QQQ - The Fourth Quarter Gets Underway. Here Are My Thoughts

2023-10-14 09:01:45 ET

Summary

- Volatility in the market has increased, leading some investors to consider moving to cash.

- Professional analysts' opinions often reflect market moves that have already happened, providing little value to retail investors.

- Municipal bonds have suffered recently, but there may be value in the sector due to attractive income and declining supply.

- Both the Tech sector and small-cap US stocks present investment opportunities due to their valuations - for different reasons.

Main Thesis/Background

The purpose of this article is to take stock of the current market environment and to give my macro-level thoughts. There has been a definite uptick in volatility recently, with a number of "down days" strung together. While we ended last week on a high, the past few weeks have likely given investors some pause. With cash paying high yields (compared to the last fifteen years) it may be crossing the mind of many to start to shift to the sidelines.

To be fair, I would always advocate for investors to balance their portfolio in a way that doesn't leave them stressed out. If moving to cash is going to help you sleep better - then go ahead and do it - especially when you can earn 5% in the interim. But running to cash when markets get more volatile is usually not a winning trade. In that mindset, I am going to examine a few areas that have piqued my interest and our subscribers may also find interesting.

Ignore The Noise: Professional Analysts Don't Have Your Back

To start this review I want to take a moment to comment on why followers would be wise to stay disciplined, stick to their plan, and not to make sharp moves based on headlines or analyst "projections". While this may sound odd coming from a writer on Seeking Alpha - this is not my profession. Yes, I work in Financial Services, but my primary function is in funds management and not stock analysis. I write here for the enjoyment and to test my investment thesis for my personal investment accounts. So I do not consider myself a part of the "professional analyst" ranks.

And - quite frankly - I view that as a positive. This is because when analysts go on CNBC or make some "upgrade" or "downgrade", it is not with your financial health in mind. Beyond that, the professional's public statements don't tend to have the best track record. What generally happens is: the market (and any other stock / sector / investment idea) makes a move in one direction or the other and then the analysts pile in with their "new" opinions that simply reflect the move that has already been made.

To see what I mean, let us look at strategist forecasts for the S&P 500 and compare that to the actual performance of the S&P 500. A quick look over the past two years shows that the S&P 500 will move and then after that happens the forecasts will shift in the same direction. Not very productive, as you can see:

S&P 500 vs Analyst Targets (Bloomberg)

{kind=link}

The takeaway for me is that all these "strategists" does is simply play catch-up.

Fair play, in a way. But what value does this provide to you - the retail investor? Not much, if anything at all. That is why I am emphasizing not to pay too much attention to national media headlines or bank strategists that come on TV. Their opinions do tend to pan out, and it is better for us retail folks to stick to our own plan regardless of what the professionals are promoting on any given day.

Munis Were Doing Okay Until Recently

As my followers know I tend to shy away from the bond market - with some exceptions. One of those exceptions is municipal debt. As a working professional in an above-average tax bracket, I generally see more value in munis than in other IG-rated credit. This has made this (and cash) a staple of non-equity portfolio.

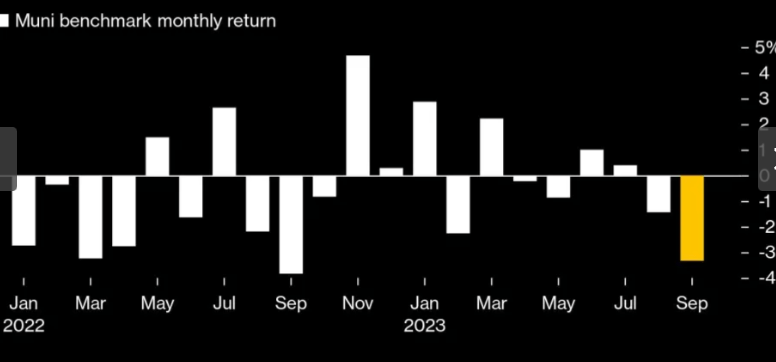

This has served me well during my investment career but - unfortunately - that hasn't been the case in the short-term. After a rough 2022, the new year started out as a refresh. But with inflation and interest rates remaining persistently high, munis have suffered along with the rest of the fixed-income market. Until September, performance had been modestly positive, but last month's loss wiped-out most of that positivity:

Muni Performance (monthly) (Yahoo Finance)

{kind=link}

It would be easy for me to say "munis are down, buy the value here". But I'm just not so sure at this juncture. Fixed-income assets rallied on the prospect that the Fed was nearing its peak and may start cutting rates in 2024. After last week's strong jobs report, that outlook is certainly in doubt now:

September Jobs Report (US Bureau of Labor Statistics)

My point here is that readers should take the "opportunity" in the muni sector with a grain of salt. Its been a disappointing year or year and a half, and more volatility could be forthcoming. I am not one of those "back of the truck" or "buy hand over fist" authors. I never pump any investment idea - even when I'm bullish. We always need to be cognizant of the risks and evaluate them carefully.

That said, it doesn't take a lot of guts to suggest there is indeed some value in munis at current levels. This is based on a couple of very straightforward metrics. One, on a tax-equivalent basis, munis lead treasuries in a big way at the moment (assuming one is in a higher-than-average tax bracket):

Yield Curve Comparison (Clinton Investment Management)

{kind=link}

The conclusion here is that from a purely income perspective munis are attractive.

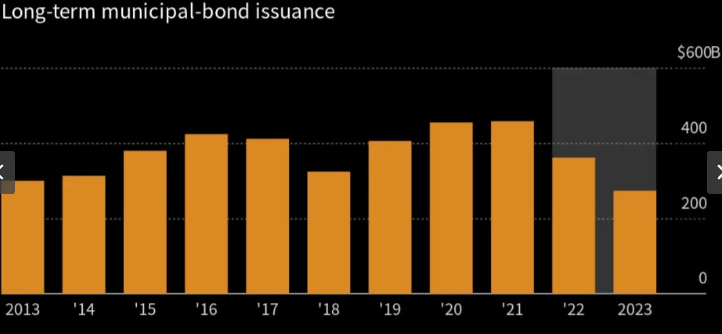

Beyond just the income consideration, there are other favorable dynamics. One is that supply has been declining over the past few years. This coincides with higher rates - as greater borrowing costs are limiting the desire for state and local governments to increase borrowing. While the supply dynamic has not helped munis in the short-term, it is bound to provide some support in the months ahead:

{kind=link}

The conclusion I draw here is that conservative, income-oriented investors could find an argument for buying munis that doesn't take a whole lot of effort. While inflation and the Fed remain headwinds, other attributes are positive. This suggests there is an incentive to buying this sector over other IG-rated bonds, such as corporates and treasuries.

Tech An Opportunity?

An unusual place for some value may be an area that is not suspected. In truth, Tech is not really "value" when compared to the rest of the market. When I say "not really", I mean it is still quite pricey. But that has been the case for years, so avoiding large-cap US Tech because it looks relatively expensive would have been the wrong approach over time.

With this mindset, the recent sell-off in the NASDAQ 100 (which is heavily exposed to the Tech sector) has put the index closer to its 10-year average in terms of forward P/E. The theme of 2023 had been that the NASDAQ's rise was sending valuations soaring. Now, the mini-correction in the index has brought the valuation back down to earth:

NASDAQ 100 Forward P/E (Bloomberg)

{kind=link}

From a pure valuation perspective, the NASDAQ 100 does not look overpriced here. This is not an exact science. When a valuation is attractive is partially subjective, and it is also dependent on actual earnings as opposed to estimated earnings - which is what make up a forward P/E.

The bottom-line for me is that if someone was waiting to build or initiate NASDAQ 100 positions then current levels seem reasonable. They are near the 10-year average and the recent sell-off has narrowed the premium gap between innovative Tech and the rest of the market. This gives me a more bullish take on the sector than just a few months ago.

**I am long the Invesco QQQ ETF ( QQQ ) and the Vanguard S&P 500 ETF ( VOO ), which are both very heavily allocated to the Tech sector.

Consumer Outlook Depends Where You Look

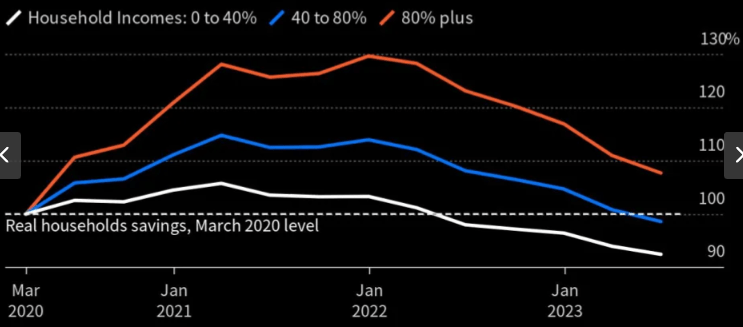

The next topic I will discuss is the have-have not dynamic in the American economy today. What I mean is that the well-off are doing quite well, while those at the bottom are more painfully aware of inflation and a more challenging job market than we saw coming out of Covid initially.

Pointedly, this is a vastly different consumer backdrop than we saw in late 2020 - early 2022. As stimulus wore off and inflation ended up being resilient (rather than transitory), American households have felt the pinch. While there is no way to avoid it, the ultimate impact is not even across income brackets - with lower income households now dipping in to savings to meet expenses:

Accumulation and Draw-down of Savings (By Income) (Federal Reserve)

{kind=link}

This is a challenging backdrop for an investor, especially one looking at consumer-oriented sectors. Is the consumer weak or strong? Hard to say for certain - since it depends on which consumer you are talking about.

In my view, this means investors need to get a bit more creative than just buying a standard or passive retail/consumer ETF that is going to cater to consumers of all stripes based on their diversity. This includes funds like the SPDR S&P Retail ETF ( XRT ) or the Consumer Discretionary Select Sector SPDR Fund ETF ( XLY ). Given the challenging backdrop for many Americans, these are options I would shy away from.

Instead, I would look at individual names that have a global customer base that is more high-end. Many European shares in this sector are reasonably priced, so think names such as Prada ( PRDSY ), Louis Vuitton ( LVMHF ), Burberry Group ( BURBY ), The Swatch Group ( SWGAY ), Kering ( PPRUF ), among others, that are across the pond. Or for those who prefer companies closer to home, think of the likes of Tapestry ( TPR ) and Ralph Lauren Corporation ( RL ). The thought here being that companies willing to charge a premium for their products still have customers at the higher end able to pay for them. That presents an opportunity in what is otherwise a difficult investment climate.

Small-Caps Are Heavily Discounted

My last topic is US small-caps. This could be seen as an odd choice if one expects a recession. But the recession mantra has been pushed for years and has not yet materialized. I'm not suggesting that a recession isn't inevitable at some point - but we shouldn't necessarily be investing today because a recession "might" happen soon. We can react to one if it occurs, but stay committed to a long-term plan for now.

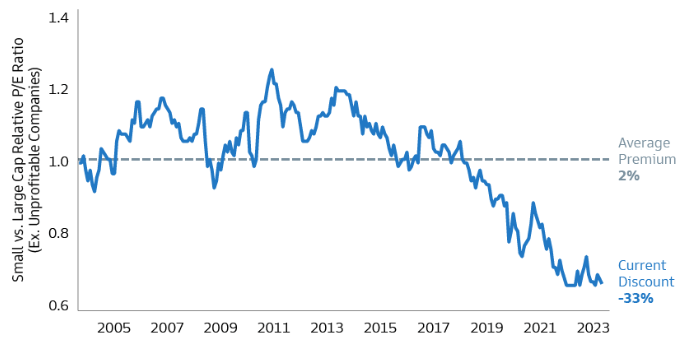

In this light, small-caps have a tremendous amount of value as they have lagged their large-cap peers. I am specifically referring to the US equity market for this example, but the divergence in performance is quite apparent. As a result, small-caps have the widest discount in almost twenty years:

Small-Cap to Large-Cap Relative P/E (Goldman Sachs)

{kind=link}

This looks a bit too appealing for me to pass-up at the moment, so I'm giving small-caps a very serious look given my portfolio is tilted almost exclusively to large-caps.

Further, small-caps can benefit from the strength in the US dollar. While larger companies are more apt to generate revenues and profits overseas, those foreign sales can be worth less when converted to a rising dollar. Small-caps, by contrast, are more geared towards the domestic (U.S.) economy because they are more likely to sell products within their own borders. This helps to insulate them from the loss of competitiveness of a stronger dollar, all other things being equal. Given the recent USD strength, this is an important attribute:

{kind=link}

For these reasons I see a bullish position on small-caps as logical, and it will be something I will take seriously in the coming days and weeks.

**I'd look to ETFs mostly to place this space, such as the Vanguard Small-Cap Index Fund ETF Shares ( VB ), or the iShares Core S&P Small-Cap ETF ( IJR ), among many other options.

Bottom-line

The market can giveth, and also taketh, we must remember that. For those who forgot, September and early October were reminders. But the truth is there is still value in this market, the American economy and job market has been resilient, and a rising USD prevents opportunities as well as challenges - it just depends on whose side you are taking!

In this light, I have covered a few areas that I see continued interest in as we move deeper in to Q4. They may not be right for everyone, and they certainly aren't the only ideas that could generate profits in the last stage of the year. But I think for those who are in need of diversification or quality bonds could benefit from the sectors I discussed here.

For further details see:

The Fourth Quarter Gets Underway. Here Are My Thoughts