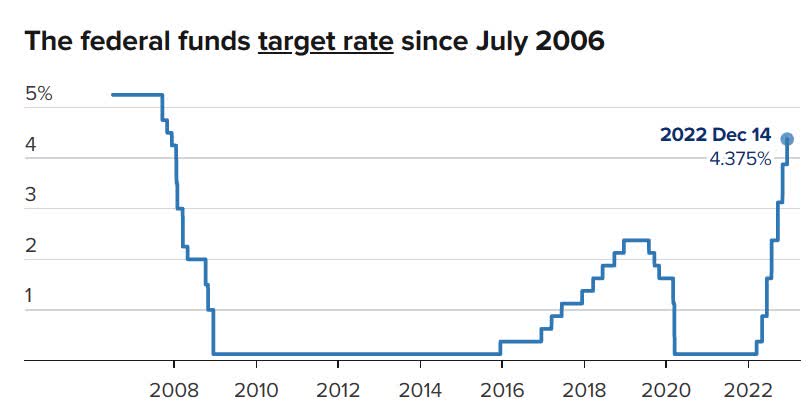

The Fed aggressively increased rates in 2022, with rates rising from 0.125% in early 2022 to 4.375% at the end of 2022. This rapid increase in rates is unprecedented and could have severe unintended consequences along the way, including the regional banking saga we saw earlier in March 2023.

The federal funds target rate since July 2006 (CNBC)

{kind=link}

The Fed is in a difficult position. As a result of its actions taken in the Covid-19 pandemic that resulted in easy monetary policy, this has also contributed to the elevated inflation levels we see today. As a result, on one hand, it has to bring inflation down to its target of 2%, which will mean they need to keep rates high for longer in order to see inflation normalize. On the other hand, it needs to do a fine balancing act as the regional banking turmoil, higher lending standards and weakening economic data are pointing to a recession.

The Fed needs to solve the problem it created with all the tools it has.

For further details see:

The Fed Has To Solve The Problem It Created