QVMS - The January Payroll Report To Confirm An Imminent Recession

Summary

- The leading indicators related to the labor market are deteriorating, signaling an imminent recession.

- Wage growth remains the key inflationary data point to follow.

- The stock market is not priced for the likely recession.

An imminent recession

The record inversion in the yield curve spread (10Y yield - 3M yield) is suggesting that there is a near certainty that the US economy will slip into a recession sometime in 2023. More information on this provided by the NY Fed .

The survey based economic data is suggesting that the recession is imminent. For example, the just released (Fed 1st) ISM purchasing managers' manufacturing index ((PMI)) at 47.4 shows the third consecutive contraction in factory activity, and a sharp downtrend, which usually precedes a recession. Here is the chart:

Trading Economics

However, the labor market shows (on surface) an amazing resilience, and it's difficult for a consumption-based economy to slip into a recession as long as the labor market remains strong. Thus, the January 2023 payroll report will provide the key data with respect to timing of the likely upcoming recession.

The January 2023 labor data expectations

The US Bureau of Labor Statistics will release the employment data for January 2023 on Friday. The consensus expectations are that the labor market will remain tight, but also to continue to cool slightly.

The unemployment rate is expected to uptick from 3.5% to 3.6%, and the total non-farm jobs created are expected to slow from 223K to 185K. The wage growth rate is expected to slow from 4.6% to 4.3%, while the average weekly hours are expected to remain at the 34.3hr/week.

| Consensus |

| Previous |

| Unemployment rate (target 4.6%) |

| 3.6% |

| 3.5% |

| Non-Farm Payrolls |

| 185K |

| 223K |

| Average Hourly Earnings YoY |

| 4.3% |

| 4.6% |

| Average Weekly Hours |

| 34.3 |

| 34.3 |

But the Fed's target is 4.6% unemployment rate

It is important to understand that the upcoming recession will be the Fed-induced recession. Despite sometimes the mixed messages, the Fed needs a recession to bring the elevated inflation back to the 2% inflation target. In fact, the Fed inverted the yield curve for exactly this reason.

In the December 2022 meeting's Summary of Economic Projections the Fed specifically states that expects the unemployment rate to rise to 4.6% in 2023, and stay at that level in 2024, before a slight decline in 2025 to 4.5%.

The Federal Reserve

Currently, the unemployment rate is 3.5%, and the rise to 4.6% in 2024 would require around 2M more unemployed in 2023. It's hard to see how a 2M jobs lost would not cause a recession.

The Bulls' hope

Given the ttm PE ratio at 21.68, S&P 500 ( SPY ) ( SP500 ) is not priced for a recession. In fact, it's pricing an above average growth. The stock market bulls argue that the Fed will be able to bring down the inflation rate - without causing a recession. In addition, they feel the Fed is likely to subsequently lower the interest rates. Thus, is a 1995-type scenario (when the Fed paused the hiking campaign without causing a recession, and subsequently adjusted the rates lower), which resulted in a strong stock market performance.

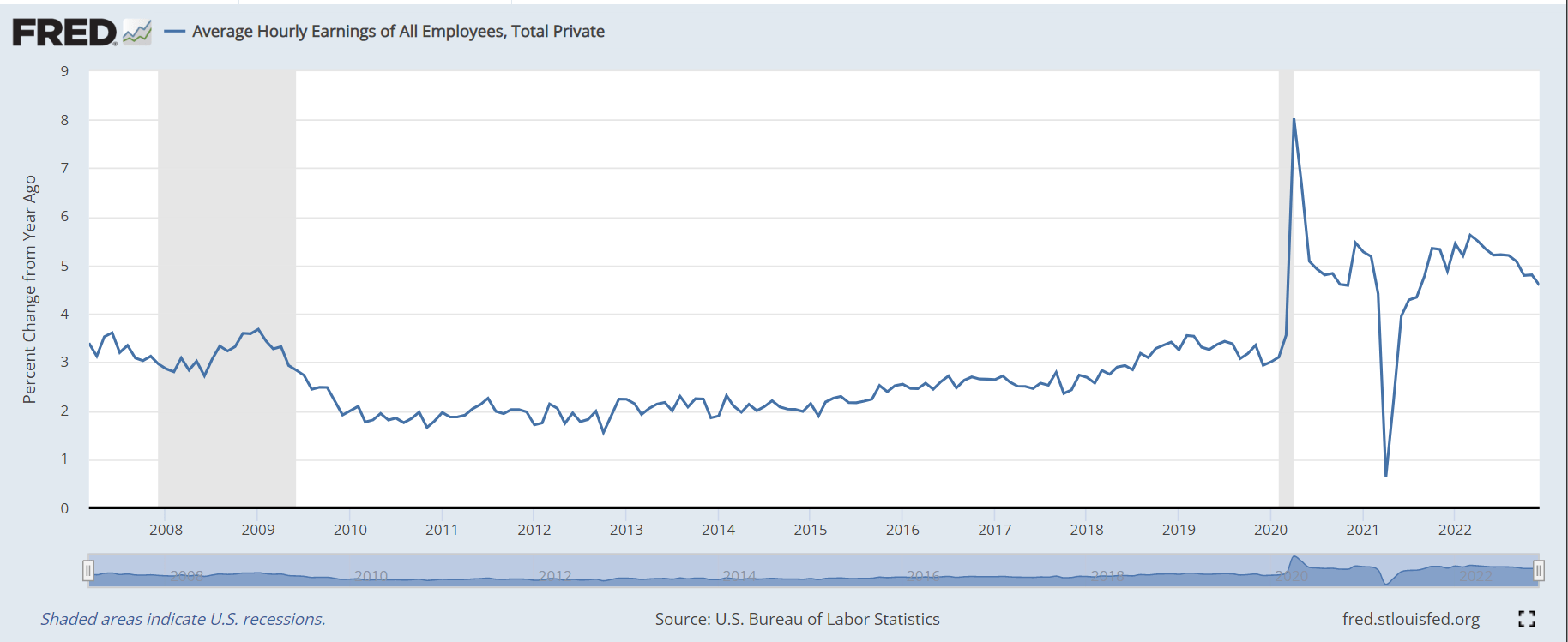

The Fed has been specific in stating that the service inflation continues to be elevated and sticky primarily due to the workers shortage, which is keeping the wages inflation elevated. The wage-price inflationary spiral is the major risk.

The bulls' hope is that the wage growth would somehow decline, without the increase in the unemployment rate, thus without a recession. In fact, the 6% rally in S&P 500 in January 2023 has started with the fall in the wage growth in the December 2022 payroll report.

The consensus expectations are that the wage growth will fall in January 2023 to 4.3%. Thus, this is the key number to follow. Here is the wage growth chart:

{kind=link}

The Bearish reality

However, under the surface, the labor market has already started to contract, and the leading indicators are pointing to the rise in unemployment rate soon.

Specifically, the average number of hours worked has been steadily decreasing from the post-pandemic high of 35 in January 2021 to 34.3 in December 2022.

This is a leading indicator of labor market deterioration, because companies usually cut the numbers worked before actually firing workers. Thus, this is another key data point to follow in the January payroll report. Here is the chart of Average Weekly Hours of all private employees:

{kind=link}

The second leading indicator is the number of all employees in temporary help services. Companies usually reduce the number of temporary workers before reducing the headcount of the full-time employees.

The chart below shows the percentage change over the last 12 months in All Employees as Temporary Workers. As you can see from the prior recessions, the number of temporary workers starts decreasing before a recession - thus, it's considered as a leading indicator. For December 2022, the number of temporary workers decreased by 1.1% from December 2021, which supports the imminent recession thesis. This is another data point to follow in the January 2023 report.

{kind=link}

So, what to pay attention to in the January 2023 payroll report?

Beyond the headline numbers, investors should closely follow:

- The average numbers worked. The number below 34.3 further supports the imminent recession thesis.

- The number of temporary workers. There were 3.0449 million temporary workers in December 2022. This number should decrease to below 3.0114 million to reflect more than 1.1% decrease and confirm the downtrend, and thus, continue to signal an imminent recession.

- Most importantly for the bulls, the wage growth should be below 4.3%, which would signal that the wage growth is falling faster than expected and support the "soft-landing" thesis.

Implication for the stock market

The leading indicators of the labor market already point to an imminent recession. The January 2023 report is likely to continue to support this. However, S&P 500 is not priced for a recession. The PE ratio for S&P 500 based in trailing 12-month earnings is at 21.68, which is overvalued based on historical average of 15-16.

Thus, there is a considerable downside for S&P 500 as the earnings estimates must be downgraded, and the valuation multiple has to contract to reflect an imminent recession.

Note, that the Atlanta Fed GDPNow estimate for 2023 Q1 is at 0.7%.

For further details see:

The January Payroll Report To Confirm An Imminent Recession